Collection agencies are under increasing pressure to recover balances efficiently while maintaining compliance and controlling costs. At the same time, consumer communication habits have shifted decisively toward mobile.

According to the Pew Research Center, over 95% of Americans across all age groups use cellphones. This makes text messaging one of the most universally accessible channels today. For agencies, that reach creates a clear opportunity.

An SMS payment gateway connects outreach directly to secure payment in a single interaction. In this guide, we explain how SMS payment gateways work, key features to evaluate, compliance considerations, and implementation best practices.

Brief look:

An SMS payment gateway is a digital collection channel that enables agencies to request and receive payments via text messaging. Rather than serving as a standalone texting tool, an SMS payment gateway operates as part of a broader recovery strategy.

In the context of collection agencies, an SMS payment gateway typically:

Now, let us look at how this actually works inside a collection workflow. Next, we examine the top features agencies should look for in text payment gateways.

Suggested Read: Using SMS for Debt Collection Guide

Collection agencies need structured controls, security safeguards, and system connectivity to ensure text-based payments function within a compliant workflow. The following functions separate purpose-built gateways from basic messaging tools.

Key features to assess include:

Tratta supports PCI-DSS Level 1 compliant payment processing within its embedded payments infrastructure. Card and ACH transactions are handled within a secure environment, reducing the need for agencies to store or manage sensitive payment data internally. Book a free demo.

Text-to-pay gateways connect outreach and payments into a single, structured workflow. Instead of separating communication from transaction, agencies send a compliant SMS that leads directly to a secure payment environment tied to the consumer’s account.

This is how they work in practice:

Agencies begin by identifying which accounts are eligible for SMS outreach. This selection is based on balance size, aging status, communication consent, and internal policy guidelines.

This stage typically involves the following controls:

These controls ensure outreach is targeted, compliant, and aligned with the recovery strategy.

Once accounts are selected, structured SMS messages are deployed within legal contact windows. Messages include required disclosures and clear opt-out instructions.

This process includes safeguards such as:

These measures reduce regulatory exposure while maintaining communication consistency.

Each message contains a unique, tokenized link tied to the consumer’s account. The link directs the recipient to a secure payment interface.

Key technical controls at this stage include:

This structure prevents unauthorized access and reduces fraud risk.

Before completing payment, the consumer must verify identity. The transaction is then processed through a secure payment infrastructure.

This stage involves protections such as:

These controls protect sensitive information while accelerating resolution.

After payment submission, the system updates the account status immediately. This eliminates manual posting delays and improves reporting accuracy.

Operational updates include:

Real-time reconciliation keeps recovery workflows accurate and auditable.

When implemented correctly, this structured process reduces friction between outreach and resolution while maintaining regulatory oversight. Next, we examine how these workflows translate into measurable advantages for collection agencies.

Suggested Read: Automated Payment Reminders

SMS payment gateways change how agencies convert outreach into revenue. When implemented within a compliant framework, SMS payments can improve both operational performance and consumer responsiveness.

Key advantages include:

While these benefits highlight the operational and financial upside, real-world performance matters more than theory. Let us look at how agencies have translated text-based strategies into measurable recovery gains.

Suggested Read: Understanding Text Messages in Debt Collection: Guides and Samples

The value of SMS-enabled payment strategies becomes clearer when supported by measurable outcomes. The following case studies demonstrate how agencies modernized outreach and increased digital recovery using Tratta.

Multi-Service Fuel Card (part of the Shell Group) implemented Tratta to replace manual outreach and expand digital payment adoption across its portfolio. By integrating SMS-enabled outreach with secure embedded payments, Multi-Service Fuel Card accelerated digital collections and improved overall portfolio efficiency.

Key outcomes included:

Additionally, by using Tratta’s Consumer Self-Service Payment Portal and omnichannel communication capabilities, the organization significantly improved recovery performance.

Couch Lambert, LLC, a multi-state legal collections firm, partnered with Tratta to modernize its payment and communication infrastructure. The firm adopted Tratta’s digital payment and outreach tools to optimize recovery while maintaining compliance standards.

Reported improvements included:

By centralizing digital communication and payment processing, Couch Lambert improved workflow consistency and positioned itself for scalable growth.

These examples illustrate how structured SMS-enabled payment strategies can drive measurable recovery gains when implemented within a single digital platform. As agencies expand digital outreach, it becomes equally important to understand the regulatory requirements governing SMS-based collections.

Suggested Read: 10 Effective Debt Collection SMS Examples That Get Results

Agencies must ensure every interaction complies with federal statutes, regulatory rules, and state-level requirements. Failure to align outreach practices with these standards can result in litigation, fines, and reputational damage.

Key regulatory considerations include:

Governs communication conduct, including harassment prohibitions, misleading representations, and required disclosures. Agencies must ensure SMS messages do not violate frequency, content, or validation notice requirements.

Clarifies FDCPA application in digital communications, including limits on contact frequency and guidance on electronic validation notices. It also establishes rules for opt-out mechanisms in electronic messaging.

Requires prior express consent for automated text messaging. Agencies must maintain documented consent records and provide clear opt-out functionality.

The Consumer Financial Protection Bureau enforces federal consumer protection laws and monitors unfair, deceptive, or abusive acts and practices (UDAAP). SMS content and delivery practices must align with these enforcement standards.

Many states impose stricter requirements than federal law. For example, California’s Rosenthal Fair Debt Collection Practices Act (RFDCPA) expands consumer protections beyond the FDCPA. It applies to original creditors as well as third-party collectors.

Managing these overlapping requirements manually increases compliance risk as digital outreach scales. Tratta addresses this challenge through its Compliance-by-Code approach, which embeds regulatory and policy requirements directly into platform architecture and workflows. Get in touch with us.

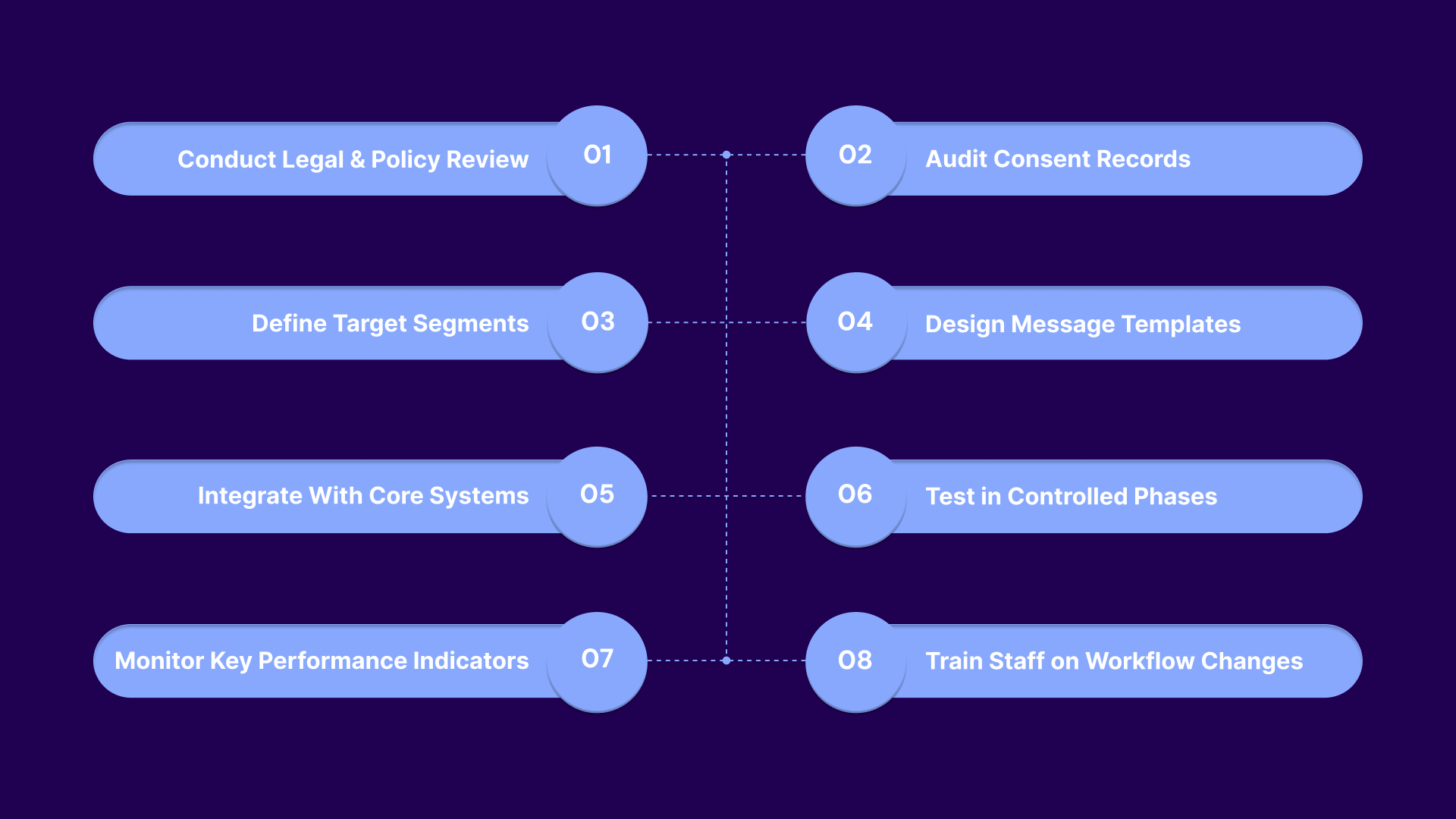

Implementing an SMS payment gateway requires more than activating a texting feature. Agencies need to align legal review, workflow design, system integration, and performance tracking before launching at scale. A structured rollout reduces compliance risk and increases adoption across portfolios.

To implement successfully:

Successful implementation depends on structured systems that automate compliance controls, payment processing, and audit documentation. Using purpose-built technology ensures SMS outreach operates efficiently, securely, and at scale.

Collection agencies risk more than missed payments without a structured SMS payment strategy. Unsecured links, inconsistent consent tracking, and manual message controls can expose organizations to compliance violations, consumer disputes, and reputational damage.

Tratta enables agencies to deploy SMS-enabled payment workflows within a single, compliance-driven framework. The platform automatically governs outreach timing, consent controls, and transaction security. This structured approach reduces risk while accelerating digital recovery at scale.

If your agency is evaluating SMS payment solutions, prioritize platforms built specifically for regulated collections. Speak with our team to assess how a new system can govern communication and payment security.

SMS payment in debt collection refers to sending secure payment links via text message, allowing consumers to resolve balances directly from their mobile devices. It connects compliant outreach with immediate payment access.

An SMS payment gateway generates secure, account-specific payment links delivered through compliant text messages. When a consumer clicks the link, they authenticate and complete payment within a secure processing environment tied to the agency’s system.

The best providers are purpose-built for regulated collections, offering PCI-compliant processing, consent management controls, audit logging, and integration with core collection platforms. Agencies should prioritize compliance governance over generic messaging tools.

SMS has not been replaced but expanded into omnichannel strategies that include email, portals, and digital payment links. Text messaging remains one of the most immediate and widely used communication channels.

Yes, when implemented properly. Agencies must comply with FDCPA, Regulation F, TCPA, and state laws by managing consent, timing, disclosures, and opt-out requirements within a structured system.