Late payments, rising account volumes, and stricter compliance rules are making risk harder for collection agencies to control. What once felt like routine recovery work is now a complex financial operation where small inefficiencies can quickly turn into portfolio losses.

The scale of the industry reflects that pressure. The accounts receivable collection services market was valued at about $13.60 billion globally. This highlights how large and competitive the recovery landscape has become.

Agencies need structured ways to identify, measure, and reduce their accounts receivable risk before it affects performance. In this guide, we break down what creates that risk, how it affects collection agencies, and the strategies to manage it effectively.

Accounts receivable risk management is the structured process of identifying, monitoring, and reducing the likelihood that outstanding balances will remain unpaid. For collection agencies, this means assessing portfolio health, prioritizing recovery actions, and ensuring that accounts do not age into losses.

Effective accounts receivable risk management usually involves several coordinated practices. These are:

Because aging directly influences collectability, unmanaged portfolios quickly accumulate higher-risk accounts. This makes it essential to understand what happens when agencies overlook accounts receivable risk in the first place.

Suggested Read: Accounts Receivable Management: Tips and Process Guide

Problems build gradually as accounts age, communication becomes inconsistent, and recovery efforts lose momentum. What begins as a few delayed payments can quickly turn into a portfolio-wide performance issue for collection agencies.

The financial and operational impact includes:

Tratta helps agencies control accounts receivable risk with automated outreach, flexible digital payment options, and real-time portfolio reporting. These tools help you keep accounts moving and reduce aging balances before they turn into larger recovery problems. Schedule a free demo today.

Collection agencies need to understand these categories to prioritize accounts and intervene before recovery becomes unlikely.

Common types of accounts receivable risk include:

The consumer may never repay the balance or may stop making payments entirely. For collection agencies, this is the most direct threat to recovery performance and portfolio value.

As accounts remain unpaid longer, the probability of collection declines. Aging reports exist specifically to identify overdue balances and determine when accounts may become uncollectible.

Consumers may challenge balances, account ownership, fees, or documentation. These disputes slow recovery timelines and often require verification, investigation, or legal review.

Internal inefficiencies such as missed follow-ups, poor account segmentation, outdated contact data, or manual workflows can allow accounts to age unnecessarily.

Debt collection regulations govern when and how agencies communicate with consumers. Mistakes in outreach, disclosures, or documentation can create legal exposure alongside financial loss.

These risks can help agencies get a clearer picture of portfolio exposure. The next step is evaluating that exposure through a structured accounts receivable risk assessment.

Suggested Read: Accounts Receivable Dashboard: Examples And Benefits

A structured assessment can help your team identify vulnerable accounts, prioritize recovery actions, and prevent balances from aging into losses.

A practical accounts receivable risk assessment typically involves the following steps:

Conducting this type of assessment gives agencies a clearer understanding of where exposure exists across the portfolio. The next section reveals the underlying factors that create receivable risk in the first place.

Suggested Read: Top 10 KPI Metrics for Effective Tracking of Accounts Receivable

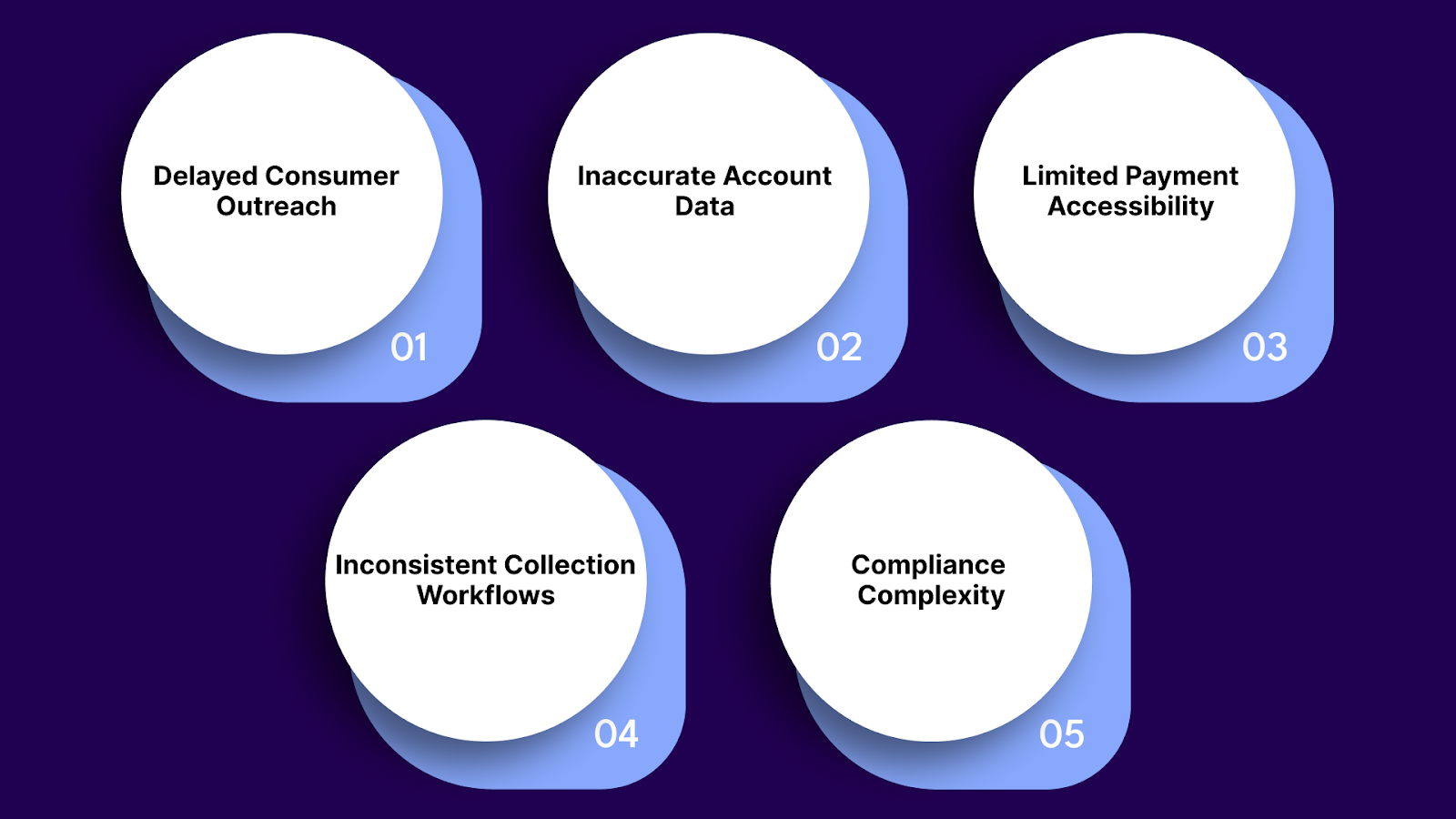

Identifying the causes helps agencies prevent accounts from aging into difficult or uncollectible balances.

These are the common factors that lead to accounts receivable risk in collections:

When outreach begins too late, consumers are less likely to respond or prioritize repayment. Early engagement plays a major role in maintaining recovery momentum.

Delayed outreach creates the following recovery challenges:

Collection outcomes depend heavily on reliable account information. Missing documentation or incorrect contact details can slow recovery efforts.

Poor data increases collection risk:

Even willing consumers may delay payment if the process is inconvenient. Friction in payment options often extends the life of receivables.

Limited payment options can slow resolution:

Without structured processes, accounts may fall through operational gaps. This often results in missed follow-ups and uneven outreach.

Unstructured workflows allow accounts to age because of:

Debt collection regulations shape how and when agencies can communicate with consumers. Managing these requirements adds another layer of operational risk.

Regulatory complexity adds operational pressure in the following manner:

Tratta helps agencies address many of these challenges through campaign outreach, digital payment options, structured workflows, and portfolio reporting. Teams can stay consistent while reducing accounts receivable risk across their operations. Learn more.

Agencies that implement clear strategies early can prevent accounts from aging into difficult recoveries. These strategies can help you reduce risk with your receivables:

Focus efforts where risk is highest:

Maintain consistent outreach:

Make payments easier:

Keep account data reliable:

Track results continuously:

Applying these strategies helps agencies reduce exposure across their portfolios and keep accounts moving toward resolution. The next step is strengthening day-to-day operations with proven best practices.

Small operational habits often determine whether accounts move toward resolution or continue aging in the portfolio. Adopting the following practices helps agencies control receivable risk on a day-to-day basis:

Strong operational habits lay the foundation for effectively managing receivable risk. However, maintaining consistency across large portfolios becomes significantly easier when supported by the right software.

Tratta is a collections-focused software platform designed to help agencies improve recoveries, simplify outreach, and give consumers easier ways to resolve debts. Instead of relying on disconnected tools, agencies can manage communication, payments, and reporting in one system.

The following features improve visibility across portfolios and help teams reduce accounts receivable risk before balances age further:

Enables secure, integrated payment processing, enabling consumers to complete transactions quickly through digital channels.

Combines email, text, and other outreach channels so agencies can reach consumers more consistently and maintain momentum in the recovery process.

Helps teams automate outreach, schedule communications, and guide consumers toward resolution through structured engagement.

Provides real-time visibility into payments, outreach performance, and account activity so agencies can identify risk and optimize strategies.

Allows agencies to configure workflows, rules, and account handling processes to match their risk management strategies and prevent receivables from aging unnecessarily.

Connects with existing systems and data sources to give teams a complete view of receivables, reducing data gaps that can increase accounts receivable risk.

Built with safeguards, audit trails, and oversight tools that help agencies manage receivables while maintaining regulatory compliance and operational accountability.

When these features work together, agencies gain stronger control over their portfolios and can respond faster when accounts show signs of risk. This is evident from the following case study.

Collections law firm Couch Lambert, LLC, adopted Tratta to optimize payment processing, automate outreach, and improve compliance across its recovery operations.

The firm handles consumer and commercial receivables, making operational efficiency critical to reducing aging accounts.

Tratta helped ensure that:

By giving consumers self-service payment options and automated communication, the firm improved collections. They also reduced operational friction across its receivables workflow.

Poor accounts receivable risk management can quietly undermine a collection agency’s performance. Without clear visibility and structured processes, small gaps in outreach or data management can turn into long-term financial losses.

Tratta helps agencies bring structure and clarity to the collections process. With automated communications, portfolio reporting, and configurable workflows, teams can reduce aging accounts while improving consumer engagement.

See how Tratta helps collection agencies improve outreach, simplify payments, and accelerate recoveries. Speak to us today.

Accounts receivable risks include non-payment, delayed payments, disputes, inaccurate account data, and compliance exposure. For collection agencies, these risks increase as accounts age and consumer engagement declines.

The four commonly recognized types are credit risk, aging risk, operational risk, and compliance risk. Each affects how likely a receivable is to be recovered and how efficiently agencies can manage portfolios.

The biggest issue is delayed or missed payments. As balances remain unresolved, recovery becomes more difficult, operational costs increase, and portfolio performance begins to decline.

Common red flags include rapidly aging accounts, repeated payment defaults, incomplete documentation, frequent disputes, and declining consumer response rates.

Agencies reduce risk by prioritizing high-risk accounts, maintaining accurate data, ensuring consistent outreach, offering flexible payment options, and using technology to monitor portfolio performance.