The latest Federal Reserve Bank of New York report shows U.S. household debt at $18.59 trillion in Q3 2025. Aging accounts are arriving faster than your team can review. One missed limitation date can waste hours of legal work and risk compliance issues.

If you work with New York portfolios, knowing which accounts are legally actionable is critical. The statute of limitations on debt in NY tells you which accounts you can sue and which are time-barred. Without it, you could spend resources on accounts that cannot be enforced.

In this blog, we break down the rules, timelines, and practical steps to help you manage accounts correctly, reduce risk, and keep recoveries on track.

Quick Insights

In New York, the statute of limitations sets the maximum time a creditor or collection agency has to file a lawsuit to recover a debt. Once this period expires, the account becomes time-barred for litigation, meaning legal action is no longer permitted under state law.

The statute of limitations on debt in NY applies only to court enforcement, not to the existence of the debt itself. An unpaid balance may remain on record, but courts will not allow a collection lawsuit if the filing deadline has passed and the defense is raised.

For collection agencies and law firms, the statute of limitations functions as a litigation gatekeeper:

New York law assigns different limitation periods based on the type of debt and the nature of the underlying contract. Correctly classifying each account is essential, as applying the wrong statute can result in dismissed cases, compliance findings, or unnecessary legal spend.

New York does not apply a single limitation period to all debt. The statute of limitations depends on the type of debt and the legal basis of the obligation. For collection agencies, correct classification is critical; applying the wrong statute can result in dismissed lawsuits, compliance exposure, and wasted legal spend.

The table below outlines the current statute of limitations periods applicable in New York, along with the governing legal authority. These timelines determine whether an account remains eligible for litigation, not whether the debt exists.

Key operational note:

The 3-year limitation under CPLR §214-i applies specifically to consumer credit transactions, regardless of whether a written agreement documents the obligation. This is a common source of misclassification, especially in mixed or purchased portfolios.

For agencies handling New York accounts, this means limitation periods must be tied to:

Suggested Read: How Do Medical Bills Influence Credit Scores and Debt Recovery?

A specific starting event triggers the statute of limitations in New York, and getting that date wrong can invalidate an otherwise eligible case.

In most New York debt cases, the clock starts on the date of default, typically the last missed payment that was due and not cured. It does not begin when the account was opened or when the balance was charged off.

A few practical rules matter here:

Example: If a borrower made their final payment in March 2021 and failed to make the April 2021 payment, the statute of limitations would generally begin running from the April 2021 default date, not from when the account was charged off months later.

There are also situations where timing can be misunderstood:

Because New York applies strict standards to limitation defenses, courts closely examine account history, payment records, and the timing of defaults. That makes accurate data intake and validation essential before legal placement or filing.

Suggested Read: Exceptions to the Statute of Limitations: Key Insights

A debt is considered time-barred when the statute of limitations for filing a lawsuit has expired. At that point, the account is no longer eligible for legal action, even if the balance still exists.

This distinction matters because time-barred does not mean uncollectable. It means the debt is no longer enforceable through the court system.

Here is how New York law separates the two concepts:

A debt may still be collected through permitted non-litigation methods if:

A debt is litigable only if:

If you attempt to file suit on a time-barred account, the case will likely be dismissed once the defense is raised. Courts in New York take statute-of-limitations defenses seriously, and agencies are expected to know whether an account is legally actionable before filing.

This is where many issues surface in day-to-day operations. If an account is routed for legal review without confirming its limitation status, you risk unnecessary legal costs, compliance findings, and avoidable disputes.

To resolve this issue, Tratta allows agencies to clearly flag enforceability status, prevent expired accounts from entering legal queues, and manage compliant, non-litigation resolutions without manual oversight. Set up a free call to see how it works.

Once an account is time-barred, how it is handled matters just as much as identifying it correctly. The law does not prohibit all collection activity, but it does draw clear boundaries around what is allowed.

If you work with mixed portfolios, this is where mistakes tend to happen. Time-barred accounts often look similar to active ones unless your processes clearly separate them.

Let's go through the actions you can take and the actions that are restricted once the statute has expired.

You may continue certain collection efforts, provided they are accurate and compliant.

This includes:

Any communication must be truthful and must not suggest that legal action is still an option when it is not. If you are reaching out, the context needs to be clear so there is no confusion about the account’s legal status.

Once the statute of limitations has expired, some actions are clearly off-limits.

You cannot:

New York applies strict standards here. Even indirect suggestions that a lawsuit is possible can create compliance exposure if the account is time-barred.

Understanding these rules is only part of the picture. Several state and federal laws shape how statutes of limitations are enforced, and those laws influence both messaging and process design. That is what the next section covers.

Suggested Read: Statute of Limitations on Debt Collection: How Long Can Debt Be Collected?

Statute-of-limitations rules do not exist in isolation. Several state and federal laws shape how limitation periods are applied, disclosed, and enforced. If you are handling New York accounts, these laws influence both legal decisions and day-to-day collection activity.

The CPLR is the legal foundation for New York's statute-of-limitations rules. It defines:

Sections such as CPLR 213, 214, 214-i, and 211 determine whether a lawsuit can move forward. Courts rely heavily on these provisions, which is why accurate classification and timing matter before any filing decision is made.

The Consumer Credit Fairness Act significantly changed how consumer credit cases are handled in the state.

The CCFA:

If you manage consumer credit portfolios, this law directly affects which accounts can be placed for legal action and which must be handled outside the court system.

Federal law also plays a role. The FDCPA governs how collection communications are conducted, including those related to time-barred debt.

Under the FDCPA:

Even when state law allows specific actions, federal standards still apply to how those actions are presented.

Regulatory expectations in New York go beyond statutes. The Department of Financial Services closely examines how agencies:

This makes internal controls and documentation just as necessary as legal interpretation.

In unison, these laws create a compliance environment in which statute-of-limitations errors are rarely treated as minor. They often signal broader process gaps.

That brings up a practical question. How do organizations manage these requirements across large, changing portfolios without slowing recovery or increasing risk? The following section looks at the challenges that surface at scale.

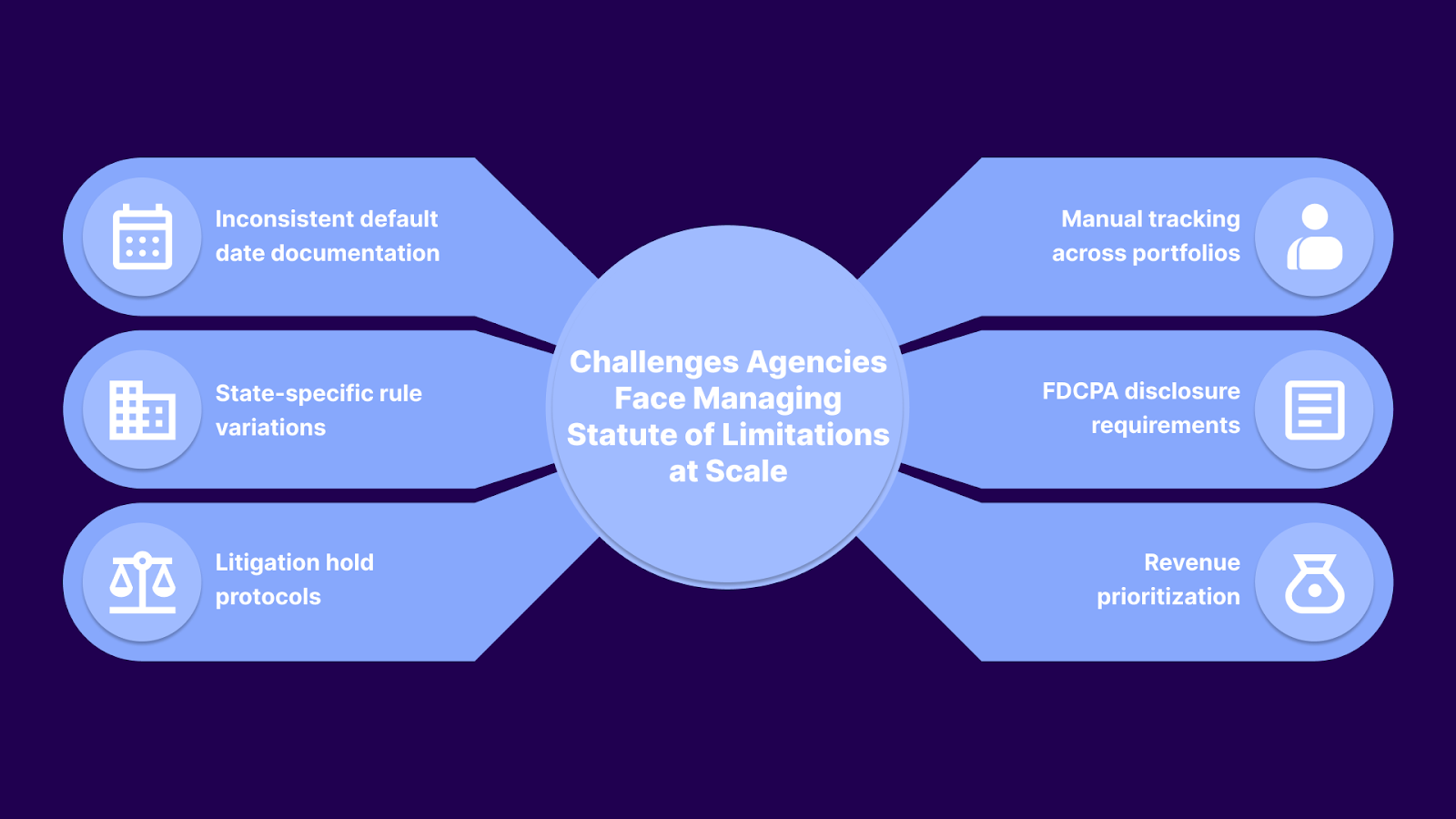

Tracking statute-of-limitations status across large portfolios becomes difficult without structured systems in place. As volume increases, small gaps in data or process can turn into real compliance risk. Agencies commonly encounter the following challenges.

Accounts that pass through multiple creditors or debt buyers often arrive without a clear record of the last payment or default date. Conflicting or missing information makes it difficult to confirm whether the statute has already expired.

What helps:

Managing several portfolios at once means tracking different timelines, documentation standards, and internal notes. When this is handled manually, deadlines are more easily missed, and decisions vary from one team to another.

A better approach:

Tratta supports this approach by centralizing statute-of-limitations data and applying consistent, state-specific rules across portfolios. Book a free call to see how teams operationalize this at scale.

Agencies operating across states must manage different limitation periods. New York’s three-year statute of limitations for consumer credit does not align with longer timelines elsewhere, which can lead to errors if accounts follow the same workflow.

How to stay aligned:

When collecting on time-barred debt, federal and state rules require specific disclosures. If the enforceability status is unclear, outreach can unintentionally imply that legal action is still available.

To keep messaging compliant:

Once an account is time-barred, litigation must permanently stop. Manual controls alone make it easy for expired accounts to slip into legal review.

Where controls matter most:

Time-barred accounts typically generate lower recovery rates because litigation is no longer an option. Without a clear separation, resources can be spread inefficiently.

To allocate effort wisely:

These challenges often compound when data, workflows, and compliance rules are disconnected. Solving them requires visibility and controls that follow each account throughout its lifecycle.

Managing statute-of-limitations rules in New York requires more than policy knowledge. It requires systems that connect account data, compliance controls, and resolution workflows in one place. This is where Tratta fits.

Tratta is designed to give you complete visibility and control over every account, making compliance a built-in part of your operations rather than an afterthought. The platform combines automation, workflow management, and analytics to help you efficiently manage time-barred and litigation-eligible accounts.

Here’s how Tratta’s features directly support statute-of-limitations compliance and account management:

Allows customers to voluntarily resolve or pay debts while ensuring interactions comply with the limitation rules. You can offer digital resolution options without implying legal action.

Enables secure payment processing for collectable accounts while ensuring time-barred accounts are handled in compliance with requirements.

Supports compliant outreach across diverse customer bases, providing clear instructions without suggesting litigation where it is not allowed.

Coordinates emails, calls, and messages across channels, automatically applying enforceability rules to prevent improperly escalated time-barred accounts.

Customizable campaigns allow you to target accounts differently based on statute-of-limitations status, optimizing resource allocation and recovery strategy.

Provides actionable insights into account status, compliance risk, and portfolio performance, helping you identify potential gaps before they become issues.

Supports unique workflows, state-specific rules, and organization-level policies, ensuring your teams follow New York statute-of-limitations rules without manual guesswork.

Works with existing agency, legal, and compliance systems to maintain enforceability data consistently across platforms.

Ensures all account data, communications, and payments comply with regulatory standards, including the FDCPA, New York-specific laws, and internal audit requirements.

By combining these features, Tratta reduces the risk of statute-of-limitations errors, keeps workflows efficient, and provides the transparency teams need to operate confidently.

Managing the statute of limitations on debt in NY is critical for collection agencies and credit issue companies. Missing deadlines can lead to dismissed cases, compliance issues, and wasted legal spend. Time-barred accounts require careful handling, while litigation-eligible accounts need to be prioritized to protect recoveries.

Tratta gives you visibility into every account, enforces limitation rules automatically, and organizes workflows, so your team can manage New York portfolios confidently. To see Tratta in action and understand how it can reduce risk while improving recoveries, schedule a demo today.

Yes. Consumer credit has shorter limitation periods, while most commercial debts follow six-year rules. Agencies must classify accounts correctly to apply the appropriate statute-of-limitations timeline.

Yes. Bankruptcy can temporarily pause collection actions, effectively tolling the statute. Limitation timelines resume after discharge or closure, depending on federal and state bankruptcy rules.

Yes, only if a written agreement explicitly acknowledges debt and resets the timeline. Otherwise, informal arrangements do not legally extend the statute of limitations.

Agencies must apply each state’s rules separately. Cross-state portfolios require tracking limitation periods individually to avoid misfiling or compliance violations.

Yes. Missing or inaccurate digital records can create disputes over default dates. Agencies must validate data integrity to maintain enforceability and prevent legal or compliance issues.