A single gap in your IVR flow can do more than create friction. It can expose your agency to repeated compliance violations, especially when automation scales the same mistake across every interaction. As IVR becomes a core part of collection operations, the real challenge is not efficiency. It is to ensure that every automated step aligns with FDCPA requirements.

The financial risk is clearly defined. Under the Fair Debt Collection Practices Act, consumers may recover up to $1,000 in statutory damages per action, along with actual damages and attorney’s fees for violations.

Building a debt collection IVR FDCPA-compliant setup is therefore critical. In this article, we break down what compliance looks like in IVR systems and outline eight ways to reduce risk while maintaining operational control.

An IVR system in debt collection must follow the same legal standards as live agents. The Fair Debt Collection Practices Act (FDCPA) and Regulation F apply equally to automated interactions, meaning every prompt, disclosure, and action must be compliant.

The challenge is that IVR systems operate at scale, so even a small logic or scripting gap can result in repeated violations across hundreds of interactions.

A compliant IVR system must enforce the following requirements:

The real value comes from how IVR systems are designed to enforce them consistently, which is where a well-structured approach becomes critical. In the next section, we look at how compliant IVR systems help in improved debt recovery.

Suggested Read: The IVR Payment Gap: What Most Debt Collectors Are Missing in 2026

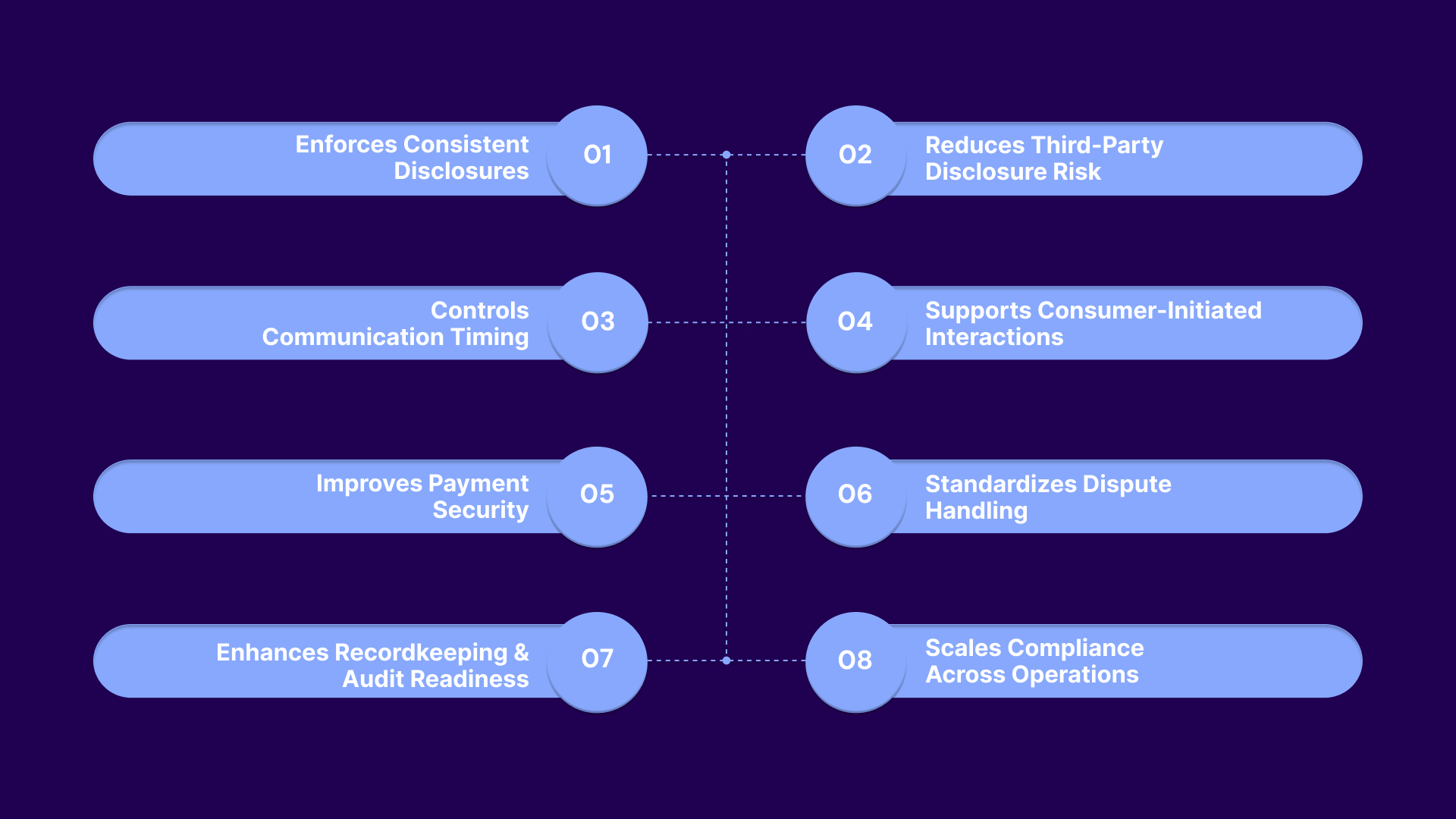

A compliant IVR system improves how your collection operations function at scale by standardizing interactions, reducing manual effort, and ensuring every step aligns with regulatory requirements. When designed correctly, it becomes a control layer that strengthens both compliance and performance.

This is how the right technology helps:

A compliant IVR ensures that every interaction includes required disclosures without relying on agent memory. This eliminates variability and reduces the risk of missed or incorrect statements. It creates a standardized communication flow across all accounts.

The following elements must be consistently enforced in IVR disclosures:

Intelligent IVR systems can verify identity before sharing sensitive information. This helps prevent accidental disclosure to unauthorized individuals. It ensures compliance with privacy requirements while maintaining secure interactions.

Key controls that support secure identity verification include:

A compliant IVR enforces when and how often consumers are contacted. This reduces the risk of excessive or improperly timed communication. It ensures all outreach remains within regulatory limits.

Important controls for managing communication include:

Inbound IVR systems allow consumers to engage on their own terms. This reduces reliance on outbound calls and minimizes compliance exposure. It creates a more controlled and non-intrusive engagement model.

Key benefits of consumer-initiated IVR interactions include:

A compliant IVR can redirect consumers to secure payment environments rather than collect sensitive data over calls. This reduces the risk of data exposure and aligns with security standards. It ensures payment processes remain both compliant and traceable.

Secure payment handling in IVR systems includes:

IVR systems can guide consumers through dispute processes in a structured way. This ensures disputes are captured accurately and handled consistently. It reduces the risk of missed or improperly managed disputes.

Key elements of compliant dispute handling include:

Every IVR interaction can be logged automatically. This creates a detailed audit trail that supports compliance verification. It ensures agencies can respond effectively to disputes or audits.

Essential recordkeeping capabilities include:

A compliant IVR applies the same rules across every interaction, regardless of volume. This eliminates dependency on manual processes and reduces human error. It allows agencies to scale operations without increasing compliance risk.

Core elements that enable scalable compliance include:

Tratta provides these advantages through its inbound, multilingual payment IVR and Compliance-by-Code approach. It embeds regulatory controls into every interaction while enabling secure, consumer-initiated payment experiences across channels. This allows agencies to scale collections confidently while maintaining consistent, audit-ready compliance. Schedule a free demo.

Fully automated AI-powered IVR systems promise efficiency and scalability, but without proper controls, they can introduce significant compliance risk. Unlike rule-based systems, AI-driven flows can generate responses dynamically, making it harder to ensure every interaction aligns with FDCPA requirements.

The most common risks associated with fully automated AI IVR systems include:

These risks highlight a broader issue. When automation operates without structured compliance controls, it can create violations faster than manual processes ever could. The next section looks at the consequences of such violations.

Suggested Read: The Power of IVR in Simplifying Debt Collection

Because IVR operates at scale, one compliance gap can result in repeated violations across hundreds or thousands of consumer interactions. This amplifies legal exposure, increases complaint volume, and can trigger regulatory action quickly.

The consequences under the FDCPA include:

FDCPA is only one part of the regulatory landscape. IVR systems in debt collection may also fall under additional laws that govern communication, consent, and data handling, further increasing compliance complexity.

These are:

Tratta reduces compliance risk through an inbound, consumer-initiated IVR that gives consumers control over when and how they engage. It standardizes disclosures, identity verification, and payment flows within a secure, rule-driven system. Get in touch with us to learn more.

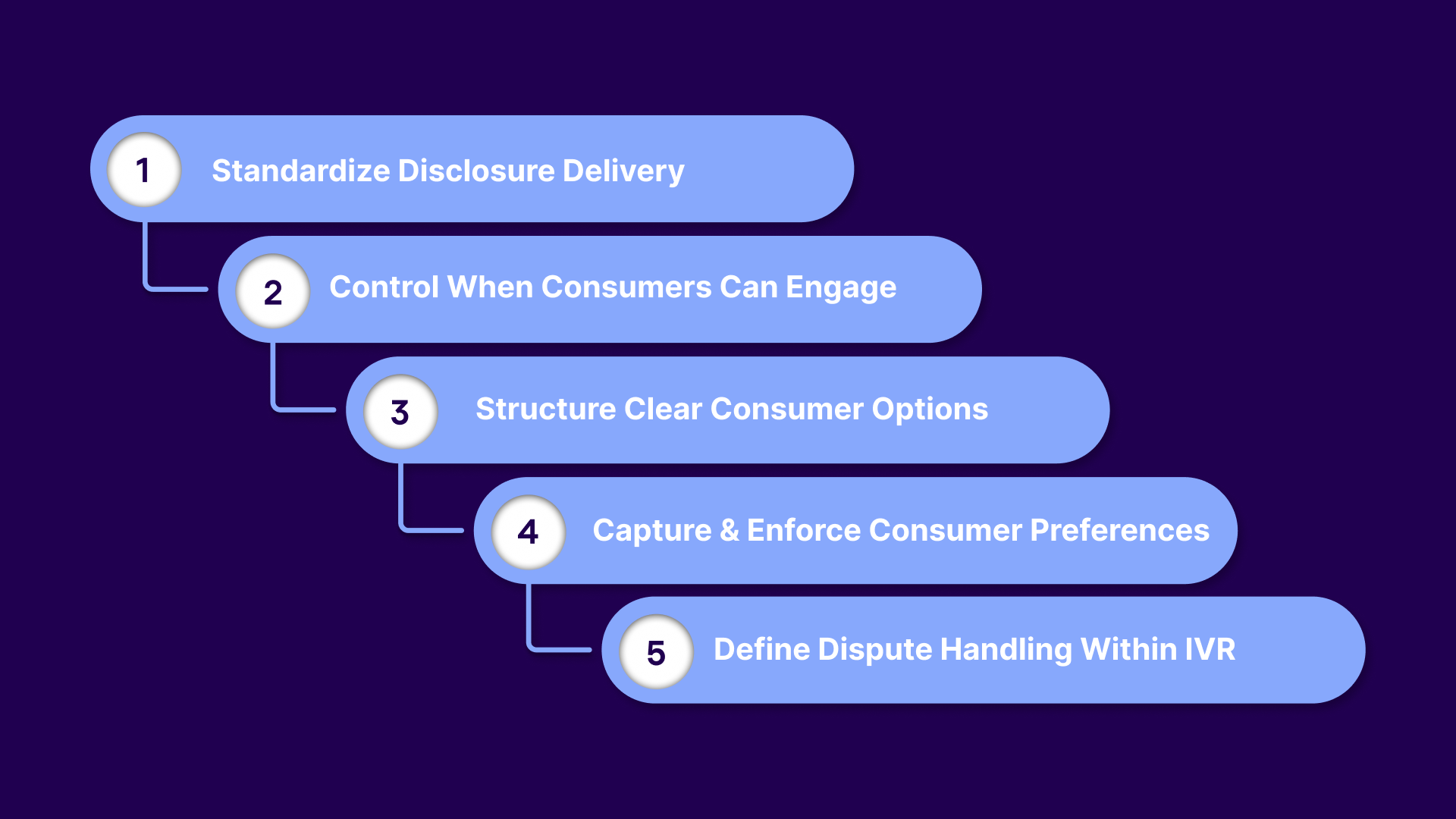

IVR compliance should be an extension of your collection strategy, policies, and day-to-day operations. Every call flow must reflect how your agency handles disclosures, disputes, payments, and consumer interactions in a compliant and consistent manner.

To implement compliant IVR call flows, agencies should focus on the following operational practices:

Even with strong operational practices in place, maintaining consistency across high volumes of interactions can be challenging. This is where the right technology becomes essential for enforcing rules, standardizing execution, and supporting compliant collection at scale.

Suggested Read: Optimizing IVR for Better Self-Service: Best Practices and Benefits

.jpg)

Tratta is a digital debt collection platform built to help agencies automate operations without compromising compliance or consumer experience. It connects payments, communications, workflows, and reporting into a single system, allowing agencies to manage collections with greater control, transparency, and consistency.

Core features include:

Enables inbound, consumer-initiated payments through a secure and accessible IVR system. It reduces outbound pressure while supporting compliant, self-service resolution across languages.

Allows consumers to view accounts, set up payment plans, and resolve balances independently. This improves transparency while reducing agent dependency and compliance risk.

Provides secure, compliant payment processing across multiple channels. It ensures accurate tracking, reconciliation, and protection of sensitive financial data.

Centralizes SMS, email, and voice interactions into a single system. This ensures consistent messaging, proper disclosures, and controlled communication across all touchpoints.

Automates outreach using rule-based segmentation and timing. It helps agencies maintain compliant communication strategies while improving engagement.

Offers real-time visibility into performance, consumer behavior, and compliance metrics. This allows agencies to monitor operations and address risks proactively.

Enables agencies to configure workflows, messaging, and operational rules. This ensures alignment with both regulatory requirements and internal policies.

Connects seamlessly with existing systems for real-time data flow. This eliminates silos and ensures compliance is maintained across the entire operation.

Protects sensitive data through encryption, access controls, and secure infrastructure. It supports regulatory requirements while minimizing risk exposure.

Supports agent-led interactions with full visibility into account history and compliance requirements. It ensures human interactions remain consistent with system-enforced rules.

Tratta’s inbound IVR is designed to give consumers control while keeping your operations compliant and efficient. It connects easily with your broader collection workflows, ensuring every interaction, from payment to account access, follows consistent rules and secure processes.

When IVR systems are not designed with compliance in mind, they can quickly become a source of repeated violations, consumer complaints, and legal exposure. What seems like an efficiency gain can turn into operational risk, especially when automation scales errors across every interaction.

Tratta helps address this by enabling inbound, consumer-initiated IVR experiences that prioritize control, transparency, and secure engagement. Connected workflows, standardized processes, and real-time visibility allow agencies to automate confidently while maintaining compliance.

Build a more controlled, compliant IVR strategy today. Book a free demo.

A debt collector is any third party that regularly collects debts owed to another party. This includes collection agencies, debt buyers, and law firms engaged in collection activities.

The most common violations involve improper communication, such as calling at restricted times, failing to provide required disclosures, or using misleading language during collection efforts.

Consumers can request collectors to stop communication by stating: “Please cease and desist all calls and contact with me immediately.” Agencies must honor such requests under FDCPA rules.

Under Regulation F, collectors are generally limited to 7 call attempts within 7 consecutive days for each debt. Additional calls may be restricted based on prior contact.

Yes, IVR systems are allowed if they comply with FDCPA and related regulations. They must include proper disclosures, respect communication limits, and protect consumer information.