2026 Guide to Compliance-First Debt Recovery Strategy for Agencies

Debt Collection & Recovery Software

2026 Guide to Compliance-First Debt Recovery Strategy for Agencies

Published on:

June 29, 2026

Collection agencies are under constant pressure to recover more while staying within tightening regulatory boundaries. Even a small misstep across channels can trigger disputes, audits, or legal action. The CFPB reported 207,800 debt collection complaints, highlighting just how closely the industry is being scrutinized.

If you are managing third-party collections, balancing performance with regulatory expectations is not just challenging; it is exhausting. In this article, we break down how to build a compliance-first debt recovery strategy that helps your agency reduce risk, streamline operations, and improve recovery outcomes.

Quick look:

Regulatory misalignment increases risk. Inconsistent outreach, poor disclosures, and weak audit trails can lead to disputes, failed audits, and legal exposure for agencies handling third-party collections.

Regulation-driven strategies require structured execution. Agencies must move from manual oversight to systems that enforce consistency across workflows, communication, and payments.

Five pillars define effective recovery systems. Decision standardization, lifecycle structuring, channel orchestration, execution control, and traceable operations enable consistent and defensible outcomes.

A modern technology stack is essential. Workflow automation, omnichannel communication, payment infrastructure, real-time analytics, and integration layers ensure control at scale.

System design determines outcomes. Connected platforms with embedded rules and visibility help agencies maintain compliance while improving recovery performance.

What Is a Compliance-First Debt Recovery Strategy?

A compliance-first debt recovery strategy ensures regulatory alignment shapes how agencies operate, not just how they audit outcomes. For third-party collections, this means reducing reliance on manual judgment and building structured, defensible processes that balance recovery performance with legal expectations.

This approach is defined by a few key characteristics:

Pre-Action Rules: Regulatory checks guide actions before execution, reducing the chance of violations at the source

System Enforcement: Standardized processes ensure consistent handling across accounts, teams, and portfolios

Guided Outreach: Communication follows defined rules for timing, frequency, and channel-specific requirements

Proactive Control: Risks are identified and prevented within workflows rather than corrected after escalation

Audit Visibility: Every interaction is recorded with clear traceability for reviews, disputes, and audits

Traditional recovery models were not designed for this level of regulatory complexity. In the next section, we examine the gaps in legacy recovery models as regulatory expectations continue to rise.

Why Traditional Debt Recovery Strategies Break Under Regulatory Pressure

As rules expand across channels and jurisdictions, including requirements under the Fair Debt Collection Practices Act (FDCPA), legacy processes struggle to maintain consistency, control, and defensibility at scale. For collection agencies, these gaps create operational friction and measurable legal risk.

These challenges show up in critical ways:

Fragmented Systems: Agencies rely on separate tools for dialing, payments, and account management. This creates data inconsistencies, making it difficult to enforce rules uniformly across portfolios.

Manual Oversight: Agents are expected to interpret compliance requirements in real time. This slows execution and increases the likelihood of errors that can escalate into disputes or violations.

Channel Misalignment: Communication across calls, SMS, and email is often not centrally governed. Without structured controls, agencies risk breaching timing, frequency, and consent requirements.

Limited Visibility: Interaction histories are scattered across systems, leaving gaps in audit trails. When issues arise, agencies struggle to produce clear, defensible records.

Unscalable Processes: As account volumes grow, manual and disconnected workflows break down. What works for small batches becomes inconsistent and risky at scale.

Tratta centralizes consumer communication, payments, and workflows into a single operational layer, removing the fragmentation that creates compliance gaps. Its configurable workflow engine ensures that outreach, timing, and account handling follow predefined rules without relying on agent interpretation. Request a free demo.

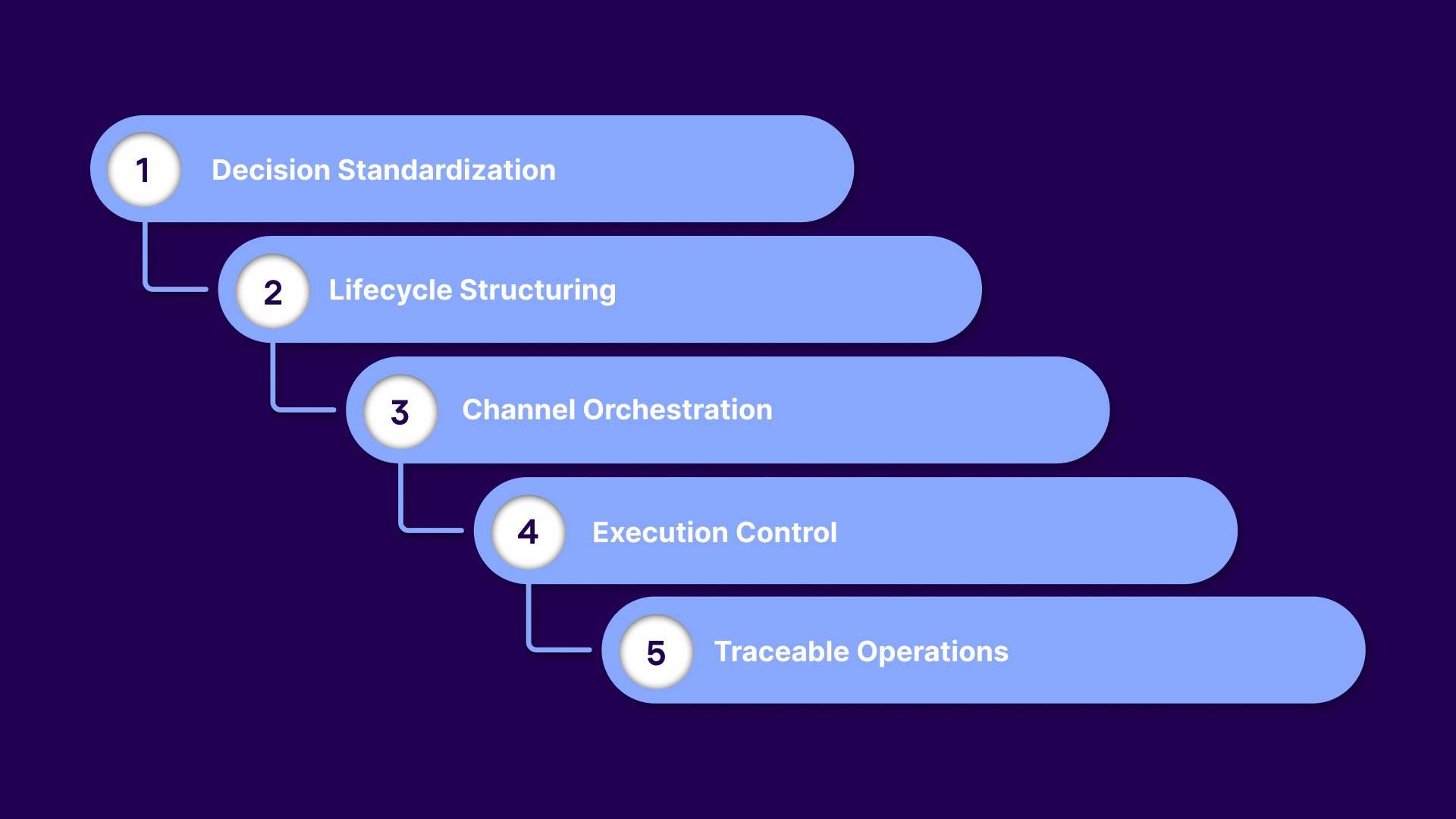

5 Pillars of a Regulation-Driven Recovery Strategy for Agencies

A regulation-driven recovery strategy is defined by how agencies structure control, not just how they avoid risk. These pillars examine how modern recovery systems are designed to operate within regulatory constraints while maintaining performance.

Each pillar reflects a distinct capability agencies need to build:

1. Decision Standardization

Agencies must remove variability from how accounts are handled. Decisions should follow predefined logic rather than relying on individual agent judgment.

This ensures consistency across operations:

Align actions across portfolios and teams

Reduce subjective decision-making

Ensure consistent treatment of similar accounts

2. Lifecycle Structuring

Recovery should follow a clearly defined sequence from first contact to resolution. This creates predictability in both execution and oversight.

This brings order to how accounts progress:

Map actions across the full account lifecycle

Define triggers for each stage

Maintain continuity across touchpoints

3. Channel Orchestration

Outreach should be coordinated across channels as part of a single strategy. Each interaction must fit into a broader communication flow, not operate in isolation.

This keeps communication aligned:

Sequence communication across SMS, email, and calls

Avoid overlapping or conflicting outreach

Maintain continuity in messaging

4. Execution Control

Actions must be governed by systems that enforce how and when they occur. This ensures that scaling operations do not introduce inconsistency.

This creates operational discipline:

Control timing and frequency of actions

Limit deviations from defined workflows

Maintain uniform execution across accounts

5. Traceable Operations

Every action within the recovery process should be fully trackable. This creates a clear record of how decisions were made and executed.

This supports accountability and visibility:

Capture step-by-step activity logs

Link actions to specific workflows

Enable full operational transparency

These capabilities depend heavily on how systems are configured and connected. In the next section, we examine the top technologies that directly impact an agency’s ability to operationalize these pillars at scale.

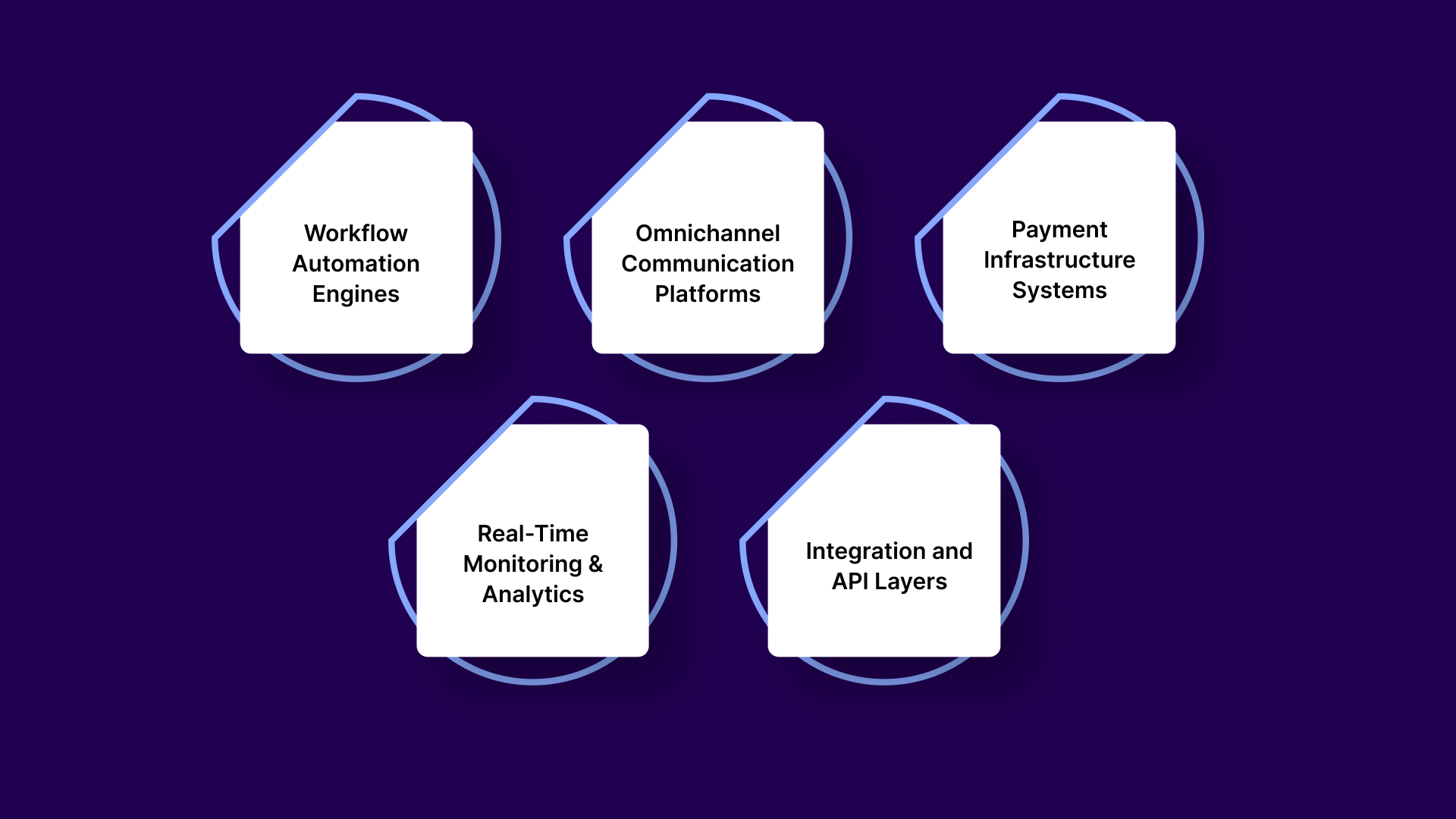

Top Technologies Powering Compliance-First Debt Recovery in 2026

Regulatory alignment at scale depends on whether your systems can enforce structure, not just support activity. For agencies handling third-party collections, the right technology stack determines how consistently you operate and how well you control risk.

Tratta brings these features together by structuring them around execution rather than isolated functions. Its campaign orchestration layer connects workflows, communications, and payments into a single flow, keeping actions aligned across systems. Contact us to learn more.

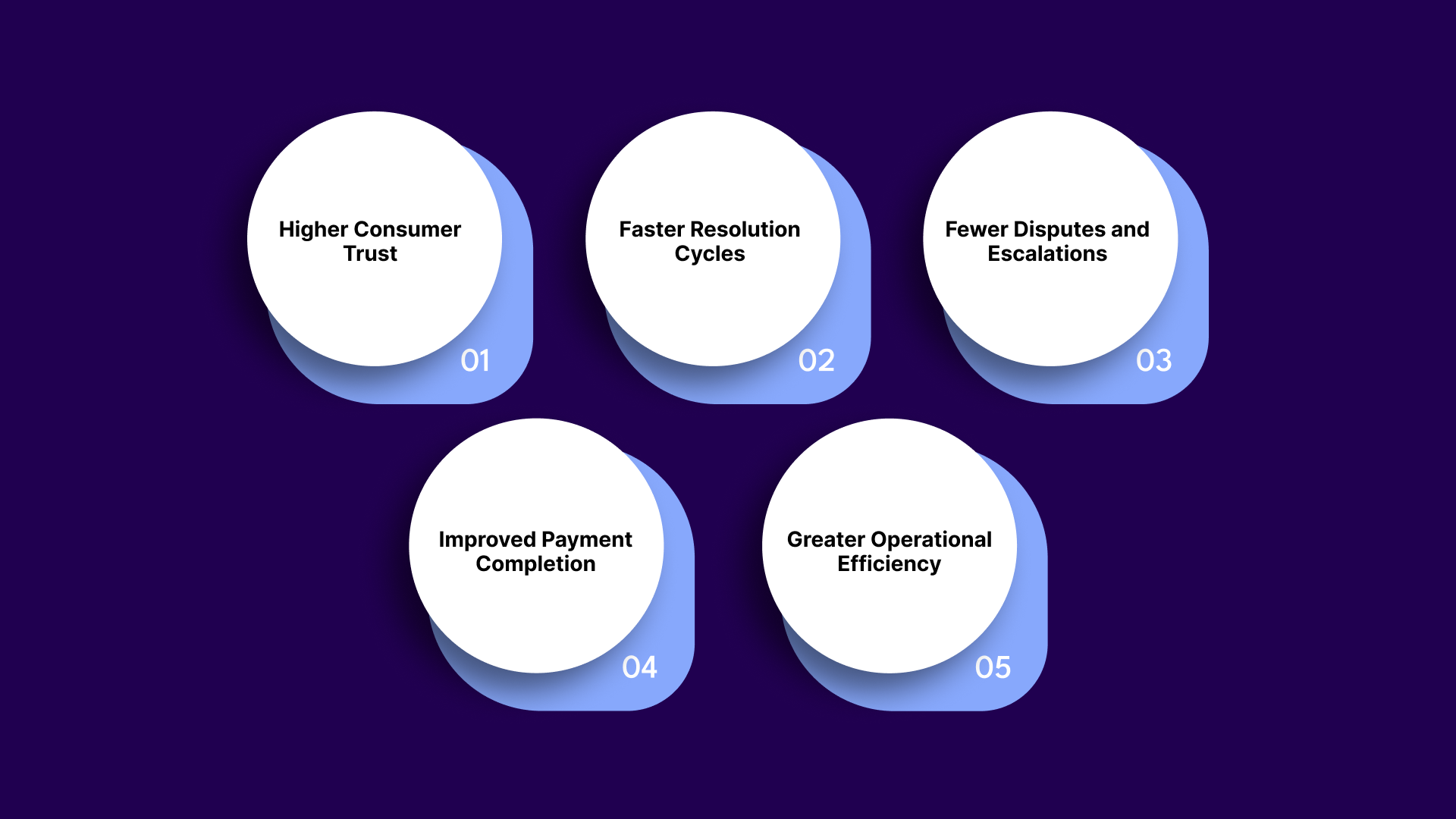

How Regulation-Driven Strategies Improve Agency Recovery Rates

When recovery operations are structured around clear rules and consistent execution, performance improves as a natural outcome. Agencies can reduce friction, build trust, and move accounts through the lifecycle more efficiently without introducing additional risk.

These improvements show up in measurable ways:

Higher Consumer Trust Consistent and predictable interactions make it easier for consumers to engage. This increases the likelihood of response and follow-through on payment actions.

Faster Resolution Cycles Structured workflows reduce delays between steps. Accounts move from first contact to resolution without unnecessary gaps or rework.

Fewer Disputes and Escalations Clear, well-timed communication reduces confusion and conflict. This lowers the volume of complaints that can slow down recovery.

Improved Payment Completion Streamlined processes and better-aligned outreach reduce drop-offs. Consumers are more likely to complete payments once they start the process.

Greater Operational Efficiency Teams spend less time correcting errors or managing inconsistencies. This allows agencies to handle higher volumes without increasing overhead.

While these outcomes are achievable, many agencies struggle during implementation. In the next section, we examine the common mistakes collection agencies make when adopting compliance-led strategies.

5 Mistakes Collection Agencies Make When Adopting Compliance-Led Strategies

Adopting a compliance-led approach is not just about adding controls. Many agencies introduce new rules without restructuring how their systems and workflows operate, which leads to friction, inefficiency, and continued risk.

Here is where most agencies go wrong:

Mistake

What Happens

Impact on Agency

Treating Compliance as a Layer

Rules are applied after workflows are designed

Gaps remain in execution and enforcement

Over-Reliance on Manual Checks

Agents handle compliance decisions in real time

Increased errors and inconsistent outcomes

Disconnected Tool Stack

Systems operate independently without alignment

Poor data flow and weak control over actions

Ignoring Execution Flow

Actions are not sequenced properly across accounts

Delays, overlaps, and consumer confusion

Limited System Visibility

Activity is not tracked across all touchpoints

Weak audit readiness and delayed issue detection

To move past these challenges, agencies need to shift how they structure operations:

Embed rules into workflows instead of applying them after execution

Reduce manual decision-making by standardizing processes

Connect systems into a single flow rather than managing them separately

Structure communication across channels to avoid overlap and inconsistency

Ensure full visibility across actions to support oversight and audits

This shift requires more than process changes. In the next section, we look at how you can bring these elements together into a system that supports consistent, controlled execution at scale.

Turn Compliance-Driven Strategies Into Controlled Execution with Tratta

Tratta is a debt collection platform built to help agencies manage consumer engagement, payments, workflows, and compliance within a single system. It is designed for third-party collections, where regulatory alignment depends on the consistency with which actions are executed across accounts. Instead of layering compliance on top of operations, Tratta structures how recovery actually happens.

Key features include:

Consumer Self-Service Platform Provides a controlled digital environment where consumers can view accounts and resolve balances independently. Standardizes disclosures, payment options, and account actions, reducing variability in agent-led interactions and ensuring consistent, compliant experiences across all consumer touchpoints.

Embedded Payments Integrates payment processing directly into workflows, ensuring transactions follow structured recovery logic. Improves traceability by linking every payment to a defined action, reducing friction while maintaining control over how and when payment options are presented.

Multilingual Payment IVR Enables consumers to complete payments through an automated, multilingual system. Ensures consistent messaging and disclosures across languages, reducing reliance on agent interpretation and minimizing communication-related compliance risks in diverse consumer interactions.

Omnichannel Communications Centralizes SMS, email, and voice interactions within a single system. Controls timing, frequency, and sequencing across channels, ensuring outreach adheres to defined rules and reducing the risk of overlapping communications or regulatory violations.

Campaign Management Allows agencies to design structured outreach strategies across account segments. Ensures communication follows predefined sequences, aligning execution with regulatory expectations and reducing inconsistencies across portfolios.

Reporting and Analytics Provides real-time visibility into account activity, communication performance, and payment behavior. Helps identify inconsistencies early and supports audit readiness through complete, traceable records of all actions and interactions.

Customization & Flexibility Enables agencies to configure workflows, communication logic, and payment rules based on regulatory requirements. Ensures compliance is embedded into system behavior, allowing quick adaptation to changing rules without disrupting operations.

Integrations Connects with CRMs and third-party systems to maintain consistent, real-time data across platforms. Eliminates discrepancies that can lead to inconsistent execution, ensuring actions are based on accurate and synchronized information.

Security & Compliance Incorporates built-in safeguards to support regulatory requirements and protect sensitive data. Ensures all communications, transactions, and workflows operate within a secure environment designed to reinforce compliance through system-level controls.

Contact Center Brings agent interactions into the same system as workflows and communication history. Ensures manual actions follow structured processes and are fully recorded, reducing variability and maintaining consistent, compliant engagement across accounts.

Tratta simplifies onboarding by aligning the platform to your existing processes from the outset. Implementation is guided to ensure workflows, outreach logic, and payment handling reflect how your agency already operates. This allows you to roll out without disruption, maintaining continuity across active accounts while improving operational control.

Conclusion

When compliance is not built into how recovery operations run, agencies face tangible risks. Misaligned outreach, inconsistent disclosures, and incomplete records can lead to disputes, failed audits, and potential legal exposure. As volumes grow, these gaps compound, making it harder to maintain control across third-party collections.

Tratta enables agencies to define and enforce how recovery actions are carried out across accounts, rather than relying on fragmented tools and manual interpretation. With structured campaign orchestration, controlled communication flows, and real-time audit visibility, agencies can maintain consistent, compliant execution at scale.

1. What is the most common violation of the Fair Debt Collection Practices Act?

The most common violations involve improper communication, including contacting consumers at restricted times, using misleading language, or failing to provide required disclosures. Inconsistent outreach across channels is a frequent trigger in third-party collections.

2. What is the 6-year rule in debt recovery?

The 6-year rule typically refers to the statute of limitations for collecting certain debts, depending on state law. After this period, legal action may be restricted, though collection attempts may still be permitted within regulatory boundaries.

3. How can collection agencies reduce compliance risk at scale?

Agencies reduce risk by embedding regulatory rules into workflows, standardizing communication, and maintaining complete audit trails. Relying on manual oversight or disconnected systems increases variability and exposure across accounts.

4. Why is omnichannel communication risky for collection agencies?

Without centralized control, outreach across SMS, email, and calls can overlap or violate timing and consent rules. Agencies need structured communication flows to ensure consistency and avoid regulatory breaches.

5. What role do audit trails play in debt collection compliance?

Audit trails provide a complete, traceable record of all interactions and actions. They are essential for defending against disputes, responding to audits, and demonstrating that recovery processes followed regulatory requirements.

Note: This information is not legal advice. Tratta recommends that you consult with your legal counsel to make sure that you comply with applicable laws in connection with your collection and outreach activities.

Sign up for our monthly newsletter

Debt collection insights that keep you compliant and competitive.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.