Regulatory pressure in debt collection is not easing; it is changing shape. Public enforcement has become less predictable, but litigation risk, especially under TCPA, continues to surge. The result is not relief. It is a shift in where and how organizations get exposed.

For collection agencies managing large consumer portfolios, that distinction matters. Fewer federal actions does not mean less legal exposure. It means exposure is moving to private litigation and state regulators, two channels that are harder to predict and faster to escalate.

This guide covers the full stack of US debt collection legislation: what each law requires, where compliance programs routinely break down, and what the current regulatory environment means for collection operations.

Federal debt collection legislation is widely understood at a conceptual level. Most agencies know the FDCPA prohibits harassment. Most know TCPA requires consent. The problem is not awareness; it is execution at scale.

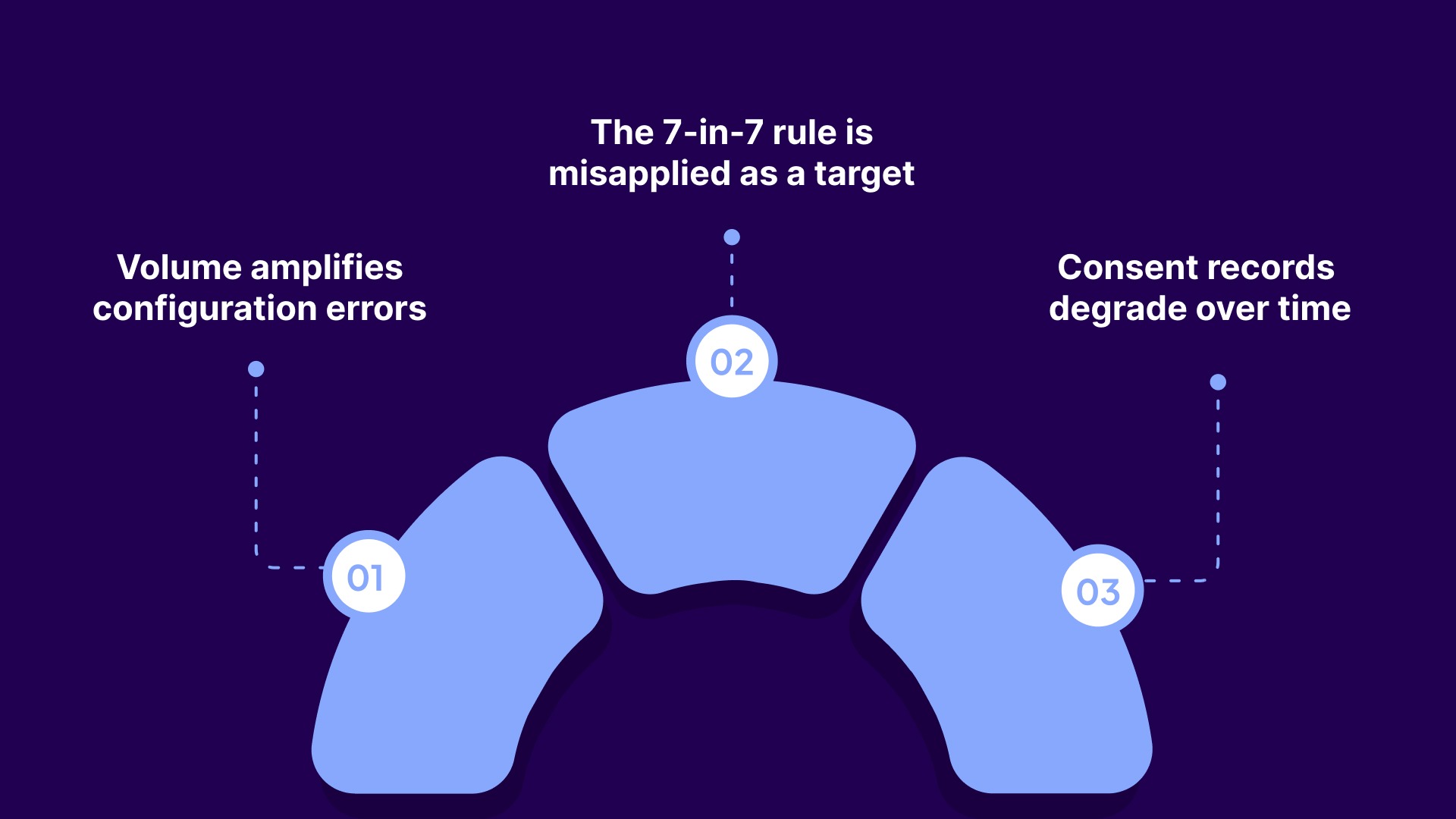

Three patterns account for the majority of compliance failures:

A single misconfigured autodialer campaign can generate thousands of TCPA violations within days. Unlike FDCPA, which caps statutory damages at $1,000 per case, TCPA damages multiply per call or message.

Regulation F caps phone contact attempts at 7 within any 7-day period per account. In practice, many teams treat seven as a permitted volume rather than a hard ceiling. Seven attempts to a non-responsive consumer is not a recovery strategy. It is maximum tolerable exposure before the next call becomes a violation.

With approximately 100,000 mobile numbers reassigned by carriers every day, consent obtained six months ago may belong to a different person today. Both the TCPA and the FDCPA provide safe harbor defenses for collectors who use the FCC's Reassigned Numbers Database, but only if that check is built into execution workflows, not just in policy documents.

When compliance gaps scale this quickly, reactive fixes are no longer enough, your systems need to enforce compliance in real time, not after the fact. See how Tratta helps you embed compliant workflows into every interaction. Book a demo today.

US debt collection compliance is not governed by a single law. It is a layered stack of federal statutes, each targeting a different dimension of the relationship to collections. Understanding how they interact, and where they conflict, is the baseline requirement for any compliance program.

The FDCPA is the foundational statute governing third-party debt collector conduct. Enacted in 1977 and significantly updated through Dodd-Frank in 2010, it applies to collection agencies, debt buyers, and attorneys who regularly collect consumer debts on behalf of others. It does not cover original creditors collecting their own accounts.

Core FDCPA requirements collection operations must enforce:

One frequently misunderstood aspect: the FDCPA prohibits threatening legal action that a collector has no intention or authority to take. This includes implied threats. Regulators are increasingly scrutinizing letters that reference "legal review" of debts that may be time-barred.

FDCPA violations carry up to $1,000 in statutory damages per lawsuit, plus attorney fees and actual damages. Class action exposure can reach $500,000 or 1% of net worth, whichever is less.

Also Read: 8 Ways to Avoid Violations with a Debt Collection IVR FDCPA Compliant Setup

The TCPA governs automated outbound communications, autodialers, prerecorded messages, and SMS. It is administered by the FCC and represents the highest per-violation financial exposure in collections.

Key TCPA requirements for collection agencies:

For debt collection outreach to existing accounts (not sales/marketing), courts have generally treated consent as provided when the consumer gave their number as part of the original transaction. However, that consent does not survive number reassignment, and it does not extend to prerecorded messages.

The regulatory picture around TCPA is also shifting. The debt collection industry, led by ACA International, is advocating for TCPA reform that would align it more closely with FDCPA and Regulation F standards, following the FCC's March 2025 deregulation review.

One important update to track: the "Revoke All" rule, which would allow consumers to revoke consent across all accounts with a single "STOP" message, has been delayed to January 31, 2027. Until then, collectors must honor any reasonable means of revocation on a per-communication basis.

Regulation F, effective November 30, 2021, is the most significant update to federal debt collection legislation since the FDCPA was passed. It implements and modernizes the FDCPA's communication rules for the digital environment.

Key Regulation F requirements beyond the base FDCPA:

The FDCPA and TCPA govern how collectors communicate. The FCRA governs what information they report. These are separate obligations, and treating them as unrelated is one of the most common compliance gaps in collection operations.

The moment a debt collector furnishes account information to a consumer reporting agency, FCRA obligations attach. Those obligations are specific and enforceable:

FCRA risk rarely starts with intentional misconduct. It builds through operational breakdowns: delayed status updates after payment, inaccurate balance corrections, and missed dispute deadlines. In October 2025 alone, 919 FCRA lawsuits were filed, making it one of the highest-volume months on record.

Unlike TCPA risk, FCRA exposure usually does not come from a single configuration mistake. It compounds over time. Late updates, unresolved disputes, and inconsistent account reporting can signal a systemic compliance failure rather than an isolated error.

UDAAP (Unfair, Deceptive, or Abusive Acts or Practices) is enforced by the CFPB under the Dodd-Frank Act. Unlike FDCPA and TCPA, which are rule-based statutes, UDAAP is a harm-based framework. Regulators evaluate the cumulative consumer experience, including tone, sequencing, and framing, not just whether individual actions broke a specific rule.

Key UDAAP risk areas for collection agencies:

UDAAP exposure is often architectural. Standard compliance audits frequently miss it because no single action is a clear violation. The risk is in the pattern, not the individual piece.

The SCRA provides specific protections for active-duty members of the US armed forces. It applies regardless of whether the debt collector is covered by the FDCPA, making it relevant for first-party collectors as well.

Core SCRA protections that affect collection operations:

Failure to verify military status before proceeding with legal collection actions is the most common SCRA violation in collections. This applies to default judgment processes specifically. The SCRA also extends to dependents of active-duty servicemembers in certain circumstances.

The enforcement environment for debt collection legislation has shifted materially since 2024. Understanding the current landscape is necessary for calibrating compliance investment accurately.

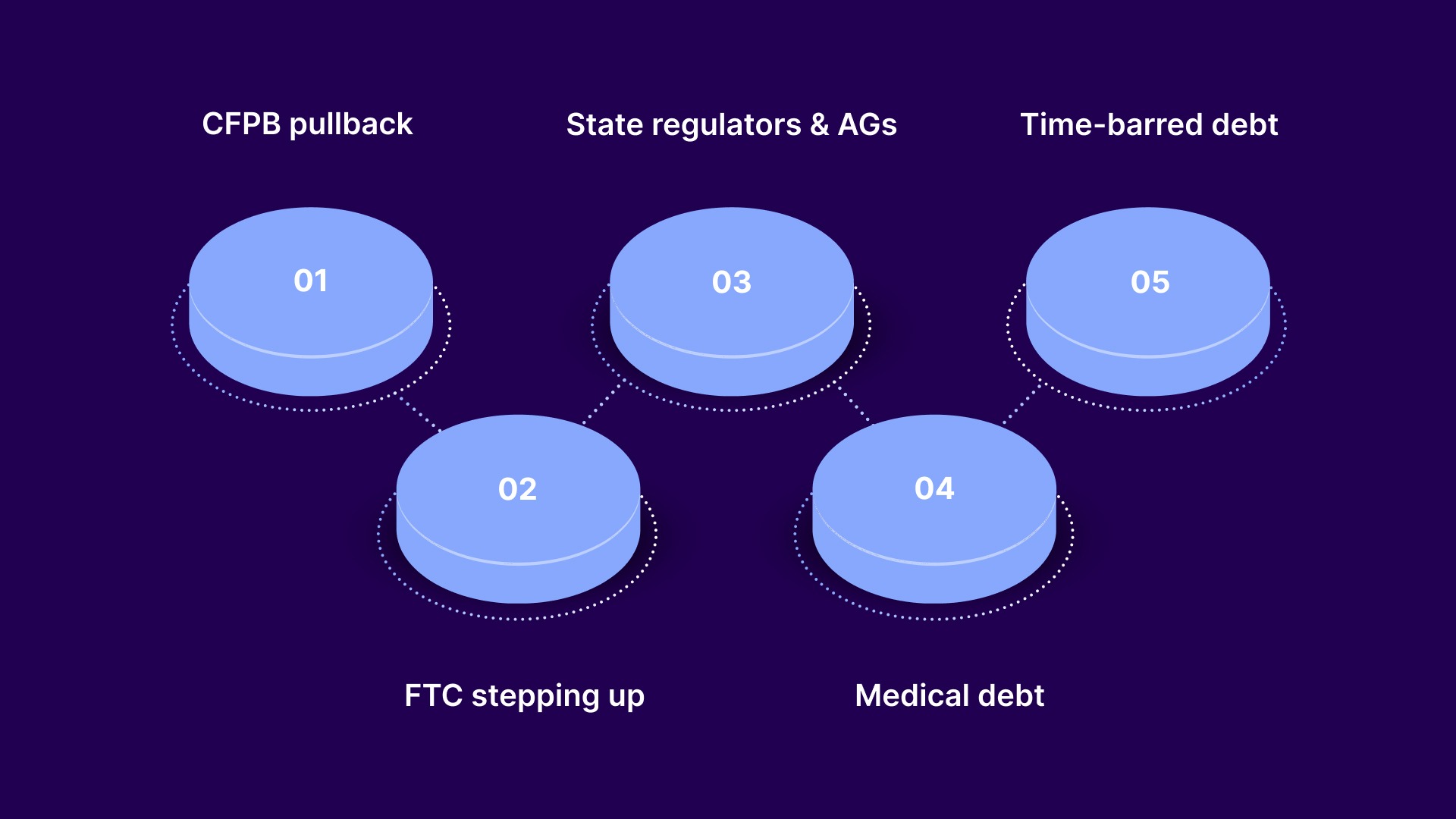

The CFPB significantly reduced its debt collection enforcement activity in 2025. The agency tracked nine enforcement actions against debt collectors, down from 16 in 2024. In August 2025, the CFPB sought comment on raising the “larger participant” supervision threshold from $10 million to $25 million, $50 million, or $100 million in annual receipts.

Six of the nine 2025 enforcement actions came from the FTC, not the CFPB. FTC actions focused on student loan debt-relief schemes and phantom debt collection, cases where agencies attempted to collect fabricated debts. As the CFPB's footprint shrinks, the FTC appears to be filling a targeted enforcement role.

The more significant change for most collection agencies is the increase in state-level enforcement activity. State attorneys general are actively investigating matters that would previously have been handled federally. California's DFPI increased annual reporting requirements under the Debt Collection Licensing Act in 2025. New York's Department of Financial Services added a former senior CFPB enforcement official to its consumer protection division.

California banned medical debt from credit reports effective January 1, 2025, under SB 1061. Maryland passed a trio of new medical debt collection laws in 2025. The CFPB's federal medical debt reporting ban remains stalled in litigation as of early 2026.

H.R. 2704, introduced in April 2025, would amend the FDCPA to explicitly prohibit any collection attempt, not just litigation, on time-barred debt. The bill remains in committee but signals the direction of federal legislative intent.

State debt collection legislation varies significantly and, in many cases, imposes stricter requirements than federal law. When state law and federal law conflict, the rule more protective of the consumer generally applies.

Agencies operating across multiple states need jurisdiction-specific compliance controls, not just federal baseline policies. State enforcement actions do not require the same investigative runway as federal actions, complaints to state AGs can escalate into formal investigations quickly.

Compliance knowledge does not produce compliance outcomes. Systems do. At high account volumes, the difference between an agency with low violation rates and one with chronic exposure is rarely training quality, it is whether compliance constraints are enforced architecturally or left to individual agent discretion.

What a functional compliance program requires:

Debt collection legislation in the US is not a single statute; it is a layered framework of federal and state requirements, each with different enforcement mechanisms and different financial consequences for non-compliance. As federal enforcement softens and state regulators fill the gap, the operational pressure is not decreasing. It is redistributing.

Agencies that treat compliance as an architectural problem rather than a training problem have meaningfully lower legal exposure over time. The tools, workflows, and systems used to manage consumer contact need to enforce compliance constraints automatically, rather than rely on agent recall under volume pressure.

If your current setup requires agents to manually manage contact frequency, consent verification, or dispute timelines, that gap will surface under audit or litigation before it surfaces in internal review.

Tratta is designed to help collection teams centralize payments, communications, and reporting in one compliance-aware platform. Explore Tratta's Security and Compliance features to see how it supports controlled workflows across your agency, or schedule a demo to walk through it with our team.

The FDCPA is the primary federal law, but collection operations are also subject to the TCPA, Regulation F, the FCRA, UDAAP, and the SCRA. No single law covers all compliance obligations; each statute governs a different dimension of the collection relationship.

TCPA penalties range from $500 per negligent violation to $1,500 per willful violation. Because penalties apply per call or message, a single misconfigured campaign targeting hundreds of consumers can quickly generate six- or seven-figure liability.

Generally, no. The FDCPA applies to third-party collectors. However, if an original creditor uses a different business name during collection that implies a third party is involved, FDCPA coverage may apply. UDAAP obligations under Dodd-Frank apply to original creditors regardless.

Regulation F prohibits more than 7 calls to a consumer regarding a specific debt within any 7 consecutive days. After a live conversation, the collector must wait 7 days before calling that account again. This cap applies per debt, not per consumer.

The FDCPA prohibits specific, defined actions. UDAAP evaluates whether the overall pattern of conduct is unfair, deceptive, or abusive, even if no single action violated a specific rule. An agency can satisfy every Regulation F requirement and still face UDAAP exposure if the cumulative consumer experience is deemed coercive or misleading.

Regulation F does not replace the FDCPA; it clarifies and operationalizes it for modern communication channels. In practice, agencies must comply with both simultaneously. Where Regulation F provides specific numeric limits or procedures, like the 7-in-7 rule or validation notice format, it effectively becomes the operational standard, while the FDCPA continues to govern broader conduct such as harassment, deception, and unfair practices.

Yes, both are permitted under Regulation F, but with conditions. Email and SMS outreach are allowed if the consumer has not opted out and if required disclosures are included, especially the validation notice in the initial email. However, collectors must also ensure compliance with FDCPA content rules and avoid third-party disclosure risks, which remain a major exposure area in digital communication.

If a reassigned number is contacted without updated consent verification, it can result in TCPA violations, even if the original consent was valid. Liability typically depends on whether the collector used available safeguards such as reassigned number databases or reasonable verification processes. This is one of the fastest-growing risk areas in automated dialing systems due to constant number recycling.

In most cases, debt buyers are treated as "debt collectors" under the FDCPA if they acquire debts in default and attempt collection. This means they are subject to the same communication, disclosure, and harassment rules as third-party agencies. However, FCRA obligations can become more complex because debt buyers often assume reporting responsibilities alongside collection activity.

The highest-risk factor is not a single law but system-level failure under scale. As account volume increases, small configuration errors, like incorrect call caps, outdated consent records, or inconsistent channel messaging, can multiply into thousands of violations quickly. Most enforcement actions originate from operational breakdowns rather than intentional misconduct, especially in TCPA and FCRA cases.