Law firm accounts receivable is one of the most overlooked pressure points in legal operations. Work may be completed and invoices sent, but cash does not always follow on time.

Industry data shows that collections continue to challenge law firms, with unpaid invoices and write-downs affecting overall revenue realization across the sector. For firms handling large volumes of creditor accounts, even small delays in billing, follow-up, or payment processing can quickly result in aging receivables.

Improving law firm accounts receivable does not come down to increasing follow-up alone. It requires a structured approach in which invoices move forward consistently, issues are identified early, and recovery remains predictable.

This guide explains how collection law firms can manage receivables more effectively, reduce aging, and maintain steady cash flow through clear processes and better visibility.

Accounts receivable (AR) refers to the money your firm has earned through legal services but has not yet collected. In a standard law firm, that means outstanding client invoices. In a collection law firm, the picture is more layered.

Your firm earns revenue through contingency fees, flat-fee arrangements, or hourly billing tied to the recovery outcomes you generate for creditors, debt buyers, or financial institutions. That revenue depends on you actually collecting from debtors on your clients' behalf, invoicing your clients correctly for that work, and receiving payment promptly against those invoices.

When any link in that chain breaks, AR grows. And unlike general practice firms, your pipeline volume is usually high. More accounts mean more chances for AR to accumulate, age, and eventually become uncollectible.

Most collection law firms carry two AR burdens simultaneously:

Many firms focus heavily on debtor recovery while letting firm-side AR drift. That imbalance creates cash flow pressure that makes it harder to staff, invest in technology, or scale.

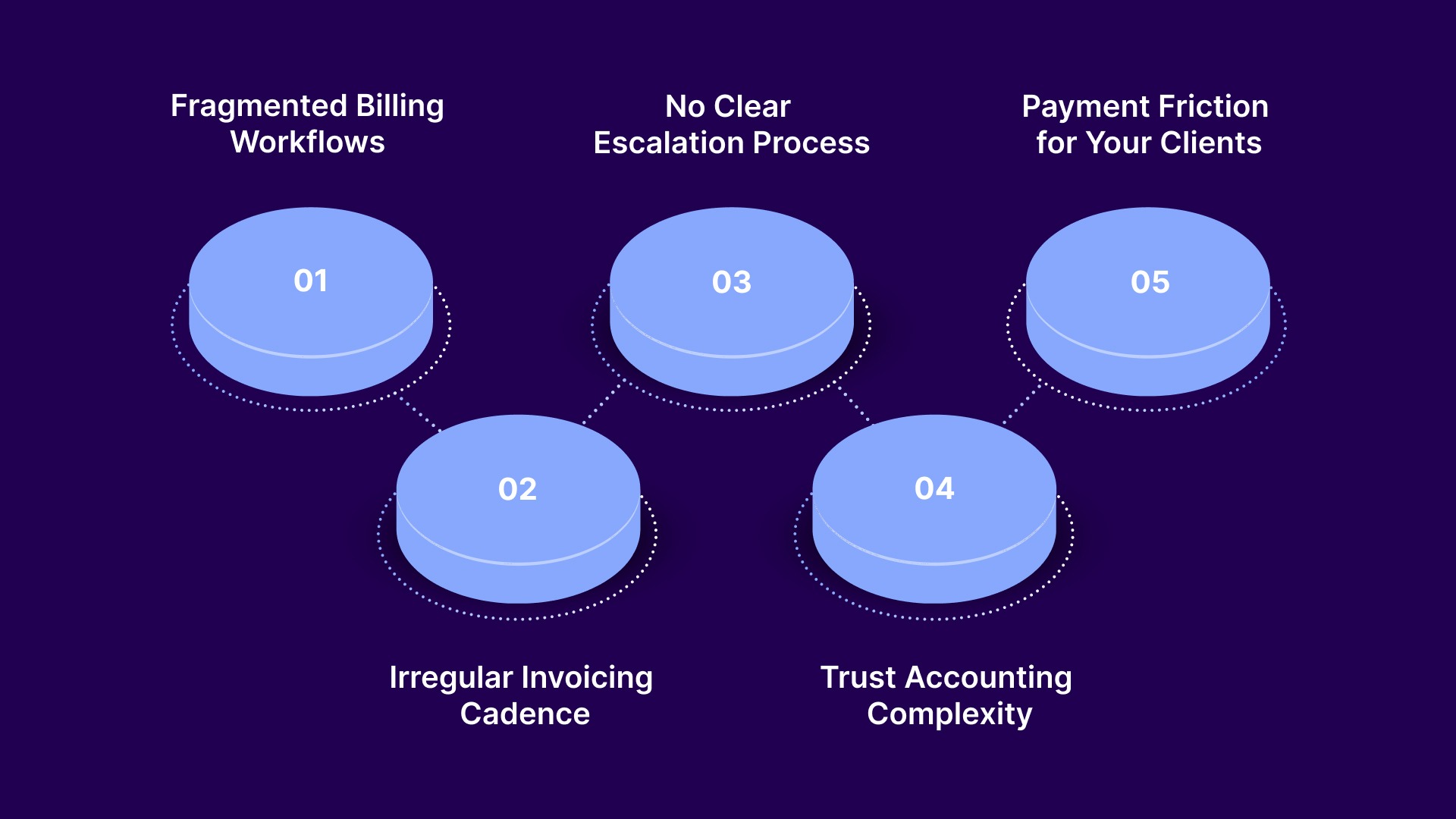

Understanding why AR ages is the first step to reducing it. The causes are usually predictable and fixable.

Many collection law firms use separate tools for case management, billing, payment processing, and reporting. When these systems do not talk to each other, invoices get delayed, errors go uncaught, and follow-up falls through the cracks.

An attorney closes out a matter. The billing entry sits in one system. The invoice is generated in another. Payment is tracked in a spreadsheet. By the time someone flags a 60-day-old unpaid invoice, the window for easy collection has narrowed significantly.

Firms that bill inconsistently give clients an implicit permission structure: payment is optional until someone chases it. Industry experience indicates that the likelihood of fully recovering accounts receivable diminishes substantially once balances are around 180 days past due. The longer the delay between completed work and invoice, the older that AR is before the clock even starts.

What happens when an invoice is over 30 days old? If the answer is 'someone probably sends a reminder email,' that is a process gap. Without defined escalation steps tied to aging brackets, AR recovery depends on who has time, not on who has a system.

For collection law firms, trust accounting adds another layer of AR risk. Client retainer funds held in IOLTA accounts cannot be accessed until work is approved. If clients are slow to approve billing, earned fees sit in trust longer than necessary. Reconciliation errors can further delay release, creating AR aging that is not actually about the client's unwillingness to pay.

Even when a creditor client is ready to pay your firm's invoice, friction in the payment process causes a delay. Clients who can only pay by check or wire transfer take longer to close out invoices. Digital payment options significantly reduce that friction.

This matters particularly when your clients are large credit issuers or financial institutions running their own AP cycles. Their internal payment approval processes already add time. If your firm then requires a non-digital payment method on top of that, you are stacking delays that have nothing to do with willingness to pay.

Suggested Read: 2026 Guide to Law Firm Accounts Receivable Software

If you do not have a current AR aging report, generating one is your first step. An AR aging report categorizes your outstanding invoices by how long they have been unpaid. It gives you a clear picture of where your cash is sitting and what your realistic recovery looks like.

Here is how to interpret the standard aging brackets for a collection law firm:

Note: Recovery likelihood figures are general benchmarks based on industry data. Your actual results will vary by client type, fee arrangement, and collection history.

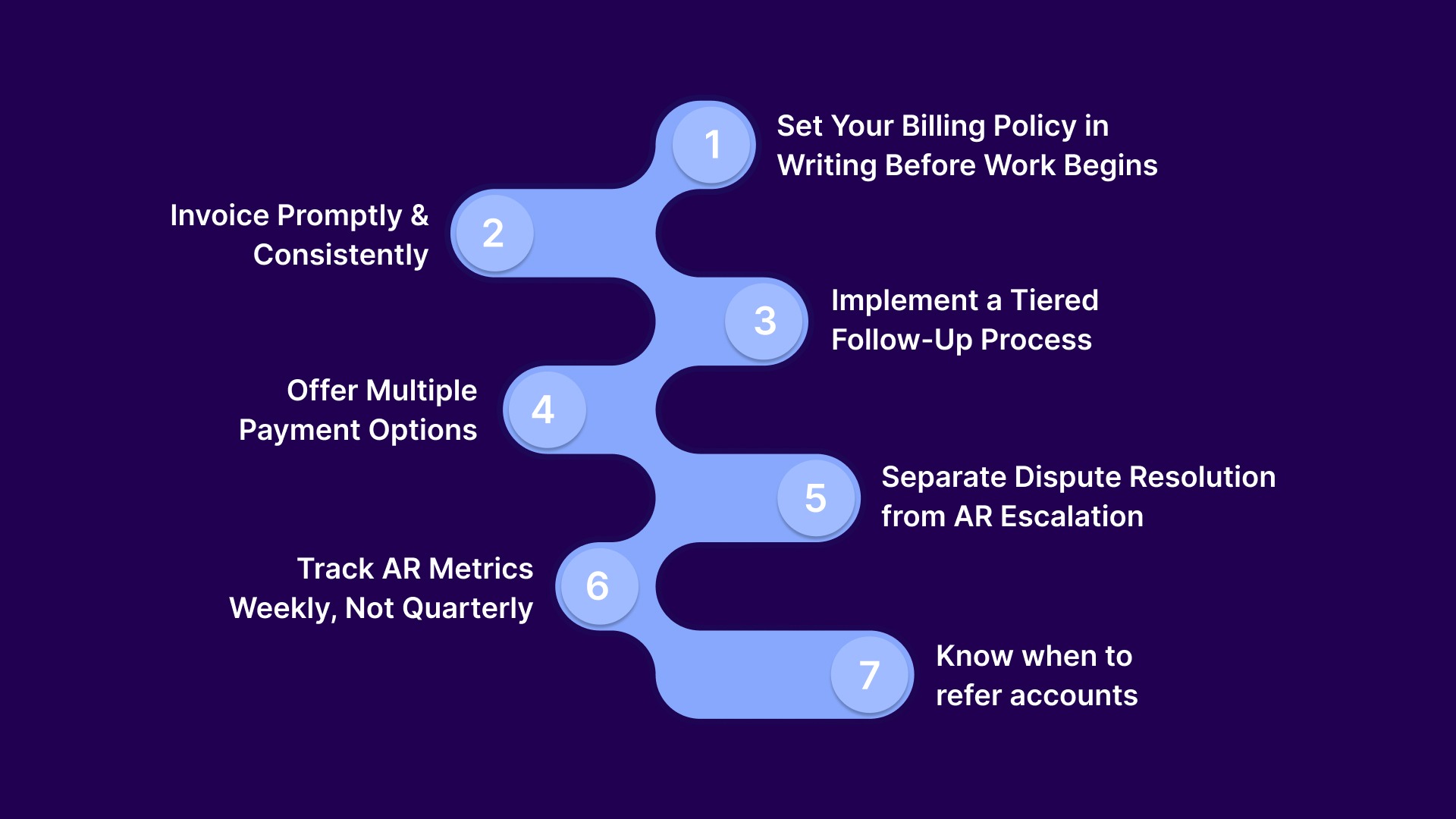

Good accounts receivable management for law firms is not about working harder on follow-up. It is about designing a system where invoices get sent on time, aging is visible, and escalation is automatic rather than dependent on someone's bandwidth.

Here is a framework built specifically for the operational realities of collection law firms.

Every client engagement should include a written billing policy, ideally embedded in the engagement letter. This should specify the billing cycle (weekly, bi-weekly, or monthly), the payment terms (Net 15, Net 30), accepted payment methods, and any consequences for late payment.

Clients who sign engagement letters with explicit billing terms pay faster. They cannot claim surprise when an invoice arrives, and disputes are easier to resolve because expectations were set at the start.

The fastest way to reduce your AR aging average is to shorten the gap between work performed and invoice sent. For collection law firms handling hundreds or thousands of accounts, this requires a consistent billing cadence tied to your case management system.

If you are billing monthly, set a firm date and hold to it. If you are working on contingency, invoice fees immediately upon recovery. Every day between completed work and the invoice sent is a day added to your AR age.

Manual follow-up is inconsistent because it depends on who has time. A tiered process removes that variable:

The exact thresholds can shift based on your client relationships, but the key is that escalation is automatic and documented, not dependent on memory.

Clients who can only pay by check or ACH wire introduce a delay by default. Firms that accept digital payments, including credit cards and online portals, consistently report faster invoice closure.

This matters especially when your clients are financial institutions, debt buyers, or credit issuers who have their own AP departments and processing timelines. Giving them a simpler path to payment reduces their friction and your waiting time.

When a client disputes an invoice, it should not sit in the same queue as a standard overdue notice. Disputes require investigation. Aging invoices require follow-up. Mixing them creates confusion and often delays both.

Build a clear process for flagging disputed invoices separately, documenting the basis of the dispute, and resolving them within 10 to 15 business days. Resolved disputes convert faster to payments than ones that drift.

The firms that manage AR well are not running end-of-quarter reports. They are reviewing key metrics weekly: Days Sales Outstanding (DSO), collection rate by client or practice area, invoice aging by bracket, and dispute volume. These metrics show you where the process is breaking before it becomes a write-off decision.

For firm-side AR past 180 days with no client engagement, the decision is binary: write it off or refer it out. Attempting internal recovery beyond that point costs more in staff time than the expected return. A referral to an external collection specialist is an operational decision, not a failure. The key is having a written policy that triggers it automatically, not a case-by-case judgment that delays it indefinitely.

Managing high-volume AR across creditor clients is operationally complex. Tratta's Reporting and Analytics tools give collection law firms real-time visibility into account status, payment activity, and recovery performance, so your team can prioritize the right accounts at the right time.

Explore Tratta's Reporting and Analytics Tool

Suggested Read: How To Calculate Average Net Accounts Receivable: Definition, Formula & Examples

Accounts receivable issues do not always come from delayed billing. In many cases, invoices are sent on time, reminders are issued, and payment still does not follow. At that point, the approach needs to shift from routine follow-up to targeted collection action.

Here is how collection law firms handle accounts when standard follow-up fails to produce results.

A client who stops responding to invoices is not always refusing to pay. Silence often signals an unresolved issue, internal approval delay, or competing financial priorities.

The first step is a direct phone call from a named contact. Email reminders alone are easy to ignore and do not surface the underlying issue.

The objective of the call is clarity:

Getting a clear answer early allows the account to move forward. Continuing with automated reminders without direct contact usually extends the delay.

Disputes are common, particularly in contingency-based work where fee calculations or recovery methods may be questioned.

A dispute does not stop collection. It changes how the account should be handled.

To manage disputes effectively:

Accounts supported with clear documentation resolve faster. Without it, disputes tend to extend and delay payment further.

On the debtor side, lack of response reduces recovery rates and delays fee realization. Accounts that stall at this stage often require a change in engagement approach rather than repeated outreach attempts.

Firms that improve recovery on inactive accounts focus on access and flexibility:

Higher recovery consistency leads to faster case closure, which shortens the time between recovery and invoicing.

Some accounts reach a point where continued internal effort is no longer efficient.

For firm-side receivables with no payment activity or engagement beyond a defined period, a structured referral decision is more effective than continued follow-up.

To manage this consistently:

Many collection law firms use an internal policy that triggers referral after accounts have remained unpaid for several months, helping to focus internal effort on receivables with a higher likelihood of recovery.

Suggested Read: Understanding Integrated Receivables Solutions and Payment Processing

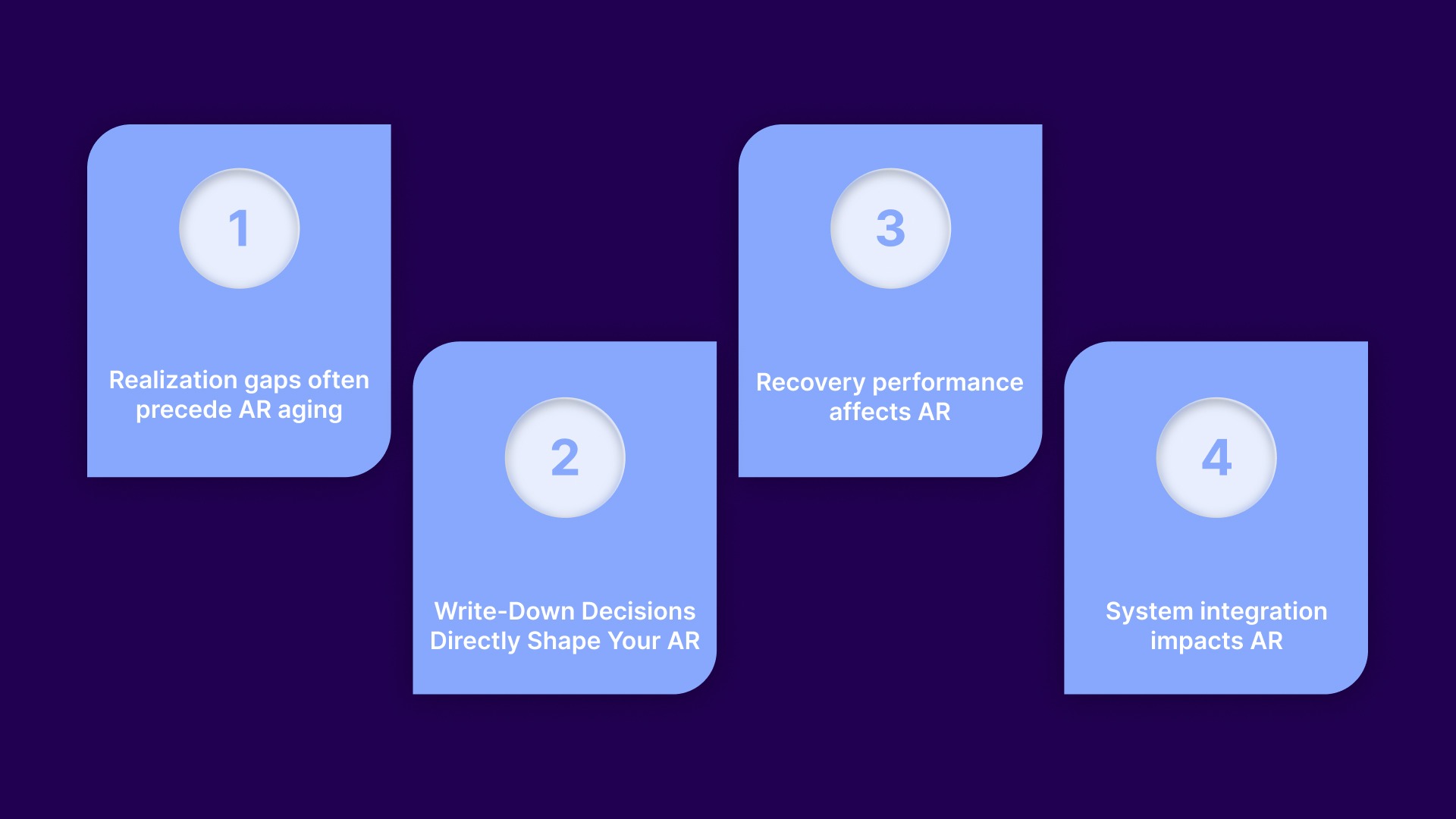

Most accounts receivable issues in collection law firms do not begin at the point of follow-up. They start earlier, in how revenue is realized, recorded, and moved into the billing process.

Addressing these upstream gaps changes both how much revenue reaches your AR pipeline and how long it remains there.

Accounts receivable begin when work is completed, not when an invoice is sent.

Many firms carry a delay between completion and invoicing due to batching, internal approvals, or workflow gaps. That delay increases the baseline age of every receivable before the client has even been billed.

For contingency-based work, this effect is more pronounced. Recovery is completed, but billing waits for a cycle instead of being triggered immediately.

To reduce this gap:

Reducing this delay improves cash flow without increasing workload. It ensures that receivables start aging only after the invoice is actually issued.

Write-downs affect how much value enters your receivables before the collection process even begins.

When handled inconsistently, they introduce revenue variability and make AR outcomes harder to predict across clients and matters.

To bring control into this process:

This makes write-downs visible and measurable, rather than informal adjustments that reduce realized revenue.

For collection law firms, accounts receivable is closely tied to how quickly debtor-side recoveries convert into earned fees.

When payments from debtors are completed faster, fees are realized sooner. That directly reduces the time those amounts sit as receivables on your books.

Improving debtor payment access supports this:

These changes improve recovery timing, which in turn improves how quickly revenue moves through your AR cycle.

Accounts receivable performance depends heavily on the level of integration among your systems.

When case data, billing, payments, and reporting are handled across separate tools, delays occur at each handoff. Information becomes outdated, and follow-up depends on manual coordination.

To improve consistency and control:

This creates a more reliable AR process in which decisions are based on current information rather than delayed or fragmented data.

Tratta is debt-collection software designed for collection law firms, credit issuers, and agencies. It centralizes payments, communications, reporting, and workflow controls on one platform, helping your team recover more while maintaining documentation and process consistency across all accounts. See how Tratta supports collection law firm AR workflows.

Suggested Read: 7 Ways Agencies and Law Firms Use Digital Workflows for Legal Recovery

Even with defined billing processes and escalation workflows in place, accounts receivable can still break down at the execution level. Small gaps in ownership, timing, or communication often create delays that compound over time.

The following are common mistakes collection law firms make in managing accounts receivable, and how to correct them before they impact cash flow.

When invoices remain unpaid for more than 30 days, recovery probability declines while resolution effort increases.

Fix: Trigger direct outreach early, not at the end of the billing cycle.

When the same workflow handles invoicing and follow-up, accountability weakens, and delays go unnoticed.

Fix: Assign clear ownership for billing and a separate owner for escalation and recovery.

Unclear payment timelines or methods lead to disputes, delays, and inconsistent client behavior.

Fix: Define billing cycles, payment terms, and accepted methods clearly in every engagement.

Email-only follow-ups are easy to ignore, especially for busy creditor clients managing multiple vendors.

Fix: Use a mix of channels, including phone and named contacts, for overdue accounts.

Continuing internal follow-up on accounts with no engagement drains time without improving recovery outcomes.

Fix: Set a clear cutoff point for escalation, referral, or write-off and apply it consistently.

Suggested Read: Debt Collection Software For Law Firms And Attorneys

Managing law firm accounts receivable at scale requires more than defined billing policies and follow-up workflows. As account volume increases, execution gaps emerge across billing, payments, communication, and reporting.

Delays in updating payment status, missed follow-ups, and limited visibility into aging accounts create inconsistencies that directly impact recovery timelines and cash-flow predictability.

To address this, collection law firms need systems that connect every stage of the receivables lifecycle and enforce process consistency across accounts.

Tratta supports this by centralizing payments, communications, reporting, and workflow controls into a single operational layer.

The platform enables law firms to manage receivables with greater accuracy and consistency through:

Allows clients and debtors to view balances, make payments, and resolve accounts independently. This improves payment speed while reducing reliance on manual follow-up.

Integrates payment processing directly into workflows, reducing friction and ensuring transactions are captured and reflected in real time.

Tracks interactions across email, SMS, IVR, and portal messaging, ensuring consistent follow-up and complete documentation for every account.

Provides real-time visibility into invoice status, aging, and recovery performance, allowing teams to prioritize accounts and act before receivables age further.

Applies structured escalation rules, payment triggers, and account handling logic across portfolios, reducing reliance on manual coordination.

Connects case management, billing, and payment systems into a unified view, eliminating delays caused by fragmented tools and data silos.

By aligning billing, payment activity, and follow-up within a single system, Tratta helps collection law firms reduce receivable aging, improve collection consistency, and maintain operational control as they scale.

Law firm accounts receivable ultimately comes down to how consistently your firm can move invoices from issuance to payment without delays or gaps. Firms that maintain visibility, act early on aging accounts, and keep workflows aligned are better positioned to protect cash flow and scale operations without added friction.

As account volumes grow, maintaining that consistency manually becomes increasingly difficult. Platforms like Tratta help bring payments, communications, and reporting into a single system, making it easier to manage receivables with control and clarity.

If your firm is looking to reduce aging and improve collection outcomes, book a demo with Tratta to experience how a more connected approach to accounts receivable can support your workflows.

Use historical collection patterns, client payment behavior, and aging trends to build rolling forecasts. Incorporate probability-based recovery assumptions instead of treating all receivables as equally collectible.

Early payment incentives can improve cash flow for select clients. However, they must be structured carefully to avoid unnecessary revenue loss or setting expectations for routine discounts.

Establish stricter payment terms, enforce escalation consistently, and evaluate profitability after delays. High-volume clients should still meet the defined timelines to avoid long-term cash-flow strain.

Assign clear ownership across billing, collections, and reporting. Typically, finance manages invoicing, while dedicated AR or operations roles handle follow-up, escalation, and performance tracking.

Compare metrics such as DSO, aging distribution, and collection rates with those of peer firms. Use industry benchmarks and internal historical data to identify gaps and set realistic improvement targets.