A single lapse in handling payment data can expose your agency to compliance violations, financial penalties, and reputational risk. For collection agencies managing payments across phone, IVR, and digital channels, controlling how card data is captured and processed is no longer optional.

The risk is accelerating. Global losses from online payment fraud are projected to reach $362 billion by 2028, highlighting the growing exposure tied to remote transactions. This is where PCI-compliant card-not-present debt payments become critical.

In this article, you will learn what it entails, the risks involved, and the best practices to ensure secure, compliant payment handling.

Card-not-present (CNP) debt payments refer to transactions where the cardholder is not physically present at the point of payment. In collections, this typically includes payments made over phone calls, IVR systems, payment links, emails, or online portals.

Unlike in-person transactions, CNP payments rely entirely on the security of card data capture, transmission, and storage.

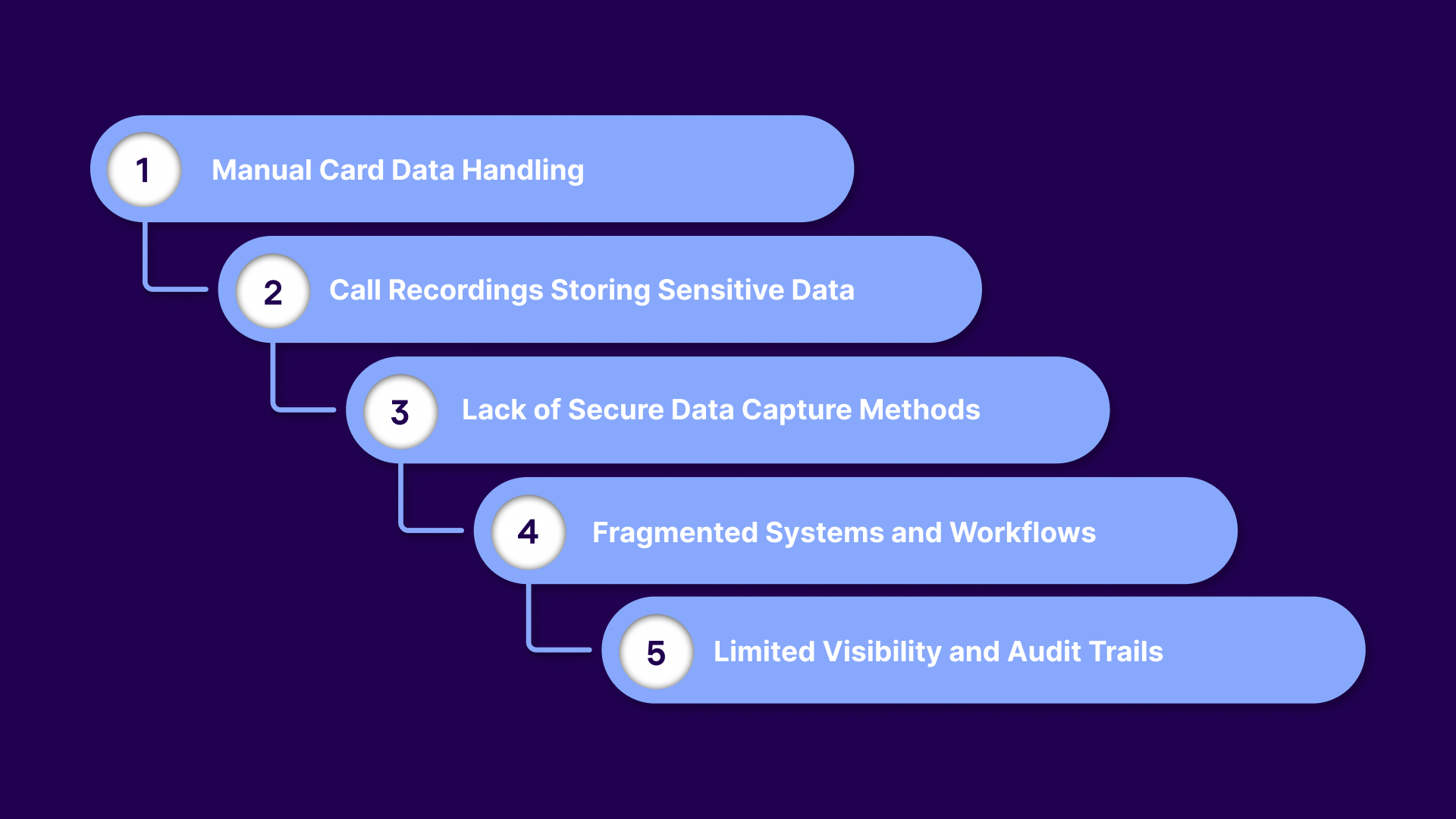

Top risks of accepting CNP payments by collection agencies:

These risks are compliance liabilities. As agencies scale digital and remote payment channels, the need for standardized, secure handling of card data becomes critical. This is where PCI compliance comes into focus.

In the next section, we will look at how PCI compliance enables safer, more scalable payment operations for collection agencies.

Suggested Read: Debt Collection and Secure Payment Portal

PCI compliance refers to adherence to the Payment Card Industry Data Security Standard (PCI DSS). This is a global framework developed by major card networks to secure cardholder data. It defines how payment data must be captured, transmitted, stored, and accessed.

This is how it helps:

PCI standards prohibit unsafe data collection methods, such as writing down or verbally storing card details. Secure input methods like IVR or hosted payment pages ensure sensitive data bypasses agents entirely.

PCI requires encryption protocols when card data is transmitted across systems or networks. This ensures intercepted data remains unreadable and unusable to unauthorized parties.

Agencies are restricted from storing full card details unless strictly protected. Tokenization replaces raw card data with secure identifiers, reducing exposure even if systems are compromised.

Access to cardholder data must be limited based on roles and continuously logged. This creates traceability and prevents unauthorized internal access.

PCI mandates detailed audit trails and regular testing of systems. This ensures agencies can prove compliance and quickly identify vulnerabilities or breaches.

Tratta operationalizes PCI compliance by embedding these controls directly into payment workflows. Instead of relying on agents to follow manual protocols, the system is designed to secure data capture, tokenization, and access controls. Book a free demo.

To securely process card-not-present payments, agencies must align their workflows with specific PCI DSS controls that govern how cardholder data is handled. These requirements directly shape how payment data is captured, transmitted, stored, and accessed across your systems.

PCI requires that sensitive card data not be exposed during collection, especially in agent-assisted environments. This shifts agencies toward controlled input methods that prevent raw data from being seen, heard, or stored.

The following practices focus on securing how card data is initially collected from consumers.

Any card data in transit must be encrypted using strong, industry-approved protocols. This ensures that even if data is intercepted, it cannot be read or misused.

The following measures ensure that card data remains protected as it moves across systems and networks.

PCI emphasizes reducing the presence of sensitive data within your systems. Tokenization replaces card details with secure substitutes, limiting exposure and simplifying compliance scope.

The following practices reduce the amount of sensitive data your systems store or retain.

Access to cardholder data must be tightly restricted and continuously monitored. This ensures that only authorized personnel can interact with sensitive systems and that their actions are fully accountable.

The following controls define who can access payment data and how that access is tracked.

PCI is not a one-time checklist. It requires continuous validation and monitoring. Agencies must be able to demonstrate compliance through documentation, testing, and audit readiness.

The following steps ensure your agency remains continuously compliant and audit-ready.

These requirements define how secure, compliant CNP payment workflows are built and maintained in collection environments. In the next section, we will look at how this can be implemented in practice.

Suggested Read: 5 Reliable Payment Gateways for Debt Collections in 2026

The focus should be on removing exposure points, standardizing processes, and ensuring that card data is never handled internally unnecessarily. When done right, compliance becomes embedded in the workflow rather than enforced manually.

Steps to implement:

1. Map and Assess Current Payment Flows

Begin by documenting how payments are currently collected across calls, IVR, and digital channels. Identify breakdowns in control, visibility, and data handling. This establishes a clear baseline for remediation and prioritization.

2. Replace High-Risk Collection Methods

Remove processes where agents directly interact with full card details. Introduce controlled input methods that isolate sensitive data from internal systems. This reduces dependency on human handling and limits exposure at the source.

3. Deploy Controlled Payment Interfaces

Use secure payment channels that standardize data capture and processing. Ensure these systems enforce protection mechanisms by default, rather than relying on configuration. This creates consistency across all payment touchpoints.

4. Reduce Data Footprint Across Systems

Limit the amount of payment information in your environment. Replace sensitive data with secure references and retain only what is operationally required. This minimizes the impact of breaches and simplifies the scope of compliance.

5. Establish Role-Based System Access

Define strict access boundaries based on job function and enforce authentication controls. Monitor system interactions to ensure accountability at every level. This strengthens internal governance over payment data.

6. Operationalize Compliance Through Training

Align teams with updated workflows that remove ambiguity in handling payment data. Focus training on process adherence rather than rule memorization. This ensures consistency without slowing down operations.

7. Continuously Validate and Optimize Controls

Regularly test systems, review logs, and refine workflows based on performance and risk indicators. Treat compliance as an ongoing operational discipline rather than a one-time initiative. This keeps your processes resilient as you scale.

Tratta enables agencies to operationalize these changes without rebuilding their entire infrastructure. By embedding secure payment orchestration, access controls, and monitoring into a single system, compliance becomes part of the workflow rather than an added layer. Get in touch with us to learn more.

PCI DSS v4.0.1 reinforces stricter, more continuous controls around how cardholder data is secured, particularly in card-not-present environments where risk is inherently higher. For collection agencies, this shifts compliance from periodic validation to an ongoing operational discipline.

The following updates have the most direct impact on how agencies manage CNP payment processes:

PCI DSS v4.0.1 mandates MFA for all access into the cardholder data environment, not just remote access. This directly impacts how agents, administrators, and third-party systems interact with payment platforms.

Organizations must now define and justify how frequently they perform certain security activities. This replaces static compliance schedules with risk-based decision-making.

Updated requirements enforce stronger password controls and authentication mechanisms. This reduces the likelihood of unauthorized access to systems handling payment data.

PCI DSS v4.0.1 increases expectations for tracking user activity and system access. Agencies must maintain detailed logs and actively monitor them to detect anomalies or potential breaches.

Strong cryptography is more explicitly enforced across all transmission channels. This ensures card data remains protected across APIs, integrations, and payment workflows.

The updated standard reinforces minimizing stored cardholder data and securing it where necessary. This pushes agencies toward tokenization and externalized payment processing.

Ongoing training programs are now required to ensure personnel understand evolving threats and compliance responsibilities. This reduces human error in handling sensitive payment data.

In the next section, we will look at how to evaluate and choose the right solution for PCI-compliant CNP payments in collection environments.

Suggested Read: Online Payment Processing Solutions for Small Law Firms

When evaluating solutions, focus on features that directly impact how card-not-present payments are handled in practice.

Necessary features include:

Tratta is built to meet stringent security and compliance requirements, including PCI DSS Level 1 and SOC 2 Type II standards. Payment data is encrypted, continuously monitored, and securely processed across all payment workflows, reducing exposure at every stage.

In addition, the compliance team supports client due diligence by conducting and sharing vulnerability scans upon request. This ensures transparency and reinforces the protection of sensitive consumer information.

When PCI compliance is not properly implemented, the risks extend far beyond regulatory exposure. Payment workflows become inconsistent, sensitive data is unnecessarily exposed, and agencies face increased chances of breaches, audit failures, and lost processing privileges.

Tratta is a payments-first collections platform designed to embed compliance directly into payment workflows. With PCI DSS Level 1 and SOC 2 Type II standards, encrypted processing, and built-in monitoring, it ensures card-not-present debt payments are handled securely and consistently at scale.

Start building a more secure, scalable collections operation today. Book a demo to see how Tratta can optimize your payment workflows without increasing compliance risk.

A card-not-present payment refers to any transaction in which the cardholder is not physically present, such as payments made by phone, IVR, or online portals within collection workflows.

Yes, but only if secure methods are used. Agents should not hear or store full card details, and payments must be processed through PCI-compliant systems, such as IVR or tokenized workflows.

You must always ensure card data is captured securely, encrypted during transmission, and never stored in raw form unless fully compliant with PCI DSS requirements.

Agencies can store card data only if it is properly tokenized and secured in accordance with PCI standards. Storing raw card numbers or CVV data is strictly prohibited.

On Form 1099-K, card-not-present transactions refer to payments processed without physical card interaction, typically categorized under online or remote payment activity reported by payment processors.

Yes, if the link directs consumers to a secure, PCI-compliant payment page where card data is entered directly without passing through internal systems or agents.

They can, if sensitive card data is captured. Agencies must use pause-and-resume recording or DTMF masking to prevent the storage of payment information in recordings.

The safest method is through self-service channels such as IVR, secure portals, or tokenized payment links, which prevent the direct exposure of cardholder data.

PCI compliance should be continuously monitored, with regular audits, vulnerability scans, and system checks to ensure controls remain effective as operations evolve.

Yes, failure to meet PCI standards can result in fines, increased fees, or even termination of merchant accounts, directly impacting the ability to accept payments.