Collection teams are expected to recover more while handling larger portfolios, navigating stricter compliance requirements, and working within limited operational capacity. When accounts with very different payment behavior and risk profiles are treated the same way, effort is misdirected, recovery slows, and compliance exposure increases.

This challenge is reflected across the industry. In 2024, the Consumer Financial Protection Bureau (CFPB) received approximately 207,800 debt collection complaints, representing about 7% of all consumer complaints. Many of these complaints relate to disputes, communication issues, and inconsistent handling, issues that often arise when diverse accounts follow identical recovery paths.

This is the problem advanced debt segmentation is designed to address. By distinguishing accounts, agencies can replace uniform strategies with structured, differentiated treatment aligned with each account's actual behavior.

This blog explains how advanced debt segmentation is used in modern collections, how agencies and creditors build and apply effective segments, and how segmentation supports more efficient, controlled, and compliant recovery execution.

Advanced debt segmentation is the practice of dividing delinquent accounts into defined groups based on shared risk, behavior, and response characteristics, rather than relying on a single factor such as balance or aging.

It focuses on identifying meaningful differences between accounts so they can be organized into segments that reflect how they are likely to behave during the recovery process.

In essence, advanced debt segmentation:

Unlike basic segmentation, which is often static and descriptive, advanced debt segmentation is designed to create clear, structured groupings that accurately represent variations within a debt portfolio.

Collection teams today operate under increasing pressure to improve recovery outcomes while managing larger portfolios, stricter regulatory requirements, and limited capacity to scale resources.

Advanced debt segmentation matters in modern collections because it enables:

By organizing accounts into structured, behavior-based segments, collection teams can operate more efficiently, maintain consistency, and manage risk at scale.

Tratta supports this by combining prioritization, automation, and compliance controls into a single system. Book a free demo and explore how it supports modern collection operations.

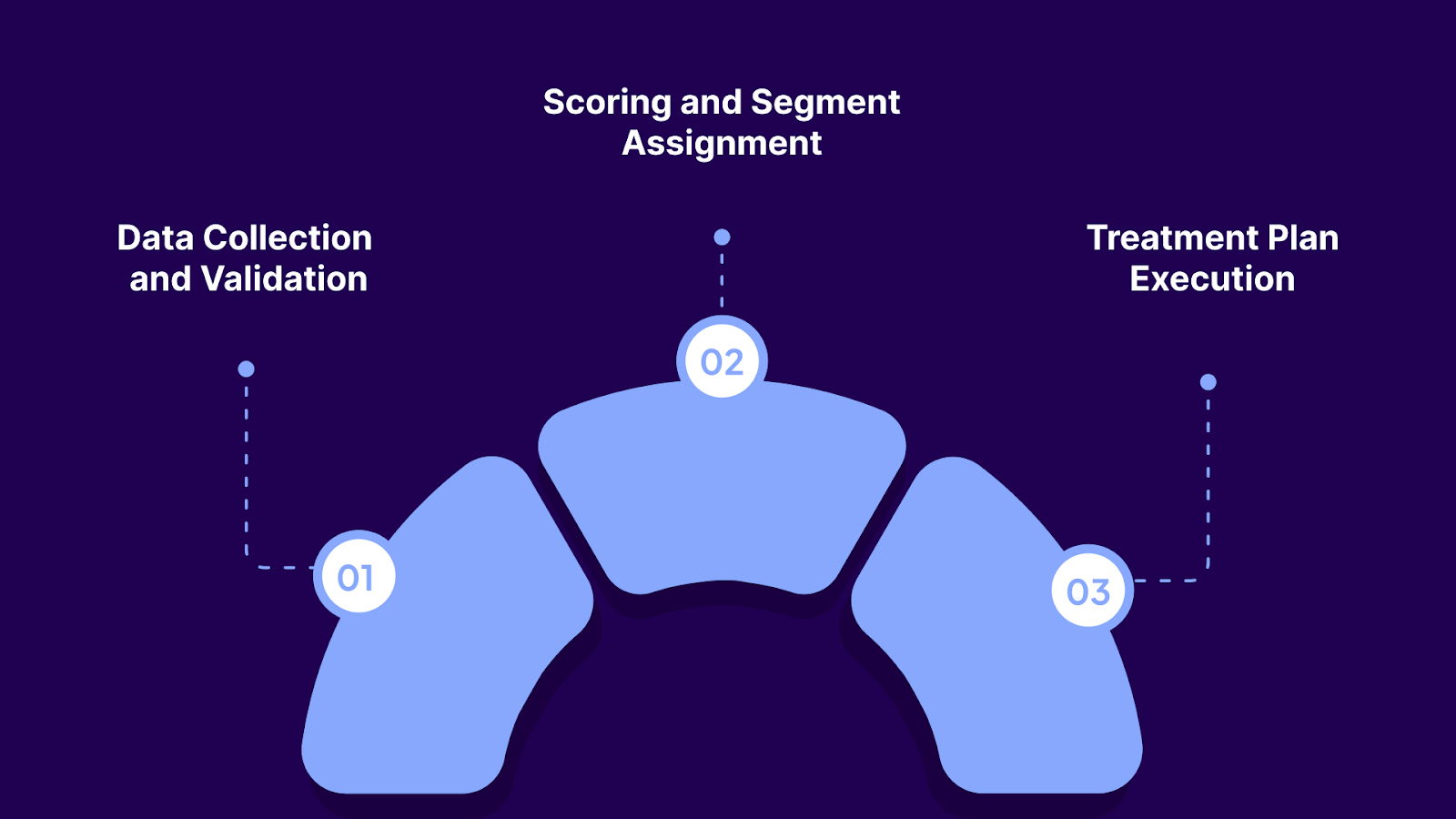

Advanced debt segmentation relies on three core components. Each component must work together to produce actionable segments.

Let’s look at them in detail:

Segmentation starts with clean, accurate data. Your system pulls information from multiple sources:

Missing or inaccurate data creates flawed segments. Before segmentation begins, data must be validated. Accounts with incomplete information are flagged for manual review or excluded from automated scoring.

This step is not optional. If your data is wrong, your segments will be wrong, and your treatment strategies will fail.

Once data is validated, scoring models assign accounts to groups. Predictive models process variables to calculate each account's probability of payment.

Common segmentation criteria include:

Each segment receives a tailored treatment plan that specifies:

High-value, high-probability accounts get personalized outreach from top collectors. Medium-probability accounts receive automated reminders with self-service payment options. Low-probability accounts are assigned to automated workflows or legal escalation.

The key is consistency. Treatment plans ensure every account in a segment receives appropriate attention without manual decision-making for each individual case.

Suggested Read: Guide to Predictive Scoring and Segmentation For Debt Recovery

Building effective segments requires more than sorting accounts by age. You need structured processes, quality data, and clear segmentation logic.

The process can be broken down into the following steps.

Start by selecting variables that influence payment behavior in your portfolio. Not all variables carry equal weight, so focus on factors that actually drive outcomes.

Common high-impact variables include:

Test different combinations to identify which variables best predict recovery for your specific portfolio. What works for medical debt may not work for credit card debt.

Predictive scoring assigns each account a probability score based on historical data. Machine learning models can process thousands of variables to identify patterns that predict payment.

These models analyze past recovery data to identify characteristics of successful accounts. Accounts with similar profiles receive higher scores. Accounts matching past failures receive lower scores.

Scores guide both segmentation and treatment decisions. A high score might trigger immediate contact from the collector. A low score might route the account to automated workflows or return.

Once accounts are scored, create segment boundaries based on performance data, not arbitrary thresholds. A typical portfolio might include:

Test different boundary definitions and measure recovery outcomes. Adjust boundaries quarterly based on actual performance.

Each segment needs a clear, documented treatment plan. This ensures consistency and prevents over-collection or under-collection.

Treatment plans should specify:

Document these rules in your system so they execute automatically.

Suggested Read: Top 10 Accounts Receivable Automation Software Solutions

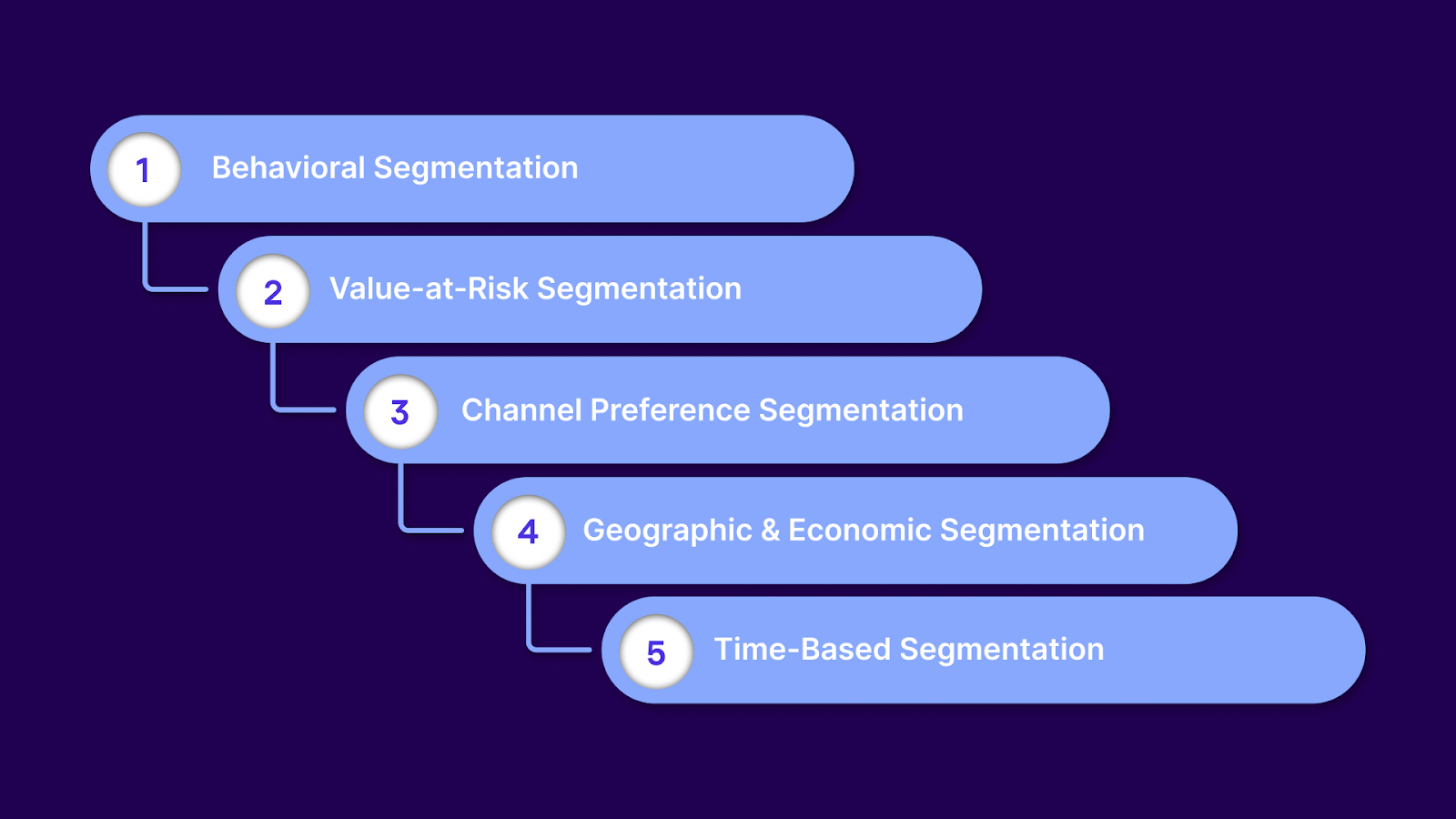

Several techniques improve segmentation effectiveness. Your agency can combine these methods based on portfolio characteristics and available data.

Segment accounts based on observed response patterns to outreach and payment options, such as:

Each group requires different strategies. What works for responders wastes resources on non-responders.

Value-at-risk (VAR) segmentation combines balance size with payment probability. This helps prioritize accounts based on expected recovery value.

The expected recovery value is calculated by combining balance size with payment probability. A $10,000 account with a 50% payment probability represents $5,000 in expected recovery, while a $200 account with an 80% probability represents $160.

This approach focuses effort on the accounts that matter most to cash flow, not just the ones easiest to collect.

Different debtors prefer different communication channels. Some respond to phone calls. Others prefer email or text.

Track engagement metrics by channel:

Use this data to assign each account to its preferred channel. This increases engagement without increasing total outreach volume.

Tratta supports omnichannel communication execution by coordinating email, SMS, IVR, and portal messaging from a single platform. Your team can route outreach based on segment preferences without having to manage multiple disconnected tools. Schedule a free demo to see segmentation-driven omnichannel outreach in action.

Payment behavior varies by location. Accounts in regions with strong economies and low unemployment typically perform better than accounts in economically distressed areas.

Geographic segmentation also helps with compliance. State laws differ on contact restrictions, interest calculations, and legal processes. Segmenting by state ensures that treatment plans automatically comply with local regulations.

This reduces compliance risk while tailoring strategies to regional economic conditions.

Account age matters significantly. Historical data shows that accounts over 90 days old have collection rates as low as 50%, meaning half of these aged receivables may never convert to cash.

Time-based segmentation adjusts strategies based on delinquency duration:

Older accounts require different approaches than recent delinquencies. Time-based rules ensure strategies match account urgency.

Suggested Read: Challenges Faced by Credit Officers & Their Impact on Collections

Segmentation improves results when executed correctly. However, poor execution creates new problems without solving existing ones.

Here are the things you need to avoid:

Creating too many segments adds complexity without improving results. Each segment requires unique rules, monitoring, and reporting. Too many segments overwhelm operations and dilute performance tracking.

Segmentation accuracy depends on data quality. Using outdated payment histories, incorrect contact information, or stale credit data produces flawed segments.

Accounts get misclassified, leading to inappropriate treatment and poor outcomes. A responsive account treated as non-responsive wastes an opportunity. A high-risk account treated as low-risk wastes resources.

Validate data before segmentation. Update account information regularly. Remove accounts with incomplete or unreliable data from scoring models.

Segments must be monitored and adjusted. Payment behavior changes. Economic conditions shift. Segments that performed well last quarter may underperform this quarter.

Track recovery rates, contact effectiveness, and payment completion by segment. If a segment underperforms, investigate why. Adjust segment criteria, treatment plans, or scoring models based on actual results.

Segmentation identifies which accounts warrant attention, not which accounts should be harassed. High-priority segments still require compliant, respectful outreach.

Segmentation should guide resource allocation, not serve as justification for aggressive collection tactics. Maintain compliance standards across all segments. Document treatment plans and ensure they meet FDCPA and Regulation F requirements.

Train collectors on segment-specific strategies and compliance guardrails. Segmentation is a tool for efficiency, not a license for abuse.

Manual segmentation is slow, inconsistent, and error-prone. Without technology support, segment assignments lag behind account changes.

Integrate segmentation logic into your collections platform. Automate segment assignment, treatment execution, and performance reporting. This ensures consistency and allows real-time adjustments based on account behavior.

Suggested Read: Machine Learning Tools for Customer Risk Assessment in Collections

Effective segmentation requires technology that centralizes data, automates workflows, and provides real-time performance visibility. Tratta provides the infrastructure debt collection agencies need to execute advanced segmentation strategies consistently and at scale.

Let's look at how Tratta operationalizes advanced debt segmentation in day-to-day collection environments.

Together, these capabilities ensure that segmentation strategies are not just designed but executed reliably, at scale, and within regulatory boundaries.

Advanced debt segmentation has shifted from a tactical option to an operational necessity. Agencies that continue to rely on uniform treatment and manual decision-making will struggle to scale, control costs, and adapt to changing consumer behavior.

The real differentiator is not whether segmentation exists, but whether it is executed consistently across workflows, channels, payments, and compliance. When segmentation is enforced by systems rather than individuals, recovery becomes more predictable and sustainable.

Tratta helps agencies close the gap between segmentation strategy and execution by embedding segment logic directly into daily operations.

Book a free demo to see how advanced debt segmentation can be executed at scale in your environment.

Most agencies perform best starting with three to five core segments. This provides meaningful differentiation without adding operational complexity or diluting performance measurement.

Segmentation logic should be reviewed at least quarterly, or sooner if payment behavior, portfolio mix, or economic conditions change significantly.

Yes. Creditors can apply segmentation pre-placement to improve account quality, determine optimal referral timing, and assign accounts to appropriate recovery partners.

No. Segmentation reallocates effort, allowing collectors to focus on higher-value interactions while automation handles routine or low-probability accounts more efficiently.

When properly designed, segmentation improves compliance by enforcing consistent treatment, controlling contact frequency, and documenting decision logic across account groups.