A consumer challenge can quickly expose weak points in a collection workflow. One file may begin with an agent call, move into a mailed letter, trigger a portal note, require creditor client records, and reach a credit reporting review before it closes.

For many recovery teams, that path is now part of normal account handling. In 2025, the CFPB received about 387,400 debt collection complaints. The most common issue was “attempts to collect debt not owed,” which accounted for 112,600 complaints, or 41% of debt collection complaints closed with an explanation or relief, according to the CFPB 2025 Consumer Response Annual Report.

For collection agencies, collection law firms, credit issuers, and debt buyers, those numbers point to a specific operations problem. Consumers are often questioning whether a balance is valid, accurate, paid, settled, recognized, or reported correctly. Debt dispute management gives your team a defined way to capture those challenges, review the right records, assign ownership, and keep a clear trail from intake to closure.

This guide explains how to structure that process so consumer challenges are easier to identify, route, investigate, document, and measure across your recovery work.

A disputed balance can touch more teams than a standard collection account. The first contact may sit with an agent. The proof may sit with the creditor client. The reporting question may sit with a furnisher review team. The final status may be needed by a supervisor, compliance lead, or client service manager.

That spread creates the pressure. The issue is no longer only whether one collector took the right note. The issue is whether your agency can preserve the full case trail across people, queues, and systems.

The CFPB’s 2025 report shows that account recognition is a major source of consumer concern. The report states that debt collection complaints about debts consumers did not recognize increased 240% compared with the monthly average for the prior two years. It also notes that many consumers said collection accounts appeared or reappeared on credit reports and requested validation or documentation from collectors, according to the same CFPB report.

For an operations leader, this trend creates a practical requirement. Your team needs quick access to placement data, balance history, payment records, communication history, and credit reporting status. If those details are scattered, the file takes longer to resolve and becomes harder to explain later.

Consumer challenges often arrive through one channel and continue through another. A phone denial may be followed by a document upload. A mailed dispute may lead to a credit reporting complaint. A CFPB complaint may reference a payment, settlement, or prior call.

When every channel has its own queue, handoffs become the weak point. Supervisors ask who last touched the file. Client service teams search for record requests. Credit reporting staff review data without seeing the full communication history.

The burden is not the number of touches alone. It is the lack of a single case view that shows issue, owner, status, records requested, and outcome.

Also Read: Guide to Credit Collections and How Agencies Handle Them

Debt dispute management covers consumer challenges about a debt or related account information. The issue may involve ownership, balance accuracy, payment posting, settlement terms, insurance responsibility, or credit reporting data.

This article is educational and operational. It is not legal advice. Your agency should review policies, templates, and case-handling rules with counsel.

Direct challenges can arrive through calls, letters, emails, portal notes, document uploads, or replies to digital messages. Agents need clear triggers for when ordinary contact becomes a file that needs review.

Common phrases include statements like these:

The same statement should receive the same label across channels, branches, and client teams.

For agencies that furnish credit information, disputed status can affect reporting review. The FDCPA text addresses false or misleading representation and includes communicating, or threatening to communicate, credit information known or that should be known to be false, including failure to communicate that a disputed debt is disputed.

Written challenges during the validation period need a separate workflow because timing can affect collection activity. Under the FDCPA, if a consumer notifies the debt collector in writing during the 30-day period that the debt, or part of it, is disputed, the collector must stop collection of the disputed debt or disputed portion until verification or a copy of a judgment is mailed to the consumer.

Regulation F defines the validation period as the period that starts when the debt collector provides validation information and ends 30 days after the consumer receives or is assumed to receive it, under 12 CFR §1006.34.

Your workflow needs to separate these files at intake so they do not sit in a general correspondence queue. The record should show when validation information was provided, when the written challenge arrived, what was reviewed, and when the response was sent.

Credit reporting challenges connect the consumer’s claim with furnished data. If your agency furnishes information, your team may receive cases through e-OSCAR or directly from the consumer.

e-OSCAR describes its system as browser-based and Metro 2 compliant, built for processing consumer credit disputes between data furnishers and consumer reporting agencies. These cases often require review of status, payment history, reporting fields, and dispute indicators.

Direct furnisher cases also have defined review duties. Under 12 CFR §1022.43, a furnisher must conduct a reasonable investigation of a direct dispute when it relates to areas such as liability for a credit account or other debt, terms of the debt, payment status, balance, or other information in a consumer report about the account.

For collection operations, credit reporting challenges need a defined owner, source records, status tracking, and a response record tied to the furnished information.

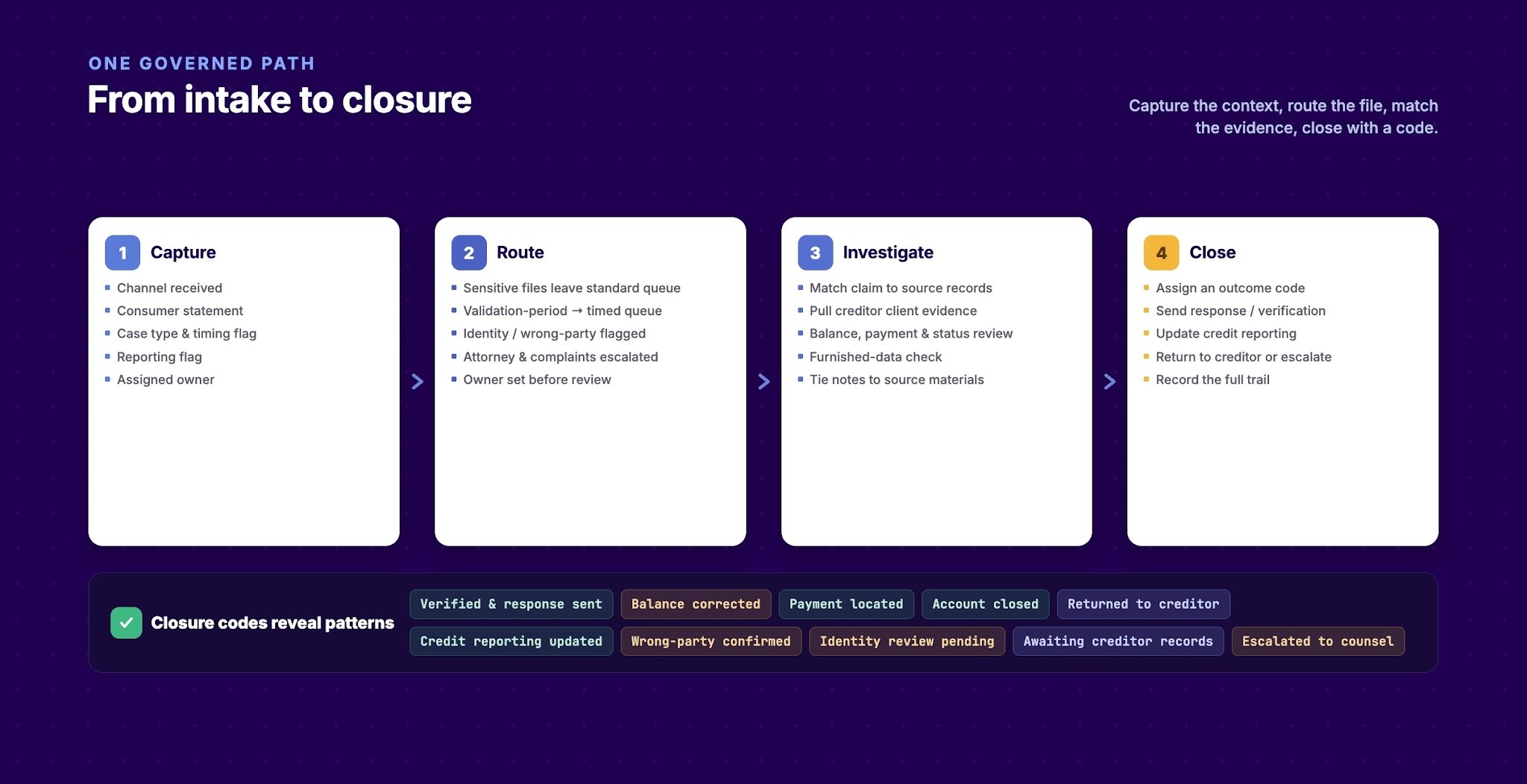

Intake has one job: turn an incoming consumer statement into a reviewable file before the context disappears. This is where the agency captures what was said, where it came from, whether timing matters, and who owns the next step.

A good intake model is simple enough for live agent work and structured enough for management review.

Your system should guide the first decision. A free-text note leaves too much room for interpretation and makes later review harder.

A practical intake record can use fields like these:

These fields help agents classify the issue without asking them to decide the final outcome.

Some files should leave the standard collector queue as soon as they are identified. The exact rule depends on your agency’s policy, account type, and counsel-approved procedures.

Common routing triggers include written validation-period challenges, identity or wrong-party claims, credit reporting challenges, attorney contact, formal complaints, and files where the agent cannot address the issue using approved information.

Clear routing protects workflow quality. Collectors know when to stop standard follow-up. Supervisors know who owns the next step. Managers can see which files are pending review.

A file record is incomplete if the letter, upload, complaint, or agent note cannot be found later. Intake should connect the source material to the file from the start.

That source material may include a scanned letter, portal message, uploaded proof of payment, CFPB complaint, e-OSCAR reference, or call note. A reviewer should be able to open the file months later and understand why it was routed without asking the original agent.

Also Read: How To Choose an Audit-Ready Debt Collection System

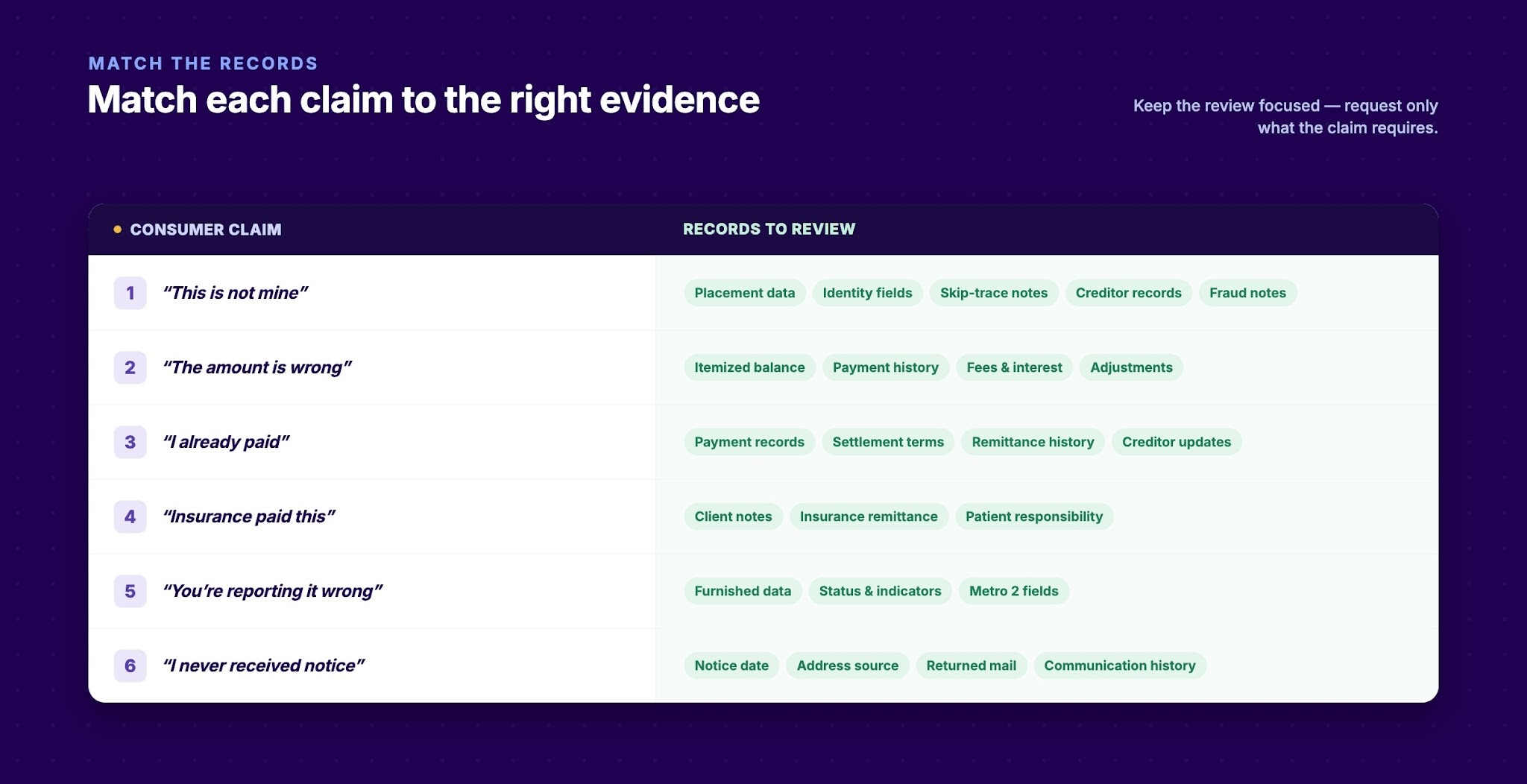

Investigation should begin with the consumer’s exact claim. A wrong-party claim, a balance challenge, a paid-in-full statement, and a credit reporting challenge each require different records.

This section covers evidence review, creditor client record requests, and closure coding.

The evidence request should fit the issue raised. This keeps the review focused and helps the case owner avoid broad document chasing.

This table should be adapted by portfolio type. A healthcare debt, credit card balance, auto deficiency, judgment, and debt buyer placement may each require different support.

Creditor client communication should not be written from scratch each time a consumer raises a challenge. Your agency needs to know which records each client can provide and how requests should be made.

A healthcare portfolio may require service dates, insurance notes, itemized statements, and patient responsibility records. A credit issuer portfolio may require agreements, charge-off statements, payment history, and prior dispute notes. A debt buyer portfolio may require sale records, account media, seller data, and placement details.

For high-volume clients, batch document requests can reduce repeated one-off follow-ups. It also gives your client service team a cleaner way to track what is pending.

Closure codes should show what happened. A vague “resolved” status hides whether the debt was verified, corrected, closed, updated, or escalated.

Better outcome codes include:

These codes turn file handling into management insight. Repeated balance corrections may point to placement file issues. Rising wrong-party claims may point to identity matching problems. Long waits for creditor documents may point to client service gaps.

Also Read: Best Collection Dashboard Features for US Recovery Teams in 2026

Dispute work depends on fast access to account context. If payments, messages, portal activity, documents, and reporting sit in separate tools, the review owner has to rebuild the file before they can act.

Tratta is debt collection software for collection agencies, collection law firms, credit issuers, and debt buyers. It brings payments, digital communications, consumer self-service, reporting, and workflow control into one platform. For debt dispute management, that helps teams see the account story with less tool-switching.

Tratta’s Reporting and Analytics helps collection leaders track activity across accounts, consumers, payments, and outcomes. In a dispute workflow, that visibility is useful when leaders need to see where work is building up.

This gives COOs and operations leaders a clearer way to manage staffing, client follow-up, QA focus, and portfolio review.

Tratta’s Consumer Self-Service Platform gives consumers a place to view balances, make payments, manage accounts, and use portal-based tools.

For disputed accounts, that matters because some consumers need a clear way to review account details or provide supporting material. A consumer may need to check payment history, upload proof of payment, review available options, or confirm recent account activity.

When those actions are tied to the account, the review owner has more context before follow-up. That can reduce back-and-forth that would otherwise happen through calls, mail, or scattered email attachments.

Tratta’s Omnichannel Communications supports consumer contact across channels such as email, SMS, voice, and chat.

That matters in dispute work because challenged files often include several touchpoints. A consumer may receive a letter, respond by text, call an agent, use the portal, and later upload a document. If those interactions are hard to connect, the team spends more time piecing together the timeline.

With connected communication history, agents and managers can review what was sent, what the consumer did, and what information was available before the file reached review.

Disputed accounts often involve sensitive consumer data, payment information, identity claims, account documents, and credit reporting details. Tratta’s Security and Compliance page describes support for audit-ready records, role-based access, secure payment handling, and data security controls.

For collection teams, this supports more controlled account handling. The value is not a promise of legal compliance. It is a more organized way to manage dispute-related activity inside a recovery workflow.

Also Read: The Complete CFPB Compliance Checklist for Collection Agencies

Debt dispute management works best when your agency gives every consumer challenge a defined path. Intake captures the issue. Routing sends sensitive files to the right owner. Investigation matches the claim to the right records. Closure codes show what happened. Reporting gives leaders a way to manage the process across portfolios and clients.

For collection agencies, collection law firms, credit issuers, and debt buyers, stronger file handling supports clearer review, cleaner consumer communication, and better workflow control. If your team wants to bring payments, communications, consumer self-service, and reporting into one connected recovery process, schedule a Tratta demo to see how the platform supports dispute-ready collection operations.

Agents should document the statement as a consumer challenge and route it according to your agency’s policy. If the agency furnishes credit information, the disputed status may also need review because the FDCPA addresses failure to communicate that a disputed debt is disputed when credit information is communicated.

A dispute intake form should capture the received date, channel, consumer statement, account ID, portfolio, case type, validation-period status, credit reporting status, assigned owner, and next action. If the consumer provided a letter or document, it should be attached or linked to the file record.

A challenged account should leave the standard collector queue when your agency’s policy requires review before further account activity. Common triggers include written validation-period challenges, credit reporting issues, identity or wrong-party claims, attorney contact, CFPB complaints, and cases where the agent cannot address the issue from approved account information.

Operations leaders should track open e-OSCAR items, aging, owner, reason, response status, records needed, and outcome. They should also review patterns by creditor client and portfolio because repeated balance, identity, or status issues may point to data problems before placement.

Agencies should define document expectations by account type. Common records include itemized balances, payment history, contracts or account agreements, service dates, insurance records, charge-off statements, settlement records, and account sale or placement details. Setting those expectations before placement can reduce delays when a consumer challenges a debt.