Are missed payments, fragmented tools, and inefficient workflows slowing down your agency’s recovery efforts?

In Q1 2026, the Federal Reserve Bank of New York reported that 4.8% of outstanding U.S. household debt was in some stage of delinquency, showing how important structured recovery workflows have become for agencies. Managing multiple systems, tracking account activity, and keeping agents on top of outreach can make even the simplest collection process harder to control.

This blog explores the step-by-step collection process every agency should know, with practical ways to improve workflows, support recoveries, and maintain better visibility across operations.

The collection process is a structured workflow that agencies follow to recover overdue balances on behalf of creditors. It includes stages such as account intake, outreach, follow-up, escalation, and resolution, all designed to maximize recoveries while maintaining operational control and compliance.

For agency leaders like owners, COOs, and operations heads, understanding this process is critical to improving agent efficiency, scaling outreach, and gaining clear visibility into account performance. It also helps compliance, IT, and payment operations teams align systems and workflows to support consistent, measurable results.

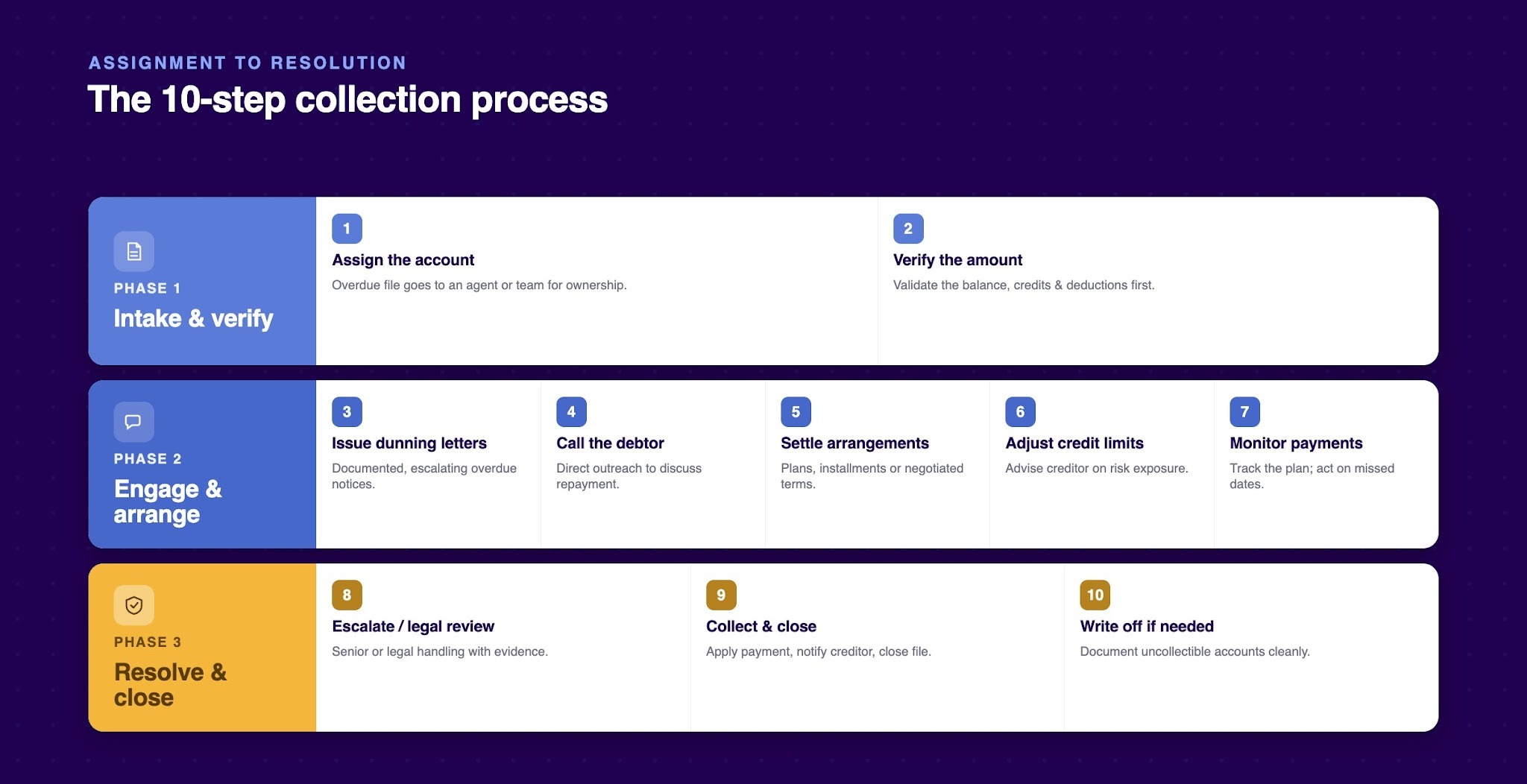

Once the process is defined, the next step is to look at how agencies move an overdue account from assignment to resolution.

Also Read: 6 Consumer-Centric Collection Tools Every Agency Should Use in 2026

The debt collections process includes the key stages agencies follow to recover overdue balances. Each step requires careful coordination between collection agents, internal teams, and sometimes external stakeholders to maximize recovery and minimize disputes.

Here are the key steps every collection agency should understand:

Once a debtor’s account becomes overdue, it is assigned to a specific collection professional or team. This step ensures accountability and enables agencies to track the progress of each account.

Assigning ownership also helps prioritize accounts by age, balance size, or risk profile, allowing agencies to focus their efforts where they can achieve the highest recovery rates.

Before contacting a debtor, it is essential to validate the outstanding balance. This involves reviewing invoices for discrepancies and accounting for deductions and previously applied credits.

Accurate verification protects creditors from disputes and supports transparent communication, enhancing trust with debtors and reducing the likelihood of contested claims.

Dunning letters serve as formal, documented notifications to the debtor that payment is overdue. Agencies often send these at set intervals, with each letter escalating the urgency of repayment.

While letters were traditionally mailed via the postal service, many agencies now complement letters with email notifications to ensure timely delivery and a documented audit trail. Properly structured dunning letters also help agencies comply with federal and state debt collection regulations.

Personalized phone outreach allows collection agents to engage directly with the debtor, understand reasons for non-payment, and present repayment options. Effective calls combine professionalism with empathy—agencies must balance the need for recovery with maintaining a respectful relationship.

But what happens when debtors prefer another communication channel?

This is where Tratta’s Omnichannel Communications can support the collection process. Tratta helps agencies reach debtors across email, SMS, chat, phone, bilingual IVR, and QR-code letters, while also supporting channel-specific routing, branded templates, and campaign tracking. This gives agencies more ways to reach debtors while keeping outreach more organized and easier to measure.

For many debtors, a one-time payment may not be feasible. Agencies work with debtors to create structured repayment plans, which can include installment schedules, extended deadlines, or negotiated settlements.

Flexible arrangements increase the likelihood of recovering funds while reducing friction in debtor interactions. Agencies also need to monitor these agreements closely to prevent missed payments.

If a debtor continues to engage but exhibits a pattern of late payments, agencies may advise creditors to adjust credit limits according to the debtor’s risk profile. This proactive step mitigates future exposure and helps maintain a healthy portfolio.

Agencies often coordinate with the creditor’s finance or credit team to ensure adjustments align with overall credit policy.

Active monitoring is critical once a repayment plan is in place. Collection agencies track scheduled payments and intervene promptly if a debtor misses a deadline.

Monitoring includes sending reminders, adjusting payment schedules when necessary, and updating records to maintain full transparency for creditors. This vigilance helps prevent accounts from falling back into delinquency.

When regular outreach and payment reminders do not result in resolution, the agency may move the account to a higher-priority workflow. This can include senior agent review, supervisor approval, additional documentation checks, or legal review where appropriate.

This step involves preparing evidence of outreach, settlement attempts, and communications, which are essential for supporting the creditor’s case in court. Agencies coordinate with legal teams to ensure actions comply with regulations, balancing the need for recovery with risk management.

When the debtor completes the payment, settlement, or court-approved repayment arrangement, the agency updates the account status and records the resolution. This step includes confirming the received amount, applying it to the correct account, notifying the creditor, and closing the recovery workflow.

For agencies, accurate closeout is important because it supports reporting, prevents duplicate outreach, and gives creditors a clear view of recovery performance.

If all collection efforts fail and no practical recovery path remains, the creditor may decide to write off the remaining balance as bad debt. For collection agencies, this does not simply mean ending the file.

The agency should document the steps taken, record why the account was closed as uncollectible, and provide the creditor with a clear final status for accounting and reporting purposes.

As agencies manage outreach, payment discussions, and account documentation, they also need to understand the Fair Debt Collection Practices.

The Fair Debt Collection Practices Act, or FDCPA, is a federal law that limits what third-party debt collectors can do when collecting certain types of debt. For collection agencies, it sets important boundaries around debtor communication, payment discussions, dispute handling, and the use of fair, non-deceptive collection practices.

For collection agencies, FDCPA-aware workflows usually affect:

Beyond recovery outcomes, agencies also need to understand the cost of managing each account.

The cost of collections is the total expense a collection agency spends to recover overdue balances for creditors. It includes agent time, communication costs, payment processing, technology, compliance oversight, reporting, and any escalation or legal support needed to move an account toward resolution.

Here are the main factors that affect the cost of collections:

Next, agencies can identify practical ways to make the process more consistent and easier to manage.

A better collection process helps agencies recover overdue balances with more control, clearer reporting, and less manual work. For agency owners, COOs, and operations leaders, the goal is to make every outreach, payment, and follow-up easier to track and manage.

Here are the tips debt collection agencies can use to improve their collection process:

Not every debtor account needs the same level of attention. Agencies should group accounts by balance size, days past due, payment history, and risk level. This helps agents focus on the accounts that need immediate action instead of treating every file the same way.

A defined workflow helps agents know when to send reminders, make calls, offer payment plans, or escalate an account. It also gives managers better control over daily operations. When each step is documented, agencies can reduce confusion and maintain more consistent communication with debtors.

Agencies need visibility into how debtors respond to reminders, payment links, IVR prompts, and repayment options. Reporting helps leaders see which accounts are active, inactive, or at risk of delay. These insights can guide better follow-up decisions and improve campaign performance.

Disconnected tools make it harder to confirm payments, update balances, and report results to creditors. Agencies should aim to integrate payment activity with account records into a single workflow. This gives payment operations and reporting teams a clearer view of recovery progress.

Every call, notice, payment arrangement, dispute, and account update should be recorded clearly. Strong documentation supports compliance reviews and helps agencies answer creditor questions with confidence. It also protects agents from repeating work or contacting debtors without a full account context.

Agency leaders should track metrics such as recovery rate, cost per collection, payment plan completion, agent productivity, and self-service adoption. These numbers show where the process is working and where it needs attention. Regular reviews help teams improve decisions instead of relying on guesswork.

For agencies seeking better control over payments, reporting, debtor communication, and workflows, the right technology can support a more connected collection process.

Also Read: Average Collection Period Calculator

Many collection agencies struggle when payments, debtor communication, reporting, and account updates are managed across separate tools. This can slow agents down, create reporting gaps, and make it harder for leaders to track recovery performance.

Tratta is debt collection software that helps agencies manage payments, digital communications, reporting, integrations, and compliance-aware recovery workflows on a single platform. It supports the collection process by helping agencies reduce manual work, improve visibility, and give debtors easier self-service payment options.

Key Tratta features that support this include:

Tratta’s self-service platform allows consumers to view balances, review payment history, upload documents, dispute debts, and access payment options on their own.

This can help agencies reduce routine agent interactions while giving debtors a clearer path to resolve accounts.

Tratta provides real-time collection analytics, dashboards, and customizable reports that track activity across the collection journey.

Agencies can see clicks, views, payment attempts, settlement engagement, and other account-level signals that help leaders understand what is working.

Collection agencies do not all follow the same policies, account strategies, or debtor communication rules.

Tratta is built to support configurable policies, messaging, workflows, and consumer experiences based on business rules.

Our REST API and integrations help connect payment data, account updates, and communication records across systems.

This supports cleaner data flow for IT teams and gives agents a more complete account context during the collection process.

Our multilingual payment IVR supports English and Spanish, allowing debtors to interact and make payments in their preferred language. It also gives agencies visibility into IVR activity, including calls, payments, transfers, and portal activity.

For agency owners, Tratta is designed to support a more controlled collection process. It helps centralize key workflows, improve visibility, reduce manual friction, and support a better self-service payment experience for debtors without removing the agency’s oversight.

A strong collection process gives debt collection agencies a clear path to manage overdue accounts from assignment through resolution. It helps teams verify balances, contact debtors, manage payment arrangements, document activity, and decide when escalation or write-off is needed. For agency owners and COOs, the right process also improves agent efficiency, reporting visibility, and control across every stage of recovery.

Tratta supports this process by helping agencies bring payments, digital communication, reporting, integrations, and compliance-aware workflows into one platform. With features such as consumer self-service, reporting and analytics, REST APIs, embedded payments, and multilingual payment IVR, Tratta helps agencies improve visibility and give debtors easier ways to move toward payment.

If your agency is ready to manage the collection process with clearer workflows and better payment visibility, schedule your demo today to see how Tratta supports modern debt recovery operations!

A structured process helps agencies keep recovery work consistent, measurable, and easier to manage. It also gives better visibility into agent activity, account status, payment progress, and creditor reporting.

Agencies can prioritize accounts based on days past due, balance size, debtor response history, payment behavior, and recovery potential. This helps agents focus their time on accounts that need timely action or closer review.

A payment plan may be useful when a debtor cannot pay the full balance at once but shows a willingness to resolve the account. Agencies should document the terms, payment dates, amounts, and any missed-payment follow-up steps.

Technology can help agencies connect payment activity, debtor communication, reporting, and account updates in one workflow. This reduces manual work, improves visibility, and helps teams manage recovery operations with more control.

Agencies can reduce errors by verifying account data before outreach, documenting every interaction, connecting payment and account systems, and using consistent workflows. This helps teams avoid duplicate contact, incorrect balances, missed updates, and reporting gaps.