A missed follow-up may seem small at first. One account ages a little longer. A payment comes in late. But across collections teams, these small gaps add up quickly. In fact, 94% of U.S. businesses still rely on manual processing to handle payments, forcing teams to spend hours on repetitive work just to keep cash flow flowing.

For debt collection agencies and creditors, this is costly. Manual accounts receivable work depends on people remembering what to do next, finding time to do it, and applying the same standards every time. That breaks down quickly as account volumes grow and compliance demands increase.

That’s why more agencies are weighing accounts receivable automation vs traditional manual processes. The value isn’t just in speed. It’s in consistency, visibility, and control over how every account is handled from first follow-up to final payment.

This article breaks down where manual accounts receivable processes fail, what automation actually looks like in a real collections environment, and when it makes sense to move away from manual systems.

Accounts receivable are the money owed to a business for goods or services already provided. In debt collection, it refers to past-due balances that must be recovered in a controlled and compliant manner.

For collection agencies and creditors, accounts receivable management is not just about tracking balances. It includes when follow-ups happen, how payments are collected, how payment plans are monitored, and how every action is documented for compliance.

Each step affects recovery speed and cost. When follow-ups are late or payments are hard to complete, accounts sit longer, balances age, and recovery rates drop. When execution is consistent, agencies collect faster and reduce operational strain. This is why the way accounts receivable is managed matters.

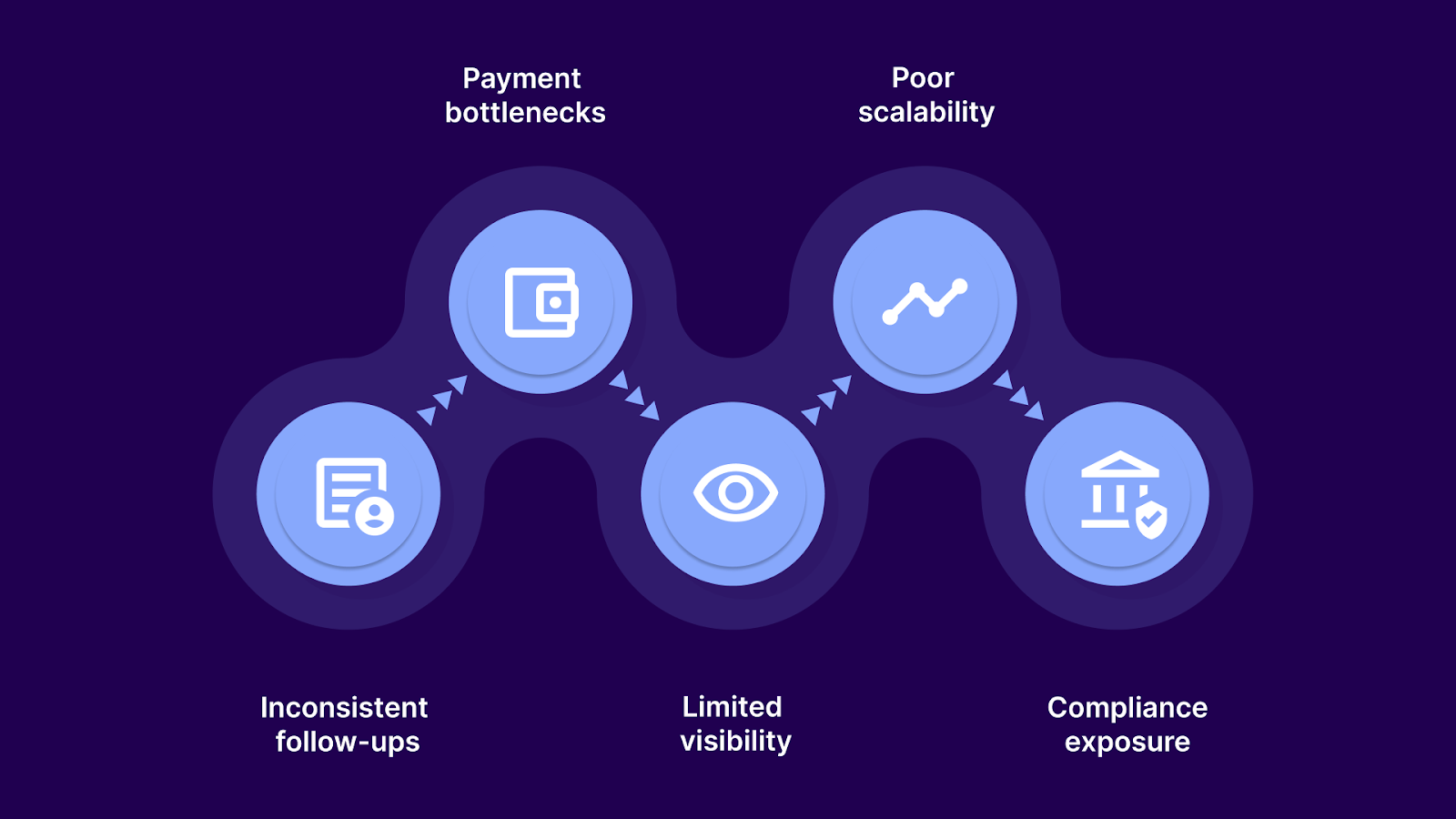

Manual accounts receivable processes rely on people to track accounts, remember follow-ups, and update records by hand. That approach can work at a small scale, but it struggles as portfolios grow and compliance demands increase.

The breakdown usually shows up in a few predictable areas:

A lack of effort doesn’t cause these issues. They come from processes that weren’t designed to handle today’s account volumes, consumer behavior, or regulatory pressure.

Accounts receivable automation uses software to automate routine collection tasks that are typically handled manually. Instead of relying on agents to track dates, send reminders, and post payments, the system performs these steps automatically based on predefined rules.

In a collection environment, automation usually covers:

The goal isn’t to replace collectors. It’s to remove repetitive work so teams can focus on accounts that need human attention.

Suggested Read: Top 10 Accounts Receivable Automation Software Solutions

Both manual and automated accounts receivable processes aim to recover past-due balances. The difference is in how consistently, quickly, and efficiently work gets done once account volume increases.

The table below shows how each approach handles core collection activities.

Manual processes keep your team reactive. Automation makes execution consistent.

For collection agencies, the comparison isn't theoretical. Agencies that use accounts receivable automation rather than traditional manual processes collect faster, handle larger portfolios with smaller teams, and maintain compliance controls that manual processes can't match.

Tratta provides the automation infrastructure collection agencies need to execute consistently across every account. Self-service payment portals, behavior-driven outreach, and real-time reporting work together to improve recovery rates without increasing headcount. Book a demo to see how it works. Schedule a demo today to experience it firsthand.

Suggested Read: Understanding Accounts Receivable: An Analysis and Calculator Guide

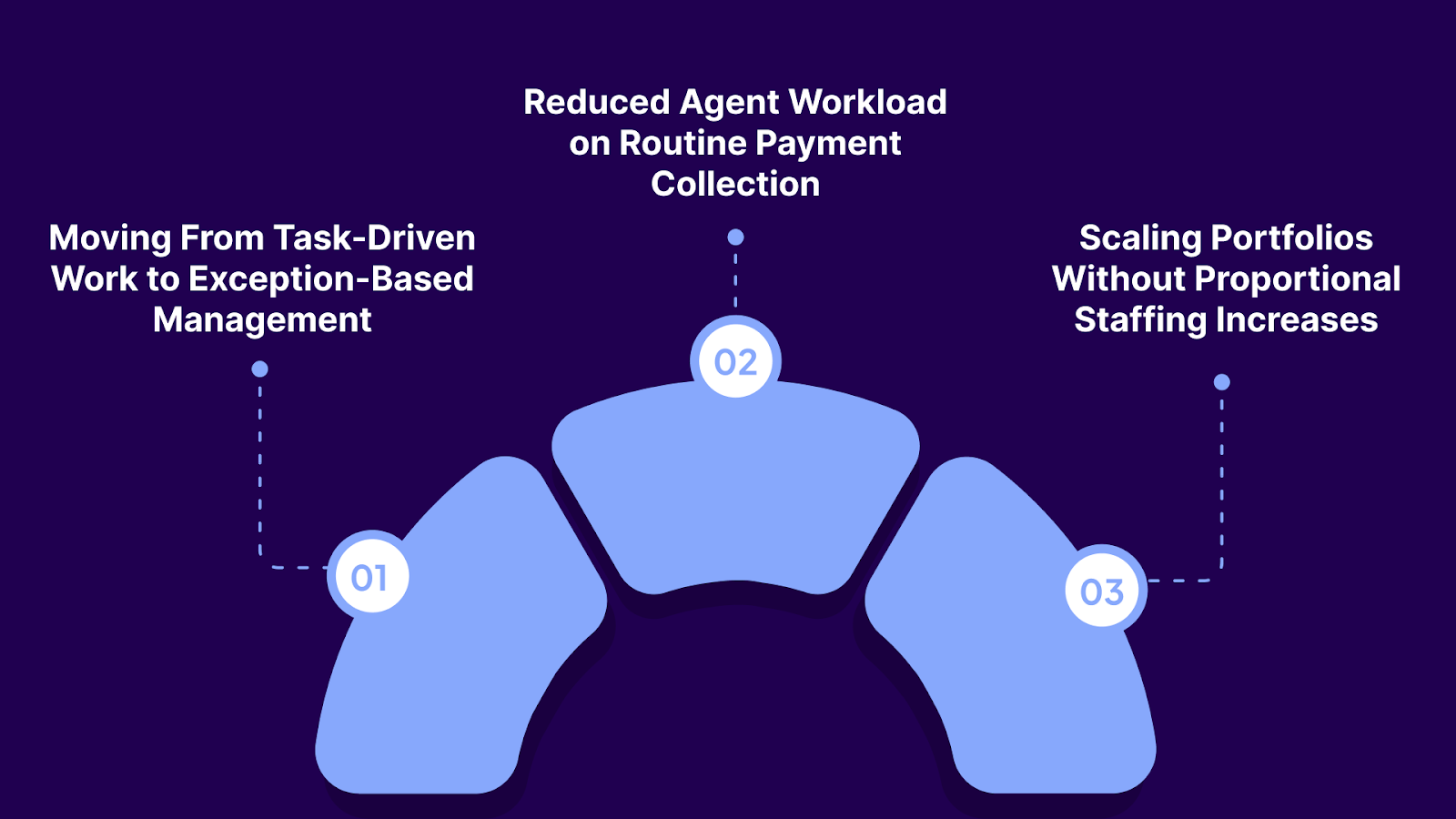

Automation changes how your team works, what they focus on, and how efficiently your agency operates. The difference shows up in three areas that affect daily workload, staffing needs, and recovery output.

Manual AR keeps your team in task mode. Agents spend their day sending reminders, processing payments, updating records, and following up on overdue accounts.

Automation handles routine tasks automatically. Your team shifts to exception-based management, where they focus on:

This shift improves both productivity and job satisfaction. Agents stop doing repetitive work and start solving problems that require human judgment.

Most payment collection doesn't require agent involvement. Consumers know what they owe, they can pay, and they just need a simple way to do so.

When consumers can pay on their own schedule without calling your agency:

As more consumers use self-service options, your agency can handle larger portfolios without increasing staff.

Manual processes create a linear relationship between portfolio size and headcount. When your portfolio grows by 50%, you need roughly 50% more agents to handle the volume.

Automation breaks that relationship:

This operational efficiency enables collection agencies to grow profitably.

Suggested Read: Best Practices for Improving Law Firms' Accounts Receivable Process

Not every agency needs to automate immediately. Small agencies with limited portfolios and predictable workloads can manage manually. But most agencies reach a point where manual processes become unsustainable.

Your agency should consider automation when you notice:

These signs indicate that manual processes are constraining growth and increasing risk.

Three factors accelerate the need for automation:

Volume: When your agency manages thousands of accounts simultaneously, manual tracking becomes impossible. Automation is the only way to execute consistently across every account.

Delinquency Stage: Accounts in later stages of delinquency require more frequent contact and tighter compliance controls. Manual processes can't maintain the frequency and documentation standards required for effective recovery and regulatory compliance.

Compliance Complexity: The FDCPA regulates communication timing, frequency, disclosure requirements, and prohibits unfair or deceptive practices. As regulatory scrutiny increases, manual compliance enforcement becomes risky. Automated controls enforce rules automatically and create audit trails that protect your agency.

Agencies that delay automation face increasing operational risk and declining competitiveness:

The longer you wait, the harder it becomes to catch up. Delaying also means continuing to expose your agency to compliance risk. Every manual interaction is an opportunity for error, and every error is a potential violation.

Tratta helps collection agencies quickly implement accounts receivable automation. The platform handles outreach, payment processing, and compliance controls, allowing agencies to scale operations without increasing costs in proportion. Book a free demo to explore the features for your agency.

Suggested Read: Top 10 KPI Metrics for Effective Tracking of Accounts Receivable

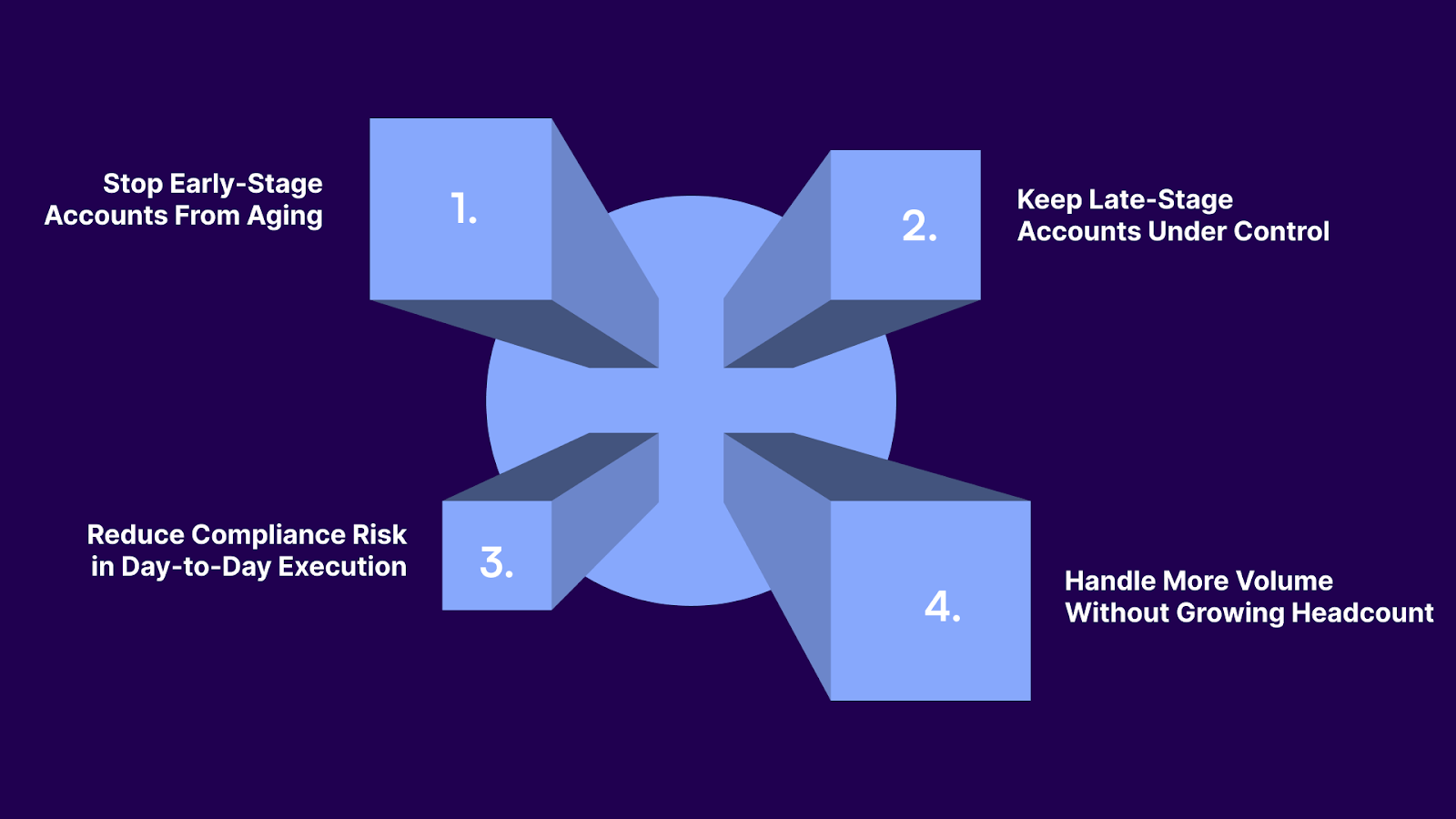

Accounts receivable automation is about eliminating delays and manual tracking from daily operations. When used correctly, it helps you keep accounts moving, control risk, and handle more volume without adding staff.

Here’s how you can apply automation across your collection operation.

When accounts first go past due, speed matters more than pressure. You can use automation to act immediately:

This reduces early aging and prevents accounts from rolling into later delinquency stages.

As accounts age, your focus shifts to return on effort. Automation helps you stay in control without losing visibility:

Nothing goes quiet, and agent time stays focused on accounts that matter most.

Compliance failures often come from small execution gaps. You can use automation to enforce rules consistently:

This lowers risk without adding more checks to your agents’ workload.

Manual processes scale through people. Automation scales through rules. You can use it to:

This keeps the cost per dollar collected under control as volume grows.

Using accounts receivable automation this way gives you more control over timing, workload, and compliance. You collect faster, spend less effort on routine work, and reduce the risks of manual execution.

Suggested Read: Main Benefits of Accounts Receivable Automation

Tratta is a technology platform built specifically for debt recovery. It combines automation, self-service access, and compliance controls into a single system that collection agencies, law firms, and creditors use to improve recovery performance.

Tratta's self-service portal allows consumers to access account information, view balances, and make payments without contacting your agency:

When consumers control their own payment experience, they're more likely to complete transactions.

Tratta executes outreach automatically based on account behavior and predefined rules:

Agencies can adjust strategies quickly based on performance data instead of waiting for monthly reports.

Tratta provides real-time dashboards that show portfolio performance, payment trends, and account movement:

This visibility enables agencies to optimize performance continuously.

Tratta enforces compliance automatically:

These controls reduce compliance risk and simplify regulatory audits. Your team doesn't need to remember every rule because the system enforces them automatically.

Tratta integrates with your existing technology stack through REST APIs:

This integration eliminates manual reconciliation and ensures that all systems stay updated automatically.

Manual accounts receivable processes create execution gaps that slow collections, increase costs, and expose agencies to compliance risk. As portfolios grow, these gaps become unsustainable.

Accounts receivable automation vs traditional manual processes isn't about replacing your team. It's about giving them tools to execute consistently at scale. Automation handles routine tasks so your agents can focus on complex negotiations and high-value recoveries.

Tratta provides the automation infrastructure collection agencies need to recover accounts efficiently while maintaining control and compliance. Self-service payment access, behavior-driven outreach, and real-time reporting work together to improve recovery rates and reduce operational costs.

See how Tratta can reduce manual effort, improve recovery outcomes, and strengthen compliance across your operation. Schedule a demo today.

Implementation timelines depend on portfolio complexity and integration requirements. Most collection agencies can deploy accounts receivable automation within 4-8 weeks when account data is clean and workflows are clearly defined.

Yes. Effective accounts receivable automation platforms integrate with existing collection management systems, CRMs, and ERPs through APIs. This allows agencies to automate processes without replacing core infrastructure.

Automation reduces manual workload for routine tasks but doesn't eliminate the need for agents. It allows teams to focus on high-value accounts, complex negotiations, and situations that require human judgment, rather than spending time on repetitive administrative work.

Automation improves compliance by automatically enforcing communication timing rules, disclosure requirements, and documentation standards. The system maintains complete audit trails and prevents common violations that occur with manual processes.

Consumer experience improves with automation. Self-service payment options, immediate account access, and precise timing of communication give consumers control over their payment experience. This reduces frustration and increases voluntary payment completion rates.