Modernizing a collection agency is an operating decision. Can your team identify the right account, contact the consumer through an approved channel, offer a clear payment path, and report on the outcome without rebuilding the record across separate systems?

That question matters more in 2026 because agencies are handling more accounts while being pushed to improve productivity, margins, and compliance controls. TransUnion reported that 52% of debt collection companies saw increased or significantly increased account volume over the prior 12 months, which makes fragmented workflows harder to defend.

For agency owners, COOs, and operations leaders, collection agency modernization means connecting payments, outreach, reporting, and compliance records so recoverable accounts keep moving through the process.

Agencies are facing operational pressure from several directions. They are dealing with higher account volume, broader digital channel use, and more demand for clear records across every consumer interaction.

More accounts create more opportunity when routing stays clean. They create more delay when assignment, outreach timing, payment updates, and reporting depend on separate systems.

TransUnion reported that higher account volume has been paired with lower collectability, a trend the report says has been underway since 2020. For collection agencies, that puts more weight on account prioritization. A larger queue needs cleaner data, fewer handoffs, and faster visibility into which accounts are ready for action.

Workable accounts can remain untouched longer than they should when teams lack that level of control.

Phone and letters still matter in collections. They remain widely used and often carry regulatory or documentation value. Digital payment access has also become a major recovery channel.

TransUnion found that self-service portal adoption among debt collection companies rose from 79% to 88% in 2024. It also reported that a quarter of companies collect more than 40% of their payments through the online portal channel.

That changes the role of the payment portal. It has to connect with outreach, payment plans, balance updates, and reporting. When the portal sits outside the rest of the operation, payment intent can still turn into friction.

Debt collection remains a high-visibility consumer issue. The CFPB received about 207,800 debt collection complaints in 2024, equal to 7% of all complaints it received that year.

A payment and outreach upgrade needs matching record controls. Calls, texts, emails, portals, payment plans, disputes, and opt-outs all create activity that your team may need to review later.

Regulation F includes telephone call frequency presumptions under 12 CFR § 1006.14. It also requires a clear and simple opt-out method for covered electronic communications under 12 CFR § 1006.6(e), and record retention under 12 CFR § 1006.100.

Also read Key Rules for Collection Agencies in 2026

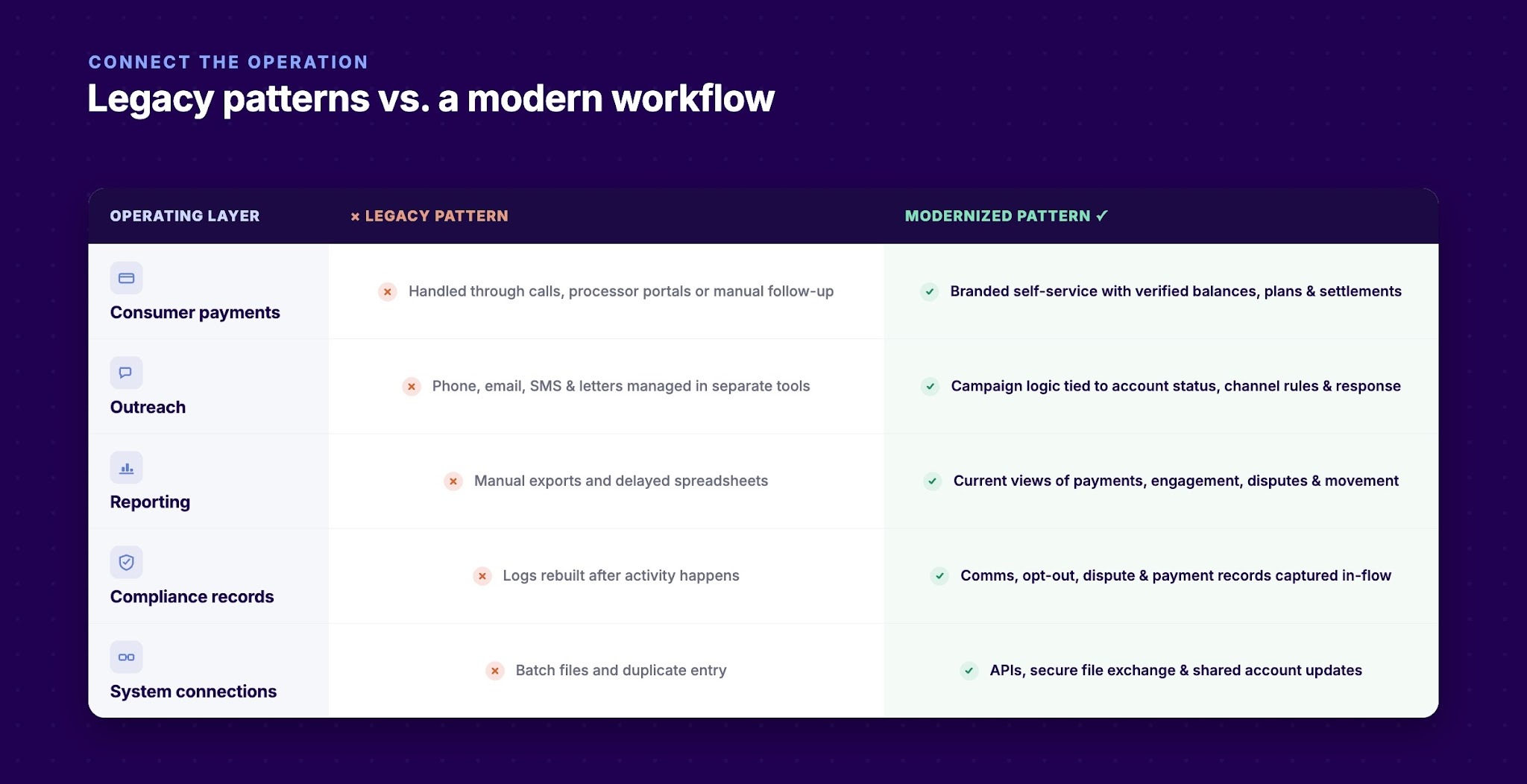

Collection agency modernization is the shift from disconnected tools to a connected recovery workflow. A practical project keeps systems that still work and fixes the data gaps between payments, outreach, reporting, and compliance records.

The proof appears in daily work. Agents see clearer account status. Managers review current activity. Payment teams reconcile with fewer manual corrections. Compliance reviewers have cleaner records to examine.

The strategic value is control. Your team can see where agents should spend time, which consumers should receive digital follow-up, which payment paths are working, and where accounts are slowing down.

Also read Breaking Down the Payment Portal Definition for Collection Agencies in 2026

Legacy systems rarely fail all at once. They create small delays that repeat across thousands of accounts. Those delays become cost, risk, and missed recovery.

In a fragmented setup, agents check multiple screens before they can act. One system may show a payment plan. Another may show the latest call attempt. A third may hold the payment status.

That creates avoidable work. It also changes the consumer conversation. The agent has to confirm information that should already be clear. If the record is incomplete, the next outreach step can be wrong.

Agent capacity then gets consumed by the setup itself. The agency may add staff, extend shifts, or create manual review queues while the workflow keeps demanding extra system work behind each account.

A delayed report limits what an operations leader can change. If campaign performance, portal activity, and payment outcomes are reviewed after the fact, the team is managing yesterday’s portfolio.

That lag matters in collection operations. A campaign with weak click-to-payment performance may need a different payment link, channel mix, or segment rule. A payment plan cohort with rising breakage may need earlier follow-up. A portfolio with low right-party contact may need a channel review.

Late signals give the agency less time to adjust while accounts are still active.

Disconnected systems often break at the handoff points. A consumer makes a payment, but the dialer has not updated. A dispute is logged, but the campaign list still includes the account. A payment plan is active, but the next message does not reflect it.

Those errors damage trust. They also create more inbound calls, more manual review, and more compliance-sensitive cleanup.

A modernized workflow should carry account status, payment activity, dispute state, and outreach history into the next step.

Also read The Debt Collector's Guide to Advanced Reporting for Recovery

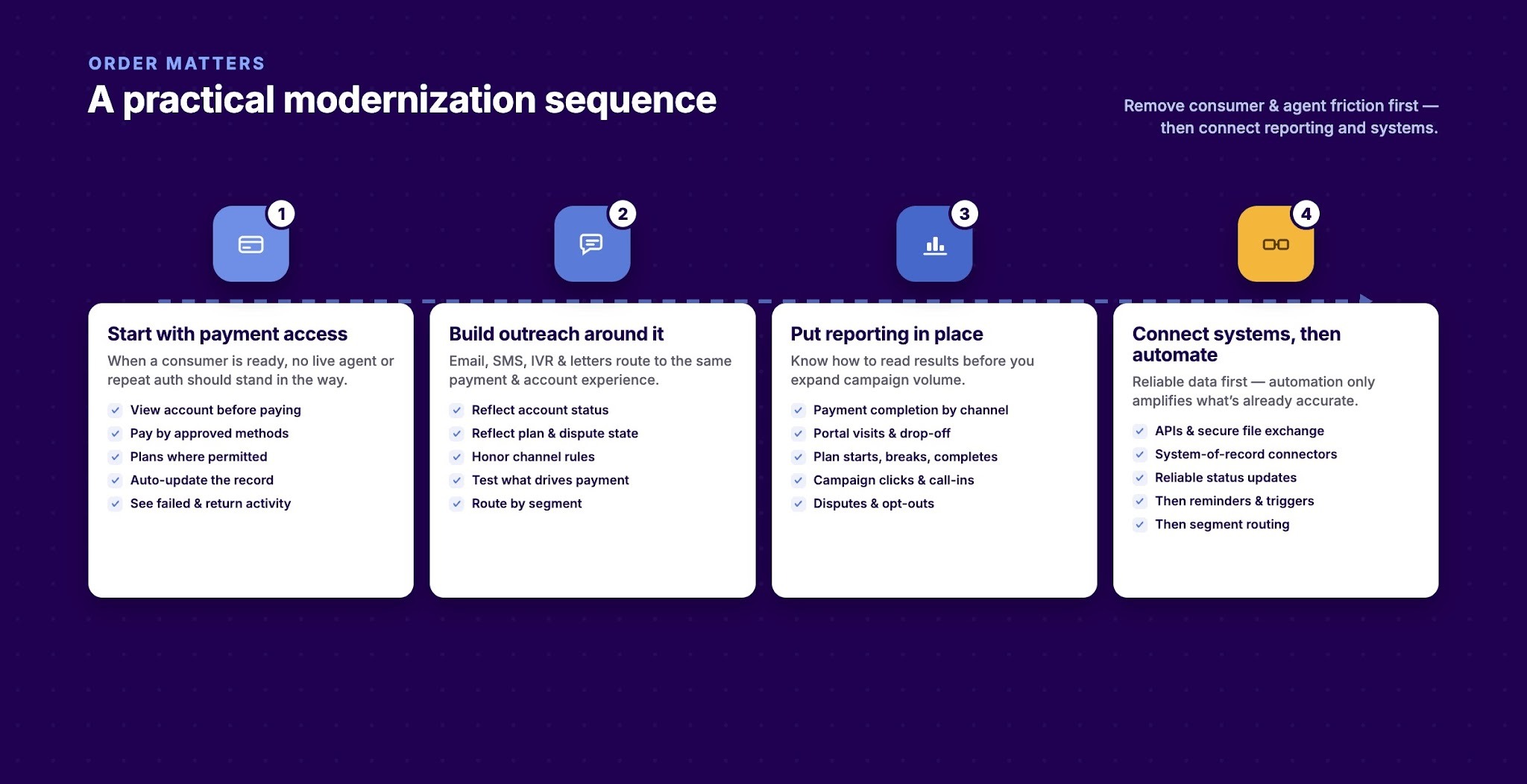

The order matters. Agencies get stronger results when they improve the areas that remove consumer and agent friction first, then connect reporting and system updates around those changes.

The first gap to close is often the payment experience. When a consumer is ready to pay, the process should support that action without requiring a live agent, repeated authentication, or a separate follow-up call.

A strong payment experience gives consumers a clear path to act. That includes balance visibility, payment options, plan setup, settlement offers where approved, and confirmation after payment.

Before you move forward, check whether the payment path covers these needs.

Payment access is often the most direct place to reduce friction because it connects to the consumer’s next action.

Outreach should do more than remind consumers that a balance exists. It should route them toward the next approved step.

Email, SMS, IVR, and letters should connect to the same payment and account experience. Campaigns should reflect account status, payment plan state, dispute state, and channel rules.

This gives your team a cleaner way to test outreach. You can see which messages drive portal visits, which links lead to payments, and which segments need agent attention.

More outreach without better reporting can create confusion. Before your agency expands campaign volume, it should know how to read the results.

Your reporting layer should show the metrics that affect daily decisions.

These numbers help leaders decide what to adjust. They also help managers separate activity from performance.

Automation works only when the underlying data is reliable. If balances, disputes, payment plans, and contact permissions live in separate systems, automated workflows can repeat the wrong action faster.

System connections should come before complex automation. APIs, secure file exchange, and reliable status updates help your agency preserve existing systems while adding better payment, outreach, and reporting capabilities.

Once the account record is current, your team can use automation for reminders, payment plan follow-up, segment routing, and campaign triggers with more control.

Also read Using Risk Scoring to Prioritize Debt Recovery

A modernization project should be judged by operating fit. A tool can look strong in a demo and still fail if it does not match how your agency handles portfolios, clients, consumers, payments, and compliance review.

Use the questions below to separate useful capability from surface-level features.

The best fit is the platform that improves the work your agency already performs. It should reduce manual gaps, make consumer payment easier, and give leaders a clearer view of what is happening across the portfolio.

Tratta is debt collection software for recovery teams that need payments, digital communications, reporting, integrations, and compliance-aware workflow control in one platform. For collection agencies, that fit matters because a modernization project can fail when the new tool becomes another disconnected point solution.

Tratta’s collection agency software supports consumer-facing payment access, administrative control, account visibility, and connected recovery workflows.

For collection agency teams, the platform includes the following capabilities.

The Consumer Self-Service Platform gives consumers a branded place to view balances, make payments, set up payment plans, upload documents, and manage account actions. This supports the payment-first part of modernization because consumers can act without waiting for an agent.

Embedded Payments supports debit card, ACH, Check21, payment plans, allocation tools, returned payment handling, and reconciliation visibility. This helps payment operations keep transaction activity close to the account record.

Omnichannel Communications supports email, SMS, chat, phone, bilingual IVR, and QR-code letters. Tratta Campaigns supports email and SMS campaigns, event-driven triggers, performance tracking, and reports tied to clicks, call-ins, and payments.

Reporting and Analytics gives teams visibility into payment trends, settlement offer engagement, portal activity, communication performance, failed payments, chargebacks, and audit history. This helps operations leaders review performance without rebuilding reports from disconnected exports.

REST APIs and integrations help agencies connect Tratta with established systems through APIs, secure file exchange, system-of-record connectors, payment plan events, and portal access links. This supports modernization without forcing a full system replacement.

Tratta’s security and compliance tools are designed to support controlled, documented workflows in a compliance-sensitive environment. Tratta does not provide legal counsel or guarantee compliance outcomes. Your legal team remains responsible for interpreting and applying legal obligations.

A collection agency can absorb more accounts for a while by adding agents, running more campaigns, or creating more manual review queues. That approach breaks down when the workflow itself cannot keep account status, payment activity, outreach history, and compliance records moving together.

Modernization gives agency leaders a cleaner way to manage growth. Agents spend less time rebuilding context. Consumers get a clearer path to payment. Managers can see where accounts are slowing down before the issue spreads across the portfolio.

If your agency is ready to modernize without replacing every working system, schedule a demo with Tratta to see how the platform supports connected recovery operations.

Collection agency modernization means connecting consumer payments, outreach, reporting, system updates, and compliance records into a cleaner recovery workflow. The goal is to reduce manual gaps that slow agents, confuse consumers, or hide performance issues.

Most agencies should start with consumer payment access. A branded self-service portal can reduce friction at the point where the consumer is ready to act. Once payment access is clear, outreach, reporting, and system connections become easier to improve.

Many agencies keep their system of record and add modern payment, communication, reporting, and connection layers around it. The key requirement is reliable data flow between systems.

Regulation F affects how covered debt collectors manage communication frequency, electronic opt-outs, documentation, and records. A modern workflow should help capture those activities in the normal course of work. This does not replace legal review or compliance oversight.

Useful metrics include payment completion rate, self-service payment share, portal drop-off rate, campaign response, account coverage, payment plan breakage, agent activity tied to outcomes, dispute volume, opt-out activity, and reporting lag.