Payment friction is one of the fastest ways for debt collections to lose recoverable revenue. When consumers cannot pay the way they want, whether that means digital wallets, ACH, or mobile options, intent drops and accounts stall.

In the U.S., nearly 70% of online adults reported using digital and mobile payments, highlighting how common electronic payment methods have become.

For debt collection agencies, law firms, and creditors, payment infrastructure now directly impacts recovery performance, compliance, and consumer experience. The right payment gateway or aggregator can simplify transactions and reduce friction, while the wrong one can quietly suppress results.

This guide breaks down the 5 most reliable payment gateways and aggregators for debt collections, based on real operational needs.

Quick look:

A gateway that works well for ecommerce often breaks down when applied to high-volume, compliance-sensitive collection activity. This list is based on how payment gateways and aggregators perform in real U.S. debt collection environments.

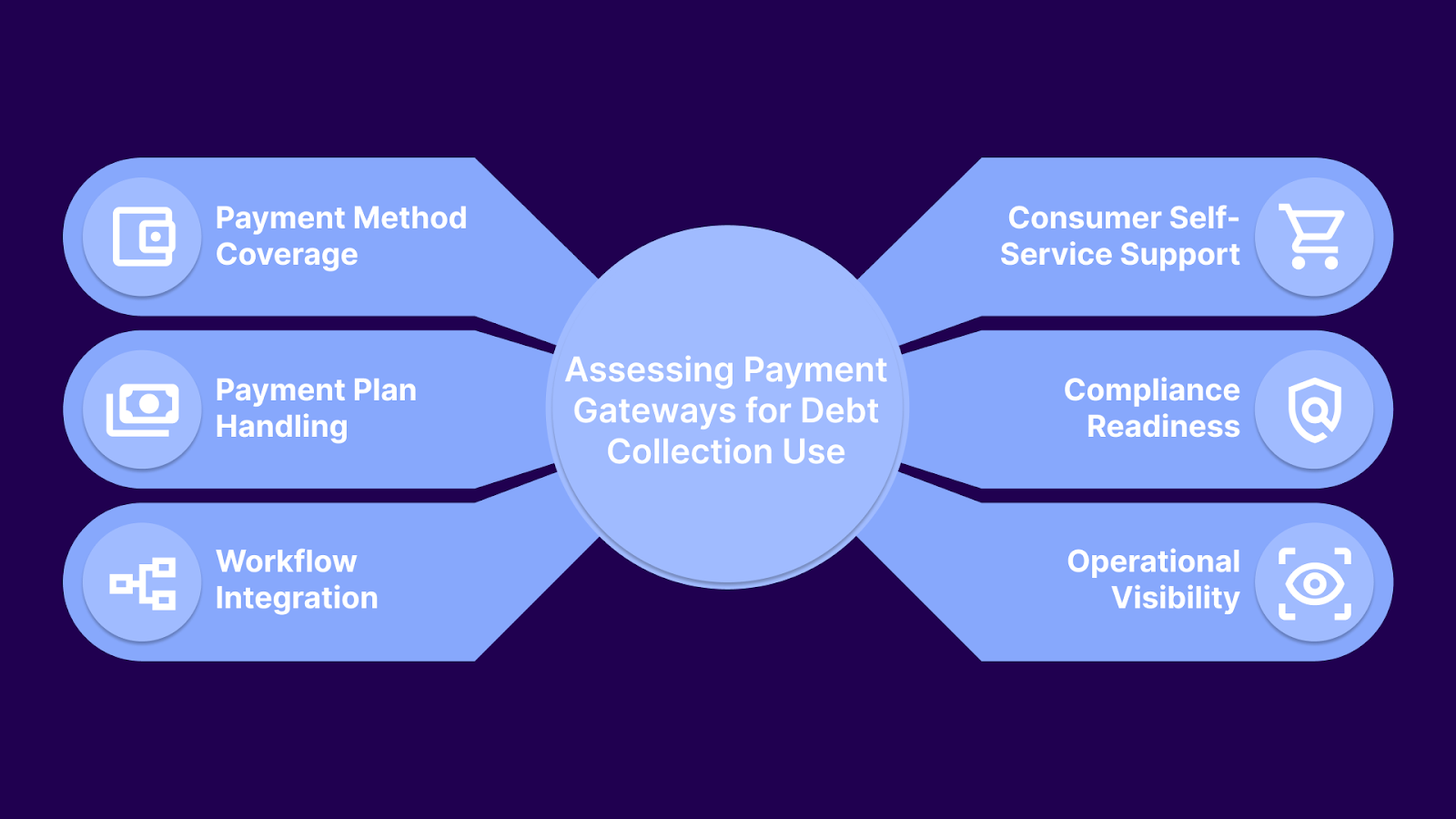

Each platform was reviewed based on how well it supports real collection use cases rather than generic checkout flows.

Evaluation criteria included:

The next section provides a side-by-side snapshot of the leading payment gateways and aggregators.

Suggested Read: Effortless Payment Collection with Automated Software Solutions

The table below provides a snapshot of commonly used U.S. payment gateways and aggregators:

The following section moves beyond surface comparisons and examines how each provider actually performs inside debt collection workflows.

Suggested Read: Modernize Collections: Find Gaps in Your Current Payment Stack

Payment gateways vary widely in how they handle transaction flow, system connectivity, and volume demands. While many offer similar surface-level capabilities, their underlying architecture and operational behavior can differ significantly in practice.

The following sections examine how each payment gateway operates, integrates, and scales.

USAePay is a payment gateway commonly used in regulated, transaction-heavy environments that require precise control over payment processing. In debt collection operations, it is typically implemented as a backend processor integrated into collection platforms rather than used directly by agents or consumers.

Key Features

Pros

Cons

USAePay is best suited for collection operations that need a reliable payment gateway and control over how payments are executed within their systems.

Tratta provides the layer that connects USAePay’s payment processing to active collection workflows. It manages consumer self-service, campaigns, account-level tracking, and compliance controls, while USAePay handles transaction execution. This allows agencies to deploy flexible payment strategies without treating payments as a standalone system.

Paywire is a payment gateway built for regulated and higher-risk payment environments. In debt collection, it is typically used as an embedded processor supporting card and ACH transactions within a broader collections system.

Key Features

Pros

Cons

Paywire by Payscout is best suited for collection operations that need a flexible payment gateway capable of supporting recurring payments and specialized processing requirements.

Suggested Read: Top Subscription Payment Processing Services Guide

NMI is often used by collection agencies that want freedom to change processors without rebuilding their payment setup. Its role is less about how payments are taken and more about keeping payment operations stable as volumes, risk profiles, or banking relationships change.

Key Features

Pros

Cons

NMI works best for agencies that want long-term flexibility in how payments are handled without constantly reworking their systems.

Authorize.Net is a long-standing payment gateway commonly used as part of legacy or established payment stacks. It is often selected for its stability and familiarity rather than for modern, API-driven payment orchestration.

Key Features

Pros

Cons

Authorize.Net is best suited for organizations maintaining established payment systems that prioritize reliability and compatibility over advanced payment control or customization.

Payrazr is commonly selected when agencies want a straightforward, portfolio-friendly payment gateway without committing to complex routing, processor abstraction, or heavy configuration. It is used to keep payment execution stable and predictable while collections systems handle recovery logic and compliance.

Key Features

Pros

Cons

Payrazr fits debt collection agencies that want a practical, adaptable gateway for handling payments at scale, while keeping recovery strategy, compliance, and consumer experience within their primary collections system.

While each gateway above plays a role in payment execution, most debt collection agencies rely on more than a single tool. The next section looks at the most common payment stack patterns used in debt collection and how they shape day-to-day operations.

Suggested Read: How Do Settlements Work in Self-Service Debt Payments?

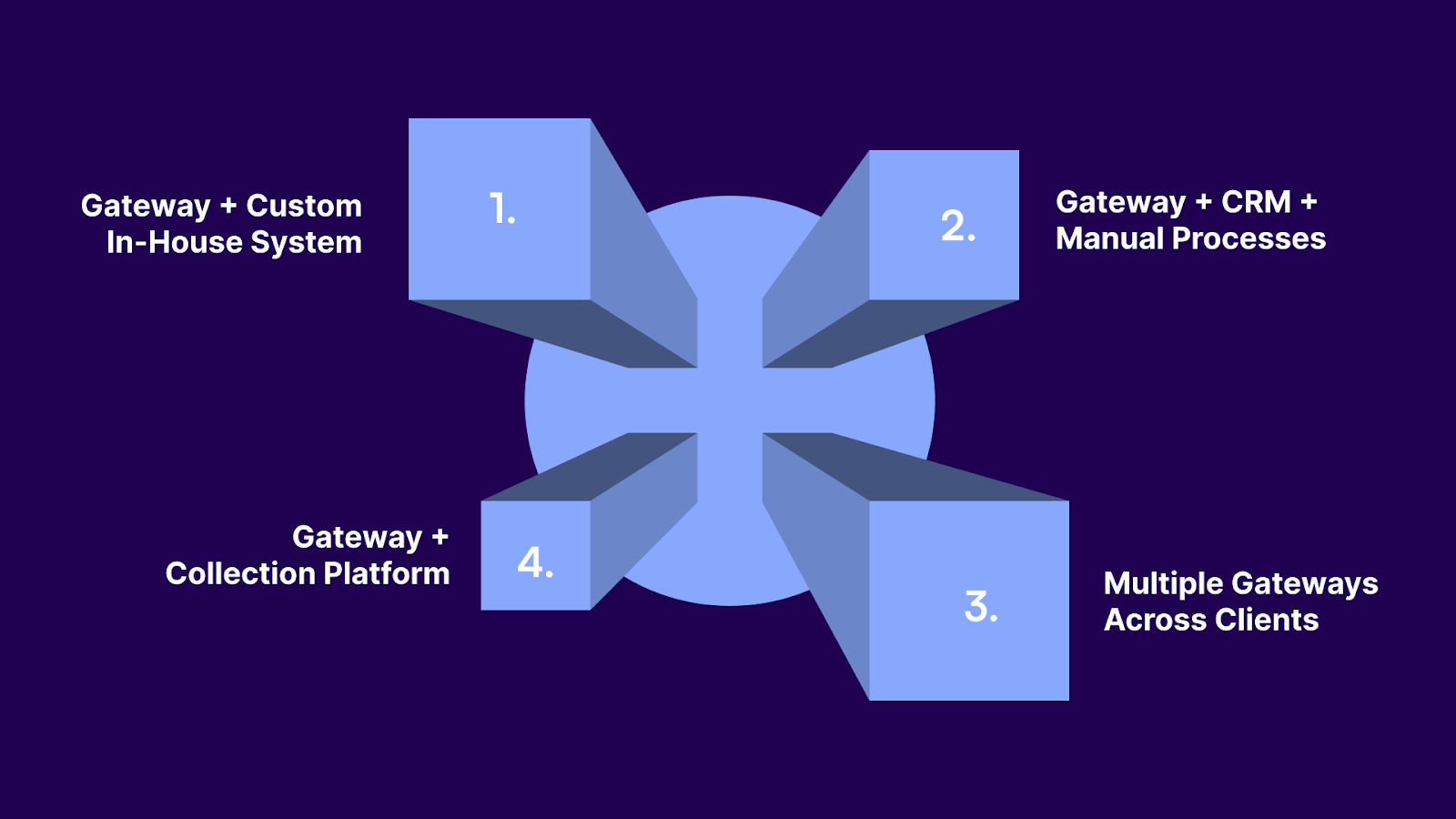

Most debt collection agencies rely on more than one tool to manage payments. How those tools are connected affects efficiency, compliance, and scale.

These are the most common setups seen in U.S. collection operations.

Some agencies use a payment gateway alongside an internally built collections system. Payments run through the gateway, while recovery rules live in custom code. This model offers control but demands ongoing technical effort.

What this setup usually looks like in practice:

Here, a gateway connects to a CRM, and collectors handle most payment activity manually. This approach often appears during growth phases. It works initially, but strains teams as accounts increase.

Where friction tends to show up:

Some agencies operate multiple gateways due to client or risk requirements. Payments are routed differently based on portfolio rules. Without coordination, complexity builds quickly.

Common operational challenges include:

In this model, the gateway focuses solely on moving money, while a collection platform governs payment logic and workflows. This separation reduces manual work and operational risk. It is the most stable and scalable way to manage payments in debt collection.

Why agencies move toward this setup:

Tratta fits this pattern by connecting payment gateways to active collection workflows. It manages self-service, campaigns, and account-level payment logic. Agencies can scale payments without increasing operational strain.

Tratta is a debt collection and recovery platform that manages payments, workflows, and compliance in a single system. It works alongside payment gateways, using them to execute transactions. Tratta controls how payments are offered, tracked, and governed across the collection lifecycle.

Core features include:

Tratta turns payment gateways into part of a single recovery system rather than isolated processors. This separation gives collection teams clarity, control, and consistency across payments, compliance, and workflows.

Payment gateways are designed to move money: they authorize transactions, route funds, and settle accounts. What they don’t manage is the broader recovery process of deciding when a payment should occur, under what terms, and how it aligns with an account’s resolution strategy.

Tratta sits above the gateway layer, linking payment execution to repayment plans, consumer self‑service, account‑level tracking, and compliance oversight. Rather than treating payments as isolated events, it structures, schedules, and governs them across the entire lifecycle of an account.

If your payment infrastructure feels disconnected from recovery outcomes, it may be time to rethink how payments are managed. Talk to us to bring structure, control, and visibility to payment workflows without replacing existing gateways.

The safest payment gateway is one that supports encryption, tokenization, PCI compliance, and strong fraud controls. Safety depends less on brand name and more on how the gateway is configured, monitored, and integrated into secure payment workflows.

There is no single best payment gateway. The right choice depends on payment methods needed, transaction volume, control requirements, integration complexity, and compliance obligations. What works for ecommerce may not work well for regulated or high-volume payment environments.

A legitimate payment gateway is PCI compliant, clearly documents its security practices, works with recognized banks or processors, and provides transparent pricing. Verifying certifications, customer references, and regulatory alignment helps confirm credibility and operational reliability.

Stripe, PayPal, Authorize.Net, Worldpay, and Fiserv are among the most widely used payment gateways in the United States. Usage varies by industry, transaction type, and business size rather than being driven by a single dominant provider.

Yes. Collection agencies must control their payment gateway to manage authorization, settlement, compliance, reporting, and disputes. Borrowers choose how to pay, but the agency’s gateway determines how payments are processed, recorded, and reconciled.