Are your agents spending too much time chasing overdue accounts while payment updates, outreach records, and reporting sit in different tools?

For debt collection agencies, improving accounts receivable collection is not just about contacting more consumers. It is about making payments easier, giving agents better account visibility, and reducing manual work without losing control of the process. These priorities also matter for credit issuers and original creditors that manage overdue accounts internally or work with agency partners.

With U.S. household debt reaching $18.8 trillion in Q1 2026 and 4.8% of outstanding debt already in some stage of delinquency, collection agencies are under more pressure to recover overdue balances without adding more manual work.

This blog explores 9 practical tips to improve accounts receivable collection, support agent efficiency, and create a smoother payment experience for consumers.

Accounts receivable (AR) collection is the process of tracking unpaid balances, contacting consumers about overdue accounts, and helping recover payments owed to a creditor. For debt collection agencies, it also includes managing payment options, follow-up timelines, account records, and reporting across a large number of accounts.

For credit issuers, AR, and operations leaders, AR collection is not only a finance task. It is a workflow challenge that affects agent productivity, consumer payment experience, reporting visibility, and the agency’s ability to recover overdue balances at scale.

Once the basics are clear, the next step is to understand the practical tips agencies can use to improve recovery workflows.

Also Read: 10 Accounts Receivables Software Helping Agencies Get Paid Faster 2026

Debt collection agencies can improve accounts receivable collection by reducing manual work, using better account data, and giving consumers easier ways to resolve overdue balances. The goal is to help teams recover more efficiently while maintaining control over workflows, reporting, and consumer communication.

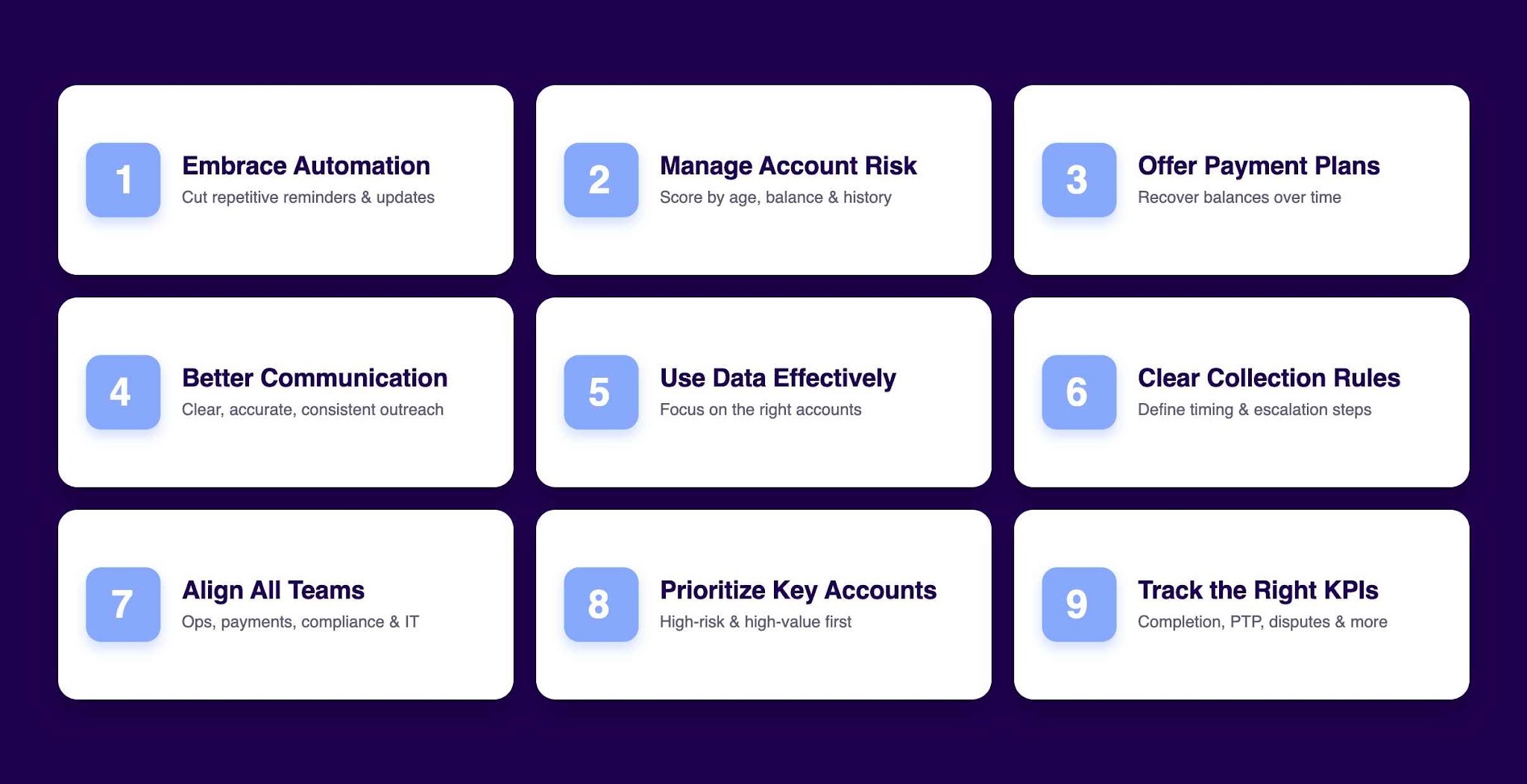

Here are 9 practical tips agencies can use to improve accounts receivable collection:

Automation can help agencies reduce repetitive tasks such as payment reminders, account updates, and basic follow-ups. This gives agents more time to focus on accounts that need direct attention, negotiation, or review.

For agency leaders, automation also supports more consistent workflows across teams, especially when handling large account volumes for multiple creditors or portfolios.

But how can agencies know whether their automated workflows are actually improving collection performance?

This is where Tratta’s Reporting and Analytics can help. Tratta provides real-time dashboards and reports that help track payment trends, consumer actions, channel performance, payment plan activity, failed payments, and account outcomes.

Collection agencies should understand which accounts carry a higher risk based on age, balance, payment history, dispute status, and recent engagement. This helps teams avoid treating every account the same.

When risk levels are clear, agencies can focus resources on accounts that need faster action, closer monitoring, or a different follow-up approach. This also helps credit issuers and original creditors get clearer visibility into how placed accounts are being managed.

Some consumers may not be able to pay the full balance at once, but they may be able to commit to structured payments. Payment plans can give agencies a practical path to recover balances over time.

For agencies, clear payment plan options can also reduce repeated calls, missed commitments, and confusion around next steps.

Strong communication helps agencies create clearer, more professional interactions with consumers. This does not mean being overly casual; it means giving consumers accurate account details, clear payment options, and consistent follow-up.

When communication is easy to understand, consumers are more likely to know what they owe, what options they have, and how to take action.

Agencies should use account data to understand which consumers are paying, which accounts are inactive, and which outreach channels are working. Without this visibility, teams may spend time on the wrong accounts.

Data can also help owners, COOs, and operations leaders review performance across agents, campaigns, portfolios, creditors, and payment channels. For credit issuers, this reporting can also provide better insight into account recovery trends.

Even when agencies are not the original creditor, they still need clear collection rules for each client, portfolio, or account type. These rules should define follow-up timing, payment options, escalation steps, documentation needs, and communication guidelines.

Clear rules help agents work more consistently and reduce confusion between operations, payment teams, compliance reviewers, and creditor stakeholders.

AR collection does not depend only on agents. Payment operations, compliance, IT, reporting teams, and client-facing teams all affect how smoothly accounts move through the workflow.

When these teams are aligned, agencies can reduce delays caused by system issues, unclear policies, missing data, or disconnected reporting. This is especially important for agencies working with multiple creditors that have different account rules or reporting needs.

Agencies should first identify accounts that need attention, such as high-balance accounts, recently engaged consumers, broken payment plans, disputed accounts, or accounts close to important workflow deadlines.

Prioritization helps agents spend time where it can have the most impact instead of working through accounts only by age or list order. It also gives leadership a clearer view of where to focus collection activity.

Agencies need more than basic collection totals to understand performance. Useful KPIs may include payment completion rate, promise-to-pay kept rate, inactive accounts, failed payments, self-service adoption, agent productivity, dispute volume, and channel performance.

Tracking the right KPIs gives leadership better visibility into what is working, where accounts are slowing down, and where workflows need attention. For credit issuers and original creditors, these KPIs can also support better oversight of recovery performance.

Next, let’s look at why the accounts receivable collection process matters.

A strong accounts receivable collection process helps to recover overdue balances in a more organized and measurable way. It gives teams a clear structure for tracking accounts, following up with consumers, managing payments, and reporting results across recovery workflows.

AR collection process matters because it can:

To see why the process matters, it is useful to look at how accounts typically move through placement, payment, dispute resolution, or closure.

The accounts receivable collection process is the structured workflow agencies use to recover balances on behalf of creditors. For debt collection agencies, this process must be clear, consistent, and easy to monitor across large volumes of accounts.

Here are the key steps in the accounts receivable collection process for agencies:

The process usually begins when a creditor places overdue accounts with the agency. Before outreach begins, the agency should validate key account details, including balance, consumer contact information, payment history, account status, and any supporting documentation.

This step helps reduce errors that can delay collections or create unnecessary back-and-forth between agents, consumers, and creditors.

Agencies need a clear view of the account terms, outstanding balance, payment options, and any creditor-specific rules. This helps agents explain the account accurately and gives payment operations teams a consistent process to follow.

When account information is easy to access, agencies can reduce confusion and give consumers a clearer path to resolution.

Once the account is active in the collection workflow, agencies track payment activity, missed payments, payment plan status, and consumer engagement. Reminders may be sent before or after due dates, depending on the agency’s workflow and communication policies.

This step is important for scaling outreach without placing all follow-up work on agents.

Collection teams then prioritize accounts for follow-up based on account age, balance, payment behavior, consumer response, and previous outreach activity. Follow-ups may happen through calls, emails, text messages, letters, or self-service payment reminders.

For agency leaders, this is where agent efficiency matters most. A clear follow-up process helps teams focus on the right accounts instead of spending time on scattered manual tasks.

But how can agencies keep follow-ups consistent across channels without adding more work for agents?

Tratta’s Omnichannel Communications can help agencies manage outreach across email, SMS, chat, phone, bilingual IVR, and QR-code letters from one platform. It supports channel-specific routing, branded email and SMS templates, automated outreach, payment-plan reminders, and event-triggered messaging based on payment activity or dispute status.

Some accounts may need additional action if they remain unpaid or inactive. Agencies may move these accounts into defined escalation workflows, such as revised payment plans, settlement review, supervisor involvement, or client-specific next steps.

Escalation should follow internal policies and applicable compliance guidance to ensure the process remains controlled and well-documented.

If a consumer raises a dispute regarding the balance, account details, payment history, or creditor information, the agency needs a clear process for investigating and resolving the dispute. Delays in dispute handling can slow down collections and affect reporting accuracy.

Once the payment is completed, the account is resolved, or the creditor provides further direction, the agency should update records and close the workflow properly.

Even with a clear process, some mistakes can slow recovery.

What Should You Avoid When Improving AR Collection?

Improving AR collection should not create more manual work, disconnected workflows, or payment friction. Collection agencies should avoid mistakes that weaken visibility, slow agents down, or make it harder for consumers to pay.

Here are the key mistakes:

After identifying what to improve and what to avoid, the next question is how agencies can support these workflows with the right technology.

Also Read: Accounts Receivable Dashboard: Examples And Benefits

For many debt collection agencies and credit issuers, AR collection becomes harder when payment tools, outreach channels, account data, and reporting are spread across different systems.

Tratta is debt collection software for agencies, law firms, credit issuers, and debt buyers. It helps recovery teams consolidate consumer payments, digital communications, reporting, integrations, and compliance-aware workflows into a single platform, enabling better visibility and control over collection activity.

Tratta supports better accounts receivable collection through:

If you are trying to improve AR collection, Tratta is designed to reduce fragmented workflows, improve reporting visibility, and give consumers clearer ways to resolve overdue balances.

Improving accounts receivable collection takes more than frequent follow-ups. Debt collection agencies need clear account data, consistent workflows, practical payment options, and better visibility into what is happening across accounts. When teams reduce manual work, prioritize the right accounts, track useful KPIs, and make payments easier for consumers, they can manage recovery workflows with more control and less operational friction.

Tratta supports this need as debt collection software built for agencies, law firms, credit issuers, and debt buyers. Our platform brings consumer payments, digital communications, reporting, integrations, and compliance-aware workflows into one place, helping recovery teams reduce disconnected processes and give consumers clearer ways to resolve overdue balances.

So, schedule your demo today. If your team is ready to improve accounts receivable collection with better payment access, reporting, and self-service workflows, Tratta can help you take the next step!

Account segmentation helps agencies group accounts by factors such as balance, age, payment history, dispute status, and recent activity. This prevents teams from treating every account the same and helps agents focus on accounts that need the right level of attention.

Disconnected systems make it harder for agents, payment teams, IT, and leadership to see the same account information. When payment records, outreach history, IVR activity, and reporting are split across tools, teams may face duplicate work, delayed updates, and weaker visibility.

Payment plans can give consumers a structured way to resolve overdue balances when they cannot pay in full at once. For agencies, clear payment plan workflows help reduce repeated follow-ups, track commitments, and create a more manageable path to account resolution.

Agencies should look for software that supports payments, communication, reporting, integrations, self-service, and compliance-aware workflows within a single connected system. The right platform should help teams reduce manual work, improve visibility, and give consumers easier ways to pay.

Digital payment options make it easier for consumers to review balances and pay through convenient channels. This can help agencies reduce payment friction, lower routine call volume, and make payment activity easier to track.