Collection agencies are under pressure to recover more while dealing with slower payments, rising compliance demands, and increasing consumer friction. Embedded payments are emerging as a direct response to this challenge, helping agencies remove barriers and convert more interactions into actual payments.

The embedded payments market reached $39.14 billion in 2025 and is expected to grow at over 35.50% annually from 2026, signaling a clear move toward integrated, payment-first workflows.

If you are seeing lower conversions despite higher outreach, you are not alone. In this article, we break down how embedded payments help agencies recover more and where they drive the biggest impact.

Brief look:

Embedded payments in debt collection refer to features built directly into the systems and touchpoints agencies already use to engage consumers. Instead of sending someone to a separate portal or relying on agent-assisted transactions, the ability to pay is integrated into the interaction itself.

This becomes critical in a high-volume environment. Debt collection in the United States is a $15.10 billion industry, where recovery depends on how easily a consumer can act when they are ready. Embedded payments ensure that intent is not lost between communication and completion.

Embedded payment processing is useful in the following areas:

Embedded payments are not a separate layer added to collections. They are integrated into every stage where a decision can be made. In the next section, we will examine how this directly improves recovery outcomes for collection agencies.

Suggested Read: Collecting Payments: 7 Quick Tips for Debt Recovery Teams

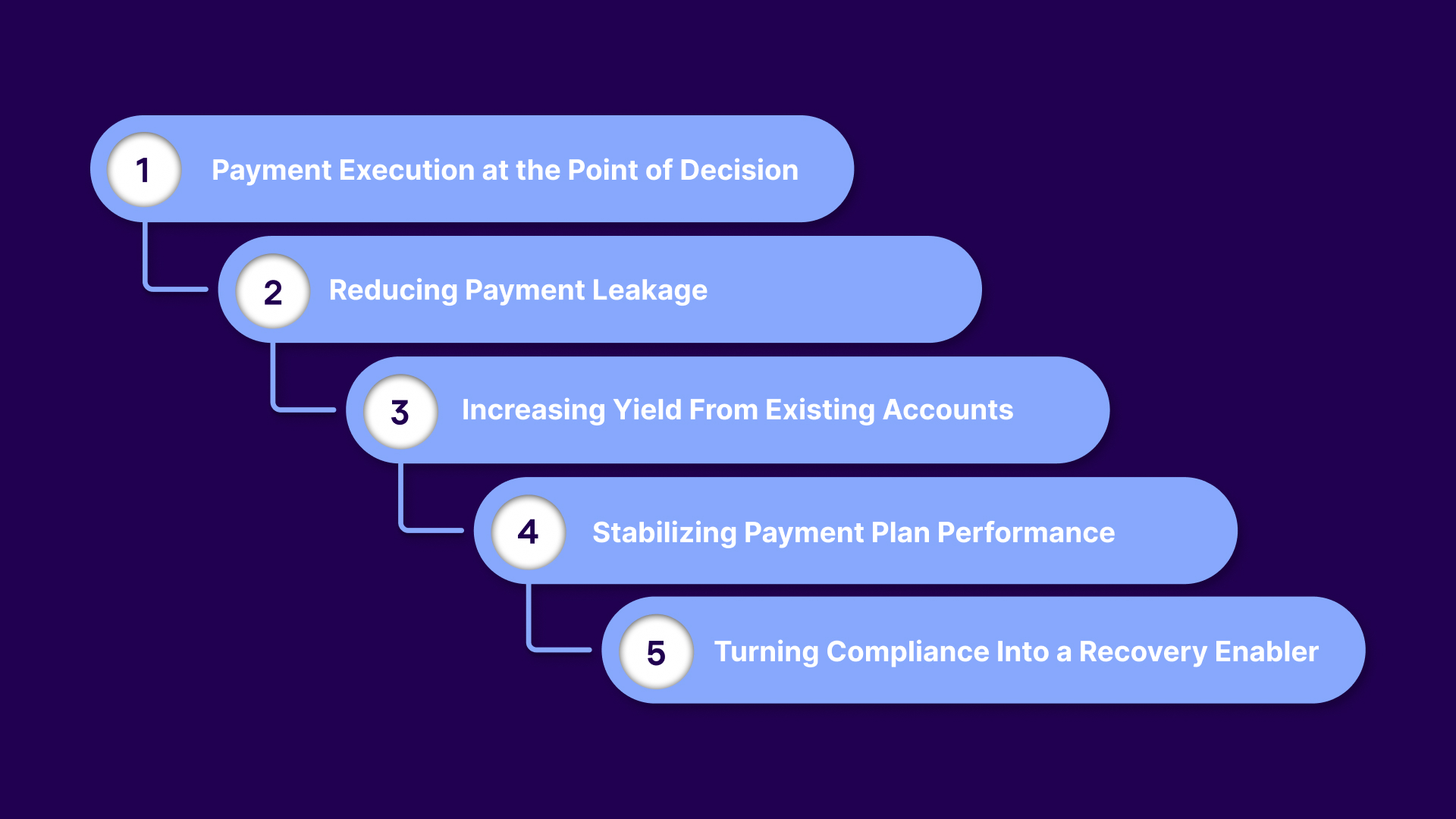

Recovery in third-party collections is not limited by outreach volume. It is constrained by how efficiently intent converts into completed payments.

Embedded payments improve recovery outcomes through the following:

Most recovery loss happens after a consumer decides to pay but before the transaction is completed. Embedded payments collapse that gap by enabling immediate execution within the same interaction, eliminating the need for follow-through behavior. This is where conversion rates are won or lost.

Key ways this improves recovery:

Tratta embeds payment capabilities directly into collection workflows. The infrastructure is designed to process payments within the same engagement layer, aligning communication and transaction into a single flow. This allows agencies to consistently convert intent into completed payments at scale. Schedule a free demo today.

Traditional collection workflows leak value at multiple stages, from initial contact to final settlement. Embedded payments processing addresses these drop-off points by ensuring that every stage of the journey includes a clear, immediate path to payment. This minimizes the cumulative loss that reduces overall recovery rates.

Key ways this improves recovery:

Most agencies focus on increasing contact rates, but embedded payments increase the yield from already-engaged accounts. By improving how payments are captured, agencies extract more value from the same portfolio without increasing operational effort. This directly impacts revenue without scaling costs.

Key ways this improves recovery:

Payment plans often fail due to friction in execution, not intent. Embedded payments make ongoing transactions easier to complete and manage, reducing missed payments and improving plan adherence over time. This creates more predictable recovery across longer cycles.

Key ways this improves recovery:

Compliance is often treated as a constraint, but embedded payment systems can turn it into a performance driver. By structuring payment interactions within controlled workflows, agencies reduce errors that delay or invalidate transactions. This ensures more payments are successfully completed without regulatory risk.

Key ways this improves recovery:

Embedded payments make recovery more predictable, measurable, and scalable. In the next section, we will look at the features agencies should prioritize when evaluating built-in payment solutions.

Suggested Read: How to Craft Payment Notices That Prompt Quick Replies

Choosing an embedded payment platform requires selecting infrastructure that directly impacts how efficiently intent converts into revenue. For collection agencies, the right features determine whether payments are captured consistently or lost across the workflow.

Table showing necessary features and their importance:

The feature set defines how well a platform performs under real collection conditions. Before choosing a solution, agencies should evaluate how each capability translates into actual payment outcomes.

Ask the following questions:

Tratta embeds end-to-end payment processing directly into collection workflows. The platform supports real-time balance validation, configurable payment types, split-payment allocation, and next-day ACH funding, ensuring transactions are accurate, flexible, and fast. Contact us to learn more.

Automation ensures all gains are applied consistently across every account, interaction, and stage of the payment journey. This means fewer missed opportunities, more predictable payment behavior, and the ability to scale recovery without increasing operational effort.

Other benefits include:

Automation ensures that embedded payments perform reliably at scale, turning isolated improvements into consistent recovery gains. In the next section, we will examine how embedded payment systems also help reduce compliance risk for collection agencies.

Suggested Read: Debt Collection and Secure Payment Portal

Compliance risk in collections comes from execution gaps across communication, payment handling, disclosures, and recordkeeping. Embedded payment systems reduce this risk by structuring how payments are initiated, processed, and recorded within controlled, rule-driven workflows.

This is how embedded payment processing helps:

Embedded systems capture consumer authorization before processing payments, ensuring compliance with Reg E. They store verifiable consent records and prevent unauthorized or disputed transactions during audits.

Validation details are presented within the payment interface. This ensures consistency between communication and transactions, reducing risks tied to incomplete, inaccurate, or misleading information.

Required disclosures are embedded into payment flows before transactions occur. This ensures consumers acknowledge terms and reduces legal exposure tied to revival risks or non-compliant collections.

Payment prompts align with permitted communication windows and consumer preferences. Systems suppress restricted interactions, ensuring that payments are initiated only under legally compliant engagement conditions.

Embedded systems validate balances in real time before processing payments. They apply predefined allocation rules, reducing errors, disputes, and risks associated with incorrect or excess collections.

Embedded payment systems codify compliance into execution, reducing reliance on manual oversight. In the next section, we will look at how a sophisticated platform brings these features together to improve performance.

Suggested Read: Customer-Centric Approach in Debt Collection Strategies

.jpg)

Tratta is a digital debt collection and payment platform built specifically for agencies, law firms, and creditors operating in regulated environments. Instead of relying on fragmented tools, agencies use one platform to manage the entire recovery lifecycle, from outreach to payment completion.

At its core is a deeply integrated embedded payments infrastructure. Tratta enables end-to-end payment processing within collection workflows, allowing consumers to pay without switching systems or restarting the process. It supports multi-method payments (ACH, cards, checks), split allocations, real-time balance sync, chargeback handling, and transaction-level tracking.

Beyond payments, the platform extends into a broader set of features that directly support recovery outcomes:

Tratta is not just a feature stack. It is infrastructure built to improve how payments are captured, tracked, and completed at scale. With rapid onboarding, full system integration, and hands-on support, agencies can launch quickly and start seeing impact without long implementation cycles.

Without embedded payments, collection agencies continue to lose revenue in the gaps between intent and execution. Consumers delay payments, workflows introduce friction, and compliance risks increase due to manual handling and disconnected systems.

Tratta addresses these challenges by unifying payments, communication, automation, and compliance into a single platform built for collections. Its embedded payment infrastructure ensures faster execution, higher conversion, and more controlled workflows, helping agencies recover more with less friction and risk.

Start turning more consumer interactions into completed payments with a system designed for recovery. Contact us to explore how Tratta can help you scale collections quickly, accurately, and in compliance.

An embedded payment occurs when a consumer receives an SMS or email with a payment link and completes the transaction within that interaction. No external portal or additional steps are required.

Integrated payments connect systems behind the scenes, but often still require separate steps to complete transactions. Embedded payments go further by enabling payment execution directly within the interaction or workflow itself.

They reduce friction between intent and action, allowing consumers to pay instantly. This increases conversion rates, shortens payment cycles, and improves overall recovery performance across portfolios.

Agencies should support ACH, debit cards, credit cards, and digital payment options where applicable. Offering multiple methods increases accessibility and improves the likelihood of successful payment completion.

Yes, when properly implemented, they enforce authorization, disclosures, and audit trails within workflows. This helps agencies meet requirements under FDCPA, Regulation E, and Regulation F while reducing manual compliance risk.