Recovery rates for third-party collections average 19% of placed debt. For debts past 180 days, that number drops to 11%. The gap between those figures is where operational decisions, including the payment collection system an agency uses, determine outcomes.

Consider a mid-sized collection agency running 40,000 active accounts. Agents spend hours manually following up on accounts that consumers never respond to by phone. Payment plans are set up over the phone, documented inconsistently, and occasionally missed due to scheduling errors. The agency collects, but it leaves recoverable dollars behind every month.

That scenario is not a technology problem in isolation. It is a workflow problem that the right payment collection system solves by design. This article covers what such a system actually does, where manual processes break down, and what collection professionals should evaluate before selecting one.

Five things you will take away from this article:

A payment collection system is software that manages the end-to-end process of recovering consumer debt, from initial account intake through payment confirmation and reporting. It connects to a collection agency's existing case management and financial systems, tracks account status in real time, and automates interactions that would otherwise require agent intervention.

For third-party collection agencies and law firms handling debt recovery, the system sits at the operational core of daily workflow. It determines which accounts get touched, when, through what channel, and at what cost.

The key components of a functioning payment collection system include:

Suggested Read: Effortless Payment Collection with Automated Software Solutions

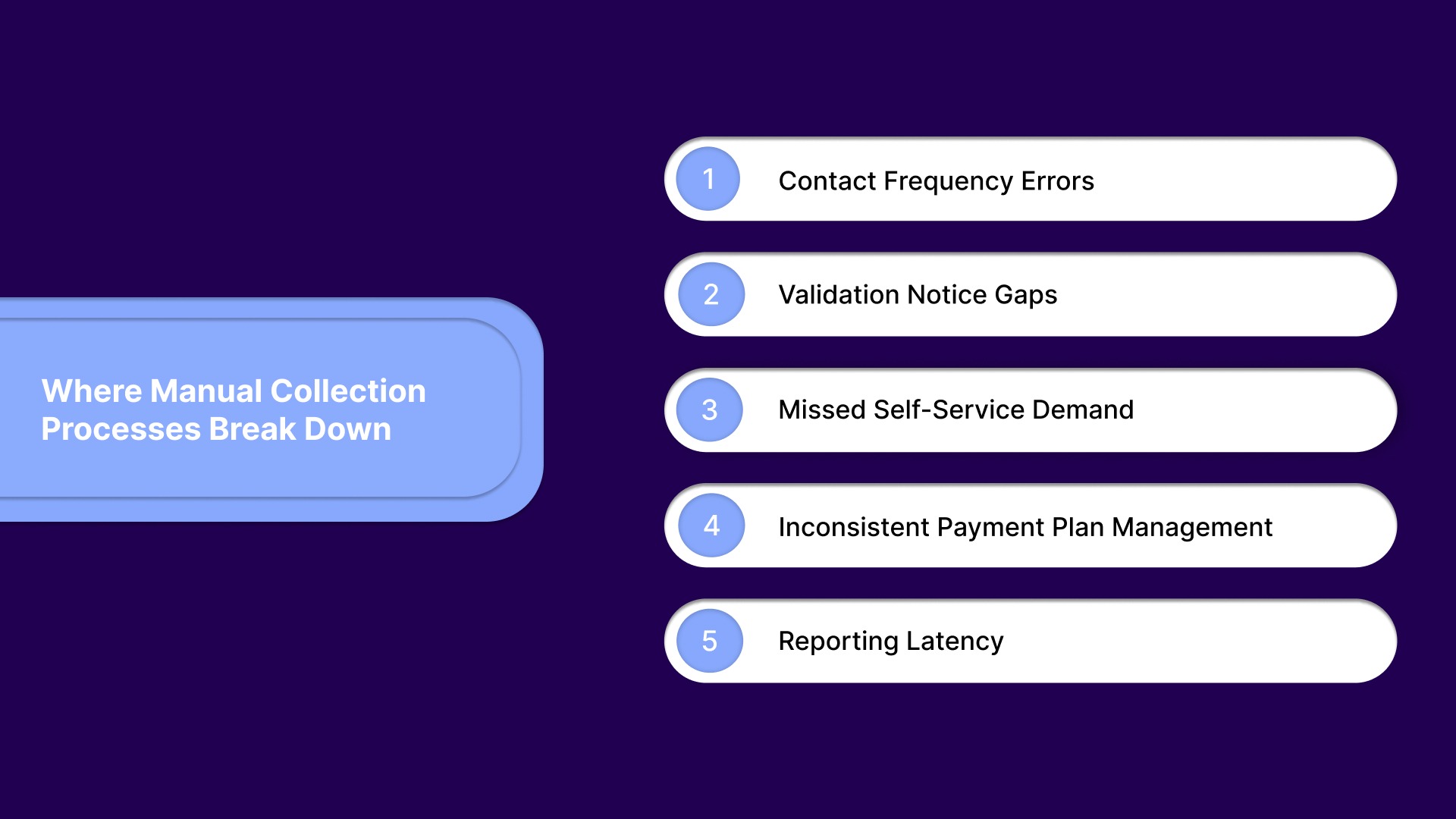

Manual debt collection is not merely inefficient. It creates specific failure points that erode recovery rates and generate compliance exposure. Understanding where those breaks occur is the first step toward evaluating what a payment collection platform must address.

Regulation F limits collectors to 7 call attempts within 7 consecutive days per account. Without a system that automatically tracks and enforces that cap, agents working on high-volume portfolios will exceed it. Each violation carries potential FDCPA liability of up to $1,000 per incident, plus attorney fees.

Manual tracking on spreadsheets or within a basic CRM does not provide real-time enforcement. The risk compounds when accounts are shared across multiple agents or when portfolios are large enough that no single agent has full visibility.

Under Regulation F, a debt collector must send a validation notice within five days of first communication. The notice must include itemized debt information, creditor details, and consumer dispute options. Manually generating and tracking those notices across thousands of accounts creates both operational overhead and compliance risk.

A 2025 CFPB Annual Report on FDCPA highlighted that failure to provide required validation notices was among the most common examination findings reported. Manual processes remain a contributing factor.

Agencies running manual or phone-first collection strategies are structurally inaccessible to the self-service preferring consumer segment. They do not lose those accounts through poor negotiation. They lose them through friction.

A consumer who wants to pay at 10 PM on a Saturday is not going to call and leave a voicemail. Without a self-service payment portal, the intent to pay converts to nothing.

When payment plans are negotiated by phone and logged manually, plan terms vary. Reminder schedules are unreliable. When a consumer misses a payment, the follow-up depends on whether an agent notices the lapse.

An automated payment collection system eliminates that dependency. Payment plans run on configured schedules, reminders fire automatically, and failed payments trigger defined escalation paths.

Manual collection operations produce reports that are hours or days behind the current status. Supervisors cannot make real-time decisions about portfolio prioritization, agent assignment, or campaign adjustments. They react to outcomes they cannot change instead of redirecting effort toward accounts still within the recovery window.

When these gaps compound across a large portfolio, teams typically move toward a platform that handles both compliance enforcement and consumer self-service. Tratta is built for exactly that. Request a demo to see how it works in practice.

The right debt collection payment platform for a collection agency is not the one with the longest feature list. It is the one whose architecture fits the agency's portfolio type, client base, and compliance environment.

The following evaluation framework reflects what experienced collection professionals actually examine.

The consumer-facing portal is where recovery either happens or stalls. Evaluate the following specifically:

Compliance must be embedded in the system's logic, not treated as a configuration layer that operators maintain manually. Evaluate:

Every agency's collection strategy differs by client vertical, debt type, and regulatory jurisdiction. A payment collection platform should support custom workflows without requiring developer intervention. Specifically:

A payment collection system that does not integrate with the agency's existing case management platform creates data duplication and reconciliation overhead. Before selecting a platform, verify:

Collection supervisors and agency principals need visibility into recovery trends, agent productivity, and campaign performance. Evaluate whether the reporting layer provides:

Once these capabilities are defined, the next question is how much operational difference they create compared with a traditional agent-led collection process.

Also Read: Overview of Debt Management and Collections System

The table below reflects where the two approaches diverge on metrics that directly affect recovery outcomes and compliance exposure.

Manual collection creates friction at every step. Build a Smarter Recovery Workflow with Tratta to simplify payments, automate follow-ups, and help more accounts move from outreach to resolution.

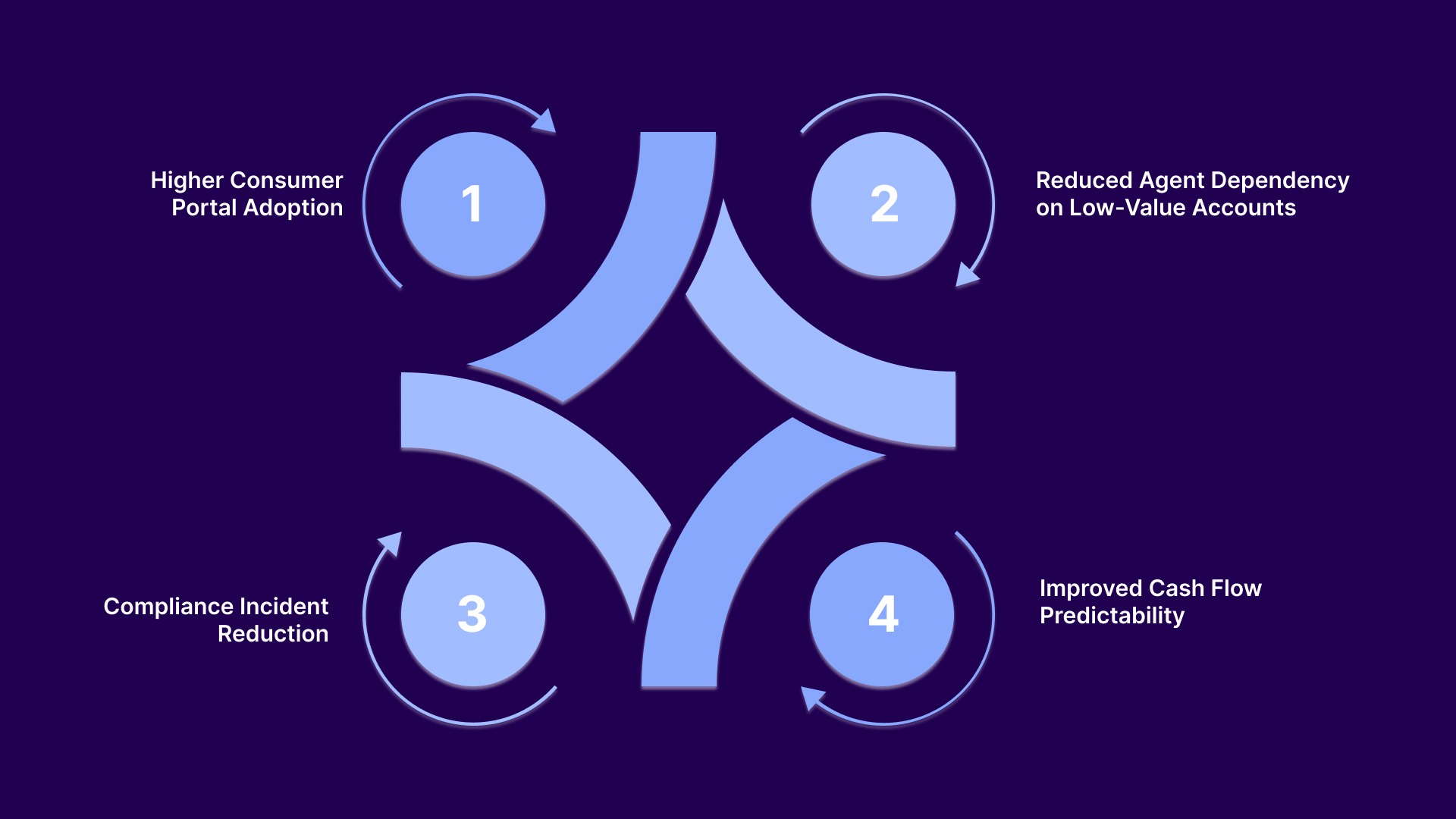

For collection agencies, improved recovery is not just “more payments.” It shows up in lower DSO, higher liquidation rates, stronger promise-to-pay kept rates, fewer broken arrangements, and lower cost per dollar collected.

Consumer portals streamline collections by giving consumers easy access to pay on their terms, which can significantly increase self-service payment volumes.

For example, InDebted, a leading collections agency, saw a 1,861% increase in self-service payment volume after adopting Tratta. This automation not only reduced agent workload but also boosted recovery rates.

Low-balance or low-complexity accounts should not consume the same agent time as disputed, high-balance, or legal-ready accounts. Automated workflows route routine payments and payment plans to self-service channels, helping agencies improve collections per agent, reduce cost per account worked, and protect agent capacity for accounts that need human intervention.

Manual processes increase the risk of missed suppression rules, incomplete consent records, contact-frequency errors, and weak audit trails. A system with built-in controls helps reduce complaint volume, documentation gaps, and audit response time by keeping payment activity, consumer interactions, and workflow decisions logged in one place.

When payment plans are tracked manually, broken arrangements are often caught too late. Automated reminders, failed-payment workflows, and real-time plan tracking help agencies monitor payment plan completion rate, promise-to-pay kept rate, failed payment rate, and average days to payment.

Collection agencies today need more than just a payment collection system, they require an integrated solution that improves efficiency, ensures compliance, and drives higher recovery rates. Tratta offers exactly that, enabling agencies to automate workflows and deliver a seamless self-service experience to consumers.

Tratta’s self-service portal allows consumers to view balances, set up payment plans, and make payments without agent involvement. This reduces agent workload and increases payment conversion rates, especially for after-hours payments.

Tratta automates reminders, follow-ups, and payment plan management based on pre-configured rules. This ensures timely payment processing, reduces missed opportunities, and increases recovery rates.

With compliance built into its foundation, Tratta proactively enforces Regulation F contact limits, delivers validation notices within the required five-day window, and maintains audit-ready records. Agencies can confidently reduce compliance risks and protect their reputation.

Tratta provides real-time dashboards that track key metrics, including recovery rates, payment plan completions, consumer engagement, and agent productivity. This allows agencies to make data-driven decisions and optimize operations.

The platform supports email, SMS, IVR, and chat, allowing agencies to engage with consumers through their preferred channels. This omnichannel approach enhances engagement and improves the likelihood of timely payments.

Tratta’s workflows can be customized based on account age, balance, debt type, or consumer behavior, ensuring that collection strategies align with each agency’s needs. It also supports configurable settlement offers and suppression rules for accounts under dispute or in litigation.

Tratta supports multiple payment methods, including ACH, credit/debit cards, and recurring payments. Integration with case management platforms ensures seamless payment reconciliation and real-time updates.

Consumers have access to payment options anytime, thanks to Tratta’s mobile-optimized portal and IVR system, enabling after-hours payments without the need for agent involvement.

A payment collection system that cannot enforce compliance automatically, lacks consumer self-service, and fails to deliver supervisors real-time visibility is not an upgrade; it's an urgent liability demanding attention. Continuing with manual processes risks compounding operational inefficiencies.

Agencies facing scaling challenges, shrinking margins, and rising compliance risks cannot afford delay. Manual fixes will not quickly close operational gaps; the platform decision is urgent. Choose a system now that aligns structurally with professional debt recovery workflow before it’s too late.

If your current process leaves recoverable accounts unworked and compliance documentation inconsistent, the operational case for change is already there. To see how Tratta's debt collection payment platform addresses both challenges, schedule a demo today and discover if it matches your portfolio needs.

Accounts receivable software typically manages invoicing and payment tracking for businesses collecting first-party revenue. A payment collection system is specifically designed for delinquent consumer debt recovery, with compliance controls, consumer-facing resolution tools, and workflow automation suited to third-party collection environments.

A well-built system enforces Regulation F contact frequency limits automatically, logs all consumer communications with timestamps, triggers validation notices within the required five-day window, and maintains audit-ready records for the required three-year retention period. Manual tracking cannot replicate that at volume.

Yes. Modern debt collection payment platforms allow consumers to view their balance, select a payment plan frequency, and schedule recurring payments without any agent involvement. Plan terms are configured by the agency within the platform, and the system handles all reminders and failed-payment escalation automatically.

At minimum: ACH bank transfers, debit card, and credit card. Recurring payment scheduling is essential for payment plan management. The platform should also support tokenized payment storage for consumers who authorize future charges, reducing friction on repeat interactions.

Implementation timelines vary by platform and portfolio complexity. Agencies should expect 30 to 90 days from contract to active deployment for modern SaaS-based systems with REST API integrations. Platforms requiring extensive custom development or on-premise configuration typically take significantly longer and create more operational disruption.

A modern system increases recovery rates by automating follow-ups, enabling 24/7 self-service payments, and prioritizing accounts based on likelihood of repayment. It reduces missed opportunities caused by delayed outreach, inconsistent agent activity, and abandoned payment intent outside business hours.

At minimum, the platform should support PCI-DSS compliance for payment processing, encryption of sensitive consumer data both in transit and at rest, role-based access controls, and detailed audit logs. These safeguards help protect financial data and reduce regulatory and reputational risk.

Yes. Enterprise-grade platforms are designed for multi-tenant portfolio management, allowing agencies to separate creditor clients, apply different workflows, and maintain distinct reporting structures. This ensures compliance rules and settlement strategies can vary by client without cross-contamination of data.

Advanced systems use predictive models to segment accounts based on repayment probability, optimal contact timing, and channel responsiveness. This helps agencies prioritize high-value actions, reduce unnecessary outreach, and improve overall efficiency without increasing agent workload.

Integration is critical. Without seamless data sync between the payment collection system and case management platform, agencies face duplication errors, delayed updates, and reporting inconsistencies. Strong API integration ensures real-time accuracy across all operational workflows.