The Complete CFPB Compliance Checklist for Collection Agencies

Debt Collection & Recovery Software

The Complete CFPB Compliance Checklist for Collection Agencies

Published on:

April 15, 2026

A single missed disclosure or improperly timed communication can trigger a complaint, disrupt recovery efforts, and expose your agency to regulatory action. For collection teams operating at scale, maintaining consistent compliance across accounts, channels, and agents is increasingly difficult.

The pressure is only intensifying. According to the Consumer Financial Protection Bureau, over 207,800 debt collection complaints were filed in a single year. This level of scrutiny leaves minimal tolerance for operational gaps. This is where a CFPB compliance checklist becomes essential.

In this article, we outline what it should include, highlight common gaps, and explain how to implement it effectively across your operations.

Brief look:

Compliance is operational, not theoretical. Regulation F defines strict requirements across validation, communication, disputes, and documentation, and even small gaps can trigger complaints or enforcement action.

Core areas must work together. Validation notices, communication limits, consumer rights, prohibited practices, handling of time-barred debt, and recordkeeping collectively define compliant collection workflows.

A checklist turns rules into action. Structuring compliance into lifecycle stages, from account intake to resolution, ensures consistent execution across teams and accounts.

Most failures come from execution gaps. Inconsistent processes, manual tracking, poor visibility, and fragmented systems create risk even when teams understand the rules.

System-driven compliance is essential at scale. Embedding controls into workflows improves consistency, reduces human error, and enables audit-ready operations in high-volume environments.

What Is a CFPB Compliance Checklist?

A CFPB compliance checklist is a structured framework that helps collection agencies align their operations with the requirements of Regulation F. It is not an official document issued by regulators, but a practical way to translate legal obligations into clear, repeatable actions across workflows. Instead of relying on individual judgment, it ensures that each account is handled consistently and in compliance.

A typical checklist outlines the following core elements:

Defined Compliance Actions: Lists required steps such as sending validation notices, handling disputes, and following communication rules.

Clear Timelines: Specifies when actions must occur, including the delivery of notices and the opening and closing of dispute windows.

Standardized Data Requirements: Outlines what information must be included in communications and records.

Process-Level Controls: Connects compliance requirements to specific stages in the collection workflow.

Documentation Expectations: Identifies what must be recorded to demonstrate compliance during audits or disputes.

Defining the checklist is only the starting point. The real challenge lies in ensuring it is consistently followed across teams and systems. The next section lists the need to follow compliance checklists diligently.

Agencies like the Federal Trade Commission continue to take action against non-compliant collectors, including court-ordered bans that permanently prohibit companies from operating in the industry. These actions are typically tied to repeated violations, deceptive practices, or failure to follow consumer protection laws.

Ignoring structured compliance frameworks exposes agencies to risks that extend beyond fines:

Regulatory Enforcement Actions: Non-compliance can lead to lawsuits, penalties, and, in severe cases, permanent bans from operating.

Operational Inconsistency: Without defined frameworks, agents handle accounts differently, increasing the likelihood of violations.

Increased Complaint Volume: Poor compliance practices often result in consumer disputes and escalations.

Client and Partner Risk: Creditors and partners expect strict compliance, and failures can result in lost contracts.

Reputational Damage: Regulatory actions and complaints can impact long-term credibility and growth.

Tratta addresses this challenge by embedding compliance directly into your collection workflows. It enforces rules across communications, payments, and account handling, reducing reliance on manual oversight. This allows agencies to scale operations while maintaining consistent, audit-ready compliance. Schedule a free demo today.

Essential Compliance Areas Every Collection Agency Must Cover

Compliance in collections spans multiple statutes, timelines, disclosures, and operational controls that must work together across every account. Missing even one requirement can trigger disputes, complaints, or enforcement action.

This is a structured view of the core areas that define compliant operations:

Under Regulation F, collectors must provide a validation notice either in the initial communication or within five days. This notice must clearly outline the debt, the creditor, and the consumer’s rights to dispute or request information. Errors in timing, formatting, or content are among the most common compliance failures.

The following points outline what must be included in every validation notice:

The total debt amount, with a clear breakdown of charges

The name of the current creditor and account reference details

A clear statement of the consumer’s right to dispute within 30 days

Instructions on how to dispute or request original creditor information

Confirmation that the notice is sent within the required timeframe

Regulation F places strict limits on how and when collectors can communicate with consumers. These rules are designed to prevent harassment while ensuring transparency across all communication channels. Violations often occur when agencies lack centralized controls over outreach.

The following points define the communication controls agencies must enforce:

No more than seven calls within a seven-day period per account

No contact outside permitted hours based on the consumer’s location

Compliance with disclosure rules across all communication channels

Immediate honoring of opt-out and communication preferences

Restrictions on contacting third parties, such as employers or relatives

The Fair Debt Collection Practices Act (FDCPA) establishes clear protections for consumers, particularly during the validation period. Agencies must pause collection activity if a dispute is raised and provide verification before continuing. Mishandling disputes is a frequent source of complaints and enforcement actions.

The following points outline how disputes must be handled:

Consumers must be allowed to dispute within the 30-day validation period

Collection activity must stop until verification is completed

Verification documents must be provided when requested

All disputes must be tracked and documented accurately

Collectors are prohibited from using deceptive, unfair, or abusive practices under the FDCPA. This includes misrepresenting the nature of the debt or using aggressive or misleading tactics. These violations are among the most common triggers for regulatory action.

The following points outline prohibited practices:

Misstating the amount, status, or legal standing of a debt

Threatening legal action without intent or authority

When a debt is beyond the statute of limitations, collectors must follow additional restrictions. While collection may still be allowed in some cases, legal enforcement is not permitted. Failure to handle time-barred debt properly creates significant compliance risk.

The following points define how expired debt must be handled:

No lawsuits or threats of legal action on time-barred debt

Clear disclosure that the debt is not legally enforceable

Accurate identification of statute of limitations status

Transparent communication about repayment obligations

Regulation F requires collectors to maintain records that demonstrate compliance with all applicable rules. Without proper documentation, agencies cannot defend against disputes or regulatory audits. Recordkeeping is a foundational part of compliant operations.

The following points outline the required records:

Logs of all consumer communications across channels

Copies of validation notices and proof of delivery

Documentation of disputes and verification responses

Full payment and transaction history

Records demonstrating adherence to compliance requirements

Tratta uses a Compliance-by-Code approach to embed regulatory controls directly into collection workflows. It enforces rules automatically, secures sensitive data, and ensures consistent, audit-ready compliance at scale. Get in touch with us to learn more.

Practical Compliance Checklist for Collection Agencies

A structured checklist helps translate regulatory obligations into clear, repeatable actions that teams can follow without ambiguity.

Use this checklist to guide your operations across the full collection lifecycle:

Stage

Action

What to Ensure

Account Intake

Receive and log new debt account

Verify the completeness of account data, creditor details, and balance accuracy before any outreach

Validate account information

Confirm ownership, amount, and supporting documentation to avoid future disputes

Check time-barred status

Identify statute of limitations and flag accounts that require special handling

Initial Communication

Send validation notice

Deliver within the required timeframe with all mandatory disclosures

Include consumer rights

Clearly explain dispute rights and how to respond

Use compliant templates

Ensure formatting and language meet regulatory standards

Early Outreach

Initiate contact with the consumer

Follow approved channels and maintain proper disclosures

Track communication attempts

Monitor frequency to stay within permitted limits

Respect timing rules

Contact only during allowed hours based on the consumer's location

Ongoing Communication

Manage call frequency

Ensure outreach does not exceed allowed attempt limits

Handle opt-outs and preferences

Immediately update systems to reflect consumer communication choices

Maintain consistent messaging

Avoid misleading or inconsistent information across channels

Dispute Handling

Receive and log disputes

Record all disputes with timestamps and relevant details

Pause collection activity

Stop all collection efforts until verification is completed

Provide verification

Share required documentation clearly and promptly

Payment and Resolution

Offer payment options

Ensure terms are transparent and compliant

Process payments securely

Maintain accurate records of all transactions

Confirm settlements

Provide clear confirmation of resolved accounts

Special Cases

Handle time-barred debt

Avoid legal threats and include required disclosures

Manage vulnerable consumers

Adjust the communication approach where required

Recordkeeping

Maintain communication logs

Track all calls, messages, and outreach attempts

Store notices and documents

Keep copies of validation notices and dispute responses

Ensure audit readiness

Maintain complete, accurate, and retrievable records

Ongoing Monitoring

Review compliance performance

Regularly audit processes and identify gaps

Update workflows

Adjust processes based on regulatory updates and findings

Even with a structured checklist covering each stage, many agencies still face compliance failures. The issue is not the absence of steps, but gaps in the consistency with which those steps are executed across teams and systems.

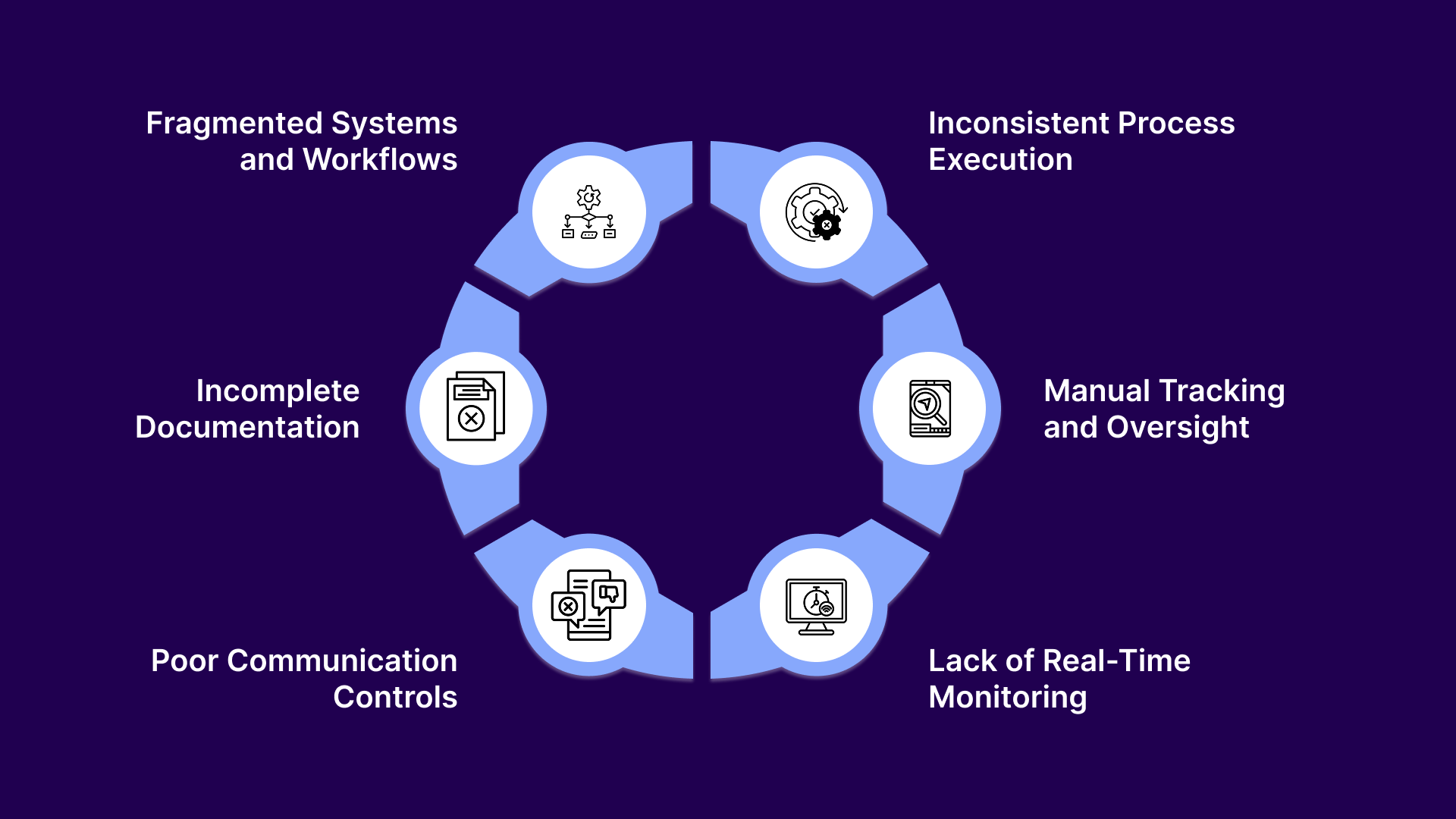

Common Gaps That Lead to Compliance Failures in Debt Collection

Most compliance failures happen because execution breaks down across systems, teams, and high-volume workflows. Small inconsistencies compound quickly, creating gaps that expose agencies to complaints, disputes, and regulatory action.

These are:

Inconsistent Process Execution: Different agents handle accounts differently, leading to missed steps and non-standard communication. This variability increases the risk of violating required disclosures and timelines.

Manual Tracking and Oversight: Relying on spreadsheets or disconnected systems makes it difficult to enforce compliance consistently. Critical actions such as notice delivery or dispute handling can be missed or delayed.

Lack of Real-Time Monitoring: Without visibility into ongoing operations, agencies cannot identify compliance issues as they happen. Problems are often discovered only after complaints or audits.

Poor Communication Controls: Managing call limits, timing, and opt-outs across multiple channels becomes difficult without centralized systems. This often leads to over-contacting or non-compliant outreach.

Incomplete Documentation: Missing or inconsistent records make it difficult to prove compliance during audits or disputes. Even compliant actions can become liabilities if they are not properly documented.

Fragmented Systems and Workflows: When tools do not integrate, compliance steps fall through the cracks between processes. This creates gaps in enforcement and accountability.

Addressing these gaps requires more than awareness or training. Agencies need systems that enforce compliance consistently, reduce manual intervention, and provide full visibility across operations. This is where the right technology becomes critical.

Turn Compliance Into a Repeatable System With Tratta

Tratta is a digital debt collection platform designed to help agencies operationalize compliance across every stage of the collection lifecycle. Instead of relying on manual processes, it connects communications, payments, workflows, and reporting into a single system that enforces consistency and control.

Tratta follows a Compliance-by-Code approach, embedding regulatory requirements directly into workflows while protecting sensitive data through encryption, access controls, and secure integrations. This ensures agencies can operate with confidence, knowing compliance is enforced automatically rather than dependent on manual oversight.

Beyond compliance, Tratta helps agencies improve recovery performance, optimize operations, and deliver a better consumer experience through its full feature set:

Consumer Self-Service Payment Portal: Enables consumers to view accounts, make payments, and set up plans independently. This reduces the agent's workload while increasing resolution speed and payment conversion rates.

Payments and Merchant Services: Provides secure, flexible payment processing across multiple methods. It simplifies reconciliation while ensuring transactions remain compliant and traceable.

Multilingual Payment IVR: Allows consumers to make payments through an automated voice system in multiple languages. This expands accessibility while maintaining consistent compliance controls.

Omnichannel Communications: Centralizes SMS, email, and voice communication into a single system. It ensures messaging remains consistent, compliant, and aligned across all channels.

Campaign Management: Automates outreach using segmentation and rule-based triggers. It helps agencies deliver the right message at the right time while maintaining compliance across campaigns.

Reporting and Analytics: Offers real-time insights into performance, consumer behavior, and compliance metrics. This allows agencies to identify risks early and optimize strategies effectively.

Customization and Flexibility: Gives agencies control over workflows, messaging, and operational rules. This ensures processes align with both compliance requirements and business needs.

Integrations (APIs): Connects seamlessly with existing systems for real-time data synchronization. This eliminates silos and ensures compliance is maintained across the entire tech stack.

Contact Center: Supports agent-driven interactions with full visibility into account history and compliance requirements. It ensures human interactions remain consistent with system-enforced rules.

Tratta is built for agencies that prioritize compliance and need it enforced consistently at scale. From day one, a dedicated onboarding specialist configures your payment rules, SoR integrations, consumer portal branding, and campaign logic to match your operations. With no onboarding or setup fees, your team is equipped to go live quickly and start collecting with confidence.

Conclusion

Without a structured approach to compliance, collection operations become vulnerable to inconsistency, missed requirements, and regulatory exposure. What often starts as a small oversight can quickly escalate into complaints, disputes, or enforcement action, especially in high-volume environments where manual processes cannot keep pace.

Tratta helps eliminate these risks by embedding compliance directly into your workflows, ensuring every action aligns with regulatory requirements. With built-in controls, automation, and real-time visibility, it enables agencies to operate with confidence while improving efficiency and recovery outcomes.

Start building a more controlled, compliant collection operation today. Get in touch with us.

Frequently Asked Questions

1. What are the 5 key areas of compliance in debt collection?

The five key areas include validation notices, communication rules, consumer rights and dispute handling, prohibited practices, and recordkeeping. Together, these ensure compliant, consistent, and auditable collection operations.

2. What are the requirements under CFPB complaint guidelines?

Collectors must provide accurate information, avoid deceptive practices, and respond appropriately to disputes. Complaints often arise from poor communication, incorrect balances, or failure to follow Regulation F requirements.

3. What are compliance checklists in debt collection?

Compliance checklists are structured frameworks that translate legal requirements into actionable steps. They help agencies ensure every account follows proper timelines, disclosures, and documentation standards consistently.

4. What is Regulation F in debt collection?

Regulation F, issued by the Consumer Financial Protection Bureau, implements the Fair Debt Collection Practices Act, defining communication limits, disclosures, and digital outreach rules agencies must follow to remain compliant.

5. Why is recordkeeping important for CFPB compliance?

Recordkeeping helps agencies prove compliance during audits and disputes. The Consumer Financial Protection Bureau expects clear documentation of communications, consent, and resolutions to ensure accountability and defensibility.

Note: This information is not legal advice. Tratta recommends that you consult with your legal counsel to make sure that you comply with applicable laws in connection with your collection and outreach activities.

Sign up for our monthly newsletter

Debt collection insights that keep you compliant and competitive.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

.jpg)