Collection agency operations leaders rarely lose accounts because agents ignore follow-up. The larger problem is that follow-up often depends on manual queues, disconnected outreach tools, and payment records that update too late.

A consumer may open an SMS but never reach a usable payment path. Another may pay through a portal but still receive the next reminder. An agent may take a call without seeing the latest email, IVR, dispute, or payment activity. The account keeps aging while your team pieces together what happened.

Dunning process automation gives collection agencies a cleaner way to manage payment follow-up at portfolio volume. It turns reminders into a governed account workflow, so your team can reduce manual checks without losing control over timing, channel rules, or consumer context.

Dunning is the structured process of contacting consumers about outstanding balances and guiding them toward resolution. In a collection agency, that process starts when an account enters recovery and continues through notices, reminders, payment options, disputes, exceptions, and agent review.

Dunning process automation uses account rules to trigger those steps without asking agents to schedule each follow-up by hand. The rules can depend on account age, balance size, debt type, client requirements, consumer response, channel permission, dispute status, payment status, or prior contact activity.

Manual follow-up often relies on spreadsheets, static queues, batch exports, agent reminders, or disconnected campaign tools. Those methods can work at low volume. They become harder to control when your agency manages large portfolios across clients, states, and account types.

An automated sequence gives every eligible account a defined path. A newly placed account can receive an initial digital notice. A consumer who clicks a link but leaves before payment can receive a different follow-up. A consumer who pays, disputes, opts out, or enters a payment plan can move out of the standard reminder path.

The result is stronger account coverage with fewer manual checks.

Many dunning resources are written for SaaS teams that need to recover failed card payments. Collection agencies work in a broader environment.

Your agency may need to manage validation notices, disputes, opt-outs, call frequency controls, payment plans, settlement offers, client rules, IVR activity, agent review, and audit records. For agencies, dunning process automation has to support the full recovery workflow.

The FTC’s FDCPA text prohibits debt collectors from using abusive, deceptive, or unfair practices. Automated outreach in consumer debt recovery needs controls that reflect that environment.

Manual dunning usually starts with a practical setup. A team builds templates, creates follow-up timing, assigns queues, and asks agents to work the accounts. Problems appear when volume, client variation, and channel activity increase.

Your dashboard may show a busy team. That does not always mean the right accounts are moving. Agents can spend too much time checking status, rebuilding history, and deciding which follow-up belongs next.

An account changes every day after placement. The consumer may open a message, click a link, make a partial payment, dispute the balance, request no further contact, change phone numbers, or qualify for a different client-approved option.

If follow-up depends on stale exports, the outreach sequence can miss those changes. Agents may work accounts that already paid. Digital notices may continue after a dispute. High-intent consumers may leave because the payment path was unavailable when they were ready.

The damage is operational. Coverage becomes uneven. Call volume stays high. Agents spend more time confirming what happened before they can decide what to do next.

Debt collection remains a high-scrutiny category. The CFPB’s 2025 FDCPA Annual Report reported approximately 207,800 debt collection complaints in 2024, representing seven percent of total complaints received that year.

The same report shows why documentation matters. The most common debt collection complaint issue involved attempts to collect debt consumers said they did not owe. Other complaint categories included written notification issues, false statements, communication tactics, and electronic communication issues.

For collection agency leaders, the lesson is practical. Your team needs clean records, clear communication history, and fast access to proof of what was sent, when it was sent, how the consumer responded, and what account status existed at the time.

Many agencies use separate systems for account management, email, SMS, IVR, payment processing, disputes, and reporting. Each tool may work inside its own lane. The process breaks when the account state is not shared.

Your team then has to answer basic questions manually. Has the consumer already paid? Did they click the SMS link? Did they opt out? Did they dispute? Was the last IVR call completed? Is this account eligible for a plan or settlement offer?

Every manual check slows the account path. It also creates more room for uneven follow-up.

Also Read: 5 Ways Automated Payment Follow-Up Services Can Support AR Teams

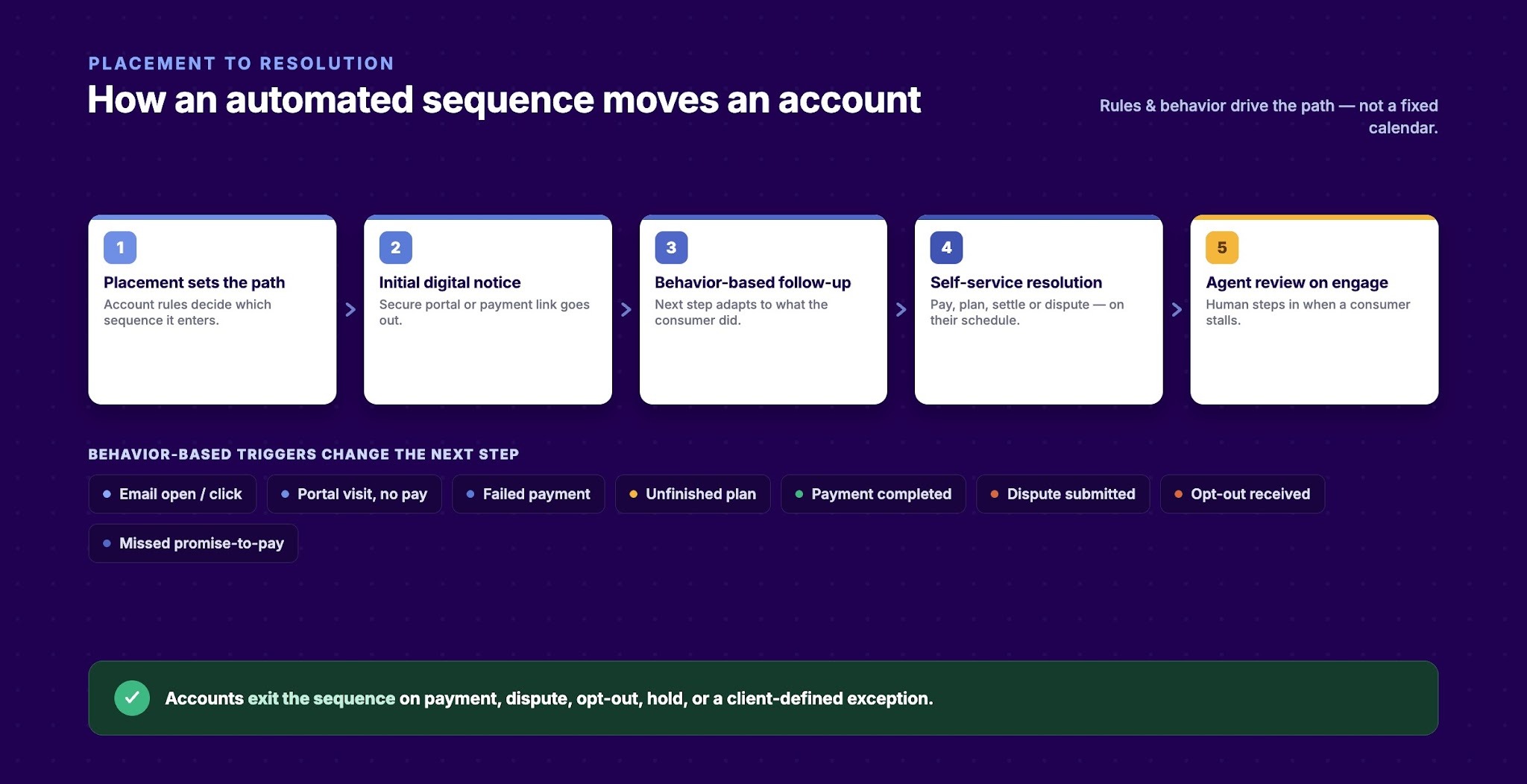

A strong automated dunning sequence follows the account from placement through payment, dispute, exception handling, or agent review. The process should reflect account rules and consumer behavior instead of relying only on a fixed calendar.

Each agency will set different rules. Client requirements, balance size, debt type, state, account age, and consumer preference all affect the starting path and the next step.

The first step is deciding which accounts enter which sequence. A newly placed medical account may need a different path than a charged-off credit card account. A low-balance account may rely more on self-service. A high-balance account may need earlier agent review.

Once the account enters the process, the system can trigger actions such as the following:

This gives agents more context before they step in. It also gives consumers more chances to resolve the account through self-service.

A static cadence sends the same message on the same schedule. That can miss important signals.

Behavior-based rules let the next step change based on what the consumer did. A consumer who opens an email and clicks the payment link should receive a different follow-up than a consumer who never engaged. A consumer who starts a payment plan but leaves before confirming it may need a different prompt from a consumer who submitted a dispute.

Common triggers include:

These triggers help your agency move from fixed reminders to account-aware follow-up.

Automated outreach loses value when every message tells the consumer to call an agent. That adds a handoff at the exact moment the consumer may be ready to act.

A stronger process routes each allowed message to a resolution path. That path may be a self-service portal, secure payment link, IVR payment option, payment plan page, settlement offer, or dispute form. The consumer should be able to act when they are ready, including outside business hours.

Outreach creates the prompt. Self-service gives the consumer a way to resolve the account.

The right setup depends on your clients, portfolio mix, state footprint, consent model, and compliance program. Even with those differences, the core requirements are similar across high-volume recovery teams.

Your process needs to coordinate channels, apply communication controls, route consumers to payment options, and show which actions are producing movement.

Collection agencies often use several channels, but those channels may run as separate campaigns. That creates confusion for agents and consumers.

A better setup ties each channel to the account record. Email can carry detailed information. SMS can drive quick portal access where allowed. IVR can help consumers verify details, pay, or move toward an agent. Phone calls can be reserved for accounts where a conversation is more likely to help.

The sequence should respond to account activity. If the consumer pays through the portal, the next reminder should stop. If the consumer clicks but leaves before payment, the next message should reflect that stage. If the consumer opts out of a channel, the workflow should honor that choice.

Debt collection communication requires careful controls. The CFPB’s Debt Collection Rule FAQs describe telephone call frequency presumptions for debt collectors, including the standard around more than seven calls within seven consecutive days and the seven-day period after a telephone conversation about a debt.

The CFPB also notes that these telephone call frequency presumptions do not apply to media such as text messages and email. At the same time, conduct across media may still violate the general prohibition against harassing, oppressive, or abusive conduct.

That distinction matters. Your agency needs controls that account for more than call counts. A dunning process should support opt-out handling, channel permissions, approved templates, timing windows, audit records, dispute paths, and review queues.

Dunning process automation should give operations leaders more than send counts. You need to know which actions produced account movement.

Useful reporting should show how accounts move through the sequence and where they stop. That includes message delivery, opens, clicks, portal visits, payment completions, plan starts, settlement activity, disputes, failed payments, and agent handoffs.

The most useful views include:

These reports help your team adjust cadence and channel strategy based on account behavior rather than agent anecdotes.

Also Read: Best Collection Dashboard Features for US Recovery Teams in 2026

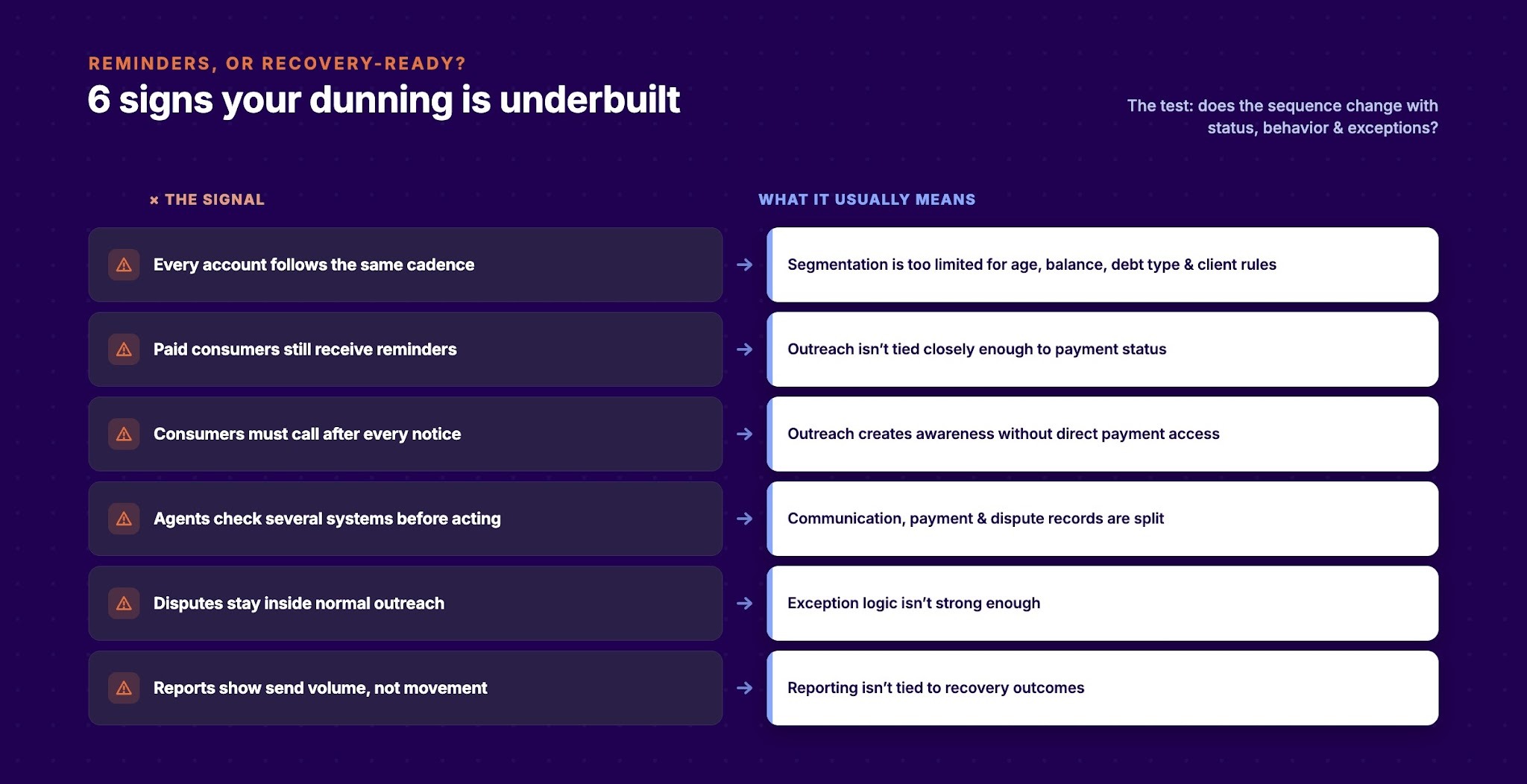

A collection agency can have automated outreach and still run an underbuilt dunning process. The test is whether the sequence changes with account status, consumer behavior, payment activity, and exceptions.

Use the checks below to separate basic reminders from a recovery-ready process.

These signals do not always call for more staff. They usually point to process design, data sharing, or reporting gaps.

A stronger review should include the teams that own recovery outcomes, controls, and payment flow. Each team should test a different part of the process.

AR leaders should ask whether the sequence improves account coverage and reduces manual review. Compliance leaders should ask how opt-outs, disputes, timing rules, and communication records are handled. Payment operations should ask whether every allowed message gives consumers a direct path to payment, plan setup, or the right exception flow.

If the platform cannot answer those questions clearly, the agency may only be automating reminders.

Much of the available dunning content focuses on subscription companies recovering failed recurring payments. Collection agencies evaluate a broader recovery path.

Your agency is often contacting consumers after an account has moved into recovery. The consumer may not recognize the agency name. They may dispute the balance. They may need validation information. They may need a payment plan or settlement option instead of a card retry.

This difference should guide platform review. A collection agency needs recovery-specific workflows, payment options, exception handling, and audit-ready communication records.

Also Read: The Debt Collector’s Guide to Advanced Reporting for Recovery

Tratta is debt collection software for collection agencies, law firms, credit issuers, and debt buyers. For agencies reviewing dunning process automation, the strongest fit is the connection between outreach, payment access, reporting, IVR, and workflow control.

Tratta supports the dunning workflow through these capabilities:

For your agency, the value is control across the recovery path. Outreach can point consumers to self-service. IVR can support phone-based resolution. Payment activity can feed reporting. Exceptions can move to review. Your team can manage dunning as part of the collection process rather than as a separate reminder tool.

Also Read: Payment Collection System: What US Agencies Need in 2026

Dunning process automation gives collection agencies a more controlled way to manage payment follow-up across high-volume portfolios. Strong workflows connect account status, communication rules, consumer behavior, payment access, and reporting.

For operations leaders, the gain is less manual tracking and cleaner account movement. Consumers get clearer paths to resolve balances. Agents get better context before they step in. Compliance and client teams get records that are easier to review.

If your agency is ready to connect outreach, self-service payments, IVR, and reporting in one recovery workflow, schedule a demo with Tratta.

Dunning process automation in debt collection is the use of rules-based workflows to send sequenced payment outreach based on account status, timing, channel permission, and consumer behavior. It helps collection agencies manage reminders without scheduling every follow-up by hand.

Bulk messaging sends the same communication to a large group at a fixed time. Automated dunning changes outreach based on individual account status, balance, response behavior, payment status, dispute status, and channel permissions.

Compliance depends on workflow design, configuration, legal review, and ongoing oversight. A platform should support approved templates, contact controls, opt-out handling, dispute paths, communication records, and role-based review. Your agency should confirm legal requirements with counsel.

A self-service payment portal gives consumers a direct way to act after outreach. When a consumer receives an allowed message with a secure link, they should be able to verify identity, view the balance, choose an approved payment option, submit a dispute where available, or set a plan without waiting for an agent.

Look for account-status triggers, direct payment links, self-service options, IVR support, communication history, configurable rules, reporting by outreach stage, opt-out handling, dispute paths, security standards, and system connections with your existing recovery tools.