Every collection team has rules, but few have a system that enforces them consistently. That gap is where recoveries stall, and compliance risk grows.

According to Federal Reserve data, the delinquency rate on credit card loans at U.S. commercial banks was 2.98% in the third quarter of 2025, leaving many receivables unpaid for more than 30 days.

An accounts receivable collection policy is not a documentation exercise. It determines how quickly accounts move, how consistently collectors act, and how reliably money is recovered.

Most agencies already have policies, but they live in manuals instead of workflows. Collectors interpret them differently. Escalations happen late. Outcomes vary across similar accounts.

This guide explains what an effective AR collection policy must define, why most policies fail in execution, and how high-volume teams enforce policies without relying on individual judgment.

An accounts receivable collection policy is a documented framework that defines how past-due accounts are managed and collected. It establishes when customers are contacted, which communication channels are used, which payment options are offered, and when accounts are escalated to collections or legal action.

The policy standardizes collection activity by linking required actions to account factors such as delinquency stage, balance, and payment history. This ensures accounts are handled consistently across teams and portfolios.

A well-defined accounts receivable collection policy:

A collection policy provides structure for consistent execution and effective accounts receivable management.

Credit and collection policies apply at different stages of the receivables lifecycle. They are often referenced together, but they govern different decisions and are owned by different teams.

This comparison clarifies where responsibility shifts once an account moves from active billing to delinquency management.

Once an account becomes overdue, control shifts from credit policy to collection policy. Treating these as separate but connected frameworks allows organizations to respond to delinquency without delaying action or blurring accountability.

Suggested Read: Best Practices for Improving Law Firms' Accounts Receivable Process

Any organization that extends credit or manages past-due balances needs an accounts receivable collection policy. The policy defines how delinquent accounts are handled and ensures collection activity is consistent, compliant, and measurable.

The need applies to the following groups:

Any organization handling past-due accounts without a documented collection policy relies on individual judgment, increasing operational inconsistency and compliance risk.

Suggested Read: Main Benefits of Accounts Receivable Automation

No federal law mandates that you have a written accounts receivable collection policy. However, the Fair Debt Collection Practices Act regulates how you collect debts, and a policy helps ensure compliance. Your policy should embed these legal requirements into daily operations:

Many states add stricter requirements. California limits contact attempts, New York requires specific licensing and bonding, and Massachusetts prohibits certain collection tactics. Your policy must comply with the most protective regulation applicable to each account.

Translating these legal requirements into daily collection activity is where many organizations struggle. Platforms like Tratta help creditors and collection agencies apply communication rules, disclosure requirements, and documentation standards consistently across every account, reducing compliance risk without increasing manual oversight. Book a free demo to discover how it can help.

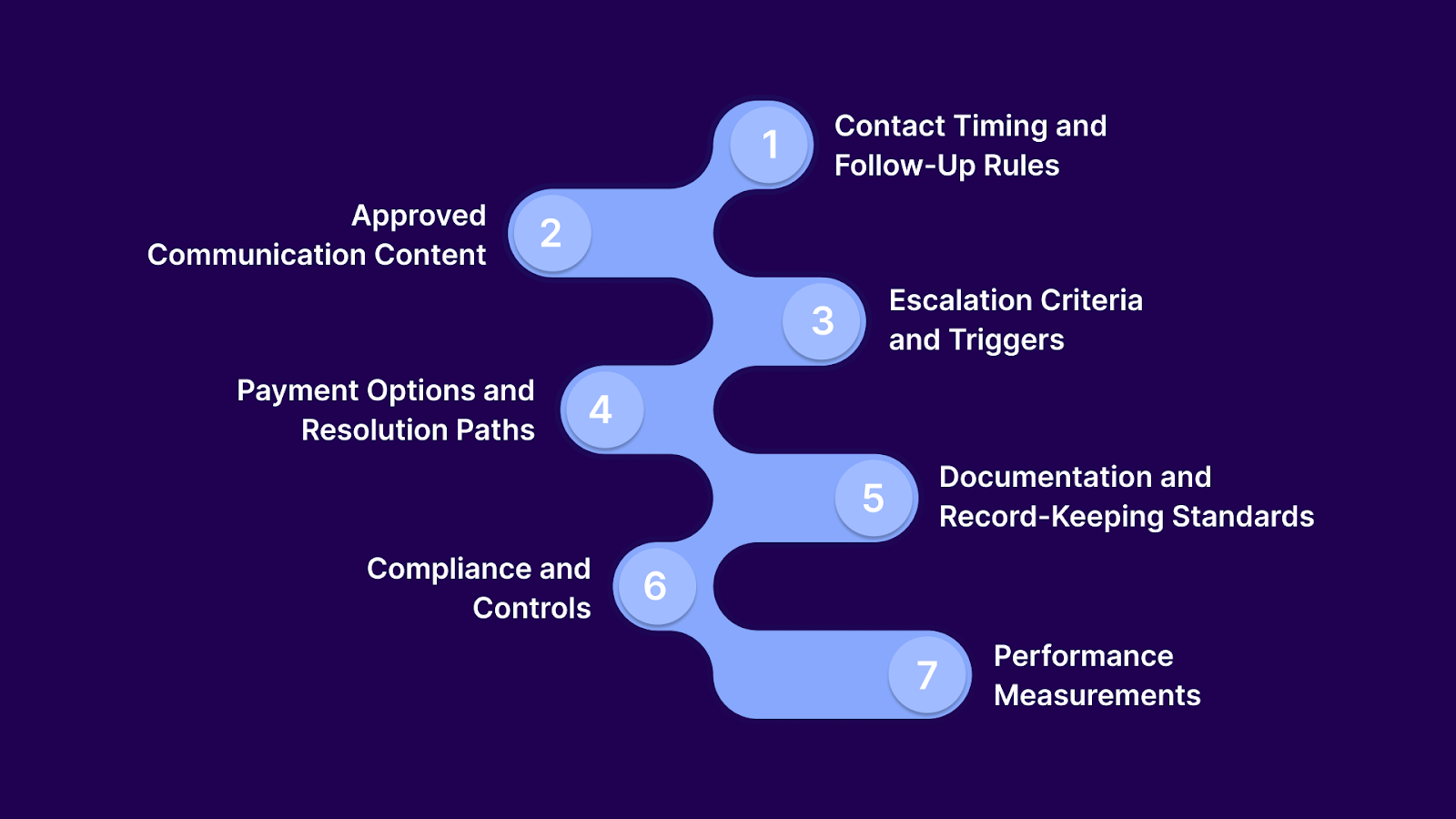

An effective accounts receivable (AR) collection policy must go beyond high-level wording and clearly specify the actions, thresholds, documentation, and controls used to collect overdue payments. It should guide collectors step by step and tie to measurable outcomes.

To function in daily operations, an AR collection policy must clearly specify the following elements.

When these elements are clearly defined, a collection policy becomes a practical operating standard rather than a set of guidelines.

Suggested Read: Top 10 KPI Metrics for Effective Tracking of Accounts Receivable

Creating an effective policy requires more than filling in a template. Follow this process to build a policy that drives results.

Document how accounts are actually worked today, not how you think they should be worked. Identify which practices drive results and which create problems.

Talk to your collectors about what works and what does not. Review accounts that resolved quickly versus those that aged unnecessarily. Find patterns in successful recovery and failed attempts.

Establish what your policy should achieve:

Your policy should support these objectives through specific procedures and controls.

Review the FDCPA requirements and all applicable state regulations for your operation. Identify the most restrictive rules that apply to your accounts.

Consult legal counsel to ensure your policy complies with all regulatory requirements. Document which regulations drove specific policy decisions.

Create contact schedules based on account age and debtor response patterns. Use data from past accounts to determine optimal contact frequency.

Define escalation triggers using specific, measurable criteria. Eliminate subjective judgment from escalation decisions.

Specify which payment options you offer and under what conditions. Establish clear approval levels for payment plans and settlements.

Your payment options should balance recovery effectiveness with operational efficiency. Self-service options reduce the collector's workload while giving debtors control over the resolution.

Translate FDCPA and state law requirements into specific collector actions. Include disclosure templates, timing restrictions, and prohibited practices with examples.

Your compliance section should tell collectors exactly what to do and what to avoid in common scenarios.

Define who does what across your collection operation. Eliminate gray areas where tasks might fall through gaps or create redundancy.

Include decision authority levels for payment arrangements, settlements, and escalations. Collectors should know when they can act independently and when they need approval.

Define how you will measure policy adherence and effectiveness. Create reporting processes that show both recovery performance and compliance metrics.

Schedule regular policy reviews to incorporate performance data, regulatory changes, and client feedback.

Have your legal counsel review the policy before rolling it out. Ensure all FDCPA requirements are met, and state-specific rules are addressed.

Document any legal recommendations and incorporate them into the final policy.

Train all collectors on the new policy before implementation. Use real account examples to demonstrate how the policy applies in practice.

Configure your collection software to enforce policy rules wherever possible. Automated controls are more reliable than individual compliance.

Collection platforms like Tratta are designed to enforce these controls by embedding policy rules directly into workflows, outreach, payments, and reporting. This ensures the policy you design is applied consistently across all accounts once it goes live. Book a demo to see how it supports policy-driven collections.

Suggested Read: Understanding Accounts Receivable: An Analysis and Calculator Guide

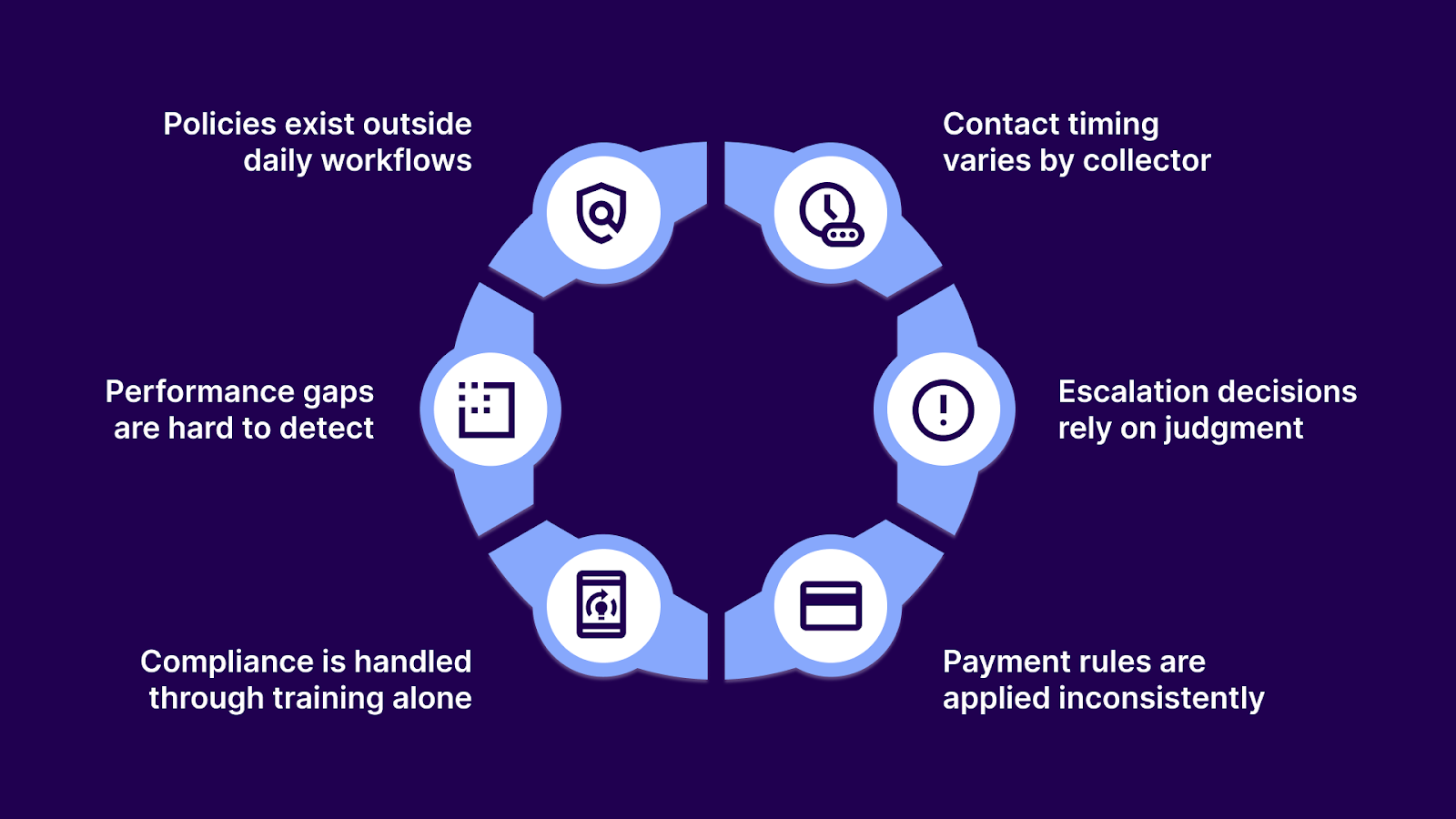

Many organizations have an accounts receivable collection policy in place, yet still experience inconsistent results, rising delinquency, and compliance exposure. These issues typically stem from execution failures rather than policy design.

Collection policies are often documented in manuals or internal documents, but not embedded into the systems collectors use every day. As a result, policy adherence depends on individual memory and interpretation.

Without system-enforced schedules, follow-up timing can differ from one collector to another. Some accounts are contacted too frequently, while others receive delayed or missed outreach, reducing recovery effectiveness.

When escalation criteria are not applied automatically, decisions are made inconsistently. Accounts may be escalated too early, too late, or not at all, resulting in uneven recovery outcomes across similar accounts.

Policies may define approved payment plans or settlement thresholds, but manual enforcement results in exceptions that go untracked or unjustified. This introduces risk and reduces predictability in recovery performance.

Training is important, but it cannot prevent errors in high-volume environments. Without system-level controls, prohibited contact times, missing disclosures, and incomplete documentation still occur.

When policy execution is not tracked in real time, managers lack visibility into missed follow-ups, broken escalation paths, and stalled accounts. Issues are identified only after results decline or complaints arise.

These failure points highlight a common reality. A collection policy only drives results when it is consistently enforced across the systems and workflows used to manage accounts at scale.

Creditors and collection agencies define accounts receivable collection policies to control follow-up, escalation, payment handling, and compliance. The challenge is not writing the policy but applying it consistently across large account volumes. Tratta is a collection and recovery platform that translates written collection policies into automated, system-driven execution.

The following platform features show how Tratta supports consistent enforcement of AR collection policies in day-to-day operations.

Automated workflows apply collection policy rules as accounts move through delinquency stages. Actions trigger when predefined conditions are met, such as account age, missed payments, or broken payment plans, ensuring follow-up and escalation occur on time without manual intervention.

The self-service portal allows consumers to view account details, make payments, and enroll in payment plans. This supports policy-approved resolution paths, reduces reliance on manual outreach, and improves payment accessibility.

Outreach is supported across phone, SMS, email, and IVR within defined timing and frequency limits. Required disclosures are applied consistently across all communication channels to align with policy and regulatory requirements.

Campaigns enable outreach sequences to be configured around collection policy rules. Accounts can be segmented by age, balance, or behavior, with each segment following defined contact schedules and messaging standards.

All communication activity, payment commitments, disputes, and status changes are recorded automatically. Documentation occurs as part of the normal workflow, creating a complete and consistent audit trail.

Dashboards provide visibility into follow-up completion, missed escalation thresholds, recovery progress, and collector activity. This allows managers to identify gaps in policy execution without manual reporting.

Communication restrictions, contact limits, and disclosure requirements are enforced directly within the platform. These controls help ensure collection activity remains aligned with internal policy and applicable regulations.

Tratta enables creditors and collection agencies to move from documented collection policies to consistent execution across every account. Policy rules become operational controls that guide follow-up, payments, and escalation at scale.

Your accounts receivable collection policy determines whether delinquent accounts resolve efficiently or become costly write-offs. Without a documented policy, collection activities depend on individual judgment. With a policy that lacks system enforcement, execution gaps create compliance risk and inconsistent results.

Effective policies define exact contact timing by account age, clear escalation triggers, specific payment options with authorization levels, complete documentation requirements, defined staff roles, and measurable performance metrics. But written policies alone cannot change outcomes. The policy must be enforced through automated workflows, built-in compliance controls, and real-time monitoring.

Tratta enables this enforcement by turning your collection policy into executable workflows. Automated outreach, self-service payments, compliance safeguards, and performance dashboards work together to ensure your policy drives consistent results across every account.

See how automation can reduce manual effort, improve recovery outcomes, and strengthen compliance across your operation. Speak with our team today.

It flags customer accounts as high-risk if ≥10% of their total outstanding invoices are overdue, requiring proactive measures like tighter credit or escalation.

An accounts receivable insurance policy protects businesses from customer nonpayment risk, but does not replace the need for active collection and follow-up processes.

The 5 C’s are character, capacity, capital, conditions, and collateral, used to assess credit risk before extending credit to a customer.

Federal law does not require it, but written policies help agencies standardize practices, support compliance, and demonstrate control during audits and client reviews.

At least annually and whenever regulations, client requirements, or recovery performance change to ensure ongoing compliance and effectiveness.