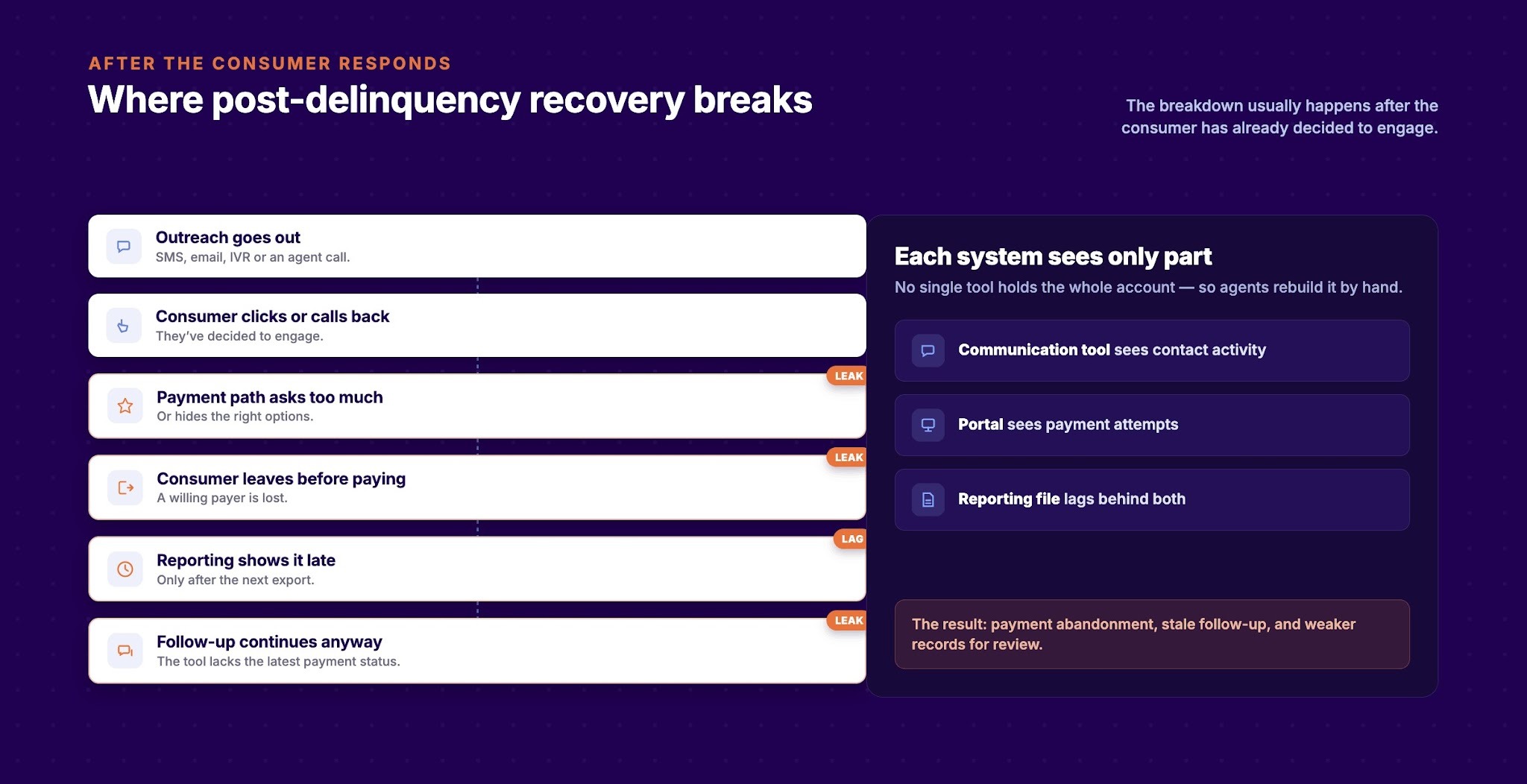

Issuer AR teams can lose recoverable balances even when outreach volume is high. In many cases, the breakdown happens after the consumer has already decided to engage.

A payment link opens a generic portal. Verification takes too long. Plan options are unclear. Account status updates late. The next message still goes out after a payment attempt. Agents then spend valuable time piecing together records before they can move unresolved accounts forward.

The scale of that challenge remains significant. Federal Reserve data published through FRED shows credit-card charge-off rates at all commercial banks were 3.84% in Q1 2026. The New York Fed reported that 4.8% of outstanding household debt was in some stage of delinquency in Q1 2026.

Credit operations improvement for credit issuers means strengthening the post-delinquency account path by connecting payments, outreach, reporting, and workflow controls.

The first weak point usually appears after the consumer responds. Your team may send the right message through the right channel, but the next step can still break.

A common issuer workflow looks like this:

That failure is costly because each system sees only part of the account. The communication tool sees contact activity. The portal sees payment attempts. The reporting file may lag behind both. The agent has to connect the record manually.

Debt collection rules depend on the role, account type, state, vendor structure, and channel. The FDCPA defines “debt collector” separately from “creditor”, so issuers should confirm coverage and obligations with counsel.

The operational requirement is clear. Your team needs current records for contact attempts, paid status, disputes, consumer requests, and account changes. The CFPB’s Regulation F FAQs describe telephone-call frequency presumptions for debt collectors, including the standard around more than seven calls in seven consecutive days and the seven-day window after a conversation about a debt.

When records sit in separate tools, your compliance or vendor management team has to rebuild the account history later. That slows review and makes documentation less reliable.

Also Read: AI Delinquency Management in Collections: Why Recovery Still Falls Short

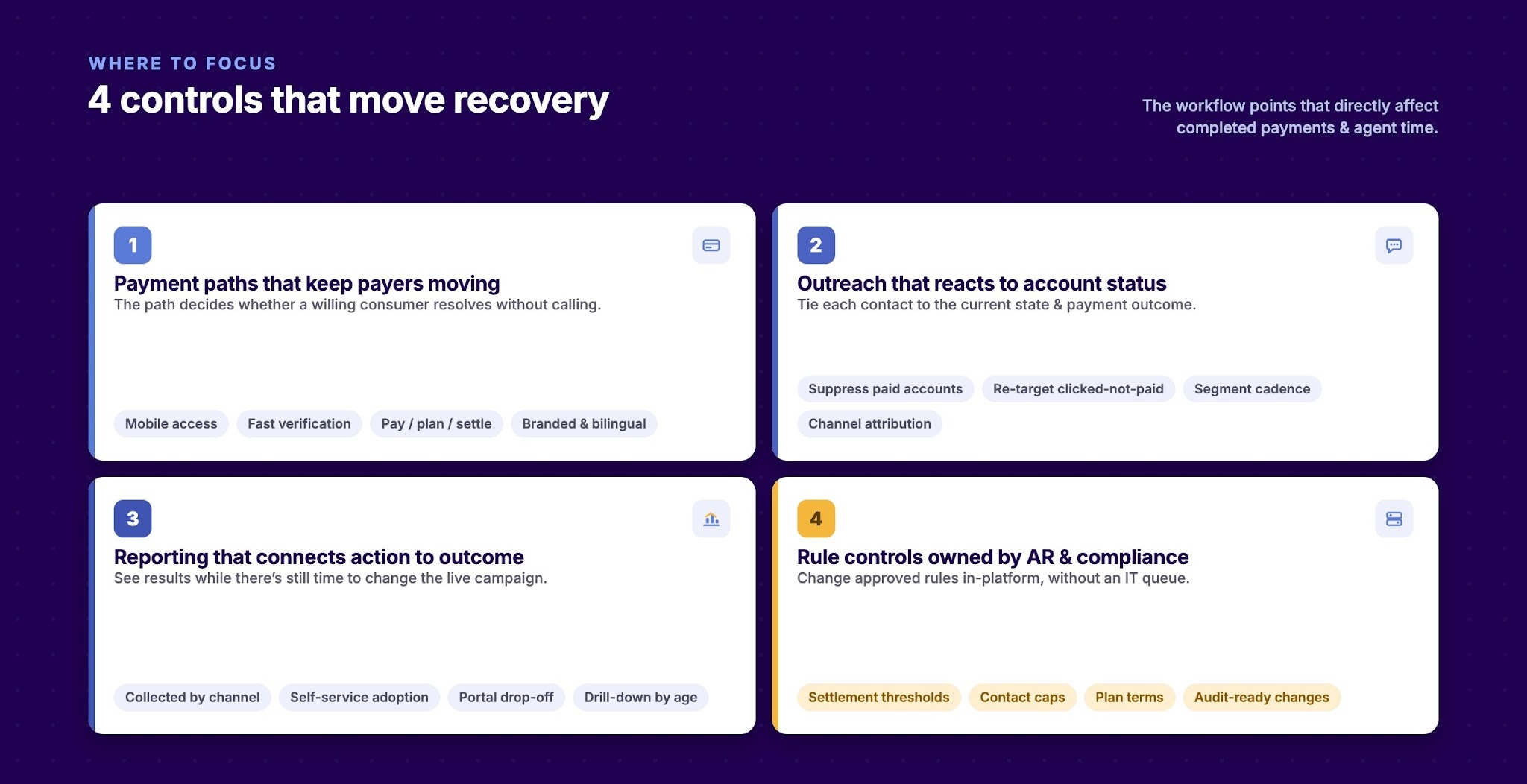

Credit operations improvement should focus on the workflow points that directly affect completed payments, agent time, and account documentation.

The payment path decides whether a willing consumer can resolve the account without calling your team.

For issuers, the branded experience matters because the consumer relationship may continue after recovery. A white-labeled path gives consumers a clearer signal that the payment experience belongs to the issuer or its approved recovery process.

Self-service adoption should sit on the same scorecard as recovery rate, call volume, and cost per collected dollar. If more consumers can complete approved actions on their own, agents can spend more time on accounts that need judgment.

Most issuers already use more than one contact channel. The harder problem is connecting each contact to the account state and payment outcome.

Your AR team should be able to answer:

When outreach is tied to current status, follow-up becomes cleaner. Paid accounts can be suppressed faster. Clicked-but-unresolved accounts can receive a more relevant next step. Your team can change campaign logic based on observed behavior without waiting for batch reports.

Many issuer AR teams have reports. Fewer have reports that connect the action to the outcome while there is still time to change the current campaign.

Useful recovery reporting should show:

This matters during the workday. If a payment link fails on mobile, you need to know before the next outreach run. If one account group responds to SMS but finishes payment through IVR, your channel plan should reflect that while the campaign is still active.

Issuer recovery teams often need different settlement thresholds, plan terms, contact caps, and escalation rules by portfolio type. When each change needs developer support, teams rely on manual notes, side files, or agent memory.

That creates avoidable risk. Policy can be applied unevenly. Rule changes become harder to audit. Agents spend more time interpreting account instructions.

Admin-level control lets AR and compliance owners manage approved rules inside the platform. Your team should be able to adjust settlement logic, contact rules, templates, and plan terms without waiting in an IT queue.

Also Read: Best Collection Dashboard Features for US Recovery Teams in 2026

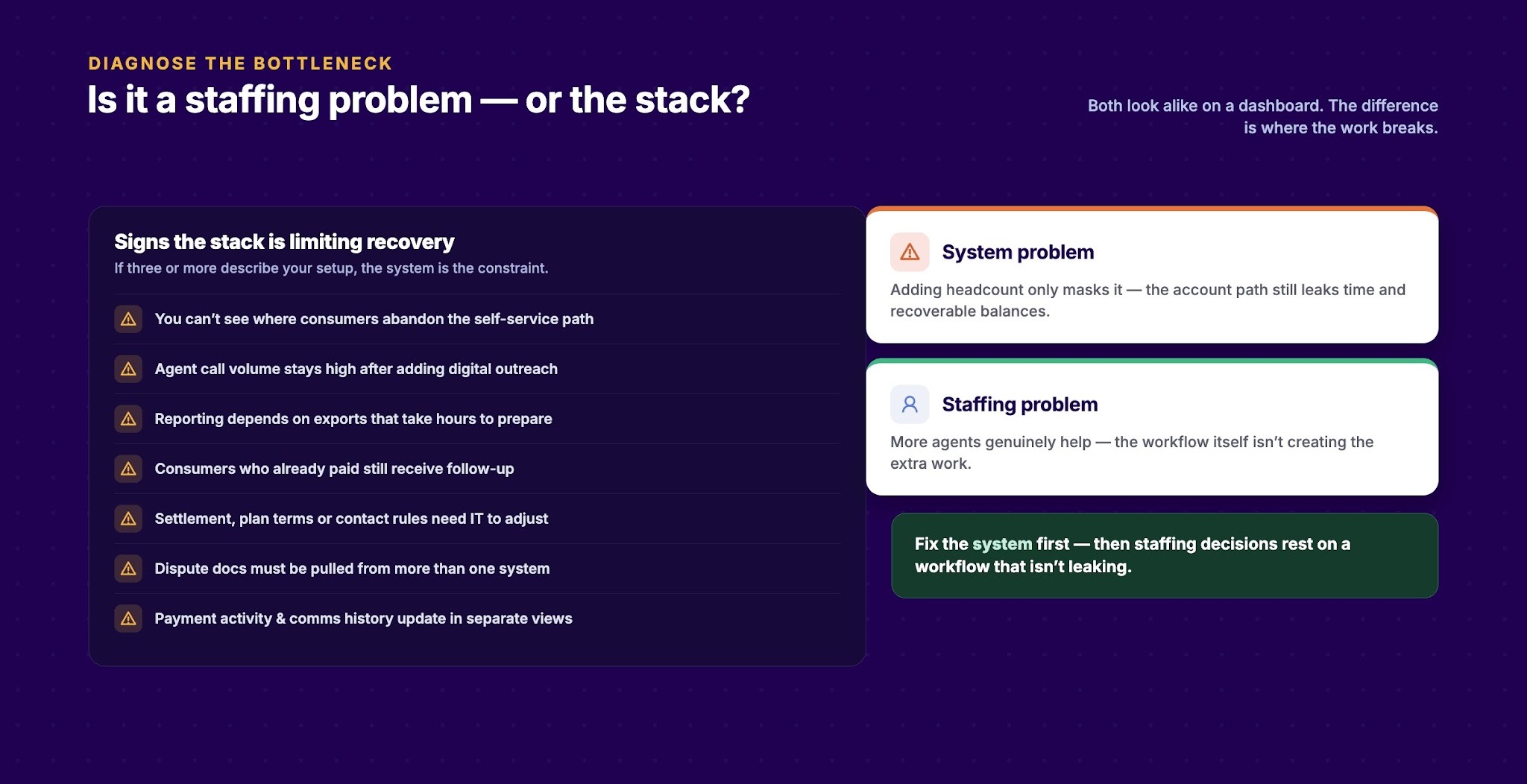

A staffing problem and a system problem can look similar from a dashboard. Both can create high call volume, slow account movement, and missed recovery goals. The difference is where the work breaks.

If three or more of these describe your current setup, the stack is likely limiting recovery:

These are process signals. Adding headcount may cover them for a short period, but the account path will still leak time and recoverable balances.

A recovery platform review should answer five practical questions:

Also Read: How Embedded Payments Help Collection Agencies Recover More in 2026

Tratta is debt collection software for credit issuers and recovery teams. It brings consumer payments, digital communications, reporting, and workflow controls into one platform for post-delinquency work.

For issuer teams evaluating recovery technology, the key consideration is how well the platform supports each stage of the post-delinquency workflow:

Tratta supports your recovery workflow through software. Your AR, IT, compliance, and customer-experience teams keep ownership of the account strategy and the creditor relationship.

Also Read: 2026 Guide to PCI-Compliant Card-Not-Present Debt Payments for Agencies

Credit operations improvement for credit issuers should change what happens after a consumer becomes delinquent.

The payment path should be easier to complete. Outreach should reflect current account status. Reporting should connect actions to outcomes. Workflow rules should be controlled by the teams responsible for recovery and review.

If your current setup creates the gaps above, schedule a demo with Tratta to see how a connected recovery workflow can support your issuer AR team.

AR or collections leadership should own the business case. IT should review system fit, data movement, security, and vendor support. Compliance or risk should review documentation, audit trails, communication controls, and how rule changes are managed.

Start with payment completion rate, self-service adoption, channel attribution, call volume, dispute volume, manual reporting time, and the number of accounts receiving outreach after payment. These metrics show whether the issue sits in staffing, channel strategy, or infrastructure.

Treat legal coverage as a counsel-led question. The platform review should focus on operational support: contact logs, current account status, configurable communication rules, dispute records, payment history, audit trails, and role-based access.

A payment portal mainly accepts money. A self-service recovery platform lets consumers view balances, confirm identity, choose approved payment options, access settlement offers where available, submit disputes, update preferences, and resolve more account actions without an agent.

IT should ask how data moves in and out, which APIs are available, how webhooks work, what security standards are met, how user permissions are controlled, what reporting exports are supported, and who handles support after launch.