It is Monday morning. You are the COO or operations lead at a collection agency. Recovery numbers are down from last week, and you have three dashboards open, trying to figure out why. One shows portal activity. Another has SMS campaign data. A third is a call center export from Friday. You spend 45 minutes reconciling them before you can even form a hypothesis.

That is the real cost of siloed reporting in an omnichannel operation. It creates decision delays that compound over time, making it harder for teams to respond quickly to performance changes.

This post covers what a useful omnichannel debt collection analytics dashboard should surface, channel by channel, and what it takes to make that data practical for running your agency.

An omnichannel analytics dashboard is a centralized view of how every outreach and payment channel is performing. It should show both aggregate performance and channel-level data across SMS, email, IVR, self-service portals, and agent-assisted touchpoints.

The critical word is "connected". In this context, omnichannel means the channels are coordinated, so consumer behavior in one channel is visible alongside behavior in every other. A consumer who opens your SMS, visits the portal, abandons the payment flow, and then receives a follow-up email is one consumer journey. A true omnichannel dashboard shows that journey as one record, instead of scattering it across separate systems.

Standard account-level reporting tells you balances, statuses, and payment histories. That is necessary when you are managing accounts, but it does not explain how multi-channel outreach is influencing recovery outcomes.

Omnichannel analytics answers a different set of questions. Which channel is generating portal visits? Are email campaigns producing payment completions or only clicks? When a consumer receives an SMS but does not respond, does a follow-up call change the outcome? These are operational questions. Without channel-level data tied to payment outcomes, you cannot answer them reliably.

Also read: Understanding Digital Debt Collection: Process & Benefits

Most collection agencies running multi-channel operations manage reporting across several sources. Payment portal data lives in one system. SMS campaign performance comes from a separate export. IVR logs may sit in another tool. Call center metrics often come from a different platform.

Answering basic operational questions then becomes a manual reconciliation process. That process is slow, error-prone, and often incomplete because not every data source updates on the same schedule or uses the same account identifiers.

The first is misallocated outreach spend. Without knowing which channel or channel sequence drove a payment, your agency cannot shift budget or adjust campaign timing intelligently. You may be investing more in email because it shows high click rates, while the actual payment completion happens after a subsequent IVR call. Without connected reporting, that relationship is difficult to see.

The second is weaker audit and dispute readiness. When a consumer disputes an account or a client requests communication records, your team needs a clean log of what was sent, through which channel, and when. If that log requires manual assembly across several systems, the review process becomes slower and more dependent on manual work.

This is about having better control over your own records, so agency staff can review communication and payment activity with less friction.

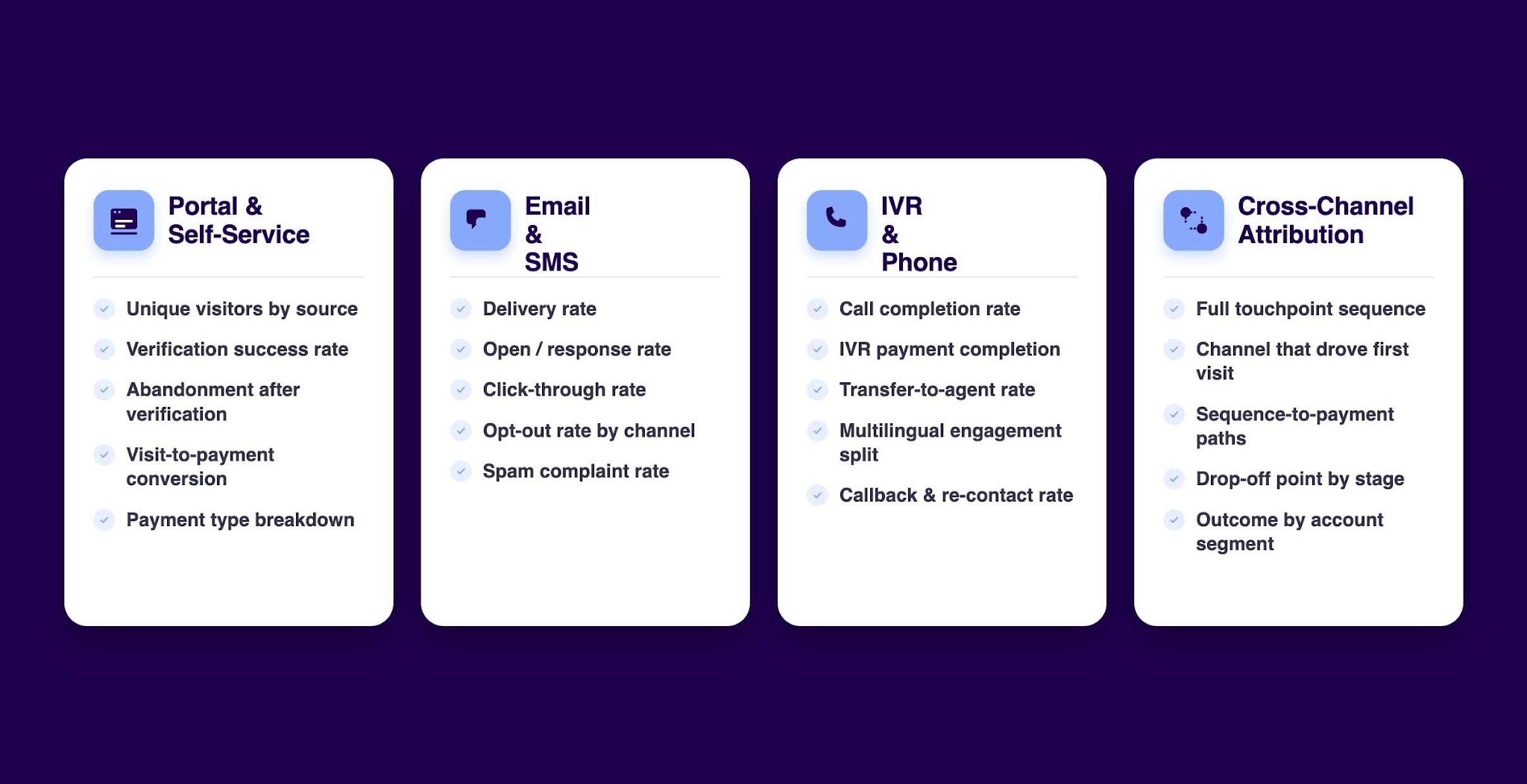

Below is a channel-by-channel breakdown of what your dashboard needs to track and why each data point matters operationally.

The self-service portal often signals high-intent behavior because consumers who visit it are actively engaging. But engagement does not always become payment, and your dashboard should show where the drop-off happens.

Track these metrics for your portal:

A high abandonment rate after verification may point to friction in the payment flow rather than a consumer engagement problem. A spike in plan selections may indicate that your current plan terms need adjustment for certain account segments. Tratta reports a 96% guest verification success rate for its consumer portal, which gives agencies a useful reference point when evaluating their own payment flow.

Email and SMS often create the first digital touchpoint. Your dashboard should separate them clearly instead of combining them into a single outreach report.

Google’s email sender guidelines recommend keeping spam rates reported in Postmaster Tools below 0.10% and avoiding a spam rate of 0.30% or higher. That makes spam complaint monitoring useful when email is part of your outreach mix.

A high opt-out rate in one channel does not automatically mean a consumer is disengaged. It may mean that the channel is not preferred. Your dashboard should track opt-outs by channel so your team can adjust outreach without over-communicating across all touchpoints.

IVR handles consumers who may not engage digitally. Its performance data tells you something different from portal or email numbers, and it has direct resourcing implications.

Track these for your IVR channel:

A high transfer-to-agent rate from IVR is a meaningful signal. It may indicate that certain account types, balance ranges, or consumer segments need a human agent. That is a staffing and queue-management insight, not only a call center metric.

If your IVR supports multiple languages, engagement split can also help you understand parts of your consumer base that may need different outreach or payment support. Tratta’s multilingual payment IVR supports payment experiences across multiple languages.

This is the layer that many collection agency reports miss, and it is often the most operationally valuable.

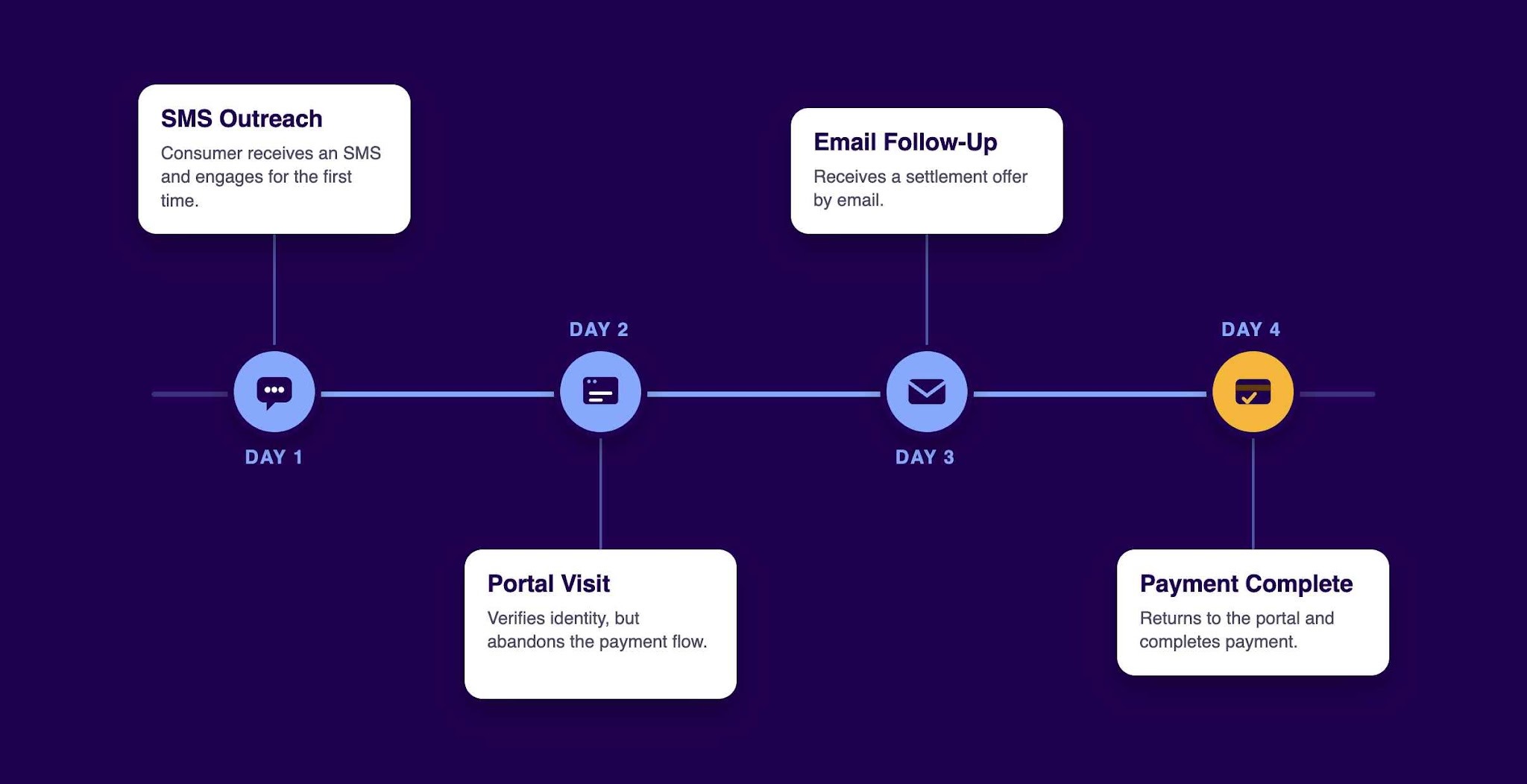

Cross-channel attribution means your dashboard can show the full sequence of consumer touchpoints before a payment, not only the channel where the payment happened. A complete journey might look like this:

Without attribution, your email campaign may get credit for the payment. With attribution, you can see that the SMS drove initial intent, the portal abandonment revealed a friction point, and the settlement email helped bring the consumer back. Those are three different operational insights.

This data helps your ops team in two ways. First, you can identify which channel sequences produce stronger recovery outcomes for specific account segments. Second, you can see where in the consumer journey drop-offs happen, which helps determine whether the issue is outreach strategy or payment-flow friction.

Also read: 5 Online Payment Solutions for Third-Party Collection Agencies

Once the right metrics are available, the next question is whether the dashboard helps teams act on them quickly. For collection operations, dashboard design matters because managers often need to move from a high-level performance dip to a specific campaign, segment, or channel issue without building a custom report.

When reporting updates after a campaign has already moved forward, teams are forced to react late. In an omnichannel environment, that delay can make campaign decisions harder.

Consider this scenario: your team sends 10,000 SMS messages on Monday morning. By Tuesday, you need to know whether the click-through rate justifies the follow-up email scheduled for Wednesday or whether you should adjust the offer. If your reporting updates too late, the decision window closes before your team has the full picture.

Real-time or near-real-time reporting enables your ops team to:

A dashboard that is visually dense is not automatically useful. The structural features that matter are the ones that help teams move from a high-level issue to a specific campaign, segment, or channel.

Looking for real-time visibility across every channel? Explore Tratta’s Reporting and Analytics to see how campaign performance, payment outcomes, and consumer engagement can be reviewed from one dashboard.

A dashboard has limited value if insights stay in reports. Its real value comes from helping teams adjust outreach timing, payment-path design, agent follow-up, and campaign sequencing before the same issue repeats across more accounts.

A unified analytics dashboard is most useful when it helps teams decide what to do next, not just review past performance.

Here is a concrete example. Your data shows that SMS drives portal visits for a specific account segment, but payment completion improves when an email with payment-plan information follows within a short window. That means the outreach workflow for that segment should reflect a specific sequence: SMS first, then a relevant email follow-up.

Translating that insight into a live campaign workflow requires analytics and campaign tools to operate from the same data. If they live in separate systems, the insight stays in a spreadsheet instead of becoming an actionable workflow adjustment.

Any analytics dashboard worth using should make it easy to identify where consumers stop engaging. For collection agencies running omnichannel outreach, two drop-off points matter most:

These two problems require different responses. More outreach volume will not fix a broken payment flow. A better payment flow will not fix a message that fails to bring consumers to the portal. You need the data to know which issue you are dealing with.

Also read: 8 Ways API-Based Recovery Tracking Can Improve Debt Collection

Not every platform that supports multiple channels also supports unified reporting across them. The functional requirements that determine whether you will get actionable analytics include:

These requirements point toward a platform where payments, outreach, and reporting work together, rather than separate tools sharing data through manual exports or disconnected reports.

One reason platforms such as Tratta are often evaluated for omnichannel analytics is that communications, payments, and reporting are connected within the same environment. When outreach activity and payment outcomes can be viewed together, collection agencies spend less time reconciling data across systems and more time acting on insights.

A genuine omnichannel analytics dashboard gives your collection agency the ability to see how every channel contributes to recovery, where consumers are dropping off, and which outreach sequences are driving payments rather than clicks. Without unified reporting, channel performance stays unclear. With stronger visibility, your ops team can make faster, better-grounded decisions without spending Monday morning reconciling three dashboards.

If you want to see what centralized omnichannel reporting looks like for a collection agency, schedule a demo with Tratta and walk through how the dashboards work for collection agency operations.

Also read: Payment Collection System: What US Agencies Need in 2026

It should track portal engagement, payment completion, email and SMS delivery, opt-out rates by channel, IVR completion, transfer-to-agent rates, and the consumer journey from first outreach to payment.

Standard reporting shows account-level outcomes such as balances, payments, and statuses. Omnichannel analytics shows how outreach channels influence engagement, payment behavior, and drop-off points across the recovery process.

It should connect outreach activity to payment outcomes across the consumer journey. For example, the dashboard should show whether an SMS created the first portal visit, whether an email follow-up brought the consumer back, or whether an IVR interaction led to completion.

A useful dashboard helps teams move from a performance issue to the underlying cause. It should allow drill-down by campaign, segment, channel, payment path, and consumer drop-off point.

Technically yes, but it usually requires manual reconciliation across multiple exports. Without centralized payments, outreach, and reporting, it is harder to maintain a reliable view of how different touchpoints contribute to outcomes.