For most collection agencies, margin loss builds across the small gaps between tasks. An agent answers a balance question the consumer portal could have handled. A payment team manually checks a failed transaction. A manager rebuilds the day's status from scattered exports and Slack threads.

That lost time matters because collection work still depends on trained staff. The U.S. Bureau of Labor Statistics says bill and account collectors held about 166,900 jobs in 2024, and many work in call centers for third-party collection agencies. BLS also projects employment in this occupation to decline 10% from 2024 to 2034, while about 13,700 openings are still expected each year on average, mainly to replace workers who leave the occupation.

For a collection agency COO, the takeaway is practical: agent capacity should not be spent on work a clearer account workflow can absorb. Every balance question, payment status check, and manual report pulls staff away from accounts that need judgment. Reducing operational costs in collections starts by moving routine actions into self-service, connecting payment status to the account, and giving managers reporting they do not have to rebuild by hand.

This guide walks through where those costs hide and what a leaner collection operation looks like in practice.

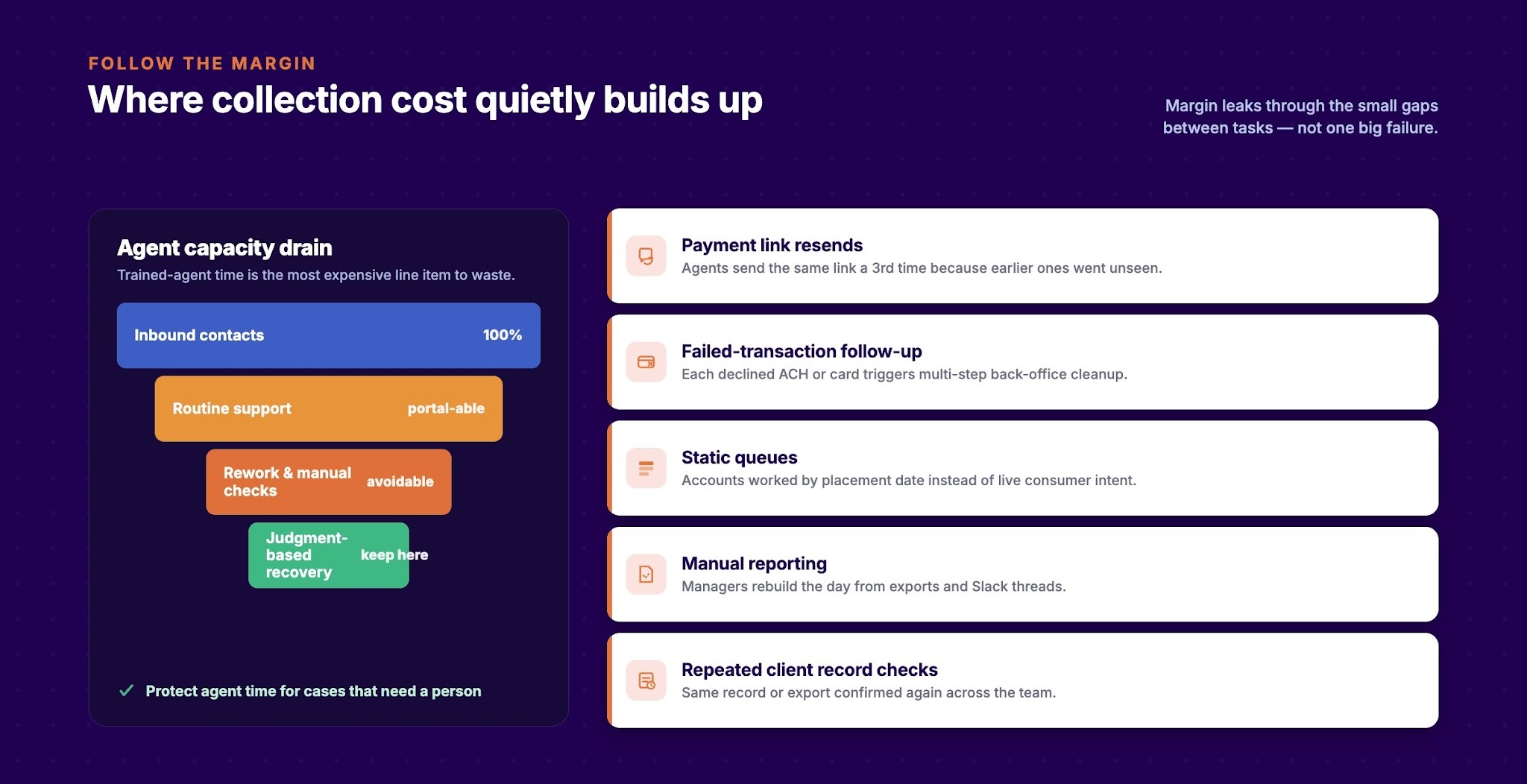

The most persistent cost problem in collections comes from capacity consumed by work that does not advance a case.

Consider a typical day at a mid-size collection agency. Agents field calls about account balances. A payment ops specialist manually reconciles a failed ACH. A supervisor spends 40 minutes assembling a status update for a client who called asking about a portfolio. A collector sends the same payment link for the third time because the consumer did not see the first two.

These tasks may be necessary in the moment. They become expensive when they repeat across every portfolio, every day.

For a collection agency COO, the sharper cost question is this: how much team spend is producing case movement, and how much is only maintaining case status?

Collector time belongs on accounts where outcome depends on a person. That includes hardship conversations, settlement negotiation, broken plan recovery, disputed accounts with conflicting documentation, and complaint-sensitive cases.

When trained agents spend time on account status lookups, payment link resends, and balance confirmations, the cost goes beyond the minute on that call. It includes all the judgment-based work that does not happen while they are answering questions a portal could handle.

A useful internal diagnostic: pull a random sample of 50 inbound contacts from last week and categorize each one.

If routine support makes up a significant share of inbound volume at your agency, that is where cost reduction starts, before you touch headcount or contact frequency.

Rework looks like ordinary activity. A supervisor requests a manual queue update. An agent checks whether a payment posted. A client services contact confirms whether a record was already sent out.

Each instance is small. Across a full portfolio, rework is a material operating cost that most agencies do not track directly because it blends into normal activity.

Common rework signals to watch for:

One case will not show the pattern. A portfolio audit will.

When payments, messages, letters, notes, and client files live in separate systems, every person who touches an account has to piece the picture together manually before they can act.

A collector sees the balance but misses the recent payment attempt. A manager reviews team productivity without seeing channel results. A payment specialist sees a failed transaction without the consumer message that preceded it.

The cost is the repeated, manual effort of reconnecting information that should already sit in one place. That overhead compounds across every case, every shift, every portfolio.

Also Read: Guide to Credit Collections and How Agencies Handle Them

Some cost problems in collections do not surface as obvious failures. They show up as queues that produce the wrong contacts, reporting that arrives too late to act on, and managers spending their day gathering status updates instead of making decisions.

A queue that does not reflect recent consumer activity leads agents toward accounts that are not ready for contact, while accounts with strong payment signals wait behind weaker ones.

If a consumer visited the portal, attempted a payment, or opened a message this morning, that signal belongs in the queue prioritization logic. Without it, agents work accounts based on placement date or portfolio assignment rather than actual consumer intent.

Useful queue signals include:

Queues built on these signals produce fewer wasted contacts per resolved account.

When reporting is slow, fragmented, or requires manual assembly, team leads stop leading and start gathering. They send messages asking which queues are behind. They build the day's picture from exports, callbacks, and Slack pings.

This is a reporting infrastructure problem, and it compounds quickly. Delayed visibility means delayed decisions. Staffing adjustments, queue realignments, and client follow-ups all happen later than they should.

Real-time or near-real-time reporting is the baseline that lets COOs and team leads act on the day's data while it still matters.

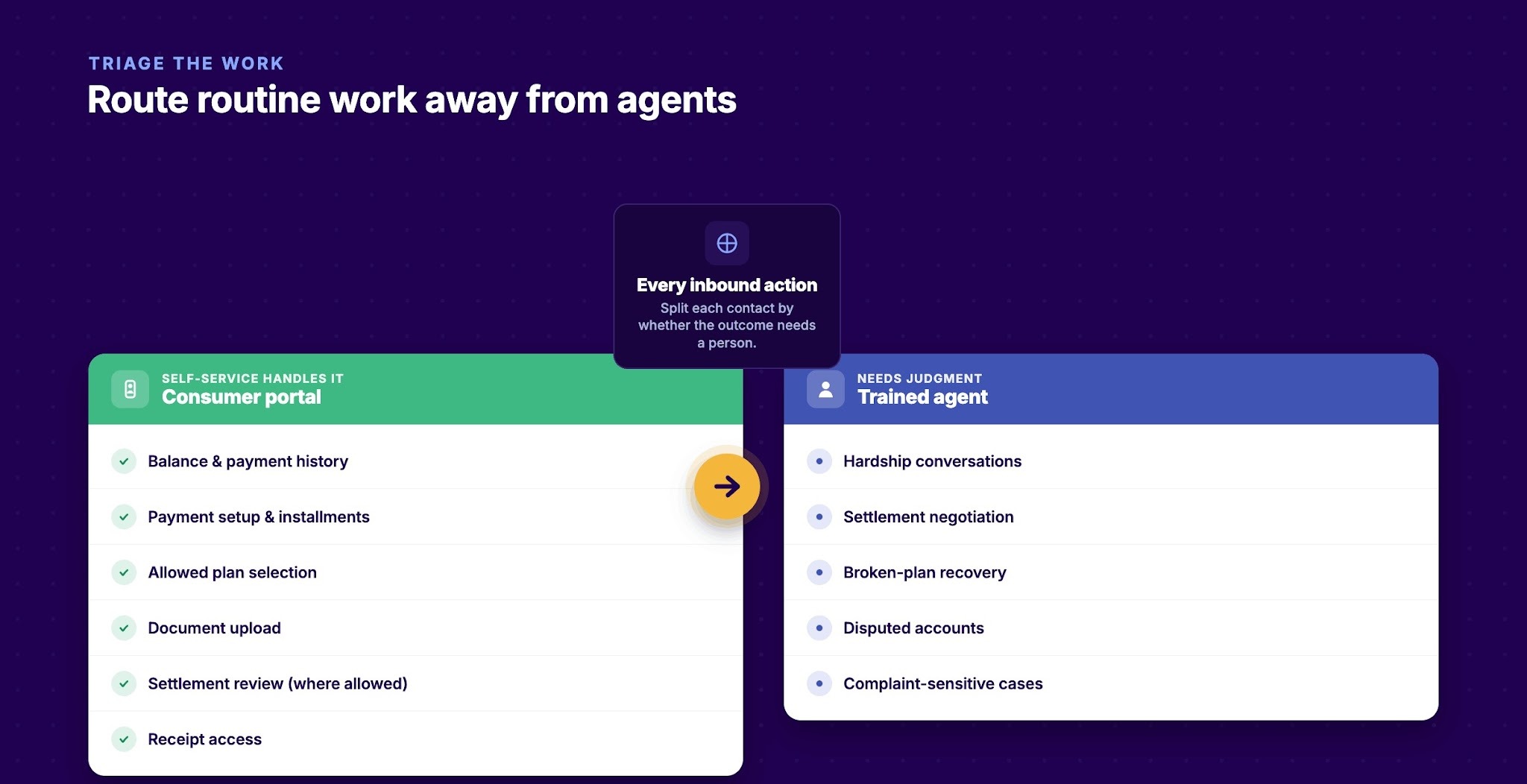

Trained agents should spend less time on low-value contacts and more time on accounts where the outcome depends on their judgment.

Self-service controls cost when consumers can complete the task without abandoning the portal and calling anyway. A hard-to-use or incomplete portal can delay the same call by 20 minutes.

Tasks well suited for consumer self-service:

When consumers can finish these actions through the portal, your agents are available for accounts where the next step requires a conversation.

One-off decisions slow agents and create uneven handling across the team. When each agent decides independently what to do with a broken plan or an unresolved dispute, outcomes vary and supervision gets harder.

A status-based routing model gives each case a defined next action based on where it stands in the recovery workflow.

Supervisors can also use this model to spot where cases are stalling, because a backlog in one status category becomes a visible signal rather than a hidden workflow problem.

Also Read: Debt Recovery Process: Practical Tips, Tools, and Strategies

A consumer who is ready to pay should be the easiest case in your queue. When payment infrastructure creates friction, that case generates support contacts, back-office cleanup, and manager review before it ever closes.

When consumers cannot find a payment method that works for their account, they call. That contact becomes service overhead created by gaps in the payment path.

The question worth asking for your current portfolio: what percentage of payment-related inbound contacts involve consumers asking how to pay, rather than raising a dispute or discussing hardship?

If that number is material, the payment path is generating preventable agent load.

A failed ACH or declined card does not resolve itself. Someone has to identify the failure, determine the cause, update the case, decide the next action, notify the consumer, and adjust any active plan.

If payment status is difficult to view alongside account context, each of those steps requires additional lookups. The cost per failed transaction extends beyond the original failure. It includes the full staff time required to move the case back to a working state.

Agencies with high failed payment volume and manual reconciliation processes carry a hidden per-account cost that does not appear in contact volume metrics.

A consumer who paid yesterday should not receive a balance demand today. A consumer with an active plan should not receive a first-contact message. A consumer whose payment failed this morning is a different priority than one whose plan has been active for three weeks.

When payment status connects to queue logic, agents contact the right accounts at the right moment. Without that link, contact patterns can fall out of sync with account reality and create consumer friction.

Also Read: How Payment Communication Software Improves Debt Recovery

Cutting call volume can still leave operating cost untouched. A team that handles fewer contacts but generates more broken plans, more review issues, or more manual reconciliation has shifted cost to another part of the operation.

Cost per contact measures the price of a single touchpoint. Cost per resolved account measures whether your operation is actually producing outcomes.

A resolved account can mean several defined terminal states your agency tracks: payment completed, plan established, settlement accepted, dispute routed, closure processed.

Tying cost to that outcome prevents cost-reduction initiatives from pushing work downstream rather than eliminating it. If your cost per contact falls but cost per resolved account holds steady or rises, the work has moved, not disappeared.

A single cost number obscures where effort is building. Knowing that cases require multiple agent touches before resolution tells you there is a problem. It does not tell you where.

Stage-level tracking covers the handoff points where stalling typically occurs:

When you know which stage is generating excess touches, you can address that stage directly rather than applying broad pressure across the whole operation.

Some portfolios generate disproportionate staff load relative to payment outcomes. This is often invisible in aggregate metrics but becomes clear when you compare effort-to-movement ratios by segment.

Metrics worth reviewing across client, portfolio, and channel:

Where effort is high and movement is low, a process gap is often the issue. Adding collectors to a broken workflow raises cost further.

Tratta is collection agency software for agencies, collection law firms, credit issuers, and debt buyers. It supports payments, digital communications, consumer self-service, reporting, and workflow control in a single platform.

The cost problems covered in this guide map directly to Tratta's platform areas:

Consumer self-service: Tratta's Consumer Self-Service Platform gives consumers direct access to balances, payment history, payment setup, document upload, and dispute tools. Basic account actions move out of the agent queue when consumers can complete them through a clear portal path.

Reporting visibility: Tratta's Reporting and Analytics covers portfolio management, payment transaction reconciliation, failed payment and chargeback tracking, session logs, audit history, and dispute reporting. COOs and team leads get visibility without manual export assembly.

Payment operations: Tratta's Embedded Payments supports electronic payments, gateway management, account routing, and plan tools inside the collection workflow. Payment status is reviewable alongside account context, which can reduce back-office lookup time.

Contact history: Tratta's Omnichannel Communications covers email, SMS, chat, phone, bilingual IVR, and QR-code letters, along with consent workflows, audit trails, payment-plan reminders, and event-triggered messages. Agents and managers can review what was sent and what the consumer did without manual timeline reconstruction.

Also Read: Best Collection Dashboard Features for US Recovery Teams in 2026

Reducing operational costs in collections works best when the agency changes where work enters the system. If every balance question, failed payment, missing document, and queue update still needs a person, cost will keep returning under a different label.

The stronger operating model is more specific. Let consumers complete routine account actions through clear self-service paths. Give agents the account context they need before contact. Connect payment status to the next action. Measure cost by resolved accounts, not activity volume alone. That gives COOs a cleaner way to reduce manual load while keeping recovery work controlled.

If your team wants fewer handoffs across payments, consumer self-service, communications, and reporting, schedule a demo to see how Tratta supports lower-friction collection operations.

Start by separating avoidable tasks from judgment-based work. Look at what is reaching your agents that a self-service path or clearer status routing could handle. Then look at payment exceptions and reporting overhead. Those three areas typically account for the largest share of avoidable cost.

Track cost per resolved account, touches per payment, payment completion rate, broken plan rate, and the share of inbound contacts that are routine support rather than active recovery conversations. These metrics will show whether a cost reduction actually removed work or just shifted it.

Yes, when the portal is functional enough to complete tasks without consumer abandonment. A portal that consumers cannot finish using sends the work back to the agent queue.

Cost per contact measures the price of a touchpoint. Cost per resolved account measures whether that touchpoint was part of a workflow that produced an outcome. Lower contact volume only reduces operating cost when resolutions improve or manual follow-up falls.

Tratta fits where agencies need fewer manual handoffs across consumer self-service, payment operations, communication history, and reporting. It supports case movement from a single platform rather than requiring staff to connect information across multiple disconnected tools.