Debt recovery teams are expected to improve results while working with limited resources, amid increased regulatory scrutiny and growing account volumes. Yet many organizations still rely on uniform recovery strategies that fail to prioritize accounts based on real payment likelihood.

Predictive scoring and segmentation address this gap by using data to determine which accounts deserve immediate attention, which can be resolved with lighter-touch strategies, and which require structured escalation.

Research shows that predictive scoring models can deliver 1.53× to 1.70× higher expected recovery amounts than random-assignment approaches, highlighting the measurable impact of data-driven prioritization.

This guide explains how scoring and segmentation work together to improve recovery rates, reduce delinquency progression, and support consistent, compliant execution across debt collection workflows.

Quick look:

Predictive scoring uses historical, behavioral, and transactional data to estimate the likelihood that an account will resolve within a defined time period.

Rather than relying on balance size or aging alone, predictive models help teams prioritize accounts based on expected recovery potential. This allows collection strategies to focus effort where it is most likely to produce results.

Pros of Predictive Scoring:

Cons of Predictive Scoring:

While predictive scoring helps determine which accounts deserve attention, it does not define what to do with those accounts. That execution layer is handled through segmentation.

The following section explains how segmentation translates predictive insights into structured, repeatable recovery strategies.

Suggested Read: Big Data Applications and Benefits in Finance

Segmentation is the operational layer that turns scoring insights into action. It groups accounts with similar characteristics so each group follows a defined recovery strategy.

Instead of making decisions at the individual account level every time, segmentation ensures consistent treatment across similar accounts while still allowing meaningful differentiation.

Pros of Segmentation:

Cons of Segmentation:

When predictive scoring and segmentation are used together, recovery decisions become both data-driven and operationally consistent. The next section explores how this combination works together.

Suggested Read: How Data Transforms Debt Collection Strategies

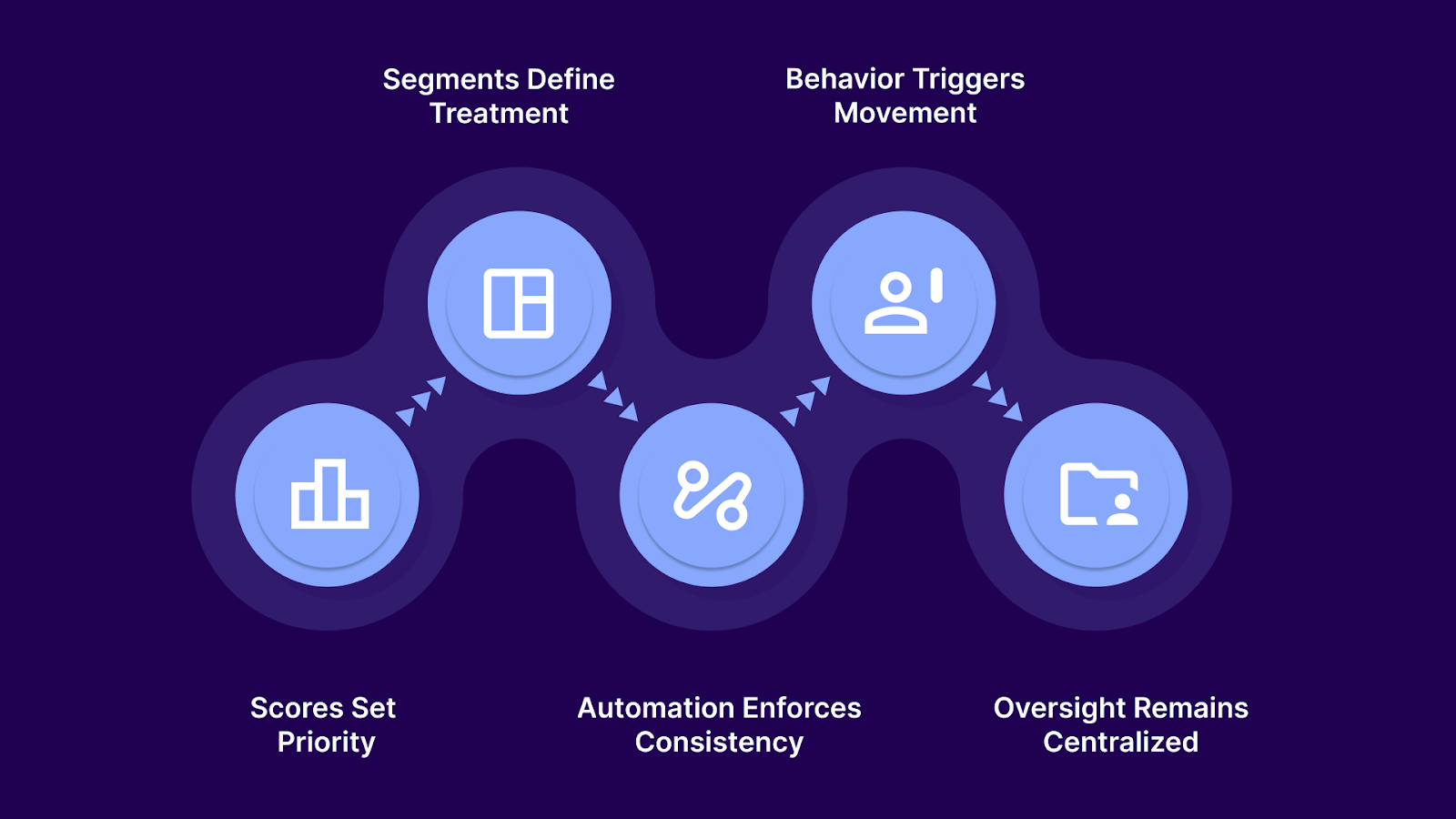

Scoring and segmentation work together to translate data insights into structured recovery execution. Scoring assesses the likelihood and timing of repayment, while segmentation determines the recovery strategy for each account group.

This is how predictive scoring and consumer segmentation interact in practice:

Tratta supports this execution layer by turning segmentation rules into system-driven workflows. It centralizes payment activity, consumer interactions, and audit records. This helps teams apply scoring- and segmentation-based strategies consistently. Schedule a free demo.

Smart scoring and segmentation replace intuition-based decisions with structured prioritization, allowing agencies to improve recovery performance without increasing contact volume or operational risk.

These are the key benefits:

These benefits depend on selecting the right scoring models for the right purpose. The next section explores the primary types of scoring used in debt recovery and how each supports effective segmentation and execution.

Suggested Read: Challenges Faced by Credit Officers & Their Impact on Collections

High-performing collection programs focus on a small set of predictive scores that directly influence prioritization, engagement, and recovery outcomes. These scoring types are the most actionable and widely applicable across collection environments.

Payment likelihood scoring predicts whether an account is likely to make a payment within a defined time window. It is the primary driver of account prioritization and determines where recovery effort should be concentrated.

This score is primarily used to guide priority decisions:

Payment timing scoring predicts when an account is most likely to respond or pay. It improves efficiency by aligning outreach with moments of highest engagement rather than increasing contact volume.

This score is primarily used to optimize outreach execution:

Channel responsiveness scoring predicts which communication channel an account is most likely to engage with. It reduces ineffective contact attempts and improves customer experience by meeting consumers where they are most responsive.

This score is primarily used to guide channel strategy:

Plan adherence scoring estimates whether an account is likely to remain compliant with a payment plan once enrolled. It helps control plan eligibility and prevents repeated plan failures. This score is critical for maintaining recovery momentum over time.

This score is primarily used to protect plan performance:

Some predictive models, such as settlement acceptance or highly granular behavioral scores, are better introduced after core execution is stable. Over-scoring too early adds complexity without improving outcomes. For most teams, fewer, well-integrated scores outperform complex models that are not operationalized.

Predictive scoring identifies opportunity, but it does not define a recovery strategy on its own. The next section explains how segmentation uses these scores to structure recovery treatments and enforce consistent execution.

Suggested Read: Machine Learning Tools for Customer Risk Assessment in Collections

Segmentation translates scoring insights into repeatable recovery strategies. Instead of making decisions at the individual account level, segmentation groups accounts by shared characteristics so each group follows a defined treatment path.

Stage-based segmentation groups accounts by delinquency or recovery stage. It ensures early-stage accounts are handled differently from late-stage or escalated balances. This model prevents premature escalation while maintaining structure.

This model is primarily used to control recovery progression:

Value-based segmentation groups accounts by balance size or expected recovery value. It helps agencies align effort with financial impact rather than volume alone. This model is critical for margin control.

This model is primarily used to align effort with value:

Behavior-based segmentation groups accounts based on responsiveness, payment activity, and engagement history. It allows strategies to adapt as behavior changes. This model keeps recovery execution responsive.

This model is primarily used to adapt strategy dynamically:

Channel-based segmentation assigns accounts to communication strategies based on preferred or effective channels. It improves engagement while reducing unnecessary contact. This model supports omnichannel efficiency.

This model is primarily used to improve engagement efficiency:

Compliance-sensitive segmentation flags accounts that require special handling due to disputes, consent limits, or regulatory constraints. It does not drive recovery intensity but governs how recovery is executed. This model is essential in regulated environments.

This model is primarily used to enforce recovery boundaries:

When segmentation is driven by scoring and enforced through automation, recovery execution becomes more consistent and defensible. The next section examines the compliance benefits.

Suggested Read: Advanced Collection Software Strategies for 2025

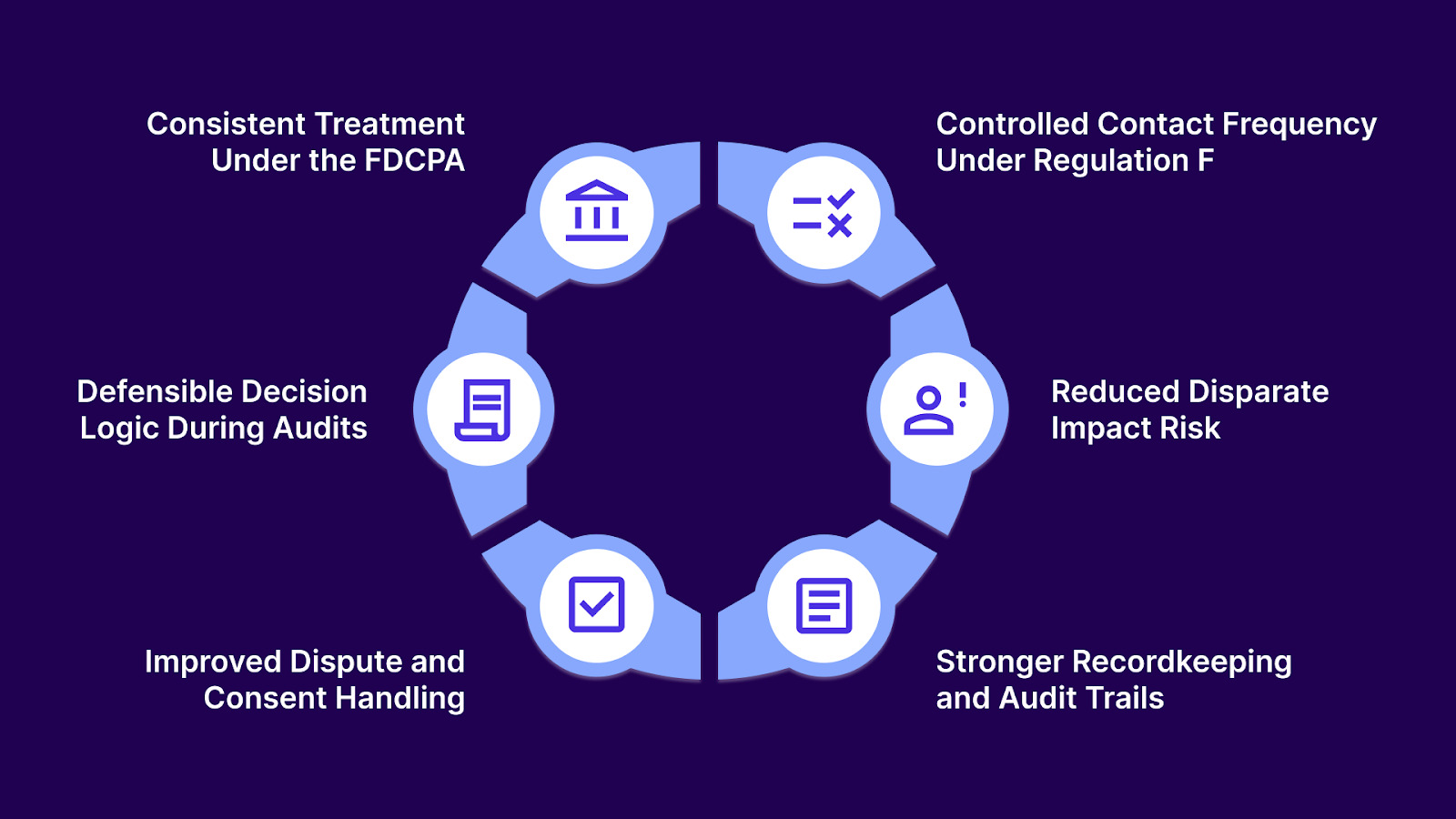

In regulated collection environments, compliance failures often stem from inconsistent treatment, unclear prioritization, and excessive manual discretion. Scoring and segmentation help replace ad-hoc decision-making with structured, repeatable logic that aligns recovery execution with regulatory expectations.

These are the key compliance benefits:

Tratta embeds compliance controls directly into recovery workflows through its Compliance-by-Code architecture. The platform maintains detailed audit trails, supports dynamic disclosures and state-specific compliance, and tracks consent and dispute activity to reduce manual risk.

When insights are disconnected from execution, agencies end up with sophisticated analytics that do not change outcomes. The issues below are the most common reasons scoring and segmentation programs underperform.

Table showing mistakes in predictive scoring and segmentation:

To keep scoring and segmentation effective over time, organizations should focus on a few execution fundamentals:

Avoiding these mistakes requires the right technology to operationalize scoring, enforce segmentation rules, and maintain compliance at scale.

Suggested Read: Collections Automation for U.S. Agencies: Proven Ways to Cut DSO

Tratta is a debt collection and receivables automation platform built to help agencies, law firms, debt buyers, and original creditors improve recovery performance with consistent, compliant workflows and consumer-centric features.

It combines payments, communications, reporting, and compliance controls into a single system so teams can act on scoring and segmentation insights without switching tools.

These are the core features that enable scoring-driven, segment-based recovery execution in real environments.

Tratta’s portal lets consumers view balances, make full or partial payments, and set up or adjust payment plans independently. It reduces the friction that often stalls early recovery and encourages voluntary resolution. Dynamic notifications and embedded payment options help improve engagement and accelerate cash flow.

Tratta supports integrated payment processing for card, ACH, and other methods directly within the recovery workflow. This minimizes payment abandonment and accelerates settlement. Real-time balance validation and flexible routing make reconciliation smoother and reduce operational touchpoints.

Automated interactive voice response (IVR) supports multiple languages, enabling consumers to make payments by phone. This expands reach across diverse populations and improves access for non-digital users. Delivering IVR payment options improves accessibility without manual call handling.

Tratta enables coordinated outreach via SMS, email, voice, and portal links as part of campaign workflows. It supports dynamic, trackable messaging that can be aligned with score-based segments. Consistent communications help reinforce priority strategies without manual trigger logic.

Users can build automated campaigns with smart scheduling, triggers, and follow-ups aligned with scoring and segmentation logic. Automation ensures accounts move through the appropriate workflows without manual reassignment. This reduces bottlenecks and improves execution consistency.

Tratta’s real-time analytics and customizable reporting provide visibility into payment behavior, segment performance, and channel effectiveness. Teams can identify recovery trends and refine scoring/segmentation logic based on outcomes. Shareable dashboards support performance measurement and decision-making.

The platform lets organizations tailor notices, payment options, communication templates, and portal layouts to match business rules or customer segments. This ensures that scoring and segmentation strategies can be operationalized to meet specific operational or regulatory needs.

Tratta offers REST APIs and secure integrations so scoring outputs and segment rules can work with core systems like CRM, ERP, or legacy collections tools. This seamless connectivity ensures scoring-driven actions are fed into execution workflows without manual syncs.

Tratta is designed with strong security protocols, SOC 2 Type II and PCI DSS Level 1 compliance, encrypted payment handling, and dynamic disclosures that align with regulatory requirements. Detailed audit trails and role-based controls support defensibility and risk management.

By embedding execution logic into the platform, agencies and creditors can turn data insights into measurable recovery outcomes. This can be done faster and with greater consistency than legacy or fragmented systems allow.

Scoring prioritizes opportunity, segmentation governs treatment, and automation enforces discipline across every stage of recovery. When predictive scoring models are disconnected from workflows or segmentation is applied inconsistently, recovery teams see little improvement and often introduce new compliance and operational risks.

Tratta supports scoring-driven recovery by providing the execution layer that many programs lack. Its consumer self-service tools, automated workflows, real-time reporting, and compliance controls allow scoring and segmentation strategies to operate consistently in day-to-day recovery operations.

If your scoring and segmentation efforts are not translating into real recovery gains, it may be time to reassess execution. Talk to our team to explore how scoring-driven recovery can work in your environment.

Scoring models should be reviewed regularly, especially when payment behavior, portfolio mix, or economic conditions change. Many organizations reassess performance quarterly to ensure models remain predictive and aligned with current recovery outcomes.

Yes. Segmentation supports compliance by enforcing consistent treatment within defined groups, controlling contact frequency, and documenting decision logic. This reduces subjective handling and helps create defensible, auditable recovery processes.

The 7-7-7 rule limits contact attempts to no more than seven calls within seven days, across no more than seven consecutive days. It helps reduce over-contact risk and supports compliance with consumer communication standards.

The four R’s typically refer to Risk, Return, Reliability, and Responsiveness. Together, they help lenders and collectors evaluate payment likelihood, expected recovery value, data consistency, and behavioral signals that influence scoring accuracy.

The three C’s are Consistency, Communication, and Compliance. Effective collection strategies apply consistent treatment, communicate clearly across channels, and operate within regulatory boundaries to improve recovery outcomes and reduce operational risk.