As an AR or collections leader at a credit issuer, you already know that recovering past-due balances depends on more than sending reminders. According to the Federal Reserve Bank of New York, 4.8% of all outstanding US consumer debt was in some stage of delinquency as of Q1 2026. Credit card balances alone stood at $1.25 trillion. That volume does not clear itself.

Every delinquent account moves through a recovery sequence. How well that sequence is designed affects how much your team collects before default, charge-off, sale, or placement. For credit issuers managing early-stage delinquency in-house, the accounts receivable workflow is where portfolio performance starts to move.

The accounts receivable workflow is the structured process a credit issuer uses to manage outstanding consumer balances, from initial billing through collection and account resolution.

It is a connected sequence of steps. When one step is weak or disconnected from the next, accounts slow down, agents lose visibility, and balances age past the point where in-house recovery is practical.

For credit issuers, accounts receivable workflow is tied to consumer account status, payment behavior, and recovery risk. Accounts can move from current to delinquent, then into default, charge-off, and post-charge-off handling. Each stage affects how your team prioritizes outreach, reviews disputes, and routes accounts for resolution.

For covered debt collection activity, Regulation F implements the FDCPA, and state-level rules may add more requirements. That means your AR workflow needs to support compliance documentation, channel-specific consent, consumer-facing payment access, and dispute handling across the full account lifecycle..

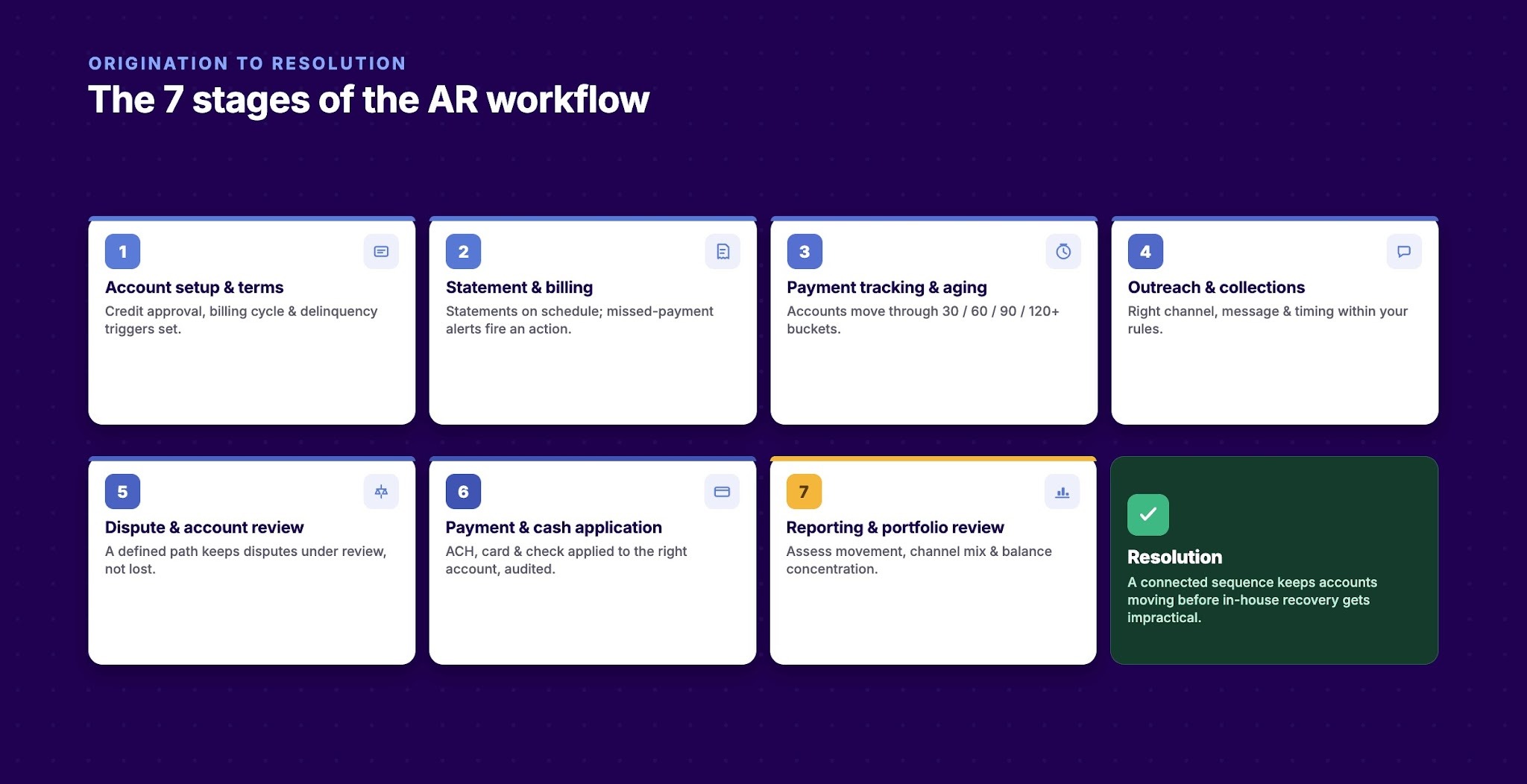

For credit issuers, the AR process spans from account origination to final resolution. Each step affects how accounts move through your portfolio and how much your team can recover.

Before collection activity begins, the foundation is credit approval and payment terms. This step establishes the billing cycle, minimum payment requirements, and what triggers a delinquency flag on the account. Unclear payment terms or poorly defined delinquency thresholds create confusion downstream when your team needs to act quickly.

This is also where digital communication preferences get captured. Consent and channel preferences set during onboarding directly determine which outreach options your team has when an account goes past due.

Statements go out on a regular schedule. For credit issuers, this is often automated. Channel selection still drives engagement. Consumers who receive digital statements with direct payment access are easier to route into payment before the balance ages.

This step is also where missed-payment alerts should trigger an action in the AR sequence, rather than sitting in a queue for later review.

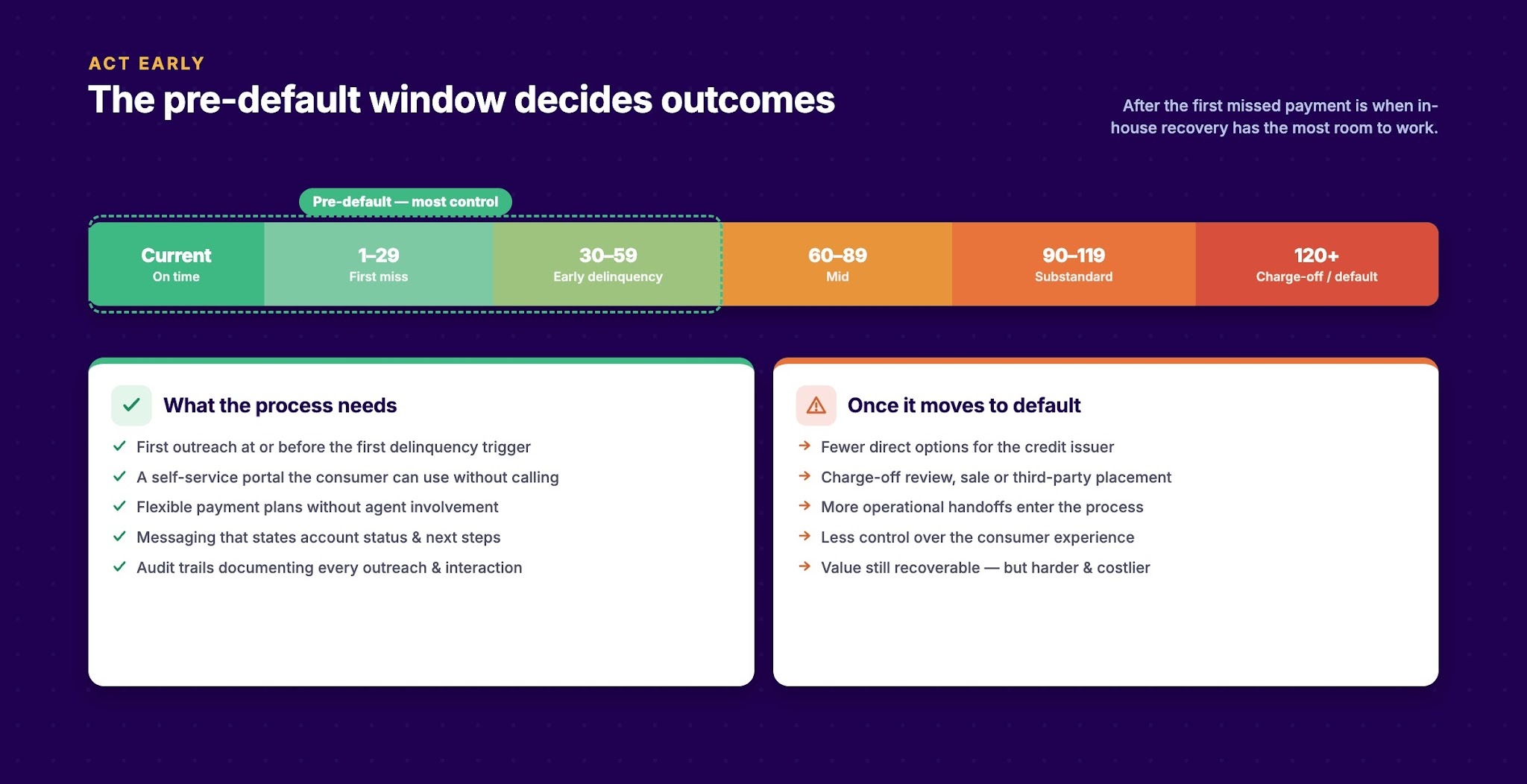

Once a due date passes without action, the account moves into the aging process. Standard aging buckets track accounts as current, 30, 60, 90, or 120-plus days past due.

This is where visibility becomes critical. Without it, accounts can move through aging buckets before your team responds. The urgency is operational and regulatory. The Federal Reserve defines credit card accounts in its supervisory model as in default when they are 120 days or more past due, in bankruptcy, or charged off. The OCC notes that closed-end credit generally should be charged off no later than 120 days past due, while open-end credit card accounts must be charged off at 180 days past due.

Your workflow needs to surface risk before those thresholds shape the next decision.

Reaching consumers who have missed payments requires the right channel, the right message, and the right timing, within the rules that apply to your program. Phone contact still matters, but it cannot carry the whole process.

According to TransUnion's 2024 Debt Collection Industry Report, 88% of debt collection companies now operate a self-service online portal, and a quarter of those companies collect more than 40% of their payments through that channel. A process without digital payment access adds friction for consumers who may be ready to resolve the balance outside call center hours.

Some accounts will include disputes. The consumer may question the balance, identify a billing error, or flag an account they do not recognize. Your AR process needs a defined path for these cases that keeps the account under review without losing visibility.

How your team communicates during a dispute, what documentation it retains, and how quickly it responds all require a repeatable process. Without a clear dispute path, your team accumulates operational drag alongside compliance pressure.

When a consumer pays, that payment must be applied to the correct account accurately. At portfolio volume, cash application errors generate reconciliation problems, produce consumer complaints, and create gaps in reporting.

Your AR process needs payment handling that supports ACH, card, and check transactions consistently, logs each payment with a clear audit trail, and applies funds to the right account without manual intervention on every transaction.

This is where your team assesses what happened across all prior steps. How many accounts moved from current to delinquent? What share resolved through a digital channel? Which aging bucket holds the highest balance concentration?

Without structured reporting here, your AR process produces activity without insight. You cannot identify what is working, where accounts are stalling, or what needs to change next cycle.

Also read: Key Steps for Accounts Receivable Collection Strategy

Knowing the steps is useful. Knowing where they fail in practice is what helps your team improve the accounts receivable workflow.

Many credit issuer AR teams operate across disconnected systems. One tool handles billing, another manages outreach, a third processes payments, and reporting lives in a separate export. When a consumer calls in, an agent may need to check two or three places to understand an account's history.

This creates slow response times, duplicated effort, and a high risk of error. When automated outreach and agent-handled calls pull from different data sources, consumers may receive conflicting information. That damages the resolution conversation before it starts.

Consumers who miss a first payment are often still reachable. Some will resolve quickly if the process is clear and accessible. Reliance on phone calls and mailed notices limits that reach.

When consumers cannot respond through the channel they use most, accounts can age without meaningful contact. The result is a larger queue for agents and fewer low-friction resolutions.

Consumer communication rules create operational pressure for credit issuers, especially when outreach spans phone, email, SMS, IVR, and portal activity. The CFPB's Regulation F governs covered debt collection activity, and state rules may add requirements for timing, consent, disclosures, or documentation.

Your legal and compliance teams should define how those rules apply to your first-party program. The AR workflow should then turn those requirements into repeatable steps, approved templates, opt-out handling, and audit records.

When reporting is limited to monthly exports or manual spreadsheet reviews, your team cannot see problems forming in time. A rise in 60-day accounts may sit unnoticed until those balances move further into delinquency. A drop in digital payment adoption may surface only after the period closes.

By the time the numbers appear, the accounts are harder and more expensive to recover.

Also read: Guide to Accounts Receivable Risk Management for Collection Agencies

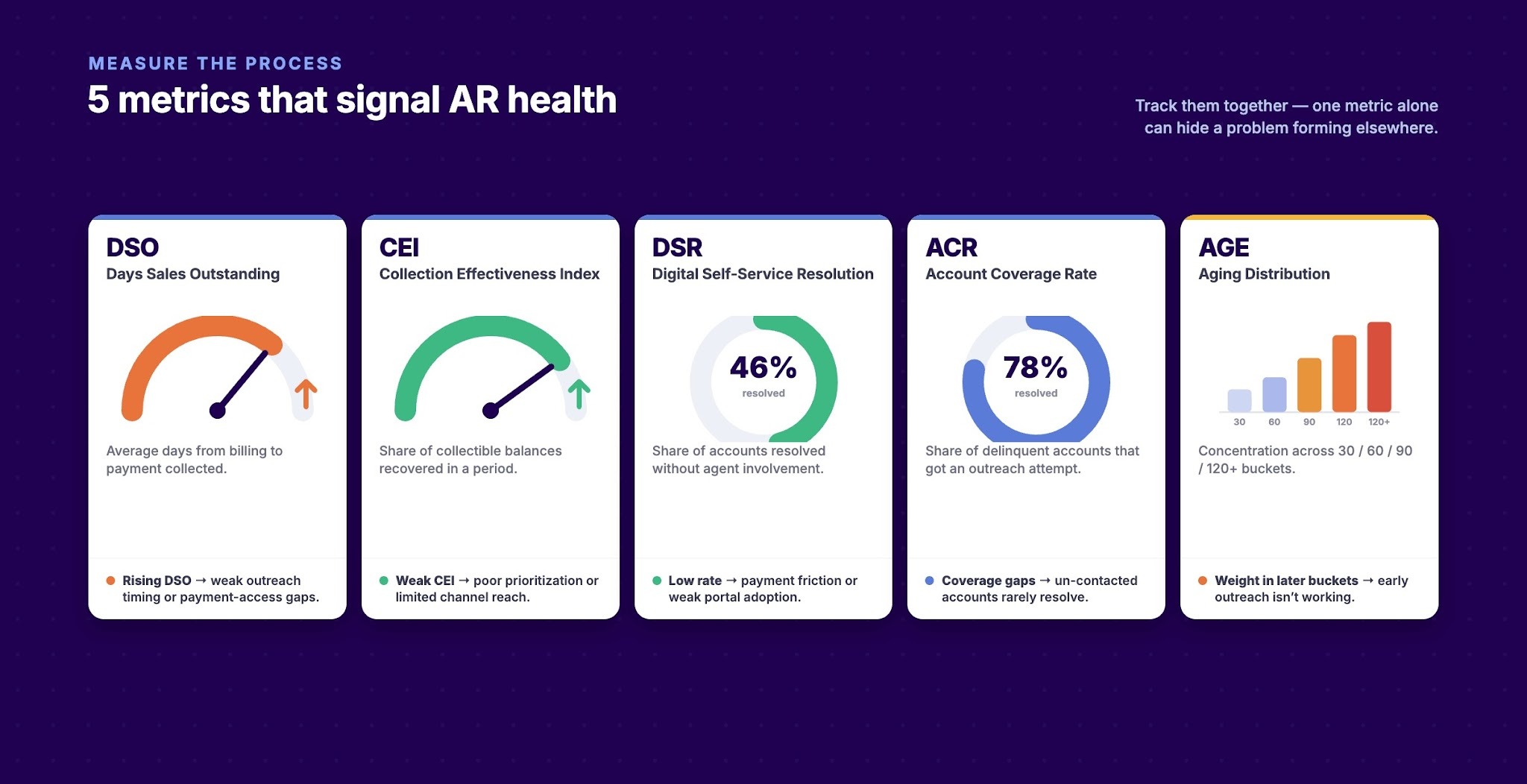

Running the AR process is not enough. You need to measure it. These metrics show whether each step is performing as intended.

Track these together. A team monitoring only DSO may miss a self-service adoption problem that is quietly reducing recovery. A team focused on CEI while ignoring account coverage may collect from reachable accounts while missing a large share of the portfolio.

Also read: Using Risk Scoring to Prioritize Debt Recovery: A Guide for Agencies and Credit Issuers

Improving your AR process does not require replacing your entire operation. It requires closing specific gaps in how steps connect and what supports each one.

When an agent accesses an account, they should have a complete view of its history in a single place. That includes billing statements sent, outreach attempts made, payment links opened, disputes logged, promises to pay, payment plan activity, and funds received.

That view changes daily decisions. An agent who sees that a consumer opened a payment link twice but did not complete the transaction can send a targeted payment follow-up. An agent who sees a recent dispute can pause the wrong outreach path and route the account for review. A supervisor can also see which accounts need agent attention and which can stay in automated treatment.

It also means automated outreach and agent-handled calls pull from the same record, so consumers receive consistent information about their balance and account status.

A branded self-service portal lets a consumer log in, view their balance, make a payment, or arrange a payment plan on their own schedule. For credit issuers, white-labeling matters here. Your consumers should interact with your brand during a sensitive collection interaction.

That continuity supports trust at the moment your consumer relationship is most at risk. It also gives your agents more time for accounts that need review, negotiation, or escalation.

A 31-day account and a 91-day account should not receive the same communication. An effective AR process sequences outreach based on aging. Early accounts may receive digital prompts and payment links. Older accounts may move to SMS, IVR, and direct agent involvement as risk rises.

Each step should have defined timing, defined channels, and compliant messaging templates ready to use. This helps your team concentrate agent effort where it has the most impact.

Operations leaders need more than period-end reports. A current AR system surfaces account-level and portfolio-level data throughout the month. That includes how many accounts sit in each aging bucket, how many have opened a payment link, how many have resolved through the self-service portal, and how this week compares to last week.

That visibility lets you catch problems while there is still time to act.

Also read: Accounts Receivable Collections: Practical Tips That Improve Cash Flow

For credit issuers, the period after the first missed payment is when in-house recovery has the most room to work. At this stage, consumers may still recognize the account, confirm payment details, and respond to clear digital payment options.

This period needs a process built for early resolution. Routine billing steps are often too light, while late-stage collection tactics can strain the consumer relationship too soon.

Early action gives your team more control over the account path. You can offer self-service payment access, review disputes sooner, and route accounts based on risk before more handoffs enter the process.

Once an account moves toward default, charge-off review, sale, or third-party placement, your credit issuer has fewer direct options. Those paths can still recover value, but they add operational handoffs and reduce control over the consumer experience.

Resolving more accounts in-house helps protect more of the balance and keeps the relationship closer to your brand.

Pre-default AR needs clear payment access, clear account communication, and fast self-service resolution options. In practice, this means the process should include the following elements.

When this stage is managed well, more accounts can resolve before they move into default, charge-off review, sale, or placement. When it is fragmented, agents lose time, consumers face more friction, and recovery decisions become harder.

Tratta is debt collection software for recovery workflows, including accounts receivable collection software for credit issuers managing pre-default recovery in-house. It centralizes consumer payments, digital communications, reporting, and compliance-aware workflow control in one platform.

For your AR team, that includes:

Tratta is designed to support compliance-aware workflows in a compliance-sensitive environment. It does not replace your legal counsel or guarantee regulatory outcomes. It gives your team the documentation, controls, and visibility that in-house AR recovery requires.

You can explore the accounts receivable collection software for credit issuers or review Tratta's reporting and analytics capabilities.

A strong accounts receivable workflow gives credit issuer AR teams earlier visibility, cleaner handoffs, and clearer payment paths before delinquent accounts become harder to recover. Success depends on connecting consumers with appropriate resolution options while your team can still influence the outcome.

If your current AR process leaves agents switching systems, consumers hunting for payment options, or leaders waiting on delayed reports, the next step is to close those gaps.

Schedule a demo with Tratta to see how the platform supports in-house AR recovery for credit issuers.

The clearest sign is when account volume grows faster than your workflow can keep up. Agents start checking multiple systems before each action. Payments need manual updates. Managers wait on exports to understand campaign performance. At that point, the issue is not only staffing. The workflow is creating extra work on every account.

More outreach only helps when consumers have a clear way to act after they respond. If a text, email, IVR prompt, or letter sends the consumer into a slow payment process, the campaign creates attention without enough resolution. A connected payment path lets the consumer view the balance, choose an approved option, and complete the payment with fewer handoffs.

Modernization gives managers current visibility into account movement, payment activity, portal use, campaign performance, disputes, and failed payments. That changes the timing of decisions. Instead of waiting for period-end reports, managers can see where accounts are slowing down and adjust campaigns, routing, or agent focus while the portfolio is still active.

A modern workflow should capture call activity, electronic message activity, opt-outs, disputes, payment activity, payment plan changes, account notes, and audit history. For covered debt collection activity, Regulation F includes requirements related to call frequency, electronic opt-outs, and record retention. This is not legal advice. Your legal counsel should define what your agency needs to document by channel, state, client, and account type.

Not always. Many agencies keep their core collection management system and connect newer payment, outreach, reporting, and self-service capabilities around it. The key question is whether account status, payment activity, disputes, and communication records can move reliably between systems without manual re-entry.