Payment friction remains one of the biggest barriers to successful debt recovery. Consumers may be willing to pay, but outdated payment processes, limited payment options, and disconnected experiences can create unnecessary obstacles. The shift toward digital payments continues to accelerate.

According to Nacha, the ACH Network processed 8.9 billion payments worth $24.1 trillion in the first quarter of 2026, while Same Day ACH payments exceeded $1.1 trillion in value for the second consecutive quarter.

As payment expectations continue to evolve, collection agencies are rethinking how consumers access and complete payments. In this article, we will examine how electronic payment transformation is reshaping collection operations, improving payment accessibility, and supporting modern recovery strategies.

Brief look:

Electronic payment transformation refers to the modernization of how consumers access, authorize, and complete payments throughout the recovery lifecycle.

"Payments modernization involves integrating regulatory compliance, operational models, customer experience, and competitive agility into a comprehensive vision for the future."

- KPMG

In third-party collections, electronic payment transformation is improving:

These improvements are becoming increasingly important as consumer payment behavior continues to evolve. The next question is why collection agencies should make digital payment strategies a priority and how payment modernization can influence long-term recovery performance.

Suggested Read: How Payment Communication Software Improves Debt Recovery

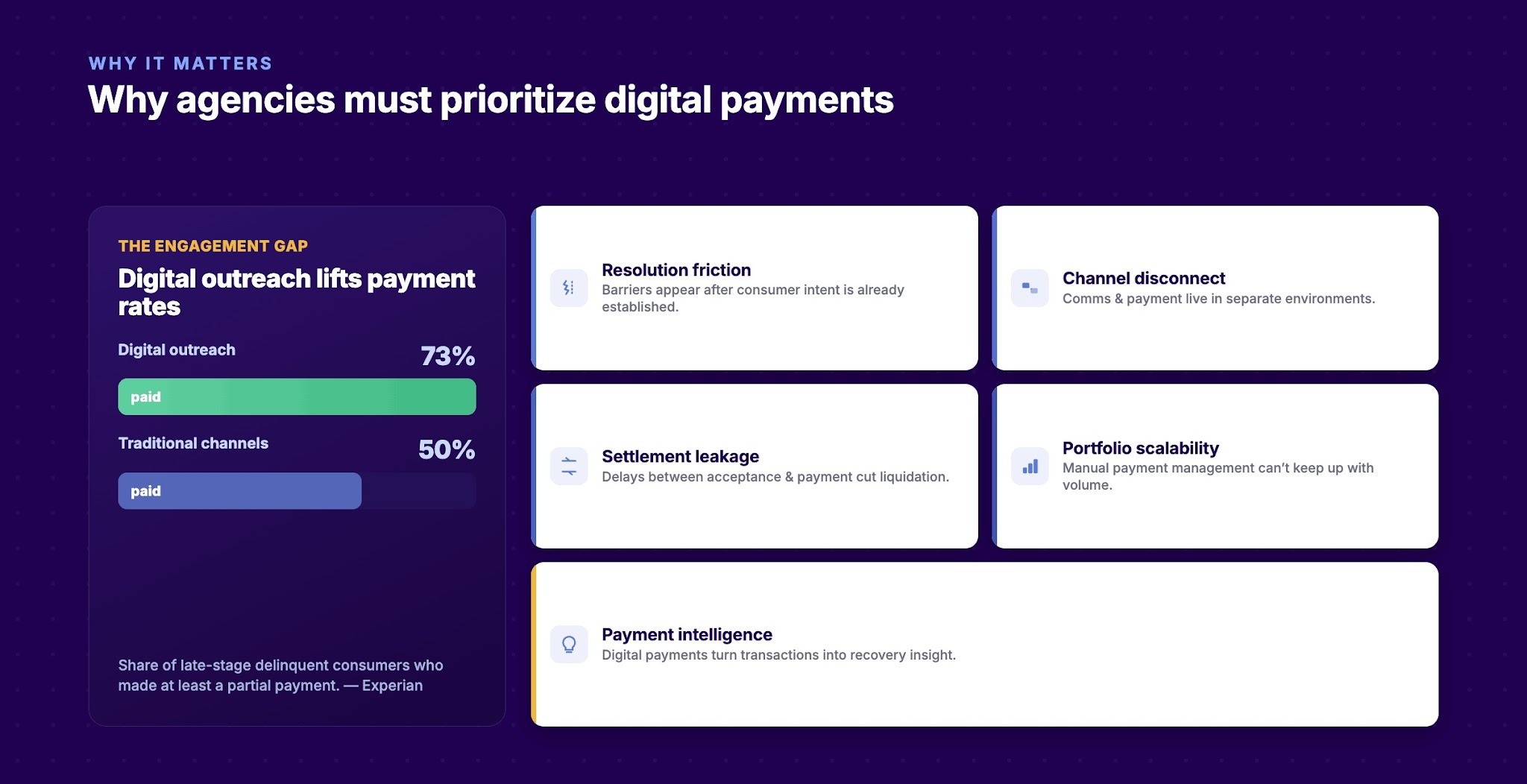

Digital payment adoption is increasingly influencing recovery performance. According to Experian, 73% of late-stage delinquent consumers made at least a partial payment after receiving digital outreach, compared with 50% contacted through traditional channels.

The following gaps highlight the growing relationship between digital engagement and payment behavior.

Many recovery strategies fail after consumer intent has already been established. Consumers may agree to resolve an account but encounter unnecessary barriers during the payment process. Digital payments reduce the operational distance between commitment and payment execution.

Collection communications and payment experiences often exist in separate environments. This fragmentation introduces abandonment risk at critical moments in the consumer journey. Digital payment ecosystems help create continuity between engagement and resolution.

Settlement performance is influenced by more than negotiation effectiveness. Delays between settlement acceptance and payment completion can reduce liquidation outcomes and increase arrangement fallout. Digital payment options help agencies capture recovery opportunities while engagement remains active.

As portfolio volumes increase, manual payment management becomes increasingly difficult to sustain. Administrative activities such as payment intake, arrangement tracking, and payment verification consume operational resources. Digital payments enable agencies to scale recovery operations without proportional increases in payment-related workload.

Traditional payment processes generate limited operational insight. Digital payment environments create structured data that can be used to analyze payment behavior, identify recovery trends, and optimize future collection strategies. This transforms payments from a transactional function into a source of recovery intelligence.

Payment modernization requires more than adding a payment button to a website.

Tratta helps agencies support digital payment transformation through Embedded Payments, Payments and Merchant Services, Consumer Self-Service Platform capabilities, and Multilingual Payment IVR. By integrating payment experiences directly into collection workflows, agencies can reduce payment friction. Schedule a free demo today.

Electronic payments are being driven by technologies that reduce payment friction, improve accessibility, and create more connected payment experiences.

These underlying technology stack helps agencies evaluate where payment modernization can create the greatest impact.

Core payment processing infrastructure:

Supporting account-based payments:

Enabling self-service resolution:

Connecting payment ecosystems:

Supporting mobile-first consumers:

These technologies represent the building blocks of modern payment ecosystems. The next step is understanding how agencies can translate these capabilities into operational outcomes. In the following section, we will examine the core components of electronic payment transformation in debt recovery.

Suggested Read: 5 Online Payment Solutions for Third-Party Collection Agencies (2026)

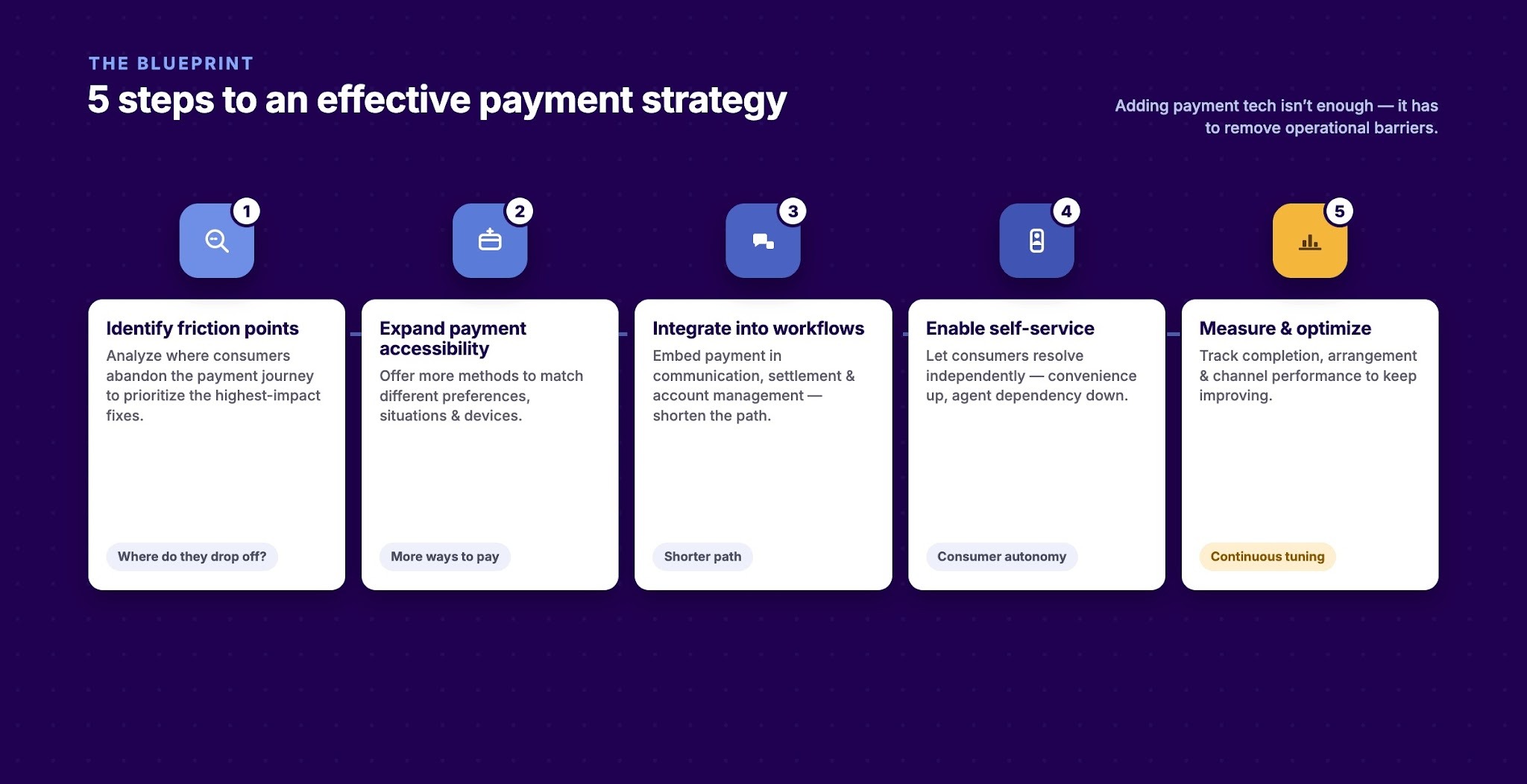

Electronic payment transformation is most effective when supported by a deliberate recovery strategy. Agencies that simply add new payment technologies often fail to address the operational barriers that limit payment completion.

The following approach helps ensure payment modernization translates into measurable recovery outcomes:

A strong payment strategy influences far more than transaction processing. In the next section, we will examine three ways digital payment strategies are changing collection operations across the recovery lifecycle.

Suggested Read: Predictions and Trends in the Debt Collection Industry for 2026

Digital payment strategy fundamentally changes how agencies execute recovery workflows, manage payment arrangements, and engage consumers throughout the account lifecycle. As payment capabilities become more integrated into collection technology, payment functions increasingly influence operational design.

Historically, communications and payments operated as separate activities. Digital payment strategies integrate payment opportunities directly into outreach, allowing consumers to move from engagement to resolution within the same interaction.

This can include:

Traditional payment plans often require significant manual administration. Digital payment systems can automate arrangement enrollment, scheduling, monitoring, and payment execution.

This may support:

Payment activity is no longer limited to transaction processing. Digital payment systems generate data that can be used to evaluate collection performance, identify trends, and inform future recovery strategies.

Common applications include:

Tratta Tratta combines payment execution with reporting and analytics, giving agencies greater insight into payment activity, arrangement performance, and recovery outcomes. This helps transform payments from a back-office function into a measurable part of collection strategy. Contact us to learn more.

While the benefits of payment modernization are well established, implementation is rarely frictionless. Many agencies must overcome technology constraints, operational dependencies, and process limitations before they can fully modernize payment experiences.

Identifying the following barriers early can help agencies build more effective transformation roadmaps:

Many of these challenges stem from treating payments as a standalone function rather than an integrated component of the recovery lifecycle.

As payment technology continues to evolve, modernization efforts are also being influenced by emerging industry trends. The next section explores the electronic payment trends collection agencies should watch in 2026.

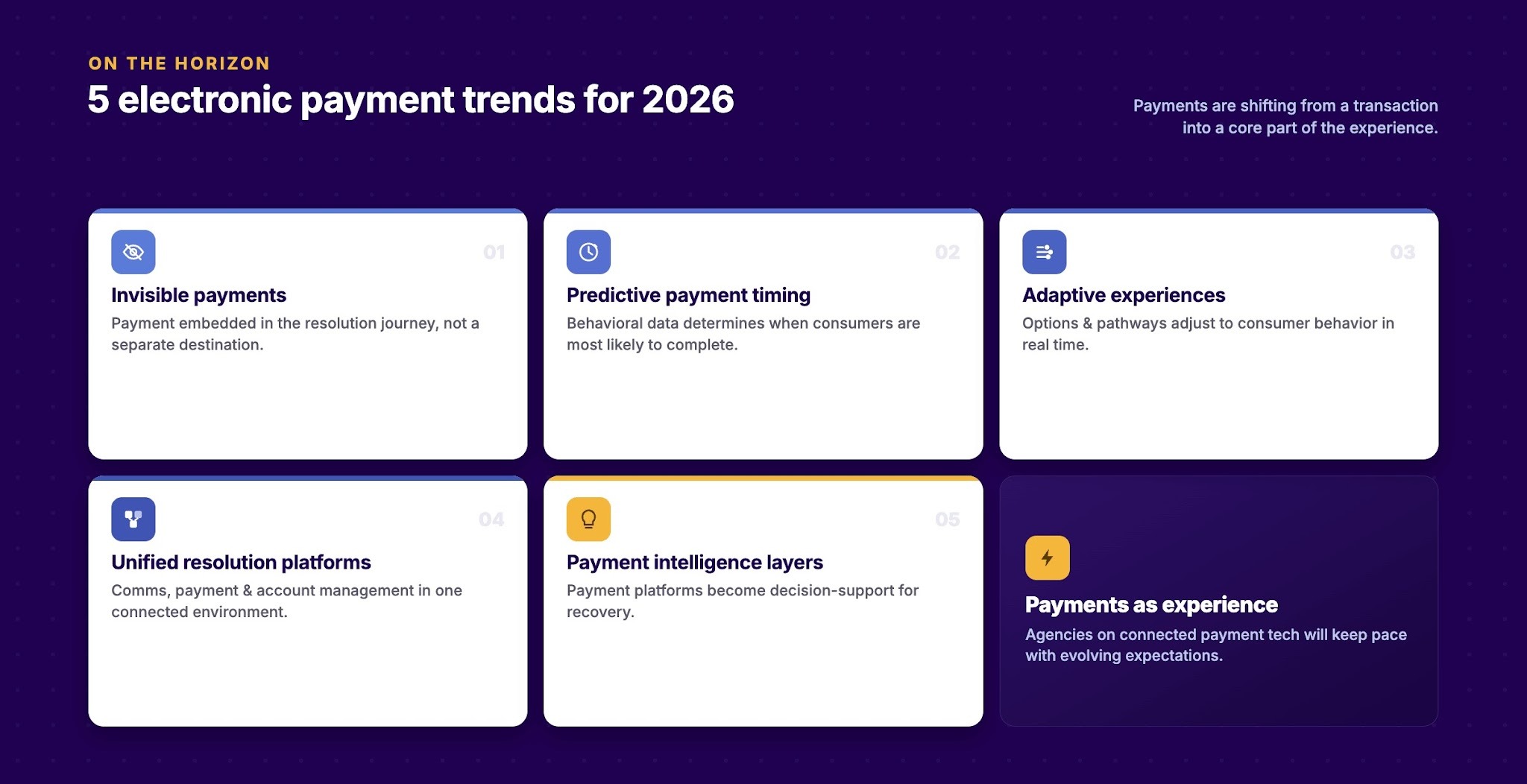

Electronic payments are evolving from a transaction mechanism into a core component of the consumer experience. According to the World Bank, digital payment adoption continues to reshape how consumers manage financial obligations, access services, and interact with financial institutions.

Key trends to watch include:

Payment trends are changing faster than many collection processes. Agencies that rely on disconnected payment systems may struggle to keep pace with evolving consumer expectations. The right debt collection software can help agencies modernize payment operations while creating a more scalable and consumer-centric recovery experience.

Agencies that continue relying on fragmented payment systems, limited payment options, and disconnected consumer experiences may face increasing payment friction, operational inefficiencies, and missed recovery opportunities. As consumer expectations continue to evolve, outdated payment processes can make it harder to convert engagement into completed payments.

Tratta helps agencies create payment experiences that are accessible, flexible, and available across multiple consumer touchpoints. By reducing payment friction, agencies can better align recovery strategies with modern consumer expectations.

Modern payment strategies require more than accepting payments online. They require technology that supports the entire resolution journey. Schedule a demo to see how we can help your agency advance its electronic payment transformation strategy.

Electronic payments refer to any payment processed electronically, including ACH transfers, card payments, and wire transfers. Digital payments are a broader category that includes mobile wallets, app-based payments, and other digital payment experiences.

Yes. Many modern payment platforms allow consumers to accept settlement offers, make settlement payments, and manage settlement arrangements through digital channels.

Preferences vary by consumer segment, but ACH payments, debit cards, credit cards, digital wallets, and recurring payment arrangements are among the most commonly used options.

Electronic payment systems can reduce manual payment processing, administrative workload, paper-based processes, and payment handling costs while improving operational efficiency.

Important metrics include payment completion rate, payment abandonment rate, payment plan success rate, average payment value, settlement conversion rate, and cost-to-collect.