Debt collection has always been about balance: recovering payments, staying compliant, and maintaining trust. That balance is getting harder to maintain.

Consumer expectations are rising. Regulatory scrutiny is increasing. Outreach now spans calls, SMS, email, and self-service portals, while costs continue to grow. The Consumer Financial Protection Bureau consistently ranks debt collection among the top sources of consumer complaints, often linked to unclear or excessive communication. At the same time, McKinsey reports that AI-led automation can reduce operational costs in financial services by 20 to 30% when applied correctly.

This widening gap between how collections need to operate and how they actually do is where AI in collections management becomes essential.

This article explains what AI in collections management means, where it creates real value, and how collection agencies, law firms, and credit-focused companies can use it responsibly without losing compliance, control, or consumer trust.

Collections management is the structured process organizations use to monitor, contact, and recover overdue payments while meeting regulatory requirements and maintaining appropriate customer relationships.

AI in collections management is often misunderstood. It does not mean aggressive automation, unchecked messaging, or removing people from the process. It also does not mean allowing algorithms to make legal or ethical decisions.

Basically, AI in collections management uses data, machine learning, and automation to support how delinquent accounts are managed, contacted, and resolved. The goal is to improve consistency, accuracy, and decision-making at scale.

Suggested read: Hard vs. Soft Collections: What’s the Difference and When to Use Each

Once the definition is clear, the real question becomes why so many collections teams are turning to AI now.

Traditional collections depend on manual work and action taken only after payments are missed. As transaction volumes grow, regulations tighten, and cost pressure increases, this reactive model no longer scales.

AI shifts collections toward earlier, more informed action. By analyzing payment behavior and risk signals, AI helps teams spot issues sooner and apply the right level of outreach. This allows human effort to focus on cases that require judgment rather than routine follow-ups.

Adoption is accelerating for clear reasons:

Organizations using AI in collections report lower days sales outstanding and better operational efficiency. As a result, the focus has shifted from whether AI belongs in collections to how it can be applied responsibly.

When used correctly, AI changes how collections teams work day to day.

AI does not replace people. It reduces manual effort, improves consistency, and brings structure to collections processes that no longer scale through human effort alone. That improvement becomes easier to see when AI is mapped to specific points in the collections lifecycle.

Suggested Read: How to Handle Debt in Collections: Strategies for Agencies

Research indicates that nearly 60% of collections firms are exploring the use of AI-based tools. When applied correctly, AI does more than improve efficiency. It changes how collections teams operate every day.

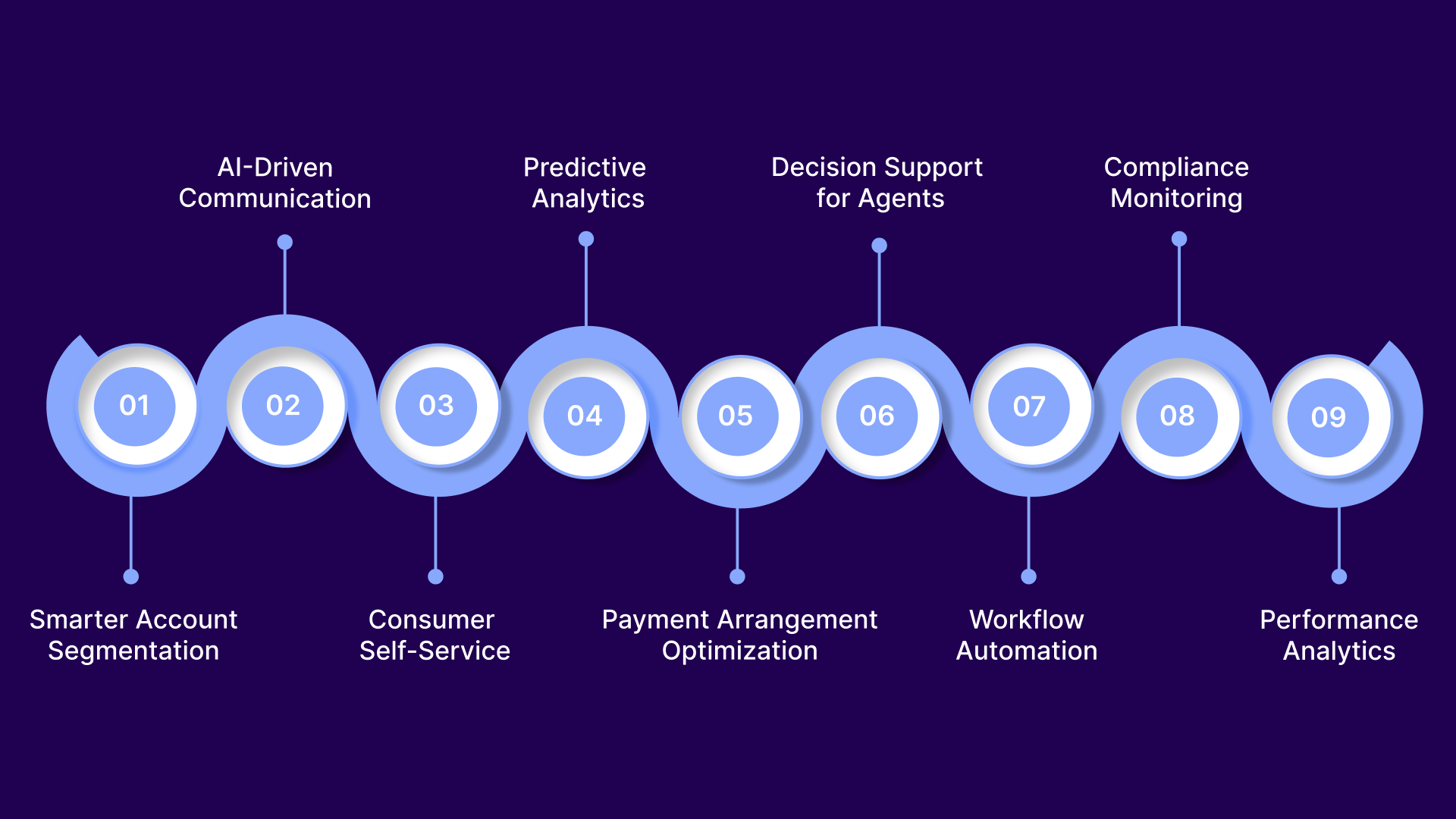

AI evaluates accounts individually instead of in batches. By analyzing payment history, engagement behavior, balance size, channel responsiveness, and time since last interaction, teams can:

This leads to fewer blind calls, lower cost per account, and more consistent recovery outcomes.

Collections now rely on multiple channels, which increases both reach and compliance risk. AI embeds communication rules directly into execution by managing:

AI also selects the most effective channel and timing based on actual engagement patterns, not assumptions.

AI enables digital self-service for consumers who prefer resolving balances without an agent. AI-supported portals provide:

Guided workflows reduce friction, lower call volume, and improve resolution rates.

AI identifies early signs of payment risk by analyzing transaction data, engagement signals, and economic indicators. This supports:

Early intervention improves outcomes without adding pressure.

AI proposes realistic repayment plans at scale by evaluating:

Plans adapt automatically to weekly, bi-weekly, or monthly schedules, improving follow-through while reducing agent workload.

AI supports, rather than replaces, human judgment by recommending:

This improves consistency and reduces repetitive decision-making.

AI automates operational tasks that slow collections teams down, including:

Self-learning models improve accuracy over time, shortening processing cycles and improving cash visibility.

Compliance is built into execution through continuous oversight. AI systems:

This reduces regulatory exposure as requirements evolve.

AI-driven analytics give leaders visibility into:

As systems learn from outcomes, strategies improve and decisions become data-driven rather than intuitive.

Suggested Read: Regulations, Benefits of AI in Debt Collection & the Road Ahead: Insights from ACA 2025

As AI moves from isolated tools into core workflows, responsible use becomes a requirement, not an option.

AI creates real value in collections only when it is applied with clear limits and oversight. For collection agencies, law firms, and credit-focused companies, responsible use begins with embedding compliance directly into daily workflows, rather than relying on reviews after issues arise.

Key principles for responsible AI use include:

When applied this way, AI improves efficiency and recovery outcomes while preserving compliance, operational control, and consumer trust. In practice, responsible AI adoption depends heavily on platform design. Solutions like Tratta embed compliance, consumer choice, and operational controls directly into daily collections workflows.

Even with responsible design, teams naturally have questions. Addressing them directly is the only way to move forward with confidence.

AI in collections often raises practical questions around compliance, implementation, and consumer trust. Addressing these concerns upfront helps teams evaluate AI realistically, without assumptions or hype.

Any tool can create risk if it is misused. When implemented correctly, AI reduces compliance risk by enforcing communication rules consistently and maintaining clear audit trails. Automation should strengthen consumer protection, not undermine it.

Most modern AI-enabled platforms are designed to integrate with existing collections systems. In practice, the challenge is less about the technology itself and more about choosing a platform with the right controls, governance, and long-term support.

Consumers respond to clarity and fairness, not the technology label. When AI improves transparency, enables self-service, and reduces friction, consumer trust tends to increase rather than decline.

No. AI is designed to support collectors, not replace them. It helps with prioritization, routine tasks, and guidance, while human agents remain essential for judgment, negotiation, disputes, and sensitive conversations.

Suggested Read: Comparison of Best Debt Collection Software

When concerns around compliance, trust, and control are addressed, the remaining question becomes practical: how do collections teams apply AI in real operations without increasing risk or disrupting existing systems? This is where platforms like Tratta become important.

Tratta is a digital-first technology platform built specifically for modern collections operations. It is not a collections agency. Instead, it provides the infrastructure collection agencies, law firms, and credit-focused companies use to manage payments, communication, and compliance in one system.

Tratta’s platform aligns with responsible AI adoption by embedding structure, controls, and consumer choice directly into daily workflows. This allows teams to apply AI-supported processes without increasing risk or rebuilding existing operations.

Core capabilities include:

By bringing these capabilities together, Tratta helps teams run more efficient, compliant collections while giving consumers clearer and more controlled ways to resolve their accounts.

AI is changing collections in practical, measurable ways. It does not replace people or judgment. It supports better decisions, more consistent communication, and stronger compliance at scale, while preserving consumer trust.

Digital-first platforms like Tratta show how this works in real operations. AI is embedded into daily workflows, supporting self-service, compliant outreach, and integrated payments rather than operating as a separate experiment.

If you want to understand how AI-driven collections management fits into existing operations, you can learn more about Tratta’s approach or schedule a free demo to see these workflows in action.

AI aggregates and analyzes data from payments, communication history, and consumer interactions. This creates a clearer view of risk, engagement patterns, and outcomes across accounts.

AI is applied through digital platforms that support segmentation, automated communication, self-service payments, and compliance monitoring. It works alongside agents, not in place of them.

No. When implemented correctly, AI reduces compliance risk by enforcing rules such as contact frequency, consent, and disclosure requirements automatically and maintaining detailed audit trails.

AI focuses on precision rather than pressure. It tailors outreach based on behavior, timing, and channel preference, helping consumers resolve balances in ways that are more likely to succeed.

Yes. AI enables digital self-service options such as balance visibility, payment plans, and dispute handling, allowing consumers to resolve accounts without speaking to an agent.