A single non-compliant text can expose your agency to audits, disputes, and financial penalties that scale fast. Regulators are already seeing the impact. In 2025, they handled roughly 113,000 robocall and robotext complaints every month, collecting over $178 million in penalties.

That level of enforcement is not slowing down. If your SMS workflows are fragmented or manually managed, staying compliant becomes difficult to sustain. Small gaps quickly turn into large risks.

This SMS Compliance Checklist is designed to help your agency identify those gaps, strengthen controls, and build a more defensible, audit-ready messaging process for 2026.

SMS compliance refers to the legal and operational controls that govern how your agency sends text messages to consumers. It covers consent, disclosures, timing, opt-outs, recordkeeping, and data protection across every interaction.

To understand how these rules apply in practice, you need to look at the key laws, regulators, and industry bodies that collectively define SMS compliance. These are:

The TCPA is the primary federal law regulating automated calls and text messages to consumers. It requires prior express consent, and for many collection scenarios, prior express written consent, depending on the communication method used.

The FCC enforces the TCPA and issues rules that clarify how it applies to modern communication channels like SMS. It defines consent standards, permissible contact hours, and enforcement priorities. The FCC also drives regulatory updates that agencies must continuously adapt to.

CTIA publishes messaging principles and best practices that carriers use to monitor SMS traffic. While not law, these guidelines are enforced indirectly through carrier filtering, blocking, and campaign approvals. Non-compliance can result in message blocking even if no law is technically violated.

The FDCPA governs how debt collectors communicate with consumers, including via text messages. It prohibits harassment, misleading statements, and unfair practices regardless of the channel used. SMS content must align with FDCPA standards to avoid consumer disputes and legal action.

The CFPB enforces the FDCPA and has expanded its interpretation to include digital communications, such as SMS. It introduced rules under Regulation F that clarify how collectors can use electronic channels. The CFPB also focuses on recordkeeping and dispute handling, increasing the need for audit-ready systems.

Several states have introduced their own telemarketing and privacy laws that expand on federal requirements. For instance, under the Florida Telephone Solicitation Act (FTSA), agencies can face $500 to $1,500 per message. This is similar to TCPA, but with stricter consent requirements and broader definitions of automated systems, making compliance more difficult.

Mobile carriers actively monitor messaging traffic for compliance with both legal and industry standards. They use filtering algorithms and registration frameworks to detect suspicious or non-compliant campaigns. Failure to meet these requirements can lead to message blocking, throughput limits, or campaign suspension.

These overlapping frameworks create a layered compliance environment where gaps can emerge quickly. In the next section, we break this complexity down into a structured, step-by-step checklist you can apply directly to your SMS workflows.

Suggested Read: Text Messaging Strategies for Debt Collection

A structured checklist helps standardize SMS compliance across teams, tools, and workflows. This reduces variability, closes gaps, and makes your processes easier to audit.

Table showing a handy SMS compliance checklist:

A checklist only works if each control is clearly understood and consistently applied. Below is a deeper look at why each control matters, what happens if it is ignored, and how it applies in real agency workflows.

Consent is the legal basis of SMS outreach under the Telephone Consumer Protection Act (TCPA). Agencies must be able to prove that a consumer has given prior express consent, and in some cases prior express written consent, before sending messages.

To ensure consent is valid and defensible, focus on:

If this step is skipped or poorly documented, every message sent can be treated as an independent violation, exposing the agency to statutory damages. In high-volume environments, this quickly escalates into significant financial and legal risk.

Opt-out compliance is mandated under both the Telephone Consumer Protection Act (TCPA) and enforced through carrier standards influenced by the Cellular Telecommunications Industry Association (CTIA). Consumers must be able to revoke consent easily, and agencies must honor that immediately.

To maintain compliant opt-out workflows, ensure:

Failure to process opt-outs in real time can lead to repeated unwanted messages, which regulators and courts often interpret as willful violations.

Tratta supports this through a self-service preference center and automatic opt-in/opt-out enforcement. It helps ensure consumer preferences are consistently applied across communication channels. Schedule a free demo.

The Fair Debt Collection Practices Act (FDCPA) and Federal Communications Commission (FCC) rules impose limits on when and how often consumers can be contacted. Agencies must avoid messaging at inconvenient times or at excessive frequency.

To stay within acceptable limits, agencies should:

Ignoring these controls can result in claims of harassment or abusive practices, even if consent exists. This is particularly risky in collections, where repeated outreach is common and closely scrutinized.

SMS content is governed by the Fair Debt Collection Practices Act (FDCPA), which prohibits misleading, deceptive, or unfair communication. Every message must clearly identify the sender and avoid language that could be interpreted as threatening or ambiguous.

To ensure compliant messaging content, focus on:

If content standards are not followed, agencies risk disputes, consumer complaints, and regulatory scrutiny. Even minor wording issues can trigger allegations of misrepresentation or unfair practices.

Consumer data used in SMS outreach is subject to broader regulatory expectations, including oversight from the Consumer Financial Protection Bureau (CFPB). Agencies must ensure that personal information is securely handled and protected from unauthorized access.

To maintain strong data protection practices, agencies should:

Weak data controls increase the risk of breaches, misuse, and regulatory penalties. In addition, poor data governance undermines trust and can complicate dispute resolution.

Recordkeeping is critical for demonstrating compliance under both the Telephone Consumer Protection Act (TCPA) and Consumer Financial Protection Bureau (CFPB) expectations. Agencies must be able to produce clear evidence of consent, messaging activity, and opt-out handling.

To ensure audit readiness, agencies need to:

If records are incomplete or missing, agencies lose the ability to defend themselves during audits or legal disputes. This often results in unfavorable outcomes, even if processes were followed in practice.

A defined checklist creates structure, but it does not guarantee consistent execution. In the next section, we examine where agencies typically fall short and how those gaps lead to compliance risk.

Suggested Read: SMS Debt Collection: Significance, Uses, and Templates

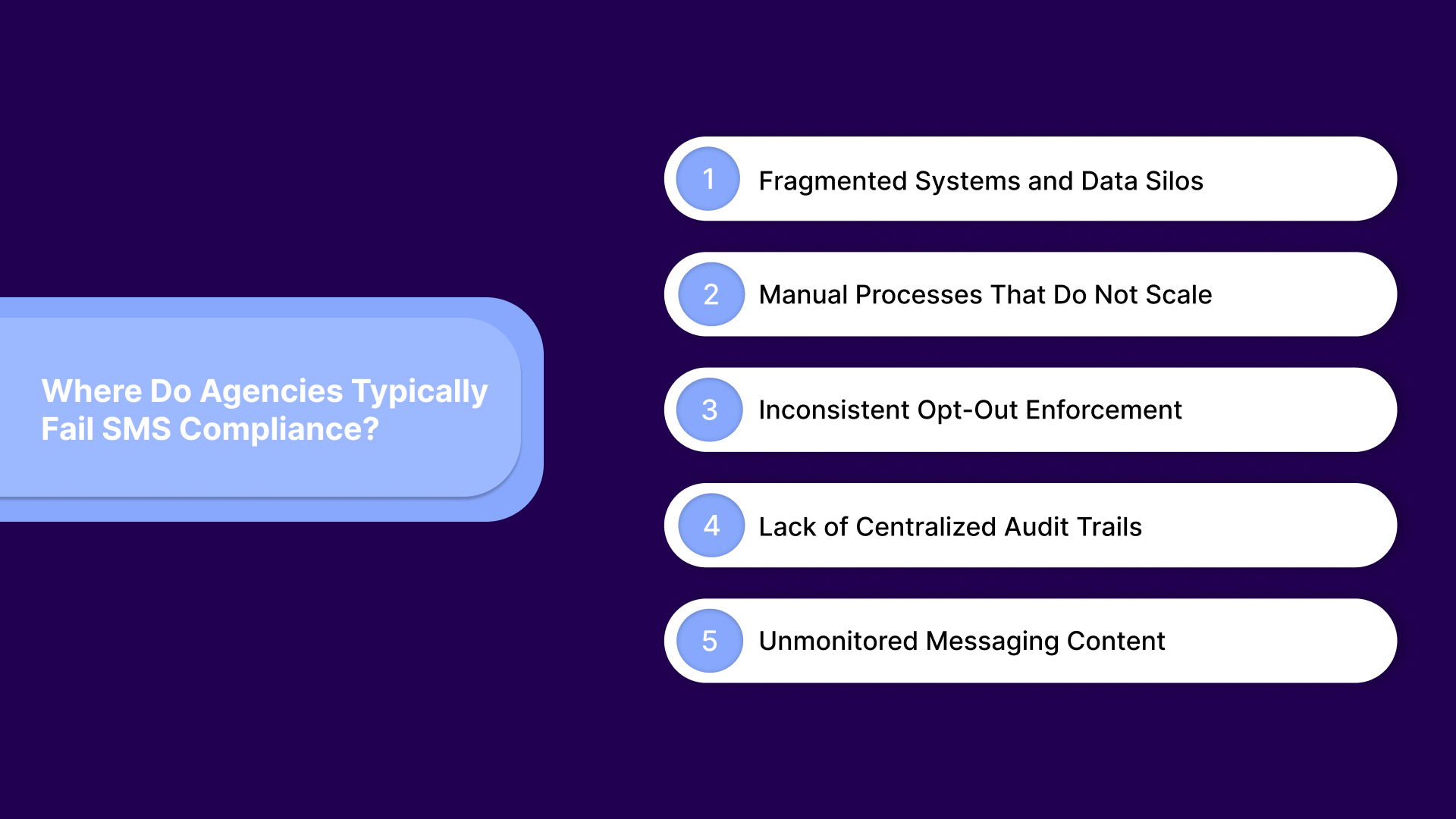

Most compliance failures occur in how controls are executed across systems, teams, and workflows. For collection agencies managing high message volumes, even small breakdowns can quickly escalate into repeat violations.

The most common failure points include:

Tratta addresses these gaps by centralizing communications, consent tracking, and audit trails within a single, controlled system. This ensures compliance rules are enforced consistently at the point of action, eliminating the breakdowns that typically occur across disconnected workflows. Call us to learn more.

A single gap, whether in consent, opt-outs, or timing, can quickly scale into widespread exposure across campaigns. The real risk lies in how these violations compound across volume, jurisdictions, and regulatory layers.

The impact of non-compliance includes:

Violations are typically calculated per message, which means liability scales with every SMS sent. Under the Telephone Consumer Protection Act (TCPA), agencies face a $ 500-per-message penalty, up to $1,500 for willful violations.

Additional exposure can arise under Do Not Call (DNC) rules, where penalties of $53,088 per violation further compound risk across campaigns.

When violations affect large groups of consumers, they often escalate into class action lawsuits. Because damages are calculated per message, even minor compliance gaps can lead to significant financial exposure at scale. This is one of the most severe risks for agencies running high-volume SMS campaigns.

Agencies may face enforcement from regulators such as the Consumer Financial Protection Bureau (CFPB) and the Federal Communications Commission (FCC). These actions can result in fines, mandated corrective measures, and ongoing compliance monitoring.

Non-compliant messaging can violate the Fair Debt Collection Practices Act (FDCPA), especially if messages are perceived as excessive, misleading, or intrusive. This exposes agencies to individual lawsuits, disputes, and reputational damage.

Non-compliance with industry standards set by the Cellular Telecommunications Industry Association (CTIA) can lead to carrier filtering or blocking of messages. This prevents legitimate communications from reaching consumers, directly impacting recovery rates.

Operationalizing compliance depends on having the right system architecture in place. In the next section, we look at how Tratta enables this through a compliance-first design that embeds these controls directly into your workflows.

Suggested Read: 10 Effective Debt Collection SMS Examples That Get Results

.jpg)

Tratta is a collections-focused platform built to combine payments, communications, and compliance into a single operational layer. Instead of relying on disconnected tools, it centralizes the entire consumer interaction lifecycle, from outreach to resolution, within one system.

Tratta strengthens SMS compliance by embedding regulatory controls directly into messaging workflows. This means consent tracking, opt-out enforcement, disclosures, and audit trails are not handled separately; they are applied automatically at the point of communication.

Beyond SMS, Tratta’s broader feature set supports compliant, scalable operations:

Allows consumers to view balances, set payment plans, resolve accounts, and manage interactions without agent involvement. This reduces manual errors and creates a controlled, trackable environment for compliance.

Supports card and ACH payments, including full, partial, and recurring plans. Integrated payment handling ensures accurate tracking and reduces reconciliation gaps across systems.

Enables automated payment and interaction through IVR systems, expanding accessibility while maintaining consistent compliance controls across voice channels.

Combines SMS, email, phone, and other channels into one platform with built-in compliance features like opt-in/opt-out enforcement, disclosures, and FDCPA logic. This ensures consistent application of rules across all communication touchpoints.

Provides automated, trigger-based messaging campaigns tied to account activity. This reduces manual intervention and ensures messaging follows predefined, compliant workflows.

Offers real-time tracking of messaging, payments, and engagement, with detailed logs that support audit readiness and performance optimization.

Allows agencies to configure workflows, templates, and communication rules to align with internal policies and regulatory requirements.

Connects with existing systems through APIs and data sync, ensuring consistency across platforms without duplicating or fragmenting compliance data.

Includes safeguards like encryption, role-based access, and compliance tracking to support regulatory alignment and protect consumer data.

Centralizes agent-consumer communication with inboxes, ticketing, and documented interactions, ensuring every touchpoint is tracked and audit-ready.

Tratta also supports rapid, structured onboarding. The platform is implemented, integrated, and configured alongside your team, enabling agencies to go live with compliant workflows already in place and minimizing disruption during transition.

Compliance gaps in SMS workflows rarely stay contained. Missed opt-outs, unclear consent records, or inconsistent messaging can quickly escalate into penalties, disputes, and lost consumer trust. For agencies operating at scale, even small breakdowns can multiply into significant financial and operational risk.

Tratta addresses this by embedding compliance directly into your communication infrastructure. With centralized messaging, automated consent enforcement, and audit-ready tracking, it ensures your agency operates with consistency, control, and confidence.

Strengthen your SMS compliance before risks escalate. See how Tratta can help you build audit-ready, compliant workflows for 2026 and beyond.

SMS compliance refers to the legal and operational rules that govern how agencies send text messages to consumers. It includes requirements around consent, opt-outs, message timing, content, and recordkeeping.

Regulatory requirements for SMS include obtaining prior express consent, providing clear opt-out mechanisms, and respecting time-of-day restrictions. Agencies must also ensure messages are not misleading and include proper identification.

TCPA compliance for SMS requires agencies to obtain and document prior express consent before sending text messages. It also mandates honoring opt-outs, following contact time restrictions, and maintaining records of all communications.

21 CFR Part 11 applies to electronic records and signatures, primarily in regulated industries like healthcare and pharmaceuticals. For collection agencies, it is not a direct requirement for SMS compliance, but highlights best practices such as secure recordkeeping, audit trails, and system validation.

Collection agencies can stay compliant by centralizing communication systems, automating consent and opt-out enforcement, and maintaining audit-ready records. Implementing real-time compliance controls reduces the risk of violations across high-volume messaging workflows.