Auto finance collections are becoming harder to manage as consumer behavior shifts and traditional outreach becomes less effective. At the same time, the US auto finance market is projected to grow from about $707.81 billion in 2026 to nearly $889.45 billion by 2031. This may lead to higher volumes of delinquent accounts flowing into third-party collections.

This creates pressure for agencies to improve recovery rates without adding operational strain. Disconnected communication, delayed follow-ups, and rigid processes make it difficult. Omnichannel communication enables consumers to engage through their preferred channels and complete payments with less friction.

In this article, we explore how omnichannel debt collection in auto finance improves recovery by connecting outreach, timing, and payments into a more seamless consumer experience.

Quick look:

Payment rates in auto finance collections are under pressure, even as account volumes continue to grow. According to Equifax, in 2025, 1.9% of consumers were 60+ days past due (DPD) on their auto finance obligations. The numbers represent a significant volume of delinquent accounts placed with collection agencies that require consistent, effective engagement.

The issue is not just delinquency. It is the gap between consumer intent and the ability to act. Many consumers are willing to resolve debts, but the collection experience often makes it harder than it needs to be.

The following gaps contribute to low payment rates:

These challenges are systemic and rooted in collection models that were not designed for digital-first consumers. In the next section, we break down what a more connected, consumer-centric approach looks like in practice and how it differs from simply adding more channels.

Suggested Read: 7 Advanced Debt Management Solutions for Collection Agencies

Omnichannel communication creates a consumer-centric experience across every touchpoint. Instead of treating channels as separate outreach tools, it connects them into a single system where communication, context, and actions flow seamlessly.

The following elements define how omnichannel debt collection works in practice:

Tratta brings this into a single platform by combining email, SMS, voice, and more into coordinated campaigns with channel-specific routing and behavior-driven triggers. It also enables personalized outreach with trackable messaging, real-time analytics, and built-in compliance controls, such as consent management and opt-in enforcement. Request a free demo.

Payment rates improve when communication feels relevant, timely, and easy to act on. Consumers expect more than generic reminders. Research from McKinsey & Company shows that 71% of consumers expect personalized interactions, reflecting a clear shift toward tailored, context-driven engagement.

Omnichannel strategies make this possible by combining data, automation, and connected communication into a single, structured approach. The following mechanisms directly impact payment outcomes:

These advantages shift collections from reactive outreach to structured, data-driven engagement that consistently improves payment outcomes. In the next section, we break down the specific components that make these strategies effective and how they come together in a practical auto finance collections environment.

Suggested Read: AI's Role in Enhancing Customer Communications in Financial Services

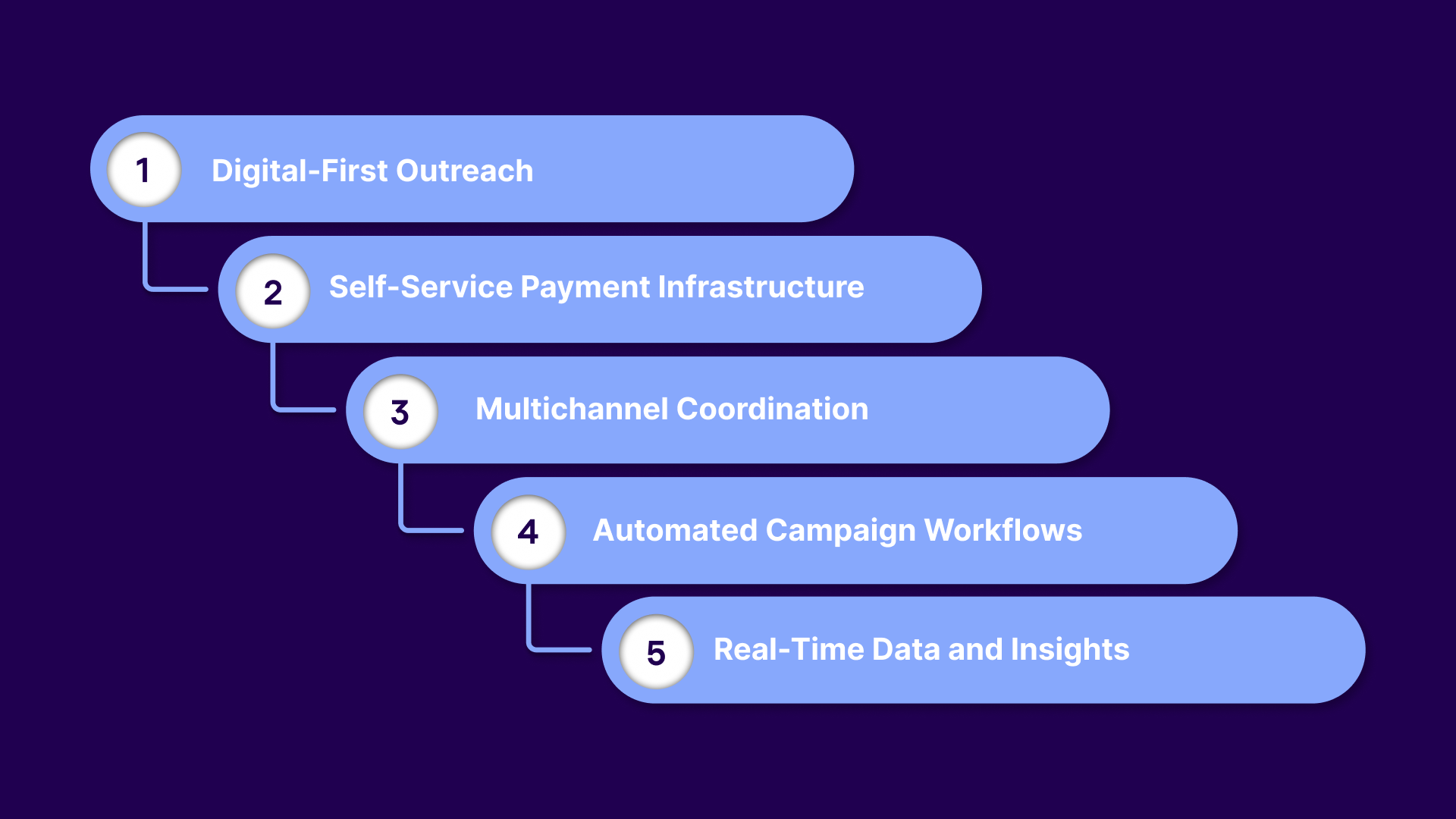

An effective omnichannel strategy is built by structuring how those channels work together to guide consumers from initial contact to completed payment. In auto finance collections, this requires a combination of communication, automation, and payment infrastructure that operates as one system.

The following components define what makes an omnichannel strategy effective in practice:

Digital channels such as SMS and email are the primary drivers of engagement in collections. They offer immediacy, higher open rates, and easier access compared to traditional call-only approaches.

These elements ensure digital outreach is consistent, scalable, and action-oriented:

Consumers are more likely to pay when they can act independently rather than rely on an agent. Self-service tools give them control over when and how they resolve their accounts.

These capabilities make self-service effective and easy to use:

Channels must work together, not compete for attention. Coordination ensures that every interaction builds on previous engagement instead of repeating or conflicting with it.

These practices keep communication aligned across channels:

Automation ensures that outreach is timely, consistent, and scalable. It removes the need for manual follow-ups while maintaining structured engagement.

These workflow elements help maintain consistent consumer engagement:

Data is what turns omnichannel from a concept into a performance-driven system. Real-time visibility allows teams to adjust strategies based on what is working.

These insights help optimize performance and decision-making:

Tratta operationalizes this strategy by giving you control over how and when each channel is used. You can design channel-specific campaigns, route communication based on consumer behavior, and ensure every interaction is tracked and compliant from the start. Get in touch with us to learn more.

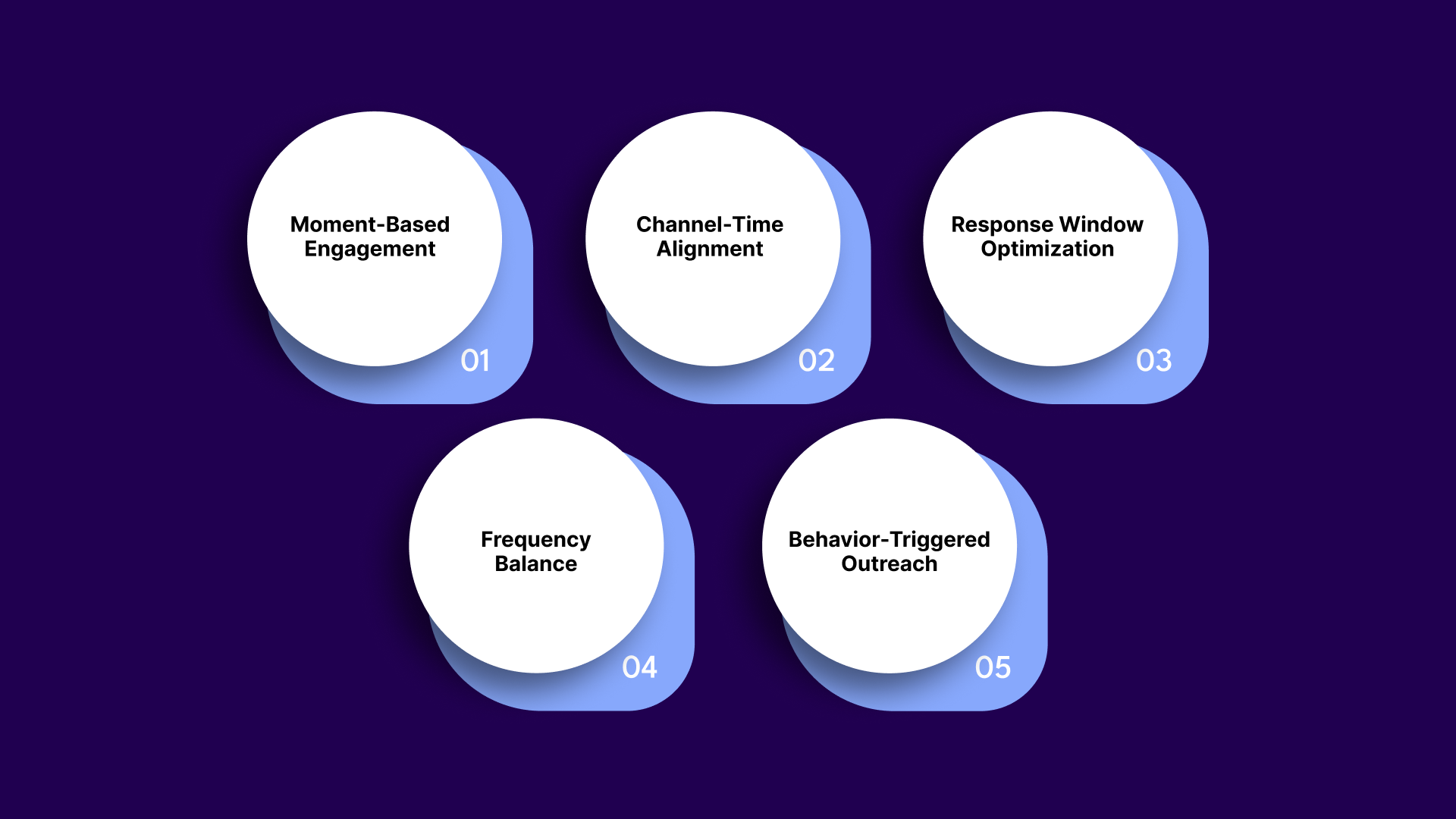

When you reach a consumer matters as much as how you reach them. Even well-crafted messages can fail if they are delivered at the wrong moment, when the consumer is unavailable, distracted, or not ready to act. Timing plays a critical role in converting intent into actual payment.

The following factors explain how timing influences payment behavior:

These timing strategies help ensure that communication reaches consumers when they are most likely to respond. In the next section, we look at how to remain compliant across channels, ensuring that outreach remains both effective and within regulatory boundaries.

As communication expands across channels, compliance becomes more complex and more critical. Each touchpoint must follow strict regulatory guidelines, and inconsistencies across channels can quickly create risk.

The table below highlights key compliance areas and the statutes that govern them:

Maintaining compliance across multiple channels requires structured processes and consistent oversight. Without it, even well-intentioned outreach can result in violations.

To reduce risk and maintain compliance, agencies should focus on the following:

As omnichannel strategies scale, manual compliance management becomes increasingly difficult. In the next section, we explore how using the right technology can help agencies enforce compliance automatically while improving efficiency and performance.

Tratta is a debt collection platform designed to help agencies automate communication, optimize payments, and improve recovery outcomes. It brings together outreach, self-service, and data into one system, allowing teams to manage higher volumes without increasing operational complexity.

Scaling collections is not about adding more agents. It is about improving how each account is handled, reducing manual effort, and enabling consumers to resolve balances independently. A structured, omnichannel approach supported by the right platform makes this possible.

The platform brings together the following features into one system:

To see how these capabilities translate into real outcomes, it helps to look at a practical example.

InDebted: Scaling Digital Collections with Coordinated Omnichannel Engagement

InDebted needed to modernize its US operations after acquiring a portfolio that relied on manual processes and lacked digital engagement. Instead of increasing agent effort, the focus shifted to building a connected system where communication and payments worked together using Tratta.

The strategy centered on aligning outreach, timing, and self-service across channels:

With Tratta enabling this coordinated approach, InDebted saw a 1,861% increase in self-serve payments and scaled to support higher account volumes. This highlights how structured omnichannel communication, combined with self-service, can significantly improve both engagement and recovery outcomes.

Auto finance collections often fall short when outreach is fragmented, follow-ups are mistimed, and payment processes create unnecessary friction. As volume increases, these gaps lead to lower engagement, missed payment opportunities, and rising operational strain.

Tratta addresses these challenges by unifying communication, payments, and automation into a single system. With features like omnichannel messaging, self-service payment portals, and real-time workflows, it enables agencies to drive higher payment rates while managing collections more efficiently.

Build a collection strategy that improves outcomes without increasing complexity. Start using a more connected, automated approach to drive consistent recovery. Learn more today.

Under Regulation F (12 CFR 1006.14), collectors may make no more than 7 call attempts within 7 days per debt, with additional restrictions after consumer contact.

When an auto finance account goes to collections, it is either assigned to a third-party agency or sold to a debt buyer. The agency then begins outreach to recover the balance through calls, digital communication, or payment arrangements based on the account terms and applicable regulations.

Yes, omnichannel strategies improve collection rates by increasing consumer engagement and reducing friction. Coordinated communication across SMS, email, and IVR makes it easier for consumers to respond and complete payments.

Agencies can improve recovery by adopting digital-first strategies, automating outreach, and offering flexible payment options. Using omnichannel communication and self-service tools helps increase engagement and payment completion rates.

The most effective channels include SMS, email, IVR, and self-service payment portals. These channels enable faster, more convenient engagement than traditional calls, especially when used together as part of an omnichannel strategy.