Debt collection often stalls when consumers avoid calls, ignore mailed notices, or delay responses. Traditional outreach methods create friction, making it harder for agencies to engage consumers and recover balances efficiently. As expectations shift toward digital convenience, many collection strategies struggle to keep up.

The percentage of collection agencies offering self-service payment portals has grown to 88%, highlighting how digital engagement is becoming standard in modern collections. To remain effective, agencies are adopting consumer-centric collection tools that simplify payments, support digital communication, and improve engagement.

This guide explores six consumer-centric collection tools every agency should consider using in 2026 to modernize their debt recovery strategy.

Consumer-centric debt collection focuses on making the repayment process clearer, easier, and less stressful for consumers. Instead of relying on aggressive outreach or rigid payment demands, agencies prioritize transparency, flexible options, and convenient digital access.

The goal is to remove barriers that prevent consumers from resolving their debts while maintaining consistent communication and compliance. Current collection strategies increasingly focus on customer experience because it directly affects engagement and repayment outcomes.

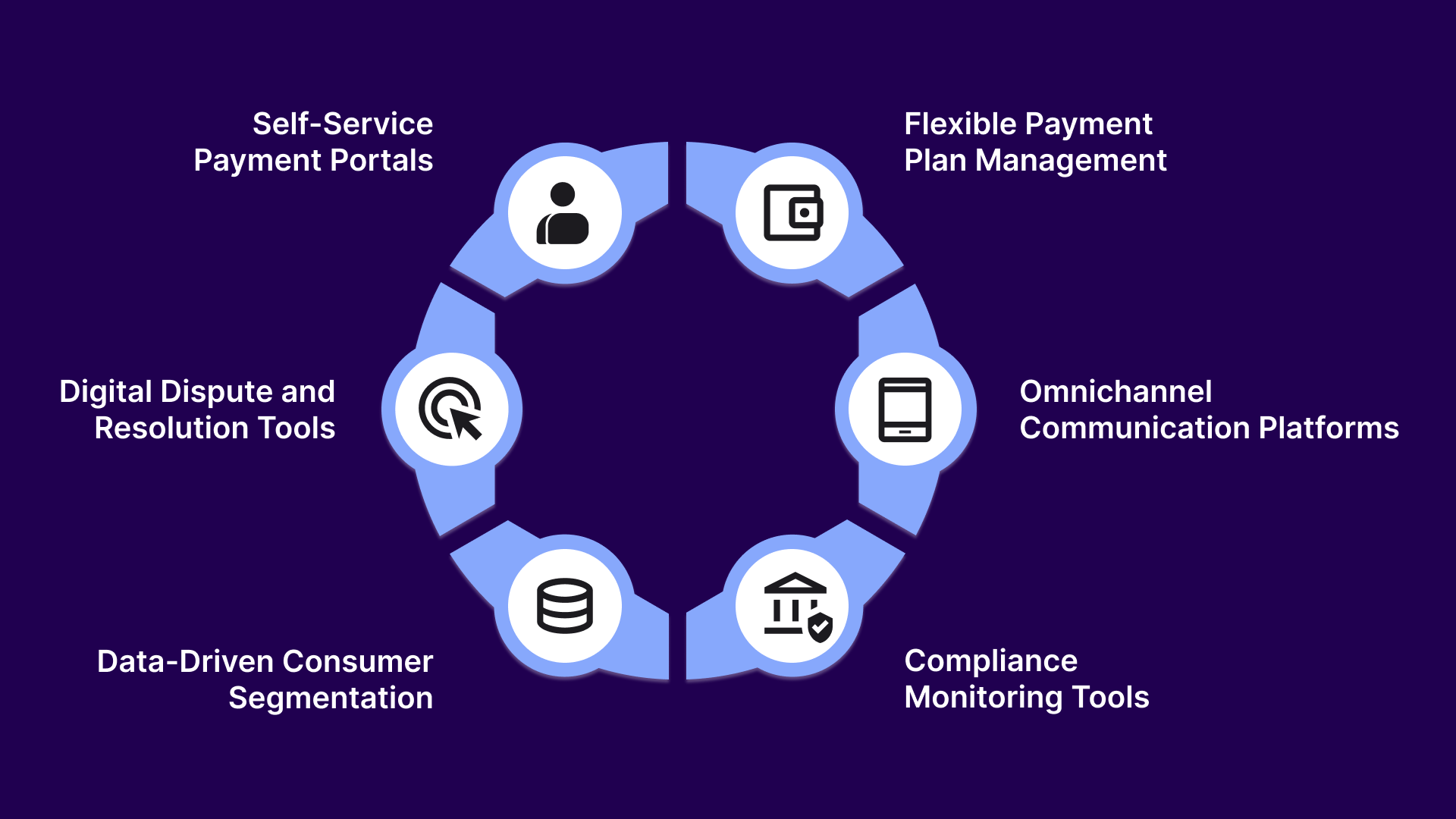

Consumer-centric collections typically include:

Adopting these practices helps agencies improve repayment rates while reducing friction in the collections process. To support this shift, many agencies are investing in consumer-centric collection tools designed to simplify payments, automate communication, and improve overall engagement.

Suggested Read: The Role of Debt Collection Agents: Delivering a Superior Customer Experience

Customer-centric collection tools reduce friction during repayment, making it easier for consumers to respond, communicate, and resolve outstanding balances. When agencies combine digital access, flexible payment options, and compliant communication, recovery efforts often become more efficient.

Below are six tools that help agencies improve engagement and increase repayment outcomes.

Self-service payment portals allow consumers to review balances, choose payment options, and resolve debts without speaking to an agent. These portals give consumers control over when and how they make payments, which can reduce avoidance behavior. Digital payment access also aligns with broader consumer expectations around online financial transactions.

These platforms help agencies improve recovery outcomes in several ways:

Many consumers are willing to repay debt but need structured payment options that fit their financial circumstances. Flexible payment plan tools allow agencies to offer installment schedules, partial payments, or settlement options that make repayment more manageable. These systems also automate plan setup and payment scheduling, reducing administrative effort.

Flexible payment plan systems support recovery by enabling:

Consumers communicate through multiple digital channels, including text messages and email. Omnichannel communication tools allow agencies to reach consumers through the channels they are most likely to respond to. These platforms also help coordinate messaging, keeping communication consistent across touchpoints.

These platforms improve debt recovery by supporting:

Digital debt collection is heavily regulated, and agencies must ensure communication practices follow applicable guidelines. Compliance monitoring tools help track communication timing, required disclosures, and documentation requirements. These systems reduce the risk of regulatory violations while maintaining consistent operational processes.

Debt collection complaints remain a major regulatory concern. In 2025 alone, more than 400,000 Americans filed complaints about debt collection calls, with many describing the calls as harassing or threatening.

Compliance tools help agencies maintain operational control by providing:

Not all consumers respond to the same outreach strategies. Data-driven segmentation tools help agencies categorize accounts based on payment behavior, risk indicators, and engagement patterns. This allows collection teams to tailor communication strategies to different consumer groups.

These tools support better recovery outcomes by enabling:

Consumers sometimes need to verify account details or dispute balances before making a payment. Digital dispute resolution tools allow consumers to submit documentation requests or disputes through secure online channels. Providing structured resolution processes improves transparency and reduces friction.

Debt collection lawsuits account for up to 4.7 million cases filed in U.S. state courts in a single year, making them one of the most common types of civil cases.

These tools support smoother resolution by offering:

Customer-oriented collection tools are becoming essential as agencies adapt to evolving consumer expectations and regulatory requirements.

Tratta helps bring these features together by supporting digital payment options, consumer engagement tools, and automated workflows within a single system. By enabling self-service payments, structured communication, and data visibility, Tratta helps agencies implement a more consumer-focused approach to debt recovery. Schedule a free demo today.

Regulatory scrutiny around debt collection has increased significantly in recent years. Agencies are now expected to provide clearer communication, transparent documentation, and accessible dispute processes for consumers.

Several regulatory requirements now push agencies toward more consumer-centric collection practices.

This federal statute governs how debt collectors communicate with consumers. It prohibits harassment, misleading statements, and unfair collection tactics while requiring clear disclosures and respectful communication.

Implemented by the Consumer Financial Protection Bureau, Regulation F modernizes the FDCPA by establishing rules for electronic communications, validation notices, and consumer contact limits.

Enforced by the Consumer Financial Protection Bureau, this law prohibits unfair, deceptive, or abusive acts and practices (UDAAP) in financial services, including debt collection activities.

This statute allows electronic disclosures and digital documentation, making secure digital communication and payment systems increasingly important for compliance.

Many states have introduced stricter consumer protection laws that regulate communication frequency, documentation standards, and dispute handling procedures. For example, New York’s Debt Collection Regulations (23 NYCRR 1) require collectors to provide clear substantiation of the debt and enhanced validation disclosures when consumers request verification.

Building a consumer-centric digital collections strategy helps agencies meet these regulatory expectations while improving engagement and repayment outcomes. The next section outlines the steps that agencies can take to begin structuring that approach.

Suggested Read: Debt Collection Payment Processing Solutions and Services

By combining technology, clear communication, and structured repayment options, agencies can create a system that meets regulatory requirements and improves recovery outcomes.

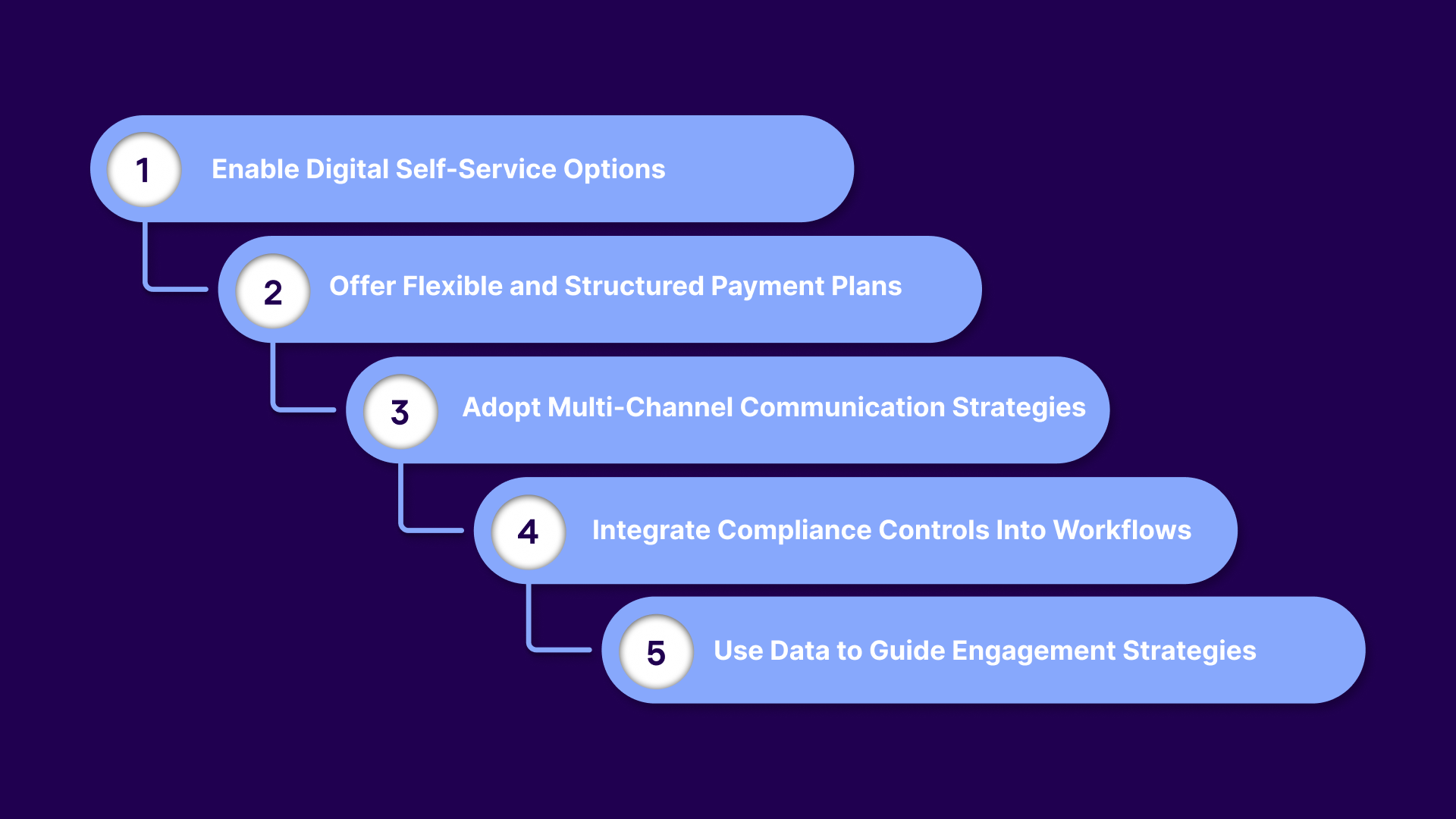

You need to take the following steps:

Consumers increasingly expect the ability to manage financial obligations online. Providing self-service portals allows consumers to review balances, select payment options, and resolve accounts without waiting for agent assistance. This reduces friction in the repayment process and gives consumers more control over how they handle their debts.

Many consumers are willing to repay their debts but need repayment options that fit their financial situation. Agencies should provide installment plans, settlement options, and automated payment scheduling that make repayment more manageable. Structured payment plans also help agencies maintain consistent payment flows and reduce missed installments.

Consumers engage with financial services through a variety of digital channels. Agencies should support communication through email, text messaging, and other compliant digital outreach methods so consumers can respond through their preferred channel. Coordinated communication strategies also help ensure messaging remains clear and consistent.

Regulatory requirements increasingly demand clear documentation, contact limits, and accurate disclosures. Agencies should implement systems that automatically track communications, maintain records, and enforce compliance rules during collection activities. Embedding compliance controls within workflows helps reduce risk and maintain regulatory alignment.

Collection strategies become more effective when agencies understand consumer behavior patterns. Data analytics can help identify payment trends, engagement preferences, and account prioritization opportunities. Using these insights allows agencies to tailor outreach strategies and improve repayment outcomes.

Tratta helps agencies operationalize consumer-centric collections by providing a digital infrastructure for payments, communication, and account management. Its platform enables secure self-service payment portals, structured consumer communication workflows, and flexible repayment options within a single environment. Call us to learn more.

When repayment processes become easier and communication becomes clearer, consumers are more likely to engage and resolve their accounts. This approach can improve recovery performance while reducing operational strain on collection teams.

Operational benefits of investing in consumer-oriented collection tools are:

Agencies must adopt the right digital infrastructure to support consumer engagement, flexible payments, and compliant communication. Choosing the right technology platform can make the difference between fragmented collection efforts and a simplified, consumer-focused recovery strategy.

Suggested Read: Predictions and Trends in the Debt Collection Industry for 2026

Tratta is a digital debt collection platform designed to help agencies upgrade how they engage with consumers and manage repayments. It focuses on improving transparency, digital accessibility, and structured communication throughout the recovery process.

These features can help you support consumer-focused debt collection.

Consumers can access their accounts, review balances, and make payments without speaking with an agent. This allows consumers to resolve accounts privately and at their convenience, which often increases repayment participation. Self-service access also helps reduce call avoidance and supports faster payment resolution.

Tratta enables secure digital payment processing directly within the platform. Consumers can complete transactions quickly through integrated payment methods, improving the payment experience. A streamlined payment process helps remove barriers that commonly delay repayment.

Interactive voice response payment systems allow consumers to resolve accounts through automated phone payments. Multilingual capabilities ensure that consumers can understand payment instructions and account information clearly. This improves accessibility for diverse consumer populations.

Tratta supports coordinated communication across channels such as phone, SMS, and email. This allows agencies to reach consumers through the communication methods they are most comfortable using. Consistent communication improves engagement while maintaining clear documentation of outreach.

Agencies can design targeted outreach campaigns that include payment reminders, settlement opportunities, and follow-up messaging. Campaign tools allow teams to personalize communication based on account activity or payment behavior. Structured outreach helps keep repayment conversations active without overwhelming consumers.

Real-time reporting tools provide visibility into payment activity, campaign performance, and recovery trends. Agencies can use this data to refine outreach strategies and identify accounts that require additional attention. Data-driven insights help teams make more informed operational decisions.

The platform allows agencies to configure payment flows, messaging, and account management workflows. Customization helps agencies align collection processes with internal policies and creditor requirements. It also allows the consumer experience to be tailored to specific portfolios.

Tratta connects with existing collection systems through APIs and secure data transfers. This allows agencies to maintain operational continuity while expanding digital capabilities. Integration support also improves data consistency across platforms.

The platform includes security controls and compliance safeguards that support regulated debt collection operations. Built-in protections help secure consumer data while maintaining audit-ready documentation. Strong security practices also help build consumer trust.

Tratta supports collection teams with tools that help manage consumer interactions and account workflows. Agents can access account details and payment activity while assisting consumers during calls. This helps ensure that conversations remain informed, efficient, and solution-oriented.

Tratta continues to improve as collection practices shift toward digital engagement and consumer transparency. The platform helps agencies create clearer, more accessible repayment experiences for consumers.

Consumer expectations are changing quickly, and collection strategies that fail to adapt can create unnecessary friction. When repayment processes are confusing, communication feels intrusive, or payment options are limited, consumers are more likely to ignore outreach or delay resolving their accounts.

Tratta helps agencies address these challenges by enabling digital payment portals, structured communication workflows, and flexible repayment options designed for advanced debt recovery. The platform supports consumer engagement, secure payments, and operational visibility, enabling agencies to manage accounts more efficiently while maintaining transparency and compliance.

If your agency is looking to optimize its collections approach, consumer-centric tools can make a measurable difference. Get in touch with us today to learn more.

Consumer-centric collections can shorten recovery timelines by making repayment easier and more accessible. When consumers can view balances, choose payment options, and communicate digitally, they are more likely to engage earlier and resolve accounts faster.

Digital documentation helps agencies maintain records of communications, disclosures, and payment activity. This documentation is important for demonstrating compliance with regulations and responding to disputes, audits, or consumer complaints.

Agencies can encourage adoption by including portal links in communication campaigns, providing clear payment instructions, and offering multiple digital payment methods. Making the process simple and accessible often increases participation.

Phone-only collection strategies can reduce engagement because many consumers avoid calls or prefer digital communication. Agencies that rely exclusively on phone outreach may experience lower response rates and slower repayment activity.

Agencies can track metrics such as digital payment adoption, consumer engagement rates, repayment timelines, dispute frequency, and campaign performance. Monitoring these indicators helps teams refine outreach strategies and improve recovery outcomes.