Debt collection via text messages is among the highest-performing outreach channels for recovery operations today. Yet the CFPB received 207,800 debt collection complaints in 2024, nearly double the prior year, and a significant share were tied to improper digital communications, including text messages.

For collection agencies, law firms, and credit issuers, the gap between channel performance and compliant execution is where most SMS programs break down. Sent to the wrong number, at the wrong time, without documented consent, a high-volume text campaign becomes a liability rather than a recovery tool.

This guide covers how debt collection via text messages works under the FDCPA, Regulation F, and the TCPA, along with workflow-stage templates, the metrics that tell you whether your program is working, and what to look for when scaling SMS across a high-volume portfolio.

Yes. Debt collectors can legally contact consumers via text message under the FDCPA, as clarified by Regulation F, which extends coverage to digital channels like SMS and email.

However, this is not unrestricted. Text messaging is permitted only within a defined compliance framework that governs how, when, and under what conditions consumers can be contacted.

At a high level, agencies must ensure:

Failure to meet these standards carries real risk. TCPA violations can result in $500 to $1,500 per message, with significant exposure at scale.

What this means in practice: SMS is legally allowed and highly effective, but it cannot be treated as a simple outreach channel. It requires structured workflows and controls to operate safely at scale.

Suggested Read: TCPA Compliance Guide for SMS Text Messages

SMS fits into a modern collection workflow as a scalable outreach layer that supports both early-stage prevention and late-stage recovery, without increasing dependence on agents. For debt collection agencies, it acts as the bridge between account status and payment action.

At a workflow level, SMS is used to trigger the right interaction based on account stage and consumer behavior, not as a one-off communication channel.

In practice, its role changes across the lifecycle:

SMS also reduces agent dependency. Routine outreach is automated, while complex scenarios (disputes, settlements) are handled with oversight.

Most importantly, SMS connects outreach directly to payment. With embedded links or portals, consumers can view balances, choose options, and pay without calling, shortening time to resolution and increasing coverage.

Used this way, SMS becomes a core driver of workflow, not just another communication channel.

Suggested Read: Understanding Text to Pay: A Simple Solution For Businesses

SMS improves collection performance by increasing reach, reducing friction, and automating routine work. Compared to traditional channels, it consistently delivers higher engagement and faster action.

SMS also improves agent efficiency by shifting routine interactions out of manual workflows:

This directly impacts cost. Agencies using digital-first approaches can reduce collection costs immensely while increasing account coverage.

At scale, SMS allows thousands of accounts to be reached simultaneously with consistent timing and messaging. The result is higher recovery per account, lower cost per interaction, and better utilization of agent time.

Suggested Read: How to Implement Billing Text Message Reminders?

Getting SMS compliance is highly operational. The agencies that handle it well build compliance logic into their workflows. The agencies that handle it poorly treat it as a checklist, and then discover the gaps during an audit or a complaint investigation.

This section summarizes the operational compliance requirements. It is not legal advice. Always consult qualified legal counsel for guidance specific to your organization.

Your right to text a consumer depends on consent. Regulation F permits text messages to consumer telephone numbers where:

Under TCPA, prior express consent is required before sending automated text messages. Consent must be documented and re-obtained periodically. Every 60 days is the standard recommended by Regulation F guidance.

Every message you send must make it easy for the consumer to stop receiving texts. When a consumer opts out, all text communication must stop immediately through that channel.

If your system does not suppress opted-out numbers automatically, you are one manual error away from a TCPA violation.

You may send debt-collection text messages only between 8:00 a.m. and 9:00 p.m. in the consumer's local time zone. Regulation F does not set a specific numerical cap on text frequency, the way it does for phone calls. The 7-in-7 rule applies only to calls.

That said, excessive messaging that could be deemed harassing remains prohibited under the FDCPA. Some state laws impose stricter limits. If you are operating across multiple states, confirm state-specific requirements before deploying campaigns.

Every SMS must clearly identify your agency. What you include and what you leave out both matter.

Avoid including full balance amounts or creditor names in messages where the phone may be shared. Third-party disclosure is one of the most frequently cited compliance concerns in SMS debt collection. Texts are far easier to screenshot and use in litigation than phone calls.

Managing consent records, opt-out flags, and time restrictions manually creates gaps that grow with every account you add. Tratta is built to enforce these controls at the system level, so every SMS campaign runs within documented, compliant parameters. Book a demo and explore how Tratta handles compliance for high-volume collection operations.

Compliance sets the floor. Message quality determines performance above it. The agencies that get the best results from SMS are the ones that treat message design with the same rigor as compliance.

The consumer should know within the first line who is contacting them and why. Ambiguity reduces response rates and increases complaints. Identify your agency and state the purpose of the message immediately. Do not make the consumer work to understand what they are receiving.

Messages that feel threatening or aggressive reduce consumer cooperation and increase opt-outs and complaints. A professional, matter-of-fact tone that presents options rather than ultimatums produces better results. This is also a compliance requirement under the FDCPA, which prohibits harassing, oppressive, or abusive conduct regardless of the communication channel.

Every message should tell the consumer exactly what to do: click a link, reply with a keyword, call a number, or visit a portal. Remove guesswork. The shorter the path from message to action, the higher your conversion rate. A consumer who reads a text but cannot figure out what to do next is a missed recovery opportunity.

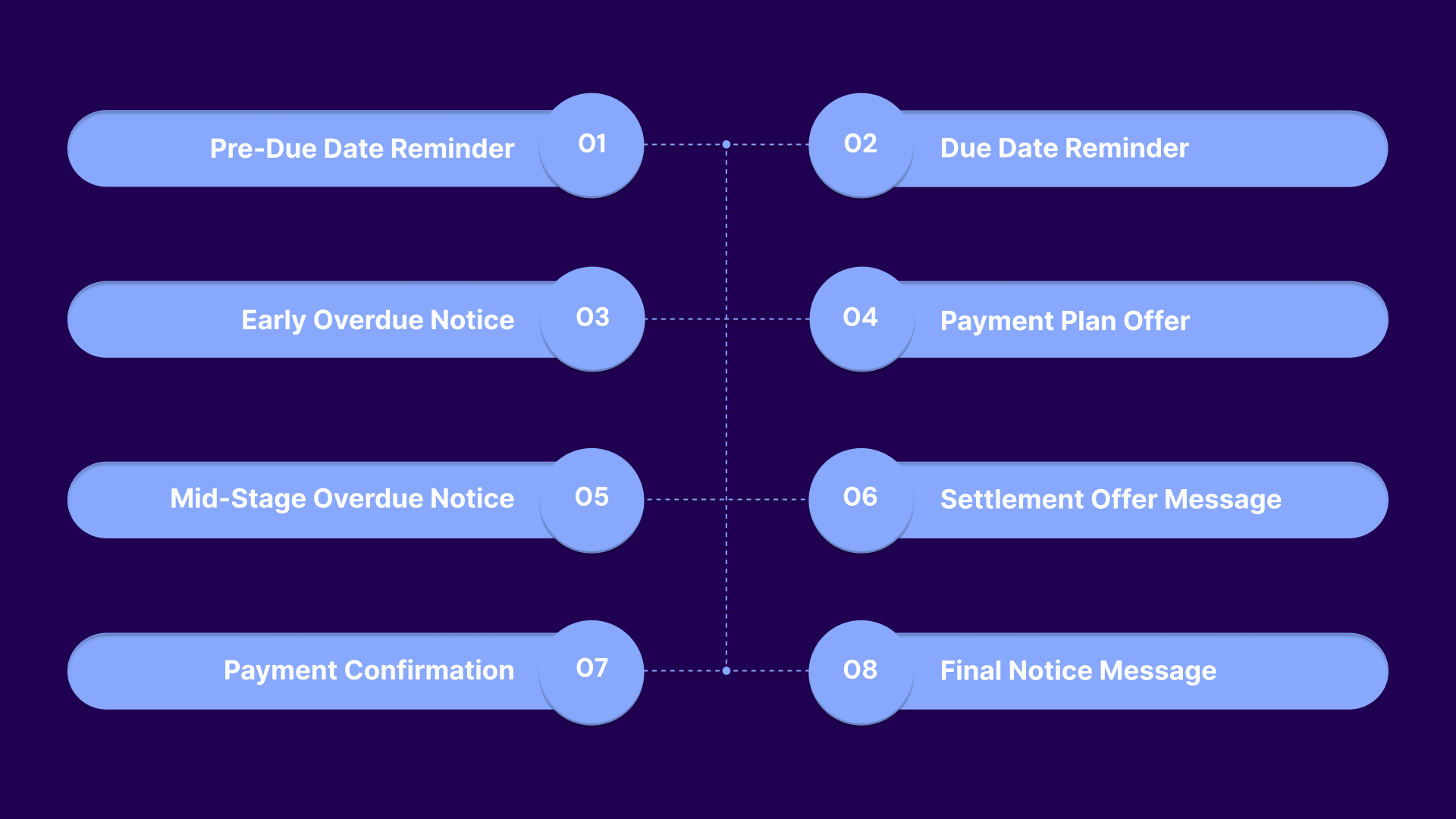

The templates below are organized by account stage and use case. Each one includes the message itself, the right timing for sending, and what to watch operationally so the data from each touchpoint informs the next one.

Have your legal team review all templates before deployment and adjust them for your portfolio-specific rules, client requirements, and applicable state laws. Keep messages under 160 characters where possible to avoid carrier splitting. Use a consistent sender ID so consumers recognize who is reaching out.

This message is your lowest-cost recovery tool. Reaching the consumer before the account goes past due keeps your costs lower and avoids the escalation cycle entirely.

Template: Hi [Name], this is [Agency Name], a debt collector, regarding your account with [Creditor Name]. A payment of $[Amount] is due on [Date]. View your options and pay securely here: [Link]. Reply STOP to opt out.

When to send: 3 to 5 days before the due date, triggered automatically from your account due date data.

What to watch for: If a consumer clicks the link but does not complete payment, trigger a follow-up within 24 to 48 hours. That behavior signals intent. Act on it before the due date passes.

Some consumers need a final prompt on the day itself. This message is short and action-focused. Keep it that way.

Template: Hi [Name], [Agency Name] here. Your payment of $[Amount] is due today. Pay now: [Link]. Need help? Call [Phone]. Reply STOP to opt out.

When to send: Mid-morning on the due date, between 9 a.m. and 11 a.m. in the consumer's local time zone. This window typically yields higher response rates than early-morning sends.

What to watch for: If you are already sending a pre-due reminder and seeing strong payment rates, test whether a single reminder outperforms the two-message sequence for certain consumer segments. More is not always better.

The account just crossed into overdue territory. Your tone should still be professional and solution-oriented. The goal is to re-engage, not escalate.

Template: Hi [Name], [Agency Name] is contacting you about a balance of $[Amount] that is now past due. View your payment options here: [Link]. Call [Phone] with questions. Reply STOP to opt out.

When to send: 3 to 5 days after the due date passes. Sending immediately on day one, even if overdue, can feel aggressive and generate more complaints than responses.

What to watch for: A consumer who opens the link but does not pay within 48 hours is a strong candidate for a payment plan message. Segment these accounts separately for the next touchpoint rather than sending another full-balance reminder.

By this point, a consumer who has not responded to full-balance reminders may need a different path. Payment plans recover accounts that would otherwise age into write-off territory. Make the offer easy to accept without calling in.

Template: Hi [Name], [Agency Name] can help you manage your balance of $[Amount] with a flexible payment plan. Set up your plan in minutes: [Link]. No call required. Reply STOP to opt out.

When to send: After two failed full-balance reminder touchpoints. The sooner you make this offer, the better. Plans accepted at 10 to 20 days past due have higher completion rates than those accepted at 45 days or later.

What to watch for: Track plan acceptance rate by account age. Use that data to time your plan offers earlier in the cycle for portfolios with consistently low full-balance recovery rates.

The tone shifts here. You acknowledge the pattern of non-payment without crossing into threatening language. You are still presenting options, but the message makes clear that time matters.

Template: Hi [Name], [Agency Name] is following up on your overdue balance of $[Amount]. We have payment options available. View them here: [Link] or call [Phone] to speak with someone. Reply STOP to opt out.

When to send: 15 to 30 days past due, after earlier touchpoints have produced no response. Space messages at least 5 to 7 days apart to avoid harassment claims.

What to watch for: If this message is generating inbound calls, but those calls are not converting to payment, the portal link destination may be the problem. Make sure the consumer lands on a payment page, not a login screen or a generic homepage.

For accounts where full balance recovery is unlikely, a time-limited settlement offer gives the consumer a specific reason to act now. The expiration date creates urgency without threatening language.

Template: Hi [Name], [Agency Name] has a settlement offer for your account. You may qualify to resolve your balance of $[Amount] for less. View your offer: [Link]. Offer expires [Date]. Reply STOP to opt out.

When to send: 30 to 60 days past due, or for accounts that have not responded to full-balance outreach. Use a specific expiration date.

What to watch for: Track settlement acceptance rate by offer percentage and balance tier. If your 60% settlement offers are converting at a meaningfully higher rate than 50% offers for a specific account segment, adjust your thresholds for that segment.

This message is often overlooked, but it does real operational work. Confirming receipt of payment reduces inbound calls asking whether the payment went through and clearly and professionally closes the loop for the consumer.

Template: Hi [Name], [Agency Name] has received your payment of $[Amount] on [Date]. Thank you. For records or questions, call [Phone] or visit [Link]. Reply STOP to opt out.

When to send: Automated trigger within minutes of payment confirmation in your system. Delay in confirmation messages increases inbound inquiry volume.

What to watch for: High inbound call volume after payment confirmation often indicates the consumer has questions about credit reporting updates. If this is a consistent pattern, add a line to your confirmation message that addresses it directly.

This is your last SMS touchpoint before account escalation. The message signals seriousness without making threats. Send it once per account.

Template: Hi [Name], this is a final notice from [Agency Name] regarding your balance of $[Amount]. Please make a payment or contact us by [Date]: [Link]. Call [Phone] for assistance. Reply STOP to opt out.

When to send: 45 to 90 days past due, as the last SMS touchpoint before escalation. Do not send this message more than once per account.

What to watch for: Track how many accounts respond to this message after ignoring earlier touchpoints. A meaningful response rate here suggests your earlier messages may have been too frequent or too similar. If that is the pattern, test spacing out your earlier sequence before assuming the account is unworkable.

Suggested Read: Structuring Text Messages That Debtors Read, Understand, and Act On

These are the five metrics that give your operations team real visibility into SMS performance, and how to track each one in practice.

Suggested Read: 5 Debt Settlement Letter Templates for Faster Negotiations

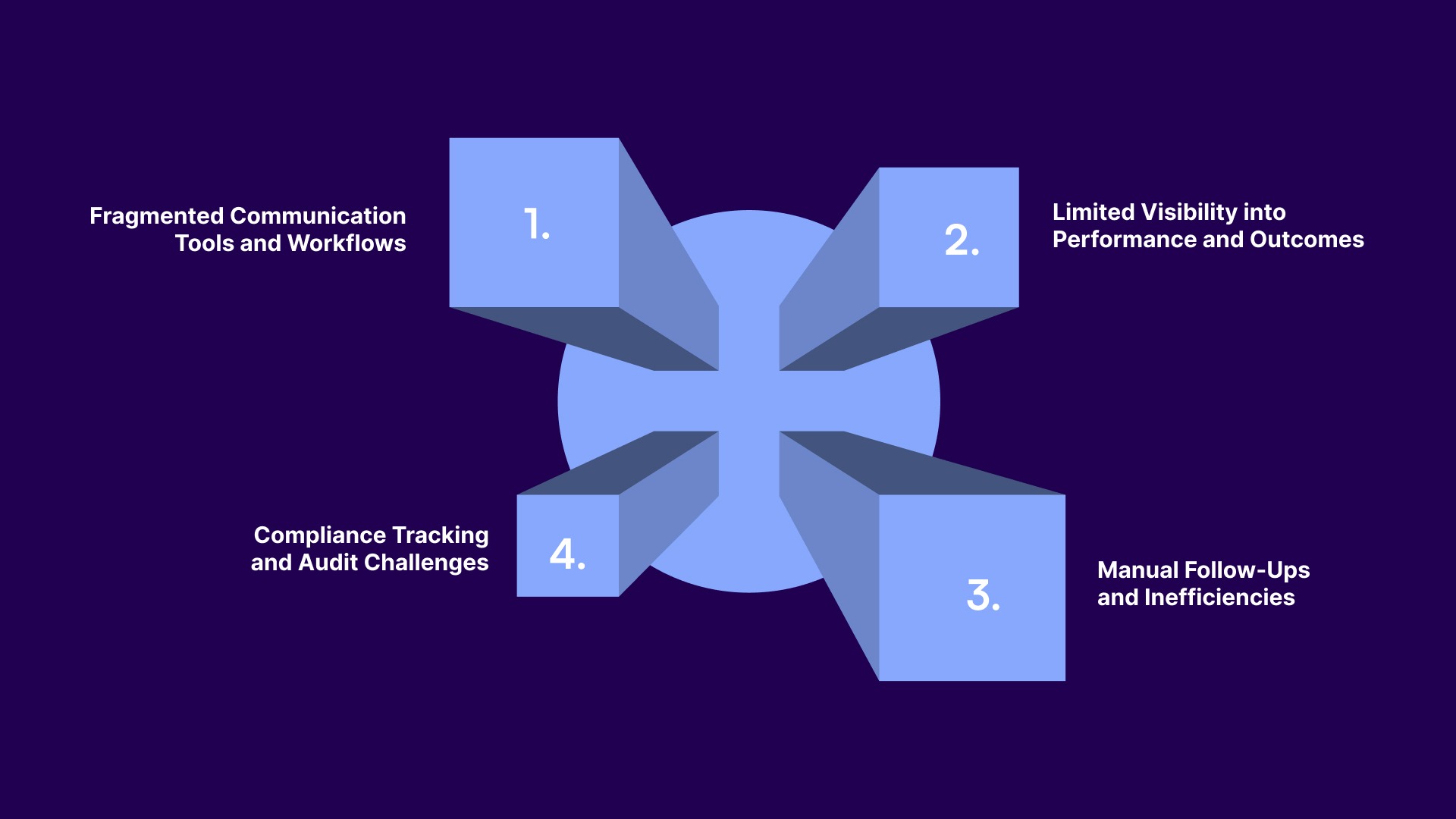

Most collection agencies face the same set of operational challenges when running SMS programs at scale. These are not edge cases; they reflect how most collection operations are currently structured.

Many agencies manage SMS through a separate messaging platform that does not connect to their payment system or collection management software. The result: agents work across multiple systems, account status is not always current, and follow-ups are sometimes inconsistent or duplicated.

Without centralized reporting, it is difficult to know which campaigns are generating payments, which message templates are underperforming, or how SMS compares to other outreach channels in terms of recovery per account.

When SMS responses come in, a consumer replying "YES" to a payment plan offer, for example, often requires manual agent action to progress. Without automation to handle responses and trigger the next step, accounts stall, and workload increases.

Regulators can request documentation of every consumer communication, including texts. Agencies that manage consent records and message histories in manual logs or disconnected systems face significant audit preparation challenges. A missed opt-out or an undocumented consent record creates real exposure.

Tratta centralizes payments, SMS outreach, and reporting in one platform, so your teams can run consistent, documented campaigns without the coordination cost of disconnected tools.

Building an SMS program that performs at scale requires more than selecting a messaging tool. It requires a structured approach to automation, integration, and workflow governance. Here is how to build the foundation correctly.

Before you deploy, define when each message type is sent and what triggers its send. A well-structured automation setup should include at a minimum:

For example, if a consumer clicks a payment link but does not complete payment within 24 hours, a behavior-based trigger can automatically send a follow-up SMS offering a payment plan. No agent involvement required. The account moves forward on its own.

Triggers remove the need for agents to manually initiate outreach and ensure every account receives consistent treatment regardless of workload.

The most effective SMS programs connect directly to your payment infrastructure. A consumer who receives a text should be able to access a self-service portal, view their balance, and pay in one flow. This requires the SMS platform to be integrated with your payment system, not operating as a separate tool with a separate login path.

Every message sent, every opt-out received, every consent record, and every payment conversion should be visible in one reporting layer. This is the foundation for audit readiness and campaign optimization. If you cannot pull a complete SMS history for a given account in seconds, your reporting infrastructure is a gap that will cost you during an audit.

Standardized message templates, system-enforced compliance rules, and documented workflows ensure that your SMS outreach is consistent regardless of which agent or campaign manager is involved. Consistency is what allows an SMS program to scale without increasing compliance risk in proportion.

Tratta is debt collection software built for agencies, law firms, and debt buyers. It replaces disconnected legacy tools with one platform for payments, digital communications, reporting, and compliance-aware recovery workflows.

Here are the features that Tratta directly addresses to mitigate operational and compliance challenges that limit SMS performance at scale.

Tratta Campaigns allow you to automate SMS and email outreach while maintaining full compliance.

You can:

Required FDCPA disclosures are applied automatically. Timing restrictions are enforced at the system level, and cease-communication requests immediately stop all outreach.

Tratta gives consumers secure, 24/7 access to resolve balances on their own terms, reducing agent workload and accelerating payment.

Consumers can:

All payment data is encrypted and tokenized. The platform maintains PCI DSS Level 1 and SOC 2 Type II certifications to protect sensitive information.

Tratta provides real-time visibility into how your SMS campaigns are performing across portfolios and workflows.

Dashboards track:

All metrics update as accounts move through campaigns and payment flows, so your operations team always has current data without manually building reports.

Tratta integrates with your existing systems without requiring a full technology overhaul.

Integration options include:

This means you can keep your current collection management system and add Tratta's SMS, payment, and reporting capabilities on top. Typical implementation takes 30 days, including configuration and training.

SMS can improve recovery performance, but only when it is managed as part of a controlled workflow. Without clear consent tracking, structured messaging, and system-level visibility, it introduces risk alongside scale.

For collection agencies, the focus should be on integrating outreach, payments, and reporting into a single workflow. This reduces manual effort, improves consistency, and makes performance measurable.

Tratta supports SMS-driven recovery by centralizing communications, payments, and reporting on a single platform.

Schedule a demo to see how Tratta supports compliant, scalable SMS workflows.

Track payment conversion, cost per dollar recovered, and recovery per account. Connect SMS activity to payment data to attribute revenue accurately across campaigns.

Segment by balance size, age, and consumer behavior. Higher balances may need negotiation paths, while early-stage accounts respond better to reminders and self-service links.

Use a structured cadence where SMS complements calls and email. Avoid overlap by sequencing outreach based on account stage and prior consumer engagement.

Typically shared between operations, compliance, and payments teams. Operations manages workflows, compliance oversees controls, and payments ensure conversion tracking and user experience.

Implement system-level controls for consent, timing, and opt-outs. Standardize templates and automate workflows to reduce manual errors as volume increases.