Debt negotiation has traditionally relied on collector experience, predefined settlement policies, and manual consumer interactions. However, advances in artificial intelligence are beginning to reshape how organizations evaluate accounts, personalize negotiations, and support debt resolution strategies. The momentum behind this shift is significant.

Research projects the global AI for debt collection market will grow to $15.9 billion by 2034, reflecting increasing investment in AI-driven collection and negotiation technologies. If you are wondering how AI could influence the future of debt recovery, you are not alone.

Collection agencies, creditors, and technology providers are all exploring new ways to improve negotiation outcomes while maintaining operational efficiency. In this article, we will examine the trends shaping AI debt negotiation in 2026, the technologies driving adoption, and what these developments could mean for the collections industry.

Brief look:

AI debt negotiation refers to the use of artificial intelligence technologies to support settlement discussions, payment arrangement decisions, and consumer engagement throughout the recovery process.

The concept is gaining traction across the collections industry as organizations look for ways to improve efficiency, personalize consumer interactions, and scale negotiation processes. As noted in a JD Supra analysis of emerging debt settlement technologies:

"These platforms analyze a consumer's debt profile, model settlement scenarios, generate negotiation strategies, and produce draft creditor communications."

In third-party collections, AI debt negotiation can support several operational functions, including:

Understanding these capabilities requires a closer look at the technologies behind them. In the next section, we will examine the core technologies powering AI debt negotiation in 2026 and how they support different stages of the recovery lifecycle.

Suggested Read: Creating Effective AI Debt Payoff Plans

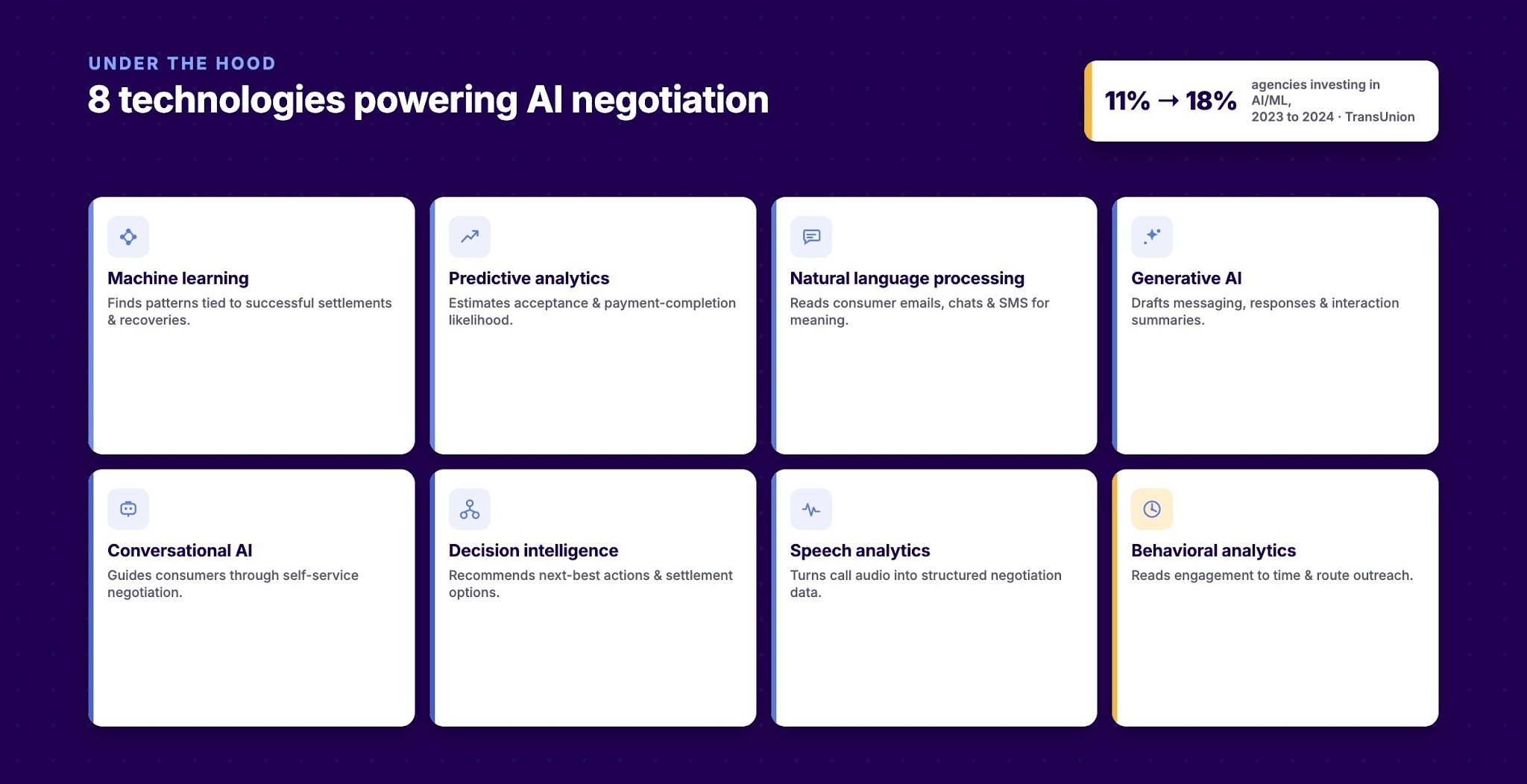

AI debt negotiation relies on a combination of analytical, predictive, and conversational systems working together throughout the recovery process. Adoption is also increasing across the collections industry.

According to TransUnion research, the percentage of debt collection companies investing in AI and machine learning increased from 11% in 2023 to 18% in 2024.

Some of the technologies supporting AI debt negotiation include:

AI may help identify negotiation opportunities, but agencies still need systems that support communication management, payment arrangements, consumer engagement, and operational oversight.

Tratta helps centralize these functions, giving agencies the infrastructure needed to execute negotiation strategies and track outcomes across the recovery lifecycle. It helps agencies support negotiation workflows through communications, payment management, consumer self-service, and operational reporting. Learn more today.

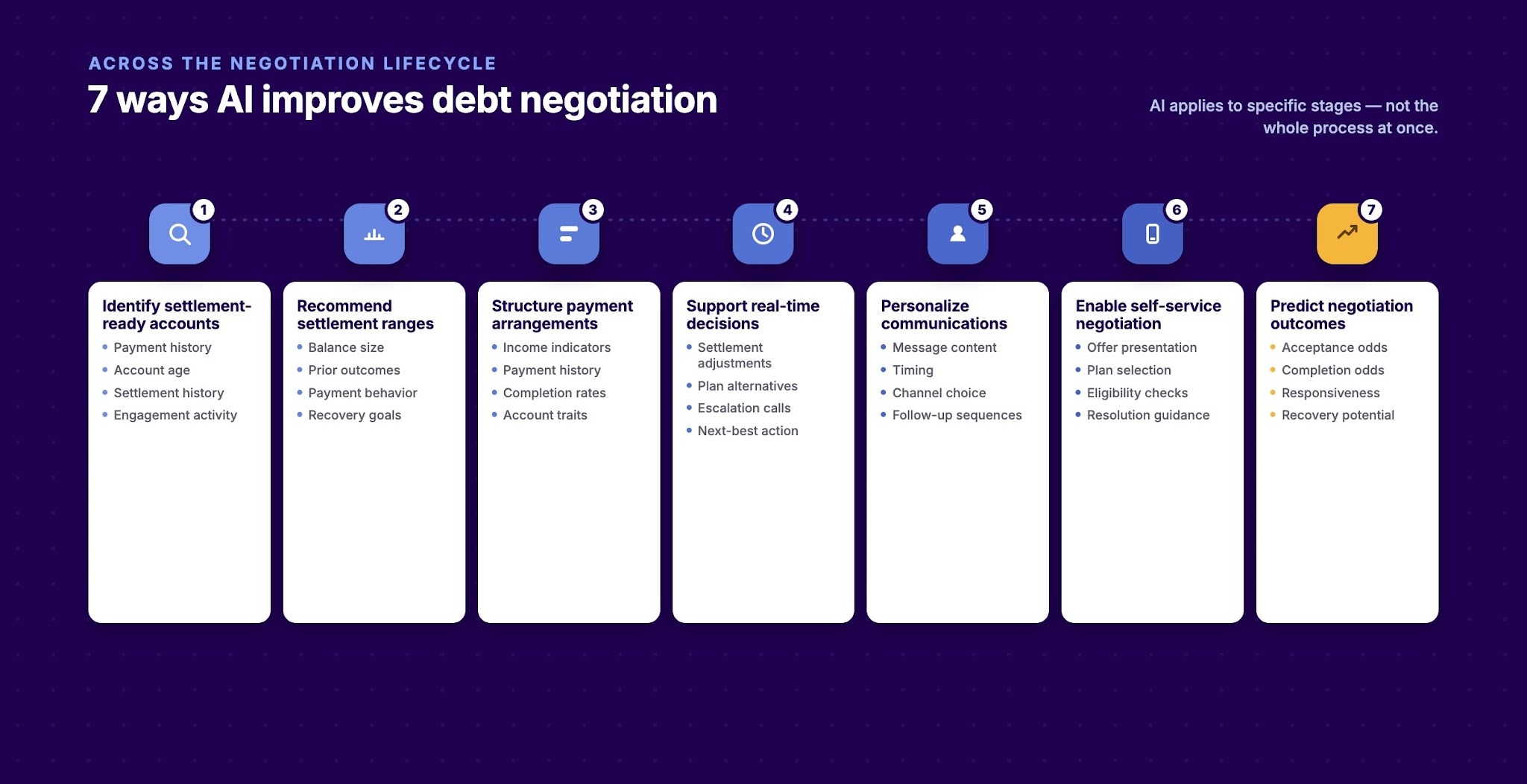

AI is increasingly being applied to specific stages of the negotiation lifecycle rather than the recovery process as a whole. Its value lies in helping agencies make faster, more informed decisions while creating more personalized consumer experiences.

The following examples illustrate where AI can directly influence debt negotiation activities.

Not every account should enter a settlement discussion. AI can help agencies identify accounts where negotiated resolutions may produce stronger outcomes than traditional collection efforts.

AI can evaluate factors such as:

Determining an appropriate settlement offer often requires balancing recovery goals with consumer affordability. AI can analyze historical outcomes to support settlement recommendations.

Inputs may include:

Settlement acceptance does not guarantee payment completion. AI can help agencies design payment arrangements that align with consumer behavior and repayment capacity.

Factors often considered include:

Collectors often need immediate guidance during negotiation conversations. AI can provide decision support by evaluating account information and historical outcomes in real time.

Potential recommendations include:

Different consumers respond to different communication styles and channels. AI can help agencies tailor negotiation-related messaging based on behavioral data.

Personalization may involve:

Consumers increasingly expect digital resolution options. AI can support self-service negotiation workflows without requiring direct collector involvement.

Common applications include:

Understanding likely outcomes before negotiations begin can improve resource allocation. AI can help agencies estimate which accounts are most likely to reach successful resolutions.

Predictive models may evaluate:

The broader question is whether these capabilities translate into measurable operational improvements. In the next section, we will examine the potential benefits of AI-led debt negotiations and their impact on collection performance.

Suggested Read: The Role of AI in Modern Collections Management Explained

While results vary by implementation, AI has the potential to enhance both operational efficiency and consumer engagement throughout the negotiation process.

Potential benefits include:

Despite these potential advantages, AI-led negotiations also introduce new challenges. In the next section, we will examine some of the potential risks and limitations associated with AI debt negotiation.

Suggested Read: AI and Data Transforming Debt Collection Methods

Collection agencies must balance efficiency gains with transparency, compliance, and consumer trust. Without proper oversight, AI-driven negotiation processes can create risks that may outweigh their intended benefits.

Some of the most common challenges include:

Many of these risks become more manageable when agencies maintain strong operational controls. Tratta helps agencies centralize account data, document consumer interactions, maintain communication records, and support compliance oversight across the recovery lifecycle. Schedule a free demo.

The question is no longer whether AI can participate in negotiations. The real question is whether it can replace the judgment, adaptability, and relationship-building skills that experienced negotiators bring to complex discussions. Current research suggests that while AI is becoming more capable, important gaps remain.

A recent study evaluating large language models in negotiation environments found that successful negotiation requires capabilities such as strategic reasoning, understanding counterpart motivations, contextual judgment, and effective communication.

The researchers concluded that negotiation remains particularly challenging for AI systems because it requires "Theory-of-Mind (ToM) skills to infer the partner's motives, strategic reasoning, and effective communication." For this reason, most experts expect AI to augment debt negotiators rather than replace them entirely.

The most likely future is a hybrid model where AI handles analysis, recommendations, and routine interactions while human negotiators focus on judgment-intensive discussions and relationship management. In the next section, we will examine the key factors collection agencies should evaluate before implementing AI within their negotiation and recovery operations.

Suggested Read: AI and Automation In Debt Collection Conversations

AI adoption is often discussed as a technology initiative, but successful implementation depends on much more than selecting the right tool. A strong foundation can significantly influence whether AI delivers measurable value.

Key considerations include:

Agencies also need systems that support communications, payment management, workflow execution, consumer engagement, reporting, and compliance oversight. The right debt collection software can help create the operational foundation needed to support both current collection strategies and future AI initiatives.

AI debt negotiation is generating significant interest across the collections industry, but adoption alone does not guarantee better outcomes. Agencies that implement AI without reliable data, strong governance, clear oversight, and scalable operational processes may struggle to achieve meaningful results.

Tratta helps collection agencies manage communications, payments, workflows, consumer self-service, reporting, and compliance activities within a single platform. This operational foundation can help agencies support negotiation strategies more consistently as new technologies continue to emerge.

The future of debt negotiation will likely combine human expertise, operational discipline, and intelligent technology. Schedule a demo to see how Tratta can support your collection operations.

Yes. AI can be applied to charged-off accounts by analyzing account characteristics, predicting settlement outcomes, and supporting negotiation strategies based on historical performance data.

AI typically evaluates factors such as account balance, payment history, prior settlement outcomes, consumer engagement activity, and portfolio performance to recommend potential settlement ranges.

Many AI-powered communication tools can support multiple languages through automated translation, conversational interfaces, and multilingual engagement workflows.

AI adoption is occurring across third-party collection agencies, debt buyers, collection law firms, and creditor recovery departments seeking to improve efficiency and consumer engagement.

Common performance indicators include settlement acceptance rates, payment completion rates, liquidation performance, negotiation cycle times, collector productivity, and consumer engagement metrics.