Most collection agencies already have a self-service portal. Most also run some form of SMS outreach. But ask how the two connect, how a text message moves a consumer directly into a branded, authenticated payment experience, and the answer is usually a workaround, not a workflow.

That gap is where recovery leaks.

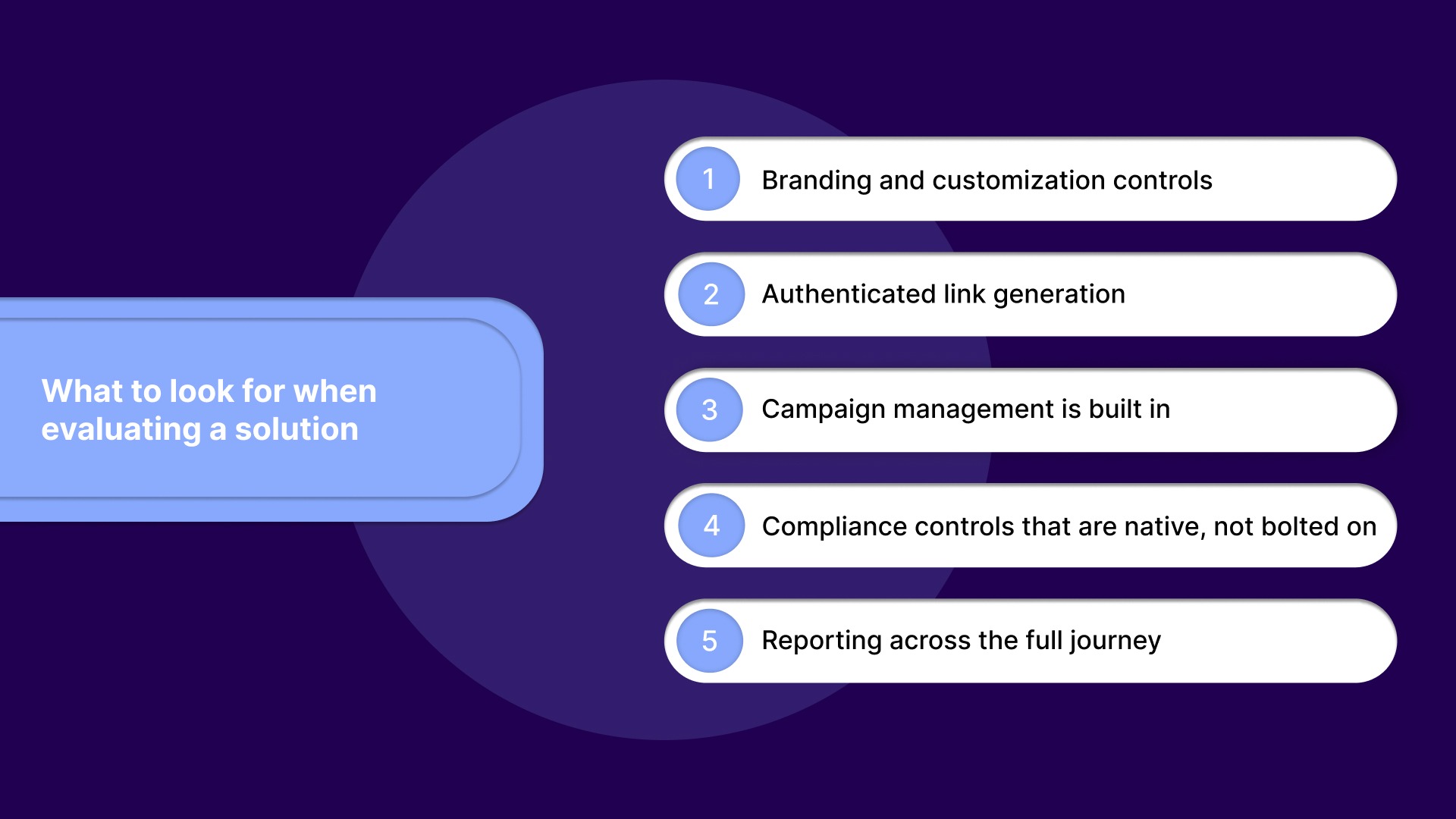

A white-label debt collection portal with SMS integration closes it. The text message and the payment destination work as a single connected recovery workflow, not as two tools your team stitches together manually. This blog breaks down what that integration looks like in practice, why it matters for recovery performance, and what agencies should look for when evaluating a solution.

A white-label debt collection portal is a consumer-facing payment platform that carries your agency's branding rather than the software vendor's. To the consumer, every touchpoint looks and feels like it's coming directly from the agency they're dealing with.

Familiarity and trust drive consumer engagement in debt recovery. A payment portal that reflects a recognized brand reduces hesitation at the moment of payment. An unbranded or vendor-branded page introduces doubt, and doubt kills conversions.

A genuine white-label solution goes beyond visuals. Agencies can configure:

Different clients, different portfolios, different rules, the portal adapts without requiring a separate system for each.

When agencies control the messaging, they control the disclosures and communication parameters. That reduces the risk of inconsistent consumer interactions and keeps the agency on the right side of regulatory requirements.

SMS is how agencies get consumers to the portal. A text message with a payment link has a structural advantage over every other outreach channel: consumers see it, and they see it fast. But the channel itself is only half the equation.

When SMS and the portal operate independently, the consumer journey breaks at the handoff. A consumer receives a text, clicks a link, lands on a generic page, and is asked to search for their account. Each extra step reduces the likelihood of payment. The drop-off isn't a consumer behavior problem; it's a systems problem.

When SMS is integrated with the portal, the link in the text takes the consumer directly to their account, pre-authenticated. They see their balance, their payment options, and their arrangement terms immediately. No login screens, no account lookups, no friction.

This is where recovery performance shifts. Agencies that paired SMS campaigns with an authenticated portal experience have moved from daily online collections of $1,500 to $2,000 into days hitting $5,000, $8,000, and $13,000.

When SMS and the portal are managed separately, campaign performance is harder to track. Agencies lose visibility into which messages drove payments, which links consumers clicked, and where they dropped off. A connected system surfaces that data in one place, letting agencies refine outreach based on actual recovery outcomes.

The performance case for a connected SMS and white-label portal comes down to one thing: reducing the distance between a consumer receiving a message and completing a payment.

Every step a consumer must take after receiving an SMS reduces the likelihood of payment. A connected system compresses that journey:

That sequence drives volume in a way that disconnected tools cannot replicate.

A connected system gives agencies visibility into:

That data tells agencies which campaigns are working, which consumer segments are responding, and where to focus outreach next.

Deploying SMS at scale in debt collection is not just a technology decision. Every text message sent to a consumer carries regulatory weight, and agencies need the right controls in place before campaigns go live.

Agencies need documented consumer consent before sending any SMS. The TCPA requires express written consent for automated or pre-recorded messages sent to mobile numbers. Regulation F adds debt-collection-specific requirements around electronic communications, including how consumers receive notice and opt out. Both frameworks need to be addressed before the first message goes out.

When a consumer replies to opt out, the agency must honor that request immediately and consistently across every channel. Agencies managing opt-outs manually through a separate SMS tool and portal risk sending a follow-up message to a consumer who has already opted out. That exposure is significant. A connected system automatically handles opt-out logic, applying it to SMS and portal communications in real time.

Every SMS sent in a collections context needs to meet specific content standards:

Getting these requirements right is the baseline. The next question is whether the platform an agency chooses makes that baseline easy to maintain.

Not every platform that offers SMS and a consumer portal delivers them as a connected system. Agencies evaluating solutions need to look past feature checklists and assess how the two actually work together in practice.

Most platforms check some of these boxes. Few check all of them, and fewer still deliver them as a genuinely connected system rather than a collection of bolt-on features. That distinction separates a platform that promises integration from one that actually delivers it.

Tratta was built to meet these requirements as a single system. The consumer self-service portal supports per-client branding and configuration, SMS campaigns generate consumer-specific authenticated links, and TCPA, FDCPA, and Regulation F controls run natively across both channels.

Reporting ties SMS sends directly to portal sessions and payment outcomes in one view, so agencies can measure what's actually driving recovery.

Recovery performance in debt collection is rarely a single-variable problem. More often, it comes down to how well the moving parts of an agency's operation connect with each other. SMS outreach and a consumer payment portal are two of the most important tools an agency runs. When they operate independently, the gap between them turns into lost payment opportunities.

A white-label debt collection portal with SMS integration removes that gap. Consumers move from a text message to a branded, authenticated payment experience without friction. Compliance controls run in the background instead of relying on agents to remember every rule. Reporting ties the full journey together, from the first outreach to the completed payment, without stitching together data from separate systems.

For agencies evaluating their current setup, the right question isn't whether they have SMS or a portal. It's whether the two are working as one.

Tratta's white-label portal and SMS campaigns work as a single connected recovery system built specifically for collection agencies. Book a demo and see how it performs for your team.

Under Regulation F, debt collectors are limited to 7 calls within 7 consecutive days for each debt. Regulation F does not set a specific numeric cap on text messages the way it does for calls, but TCPA and FDCPA provisions still require that messages not rise to the level of harassment. Some states impose additional restrictions on text message frequency in debt collection, so agencies should verify state-specific rules with legal counsel before setting campaign cadence.

No. A genuine white-label debt collection portal is hosted and maintained by the software vendor. Agencies access branding and configuration controls without managing the underlying infrastructure. This allows agencies to deploy a fully branded consumer experience without dedicated IT resources or development overhead.

Yes, provided the platform has compliance controls built into the automation layer. Automated campaigns should include consent verification before sending, real-time opt-out enforcement, and FDCPA-compliant message templates. Automation without these controls in place creates regulatory exposure at scale because the volume of messages amplifies any compliance gaps in the workflow.

When the two systems are separate, an opt-out request captured by the SMS tool may not automatically carry over to the portal's communication settings, and vice versa. This creates a risk of contacting a consumer who has already opted out through a different channel. A connected system applies opt-out logic across all channels simultaneously, eliminating that exposure.

The key metric is payment attribution, tracking which portal sessions and completed payments originated from an SMS link. Without a connected system, this attribution requires manual data matching across separate tools and is often incomplete. A unified platform automatically surfaces data, allowing agencies to measure cost per payment and revenue per text sent at the campaign level.