According to the U.S. Department of the Treasury’s 2023 Financial Report, the federal government reported over $319.9 billion in net accounts receivable. This figure highlights the scale of unpaid balances across the economy and the importance of consistent follow-up in moving money toward resolution.

For collection agencies, this reality shows up every day in the form of placements with very different levels of readiness. The way creditors handle accounts receivable follow- up before referral shapes what agencies receive. Timing, documentation, and recorded consumer responses all influence how quickly an account can move forward once it enters collections.

This guide explores what effective follow-up looks like before accounts reach an agency, where common breakdowns occur, and how agencies can assess placement quality early. By understanding these patterns, agencies can focus their effort on accounts that are better positioned for recovery and set clearer expectations with creditors.

Accounts receivable follow-up is the series of actions creditors take to contact customers about unpaid invoices before referring accounts to you. Knowing this process helps you evaluate placement quality and predict which accounts will convert.

The follow-up process typically includes:

Follow-up differs from collections in both tone and timing. It happens when accounts are still current or recently past due, before internal recovery efforts are exhausted and accounts land on your desk.

The quality of this upstream follow-up process determines the condition of accounts you receive. Accounts transferred with complete documentation, verified contact information, and clear payment history close faster than accounts with incomplete data.

For debt collection agencies, recovery performance is heavily influenced by what happens before an account is placed in collections. Accounts receivable follow-up shapes consumer behavior, data quality, and engagement levels that directly affect collection success.

Here’s why it matters:

In practice, strong accounts receivable follow-up doesn’t just support collections; it also determines how recoverable accounts are once they reach an agency.

Suggested Read: Best Practices for Improving Law Firms' Accounts Receivable Process

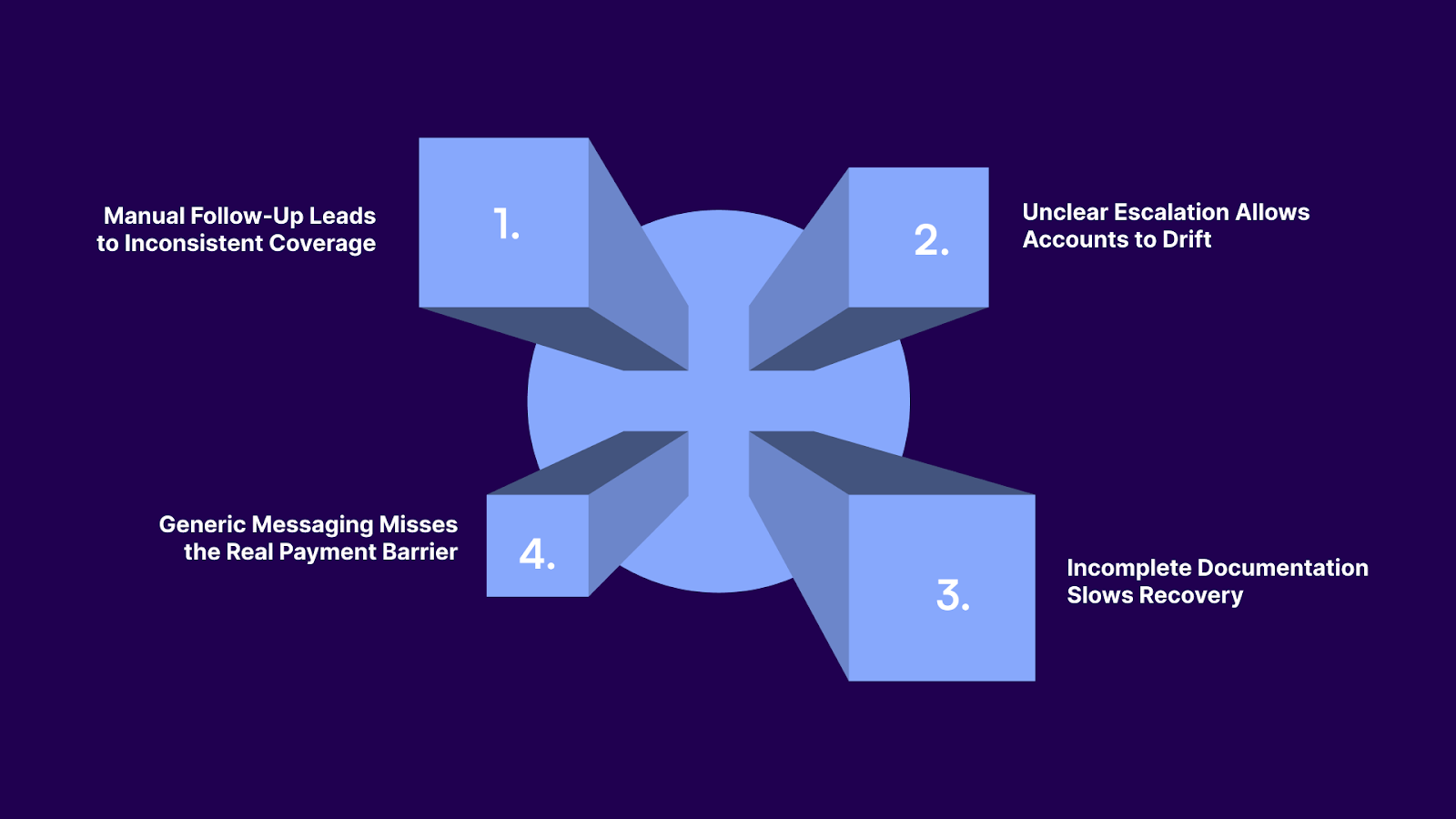

Even when creditors make genuine efforts to follow up, execution often breaks down in ways that directly impact collection agencies. Recognizing these breakdowns helps agencies understand why some placements perform better than others and identify warning signs early when evaluating new portfolios.

The most common breakdowns include the following.

When follow-up depends on spreadsheets, inbox reminders, or individual memory, consistency suffers. Some accounts receive repeated contact, while others age without meaningful engagement.

How this affects agencies:

Many creditors lack defined rules for when and how follow-up should intensify. As a result, accounts often enter collections without having received structured early intervention.

Impact on collection performance:

When prior contact attempts, payment promises, or disputes aren’t clearly documented, agencies are forced to rebuild context from scratch.

Downstream consequences:

Uniform reminders fail to account for disputes, partial payments, or consumer-specific issues. These unresolved barriers often surface only after agencies initiate contact.

Results agencies see early on:

When these challenges compound, agencies inherit accounts that require extra validation, higher compliance scrutiny, and more effort per dollar recovered. This is why structured, well-documented follow-up upstream matters so much.

Platforms like Tratta help creditors standardize outreach, centralize communication history, and maintain audit-ready records, so agencies receive accounts that are ready for recovery. Book a demo to see how it works.

Suggested Read: Understanding Accounts Receivable: An Analysis and Calculator Guide

Before an account is placed with a collection agency, it should move through a defined follow-up process designed to either resolve the balance or clearly establish that escalation is necessary. For collection agencies, this process determines placement quality, recovery effort, and compliance exposure.

In practice, the accounts receivable follow-up process has three functional stages.

This stage ensures the consumer is aware of the balance and understands how to pay.

At a minimum, this includes:

For agencies, this stage answers a simple question: Was the consumer properly notified before delinquency?

When this step is completed and documented, agencies can proceed without spending early contacts establishing basic awareness. When it’s missing, the first outreach is often consumed by disputes and clarifications rather than recovery.

Once a payment is missed, follow-up should shift from notification to intent evaluation.

This stage typically includes:

For agencies, this stage provides critical signals:

Accounts that reach collections with this engagement history allow agencies to prioritize effectively and adjust tone and strategy from the first contact.

When follow-up no longer produces engagement or resolution, the account should be prepared for referral to collections.

This stage is defined by:

For agencies, this stage determines whether an account is ready to work or requires reconstruction before collection activity can begin.

Accounts referred with full follow-up history, verified balances, and recorded consumer behavior move faster and carry lower compliance risk than accounts referred without context.

In short, the accounts receivable follow-up process before collections exists to establish notice, test intent, and document escalation. When those steps are completed, agencies can focus on recovery. When they are skipped or poorly documented, agencies absorb the operational and regulatory costs.

Suggested Read: Top 10 KPI Metrics for Effective Tracking of Accounts Receivable

You can usually tell whether an account originated from a manual or automated follow-up process within the first few touches. The difference appears in timing, consistency, documentation, and overall recoverability.

Manual follow-up can be effective at low volumes. As portfolios grow, maintaining discipline, visibility, and complete records becomes increasingly difficult. Automated follow-up does not replace judgment. It ensures that core actions occur consistently and without gaps.

Here is how manual and automated follow-up compare in practice:

Follow-up execution directly affects placement quality. Manual processes introduce variability and gaps, while automated follow-up ensures consistent timing, documentation, and escalation.

Tratta supports this automated approach by structuring follow-up, centralizing communication and payments, and preserving audit-ready records, so accounts reach collections with the context agencies need to recover efficiently. Get a free demo to see its benefits in action.

Suggested Read: Top 10 Accounts Receivable Automation Software Solutions

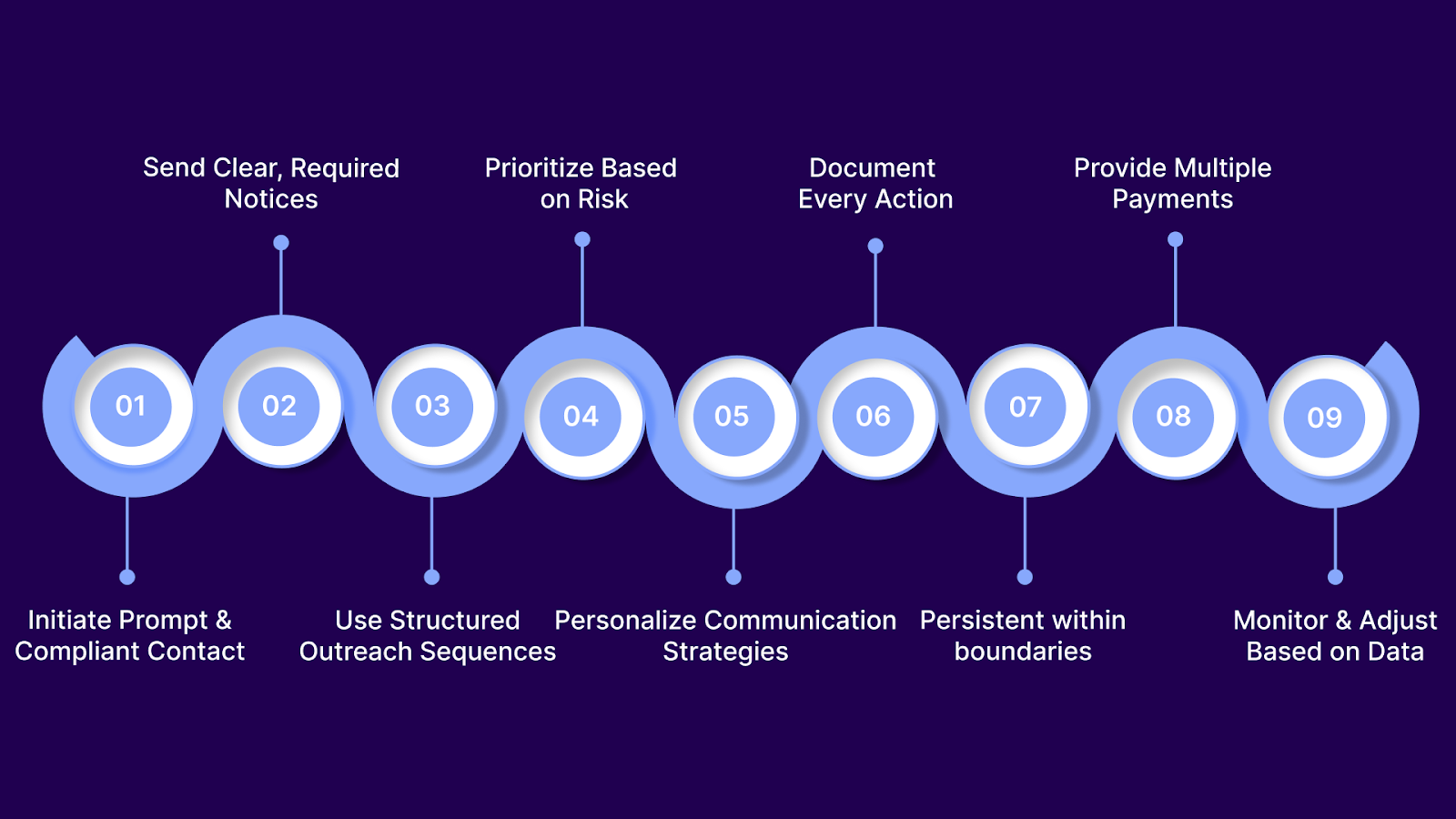

When you receive an account, you can usually tell within minutes whether upstream follow-up was handled well or poorly. The practices below consistently separate clean, workable placements from accounts that require excessive validation, compliance checks, and agent time.

Use these as benchmarks for evaluating portfolio quality and for setting expectations with creditors.

Objective: Start outreach quickly to maximize recovery while staying within legal guidelines.

Objective: Deliver legally required disclosures and validation notices accurately.

Objective: Build a predictable, recordable dunning process that respects legal limits.

Objective: Allocate agency resources where they’re most likely to yield results.

Objective: Increase engagement by aligning outreach style and timing with debtor circumstances.

Objective: Create an irrefutable compliance and performance trail.

Record:

Why this matters:

Objective: Maximize recovery while minimizing risk of legal exposure.

Objective: Reduce friction and accelerate collections.

Objective: Use real performance data to refine follow-up processes.

However, it's important to note that consistently implementing these practices is often the hardest part, which is why the right tooling becomes relevant.

Accounts receivable follow-up often breaks down due to inconsistent outreach, disconnected systems, limited documentation, and payment friction. Tratta is built to address these gaps by centralizing follow-up, payments, communication, and compliance into a single platform that preserves context as accounts move toward collections.

By consolidating activity into one system, Tratta helps ensure follow-up is executed consistently, documented completely, and aligned with actual consumer behavior, so accounts arrive ready for recovery rather than requiring reconstruction.

Campaign Management and Behavioral Automation

Customization and Configurability

Security and Compliance Controls

By structuring accounts receivable follow-up through Tratta, the issues outlined throughout this guide can be addressed at their source.

Clear, well-structured accounts receivable follow-up helps ensure accounts move into collections with continuity rather than gaps. When follow-up activity is organized and carried forward, agencies spend less time reconstructing history and more time progressing accounts through resolution.

Technology can support this handoff by keeping outreach, payments, and records connected as accounts approach placement. When follow-up data remains intact, transitions into collections are simpler and more predictable.

Tratta provides a platform for managing follow-up activity in one place, helping preserve account context through referral. Schedule a demo to see how Tratta supports structured follow-up before accounts reach collections.

Review documentation completeness, contact history continuity, escalation records, and payment updates to determine whether accounts will be workable or require reconstruction.

Missing contact attempts, unclear balances, undocumented disputes, or no recorded consumer responses often signal premature referral.

No. Automation enforces consistency while still allowing agencies and creditors to adapt messaging, timing, and escalation based on account behavior.

Ideally, before placement, during onboarding, or portfolio review, align on documentation standards, escalation criteria, and data handoff requirements.

Tratta supports upstream follow-up by centralizing outreach, payments, and records so account context remains intact as balances approach collections.