Unpaid balances don't collapse overnight. They build quietly through missed reminders, delayed follow-ups, and payment processes that create friction for consumers.

Even with steady sales, cash flow weakens when accounts receivable collections fall behind. In the U.S., overdue receivables remain a persistent financial risk, and 77% of accounts receivable teams struggle to keep up with invoice volumes, according to the VersaPay Survey.

For collection agencies and credit issue companies, this isn't just an efficiency gap. Weak collections increase compliance exposure, strain internal teams, and erode consumer trust. Accounts receivable collections now demand structure, clear processes, built-in compliance, and a consumer experience that makes resolution easier.

This article outlines practical accounts receivable collections best practices that help teams improve cash flow, recover balances faster, and reduce operational and regulatory risk.

Accounts receivable collections are the steps a business takes to recover payments owed for goods or services delivered on credit. The objective is to convert outstanding invoices into cash while maintaining compliance and stable customer relationships.

The process typically includes:

When managed effectively, collections support predictable cash flow, reduce outstanding debt, and improve working capital.

Modern accounts receivable collections go far beyond phone calls and mailed notices. Today’s teams operate within stricter regulatory requirements, multiple digital communication channels, and higher expectations for self-service and transparency. Success now depends on structured workflows, timely follow-up, and clear visibility into payment behavior.

Suggested Read: Managing Debt Collection and Vulnerability Services

Now, let’s explore the principles that guide how teams design processes, communicate with consumers, and manage risk.

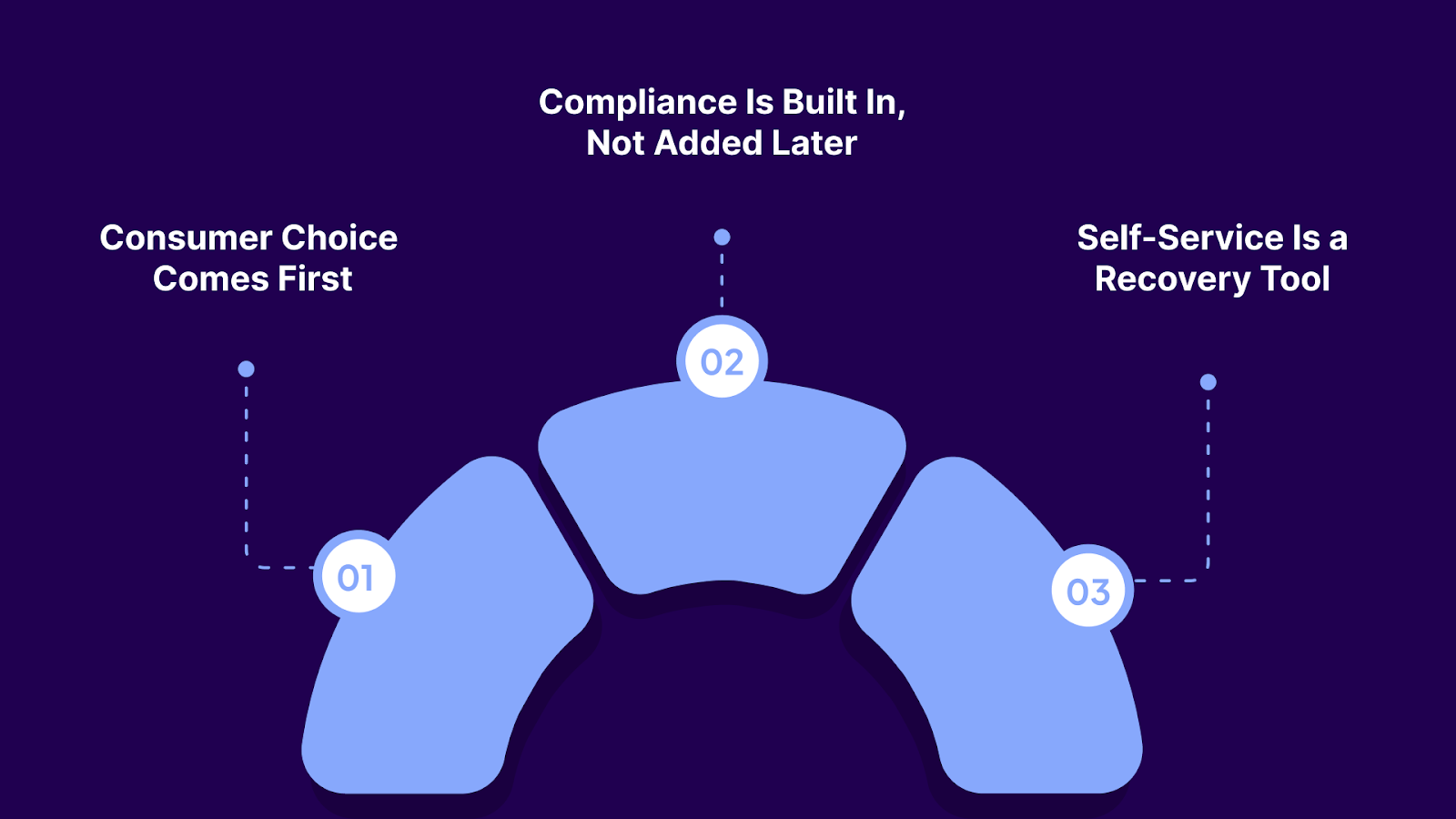

Before tactics come into play, the foundation matters. Strong accounts receivable collections are built on a small set of principles that guide how teams engage consumers, manage risk, and design processes that scale.

Consumers are more likely to resolve balances when they have control over how they engage. This includes the ability to:

The Consumer Financial Protection Bureau consistently identifies confusion and poor communication as leading causes of debt collection complaints.

Manual compliance checks break down as volume grows. Effective programs enforce rules directly within systems, including:

Embedding compliance into workflows reduces risk while allowing teams to operate efficiently.

Self-service is not a convenience feature. It’s a recovery mechanism. Secure portals allow consumers to review balances and take action immediately, reducing delays and agent dependency. McKinsey reports that digital self-service can reduce servicing costs by up to 40% to 50% while improving satisfaction.

Suggested Read: Accounts Receivable Management: Tips and Process Guide

With these principles in place, the focus shifts from mindset to execution. Let’s look at the best practices AR teams use to apply these ideas in day-to-day collection workflows.

Strong accounts receivable collections aren’t about chasing payments more aggressively. They’re about removing friction, acting early, and using clear structure to prevent issues before they escalate. The following practices reflect how mature AR teams protect cash flow while maintaining trust and consistency.

Collections break down when teams lack a clear view of risk. Without visibility, effort gets spread evenly instead of focused where recovery is most likely.

High-performing AR teams consistently track:

This visibility allows teams to prioritize early and avoid reacting only after balances have aged significantly.

Many collection issues begin before the first invoice is sent. When payment terms are unclear or inconsistently communicated, disputes and delays follow.

Effective teams ensure:

Equally important, sales, finance, and AR teams must operate on the same terms. Exceptions made without alignment slow collections and damage trust.

Every delay in invoicing extends the time it takes to get paid. Inaccurate invoices extend it even further.

Best-in-class teams:

Errors trigger disputes. Disputes pause payments. Fast, accurate invoicing removes both.

Customers rarely delay payments intentionally. They delay when paying takes effort.

High-performing AR teams reduce friction by:

When payment requires a phone call or a mailed check, resolution slows. When payment is one click away, it happens faster.

The probability of recovery drops sharply as accounts age. Waiting even a few weeks can turn a simple reminder into a complex recovery effort.

Strong teams:

Early outreach signals that payment timelines matter and prevents accounts from slipping into higher-risk buckets.

Manual processes don’t scale. They introduce delays, errors, and inconsistency.

Automation supports collections by:

This frees AR staff from repetitive work and allows them to focus on disputes, exceptions, and relationship management.

Treating all accounts the same wastes effort and increases complaints.

Effective segmentation considers:

A customer ten days late often needs clarity. A customer ninety days late may need flexibility or dispute resolution. Segmentation ensures the right action is applied at the right time.

Rigid payment demands often stall recovery. Flexibility keeps accounts moving toward resolution.

Practical options include:

Flexibility isn’t leniency. It’s a way to recover balances while maintaining control and preserving long-term relationships.

Inconsistent follow-up leads to missed accounts and mixed messages.

Strong programs define:

Standardized workflows ensure no account is overlooked and customers receive predictable, professional communication.

Aging reports are not just for reporting. They’re early warning systems.

Regular reviews help teams:

This keeps collections proactive instead of reactive.

External collection agencies should be a last step, not a default.

When internal processes are clear and timely, many accounts resolve before escalation becomes necessary. Escalation works best when it follows documented internal efforts, not replaces them.

High-performing accounts receivable collections are built on early visibility, precise action, and systems that remove friction. When teams act early, communicate clearly, and use technology intentionally, cash flow improves without increasing operational or regulatory risk.

Suggested Read: Best Practices for Improving Law Firms' Accounts Receivable Process

Even well-designed processes can break down in practice. The next section highlights common mistakes that cause collection efforts to lose momentum and how to avoid them.

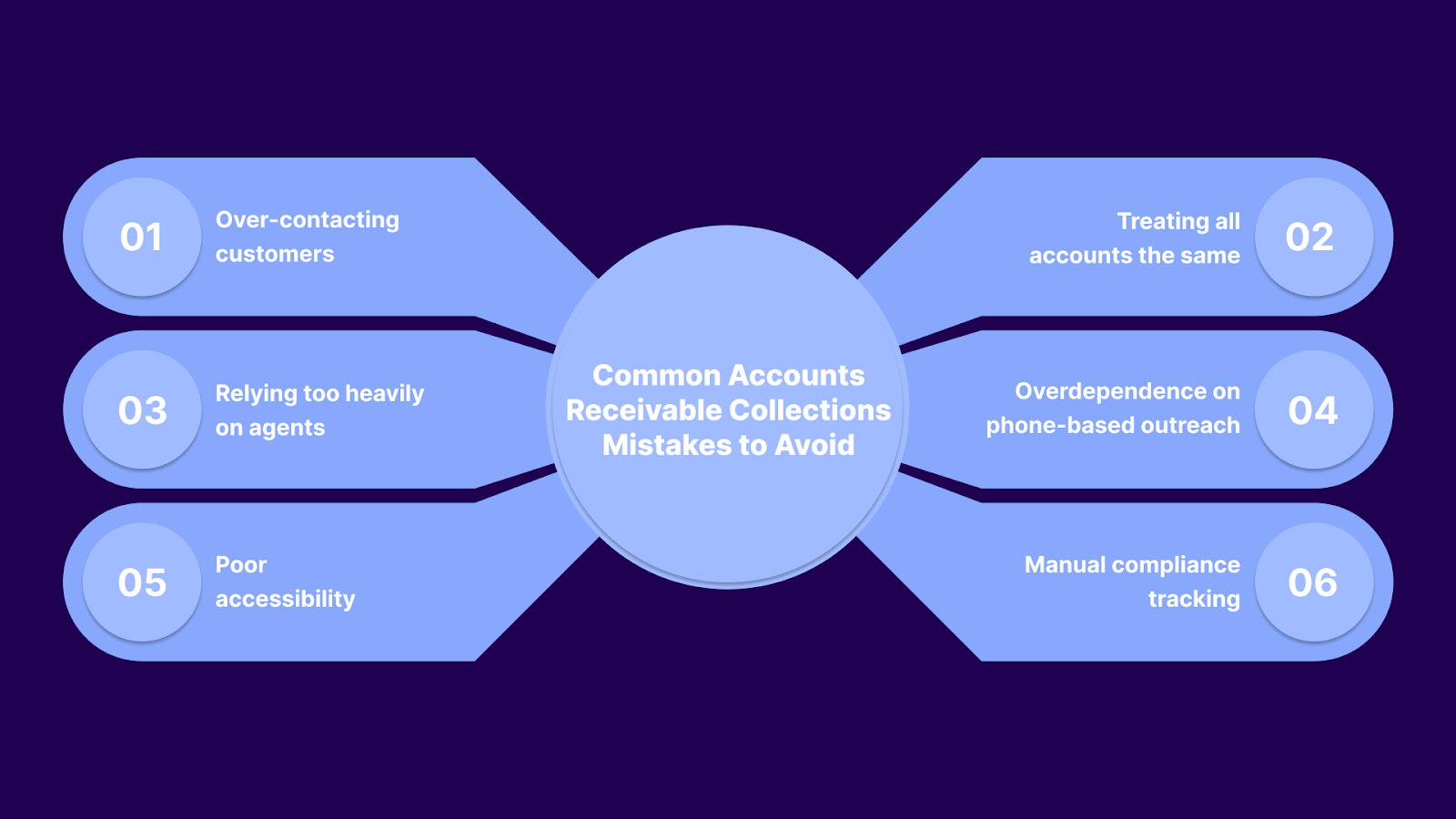

Even experienced accounts receivable teams can fall into patterns that slow recovery and increase risk. These issues often emerge gradually and are easy to overlook until they begin affecting cash flow and compliance.

Many of these issues don’t come from weak teams or lack of effort. They stem from limited visibility and outdated tools.

Suggested Read: High-Impact Collection Strategies for U.S. Agencies in 2025

Even well-designed processes reach their limits without the right systems in place. As volumes grow and compliance requirements tighten, technology becomes essential to maintaining consistent, efficient collections.

Modern accounts receivable collections work best when communication, payments, data, and compliance live in one system. Disconnected tools and manual workflows slow recovery, increase risk, and make it harder to meet consumer expectations.

This is where Tratta fits. Tratta is a digital-first technology platform, not a collections agency. It helps collection agencies and credit issue companies manage receivables through a single cloud-based system that supports the full process, from outreach to payment, with compliance built in.

Here’s how Tratta supports more effective accounts receivable collections:

InDebted partnered with Tratta to modernize its U.S. receivables operations. By introducing a multilingual self-service portal with flexible payment options and pre-charge-off capabilities, InDebted achieved a more than 1,861% increase in self-serve payments.

For collection agencies, legal recovery firms, and credit issue companies, Tratta provides a practical way to improve receivables management through automation, flexibility, and consumer-first design.

Effective accounts receivable collections help maintain steady cash flow, reduce operational inefficiencies, and limit disputes while preserving consumer trust. As collections grow more complex, teams need clear processes supported by systems they can rely on.

Tratta supports this by enabling consumer self-service through secure payment portals and giving teams visibility through real-time reporting and coordinated, compliant communication.

Learn how Tratta supports modern accounts receivable collections workflows. Book a demo to see how self-service payments and centralized data can support better outcomes for both teams and consumers.

Accounts receivable collections are the steps taken to recover payments owed for goods or services already delivered. This includes invoicing, monitoring unpaid balances, following up on overdue accounts, and recording payments accurately.

Effective collections start with timely invoicing, clear payment terms, and consistent follow-up. Using structured workflows and digital payment options helps reduce delays and keeps accounts from slipping through the cracks.

Track payment behavior closely and act early on overdue accounts. The sooner issues are identified, the easier they are to resolve without escalating risk or effort.

Delayed collections tie up cash needed for operations, payroll, and growth. Strong collection practices convert revenue into usable cash faster and help maintain financial stability.

Late or inaccurate invoicing, manual follow-ups, limited visibility into overdue accounts, and inconsistent processes are common causes. Over time, these gaps create backlogs that are difficult to recover from.

Agencies can segment accounts, offer self-service payment options, and enforce compliance through systems rather than manual checks. This improves recovery while reducing complaints and regulatory exposure.