Outstanding accounts receivable can quietly disrupt collection agency performance. As assigned accounts remain unresolved, recovery slows, cash flow becomes less predictable, and operational costs increase.

Recent industry trends highlight the challenge, with collections revenue declining at a 6.30% CAGR over the past five years, reaching an estimated $13.60 billion. Factors such as payment pauses and shifting consumer behavior have extended recovery timelines, leaving agencies managing larger volumes of unresolved accounts across their portfolios.

If accounts are taking longer to resolve and recovery outcomes feel less consistent, you are not alone. Many agencies are facing the same pressure as traditional collection workflows struggle to keep up. In this article, we explore practical strategies to reduce outstanding accounts, improve recovery efficiency, and regain control over your collections process.

Outstanding accounts receivable refers to the total value of debts that have been assigned to a collection agency but remain unpaid. These accounts may be newly placed, partially resolved, or significantly overdue, depending on their position in the collection lifecycle.

Characteristics of outstanding AR in collection:

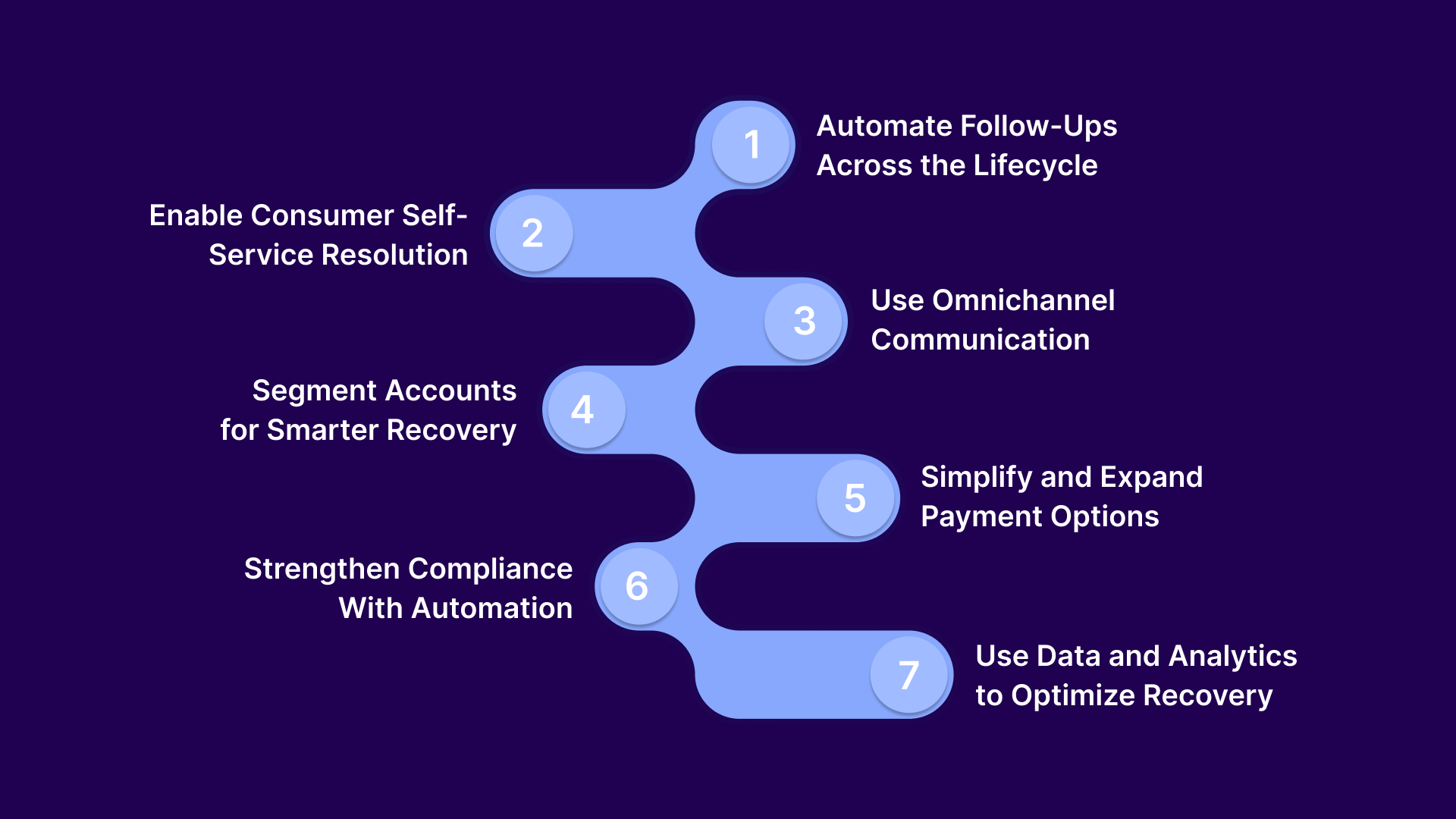

Learning about what makes up outstanding accounts receivable is only the starting point. The real challenge lies in reducing it efficiently and consistently. The next section lists 7 proven strategies to do that.

Suggested Read: Accounts Receivable Automation vs Manual Processes Explained

When processes are aligned with consumer behavior and supported by the right systems, agencies can recover faster without increasing operational strain.

These strategies can help you reduce your agency’s accounts receivable:

Manual follow-ups often lead to missed accounts and inconsistent communication. Automation ensures every account receives timely and relevant outreach throughout the collection lifecycle.

Key ways automation improves consistency and coverage include:

Consumers are more likely to resolve accounts when they can act on their own time. Self-service options remove friction and reduce dependency on collection agents.

Ways self-service simplifies and speeds up resolution include:

Relying on a single channel limits reach and response rates. Omnichannel strategies ensure you meet consumers where they are most responsive.

Effective omnichannel engagement involves:

Not all accounts require the same approach. Segmentation helps prioritize high-value and high-probability accounts for faster recovery.

Common ways to segment accounts effectively include:

Complex payment processes delay resolution and reduce completion rates. Simpler options make it easier for consumers to complete payments and resolve accounts faster.

Key payment improvements that reduce friction include:

Compliance requirements can slow down outreach if managed manually. Automated controls ensure every interaction stays within regulatory boundaries.

Core compliance practices supported by automation include:

Without clear insights, it is difficult to improve performance. Data-driven strategies help identify what works and where adjustments are needed.

Key areas where analytics improves recovery include:

Improving collections is not about adding more tools. It is about connecting workflows, communication, and payments into a single, efficient system.

Tratta brings automation, consumer self-service, and compliance together to help agencies reduce manual effort while improving recovery rates. It enables faster resolution of outstanding accounts receivable without increasing operational complexity. Schedule a free demo.

Outstanding accounts do not increase overnight for collection agencies. They build gradually as operational gaps, delayed follow-ups, and limited consumer engagement compound over time.

These factors can increase unresolved accounts:

To effectively reduce outstanding accounts, agencies also need to measure what is working and where delays are occurring. This is explained in the next section.

Suggested Read: Top 10 Accounts Receivable Automation Software Solutions

Consistent tracking allows agencies to pinpoint bottlenecks and make data-driven decisions that accelerate collections. Without the right metrics, it becomes difficult to identify delays, optimize strategies, or improve recovery outcomes.

Table showing key metrics that agencies should track:

Tracking these metrics individually is important, but real improvement comes from connecting them across the entire collection lifecycle.

Tratta offers reporting and analytics to give agencies clear visibility into key performance metrics. Teams can identify delays and refine their strategies. By combining these insights with automated workflows and integrated payment options, agencies can act more quickly to improve recovery outcomes. Call us to learn more.

By strengthening processes early in the collection lifecycle and maintaining consistency throughout, agencies can reduce risk, improve recovery timelines, and stabilize cash flow.

These are a few other tips to manage accounts receivable risks:

Applying these best practices creates a more stable and predictable collections process. However, executing them consistently at scale requires more than manual effort. This is where the right technology becomes essential.

Suggested Read: 5 Accounts Receivable Automation Best Practices Guide

Tratta is a consumer-first debt collection platform designed to help agencies optimize operations, improve engagement, and accelerate recovery. It brings together communication, payments, automation, and compliance into one connected system.

This allows agencies to manage assigned accounts more efficiently while reducing delays across the collection lifecycle

Features that help improve debt collection processes:

Gives consumers 24/7 access to their accounts, balances, and payment options. By enabling independent resolution, it reduces inbound volume and shortens time to payment.

Handles secure payment processing across channels with built-in merchant capabilities. This ensures faster transactions, better reconciliation, and fewer payment failures.

Allows consumers to make payments through an automated voice system in multiple languages. This improves accessibility and captures payments outside agent hours.

Centralizes SMS, email, and voice outreach in a single system. This ensures consistent messaging while increasing the chances of reaching consumers on their preferred channel.

Automates outreach through rule-based campaigns triggered by account activity and behavior. This keeps accounts active and reduces gaps in follow-up.

Provides visibility into recovery performance, channel effectiveness, and account behavior. These insights help agencies identify delays and refine strategies quickly.

Allows agencies to configure workflows, communication logic, and payment experiences. This ensures the platform aligns with specific operational and compliance requirements.

Connects with CRMs, core systems, and third-party tools through APIs. This eliminates data silos and keeps information synchronized across systems.

Embeds compliance controls into every interaction, including consent tracking and audit trails. This reduces regulatory risk while maintaining operational speed.

Equips agents with tools to manage interactions, track account activity, and support consumers effectively. This improves agent productivity while ensuring consistent and compliant communication.

Tratta does not just digitize collections. It restructures how recovery workflows operate across the entire lifecycle. The result is faster resolution, better consumer engagement, and more predictable recovery outcomes.

Outstanding accounts can quickly become unmanageable when follow-ups are inconsistent, engagement is limited, and payment processes create friction. As delays compound, recovery rates decline, operational costs rise, and agencies are left working harder for diminishing returns.

Tratta helps address these challenges by bringing together communication, payments, automation, and compliance into a single platform. With features like omnichannel outreach, self-service payments, and workflow automation, it enables agencies to reduce delays, improve engagement, and resolve accounts more efficiently.

Modernize your collections strategy to take control of outstanding accounts. Schedule a call today.

Total outstanding receivables are calculated by summing all unpaid assigned account balances at a given time. This includes current, overdue, and partially paid accounts across the entire receivables portfolio.

Outstanding receivables increase due to delayed follow-ups, poor segmentation, limited communication channels, payment friction, and inefficient workflows that slow down resolution and extend collection timelines.

Agencies can reduce receivables by automating follow-ups, enabling self-service payments, using omnichannel communication, and prioritizing high-value accounts based on data-driven segmentation strategies.

Key metrics include liquidation rate, roll rate, Right Party Contact (RPC) rate, Promise-to-Pay (PTP) rate, and time-to-resolution. These help measure recovery speed, efficiency, and overall collection performance.

Liquidation rate measures the percentage of total assigned debt that has been successfully collected over a given period. It helps agencies evaluate how effectively they are converting placed accounts into recovered revenue.