Collection agencies generate vast amounts of account, payment, and communication data every day. Turning that information into better recovery decisions is often easier said than done.

Research published in the International Journal of Innovative Research and Scientific Studies found that the use of big data technology in management decision-making positively impacts both operational efficiency and financial performance.

For third-party collection agencies, this presents a significant opportunity to improve prioritization, consumer engagement, and recovery outcomes. In this article, we explore how big data and debt management work together, the benefits of data-driven collections, and best practices for implementation.

Brief look:

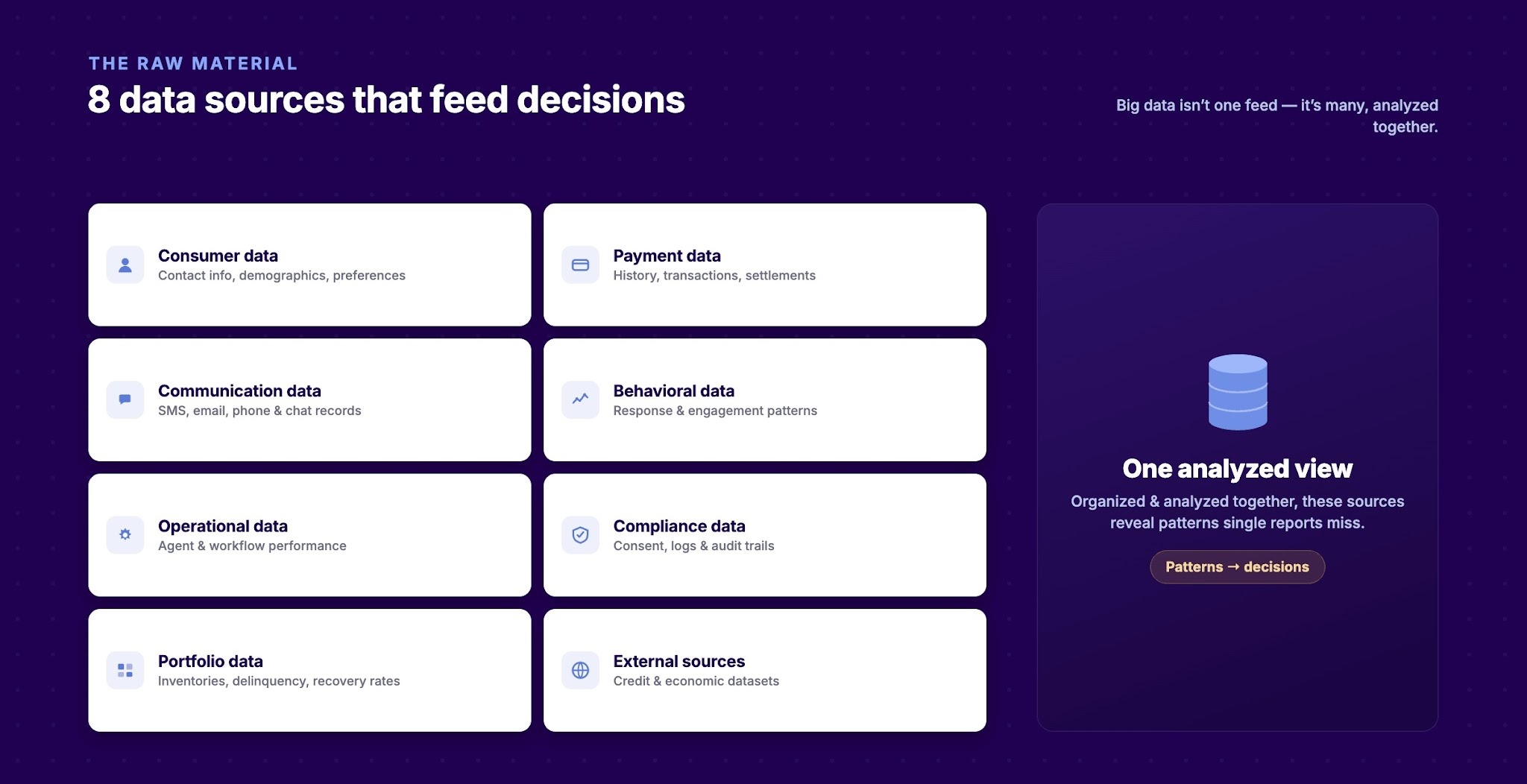

Big data refers to the large volumes of information generated throughout the collection process. For third-party collection agencies, this includes account records, payment activity, communication history, consumer interactions, and operational performance data.

By leveraging data and debt collection predictive analytics, you can gain a more complete view of existing and potential customers to better determine associated risk and enhance your overall decisioning.

- Experian

Big data is not simply about collecting information. It involves analyzing data from multiple sources to identify patterns, improve decision-making, and support better recovery outcomes.

Several components contribute to big data in collection operations:

When agencies can organize and analyze these data sources effectively, they gain a clearer understanding of both consumers and collection performance. In the next section, we will examine the key benefits of using big data in debt management and how it can support stronger recovery outcomes.

Suggested Read: Guide to Predictive Scoring and Segmentation For Debt Recovery

Collection agencies generate and manage large amounts of information every day. When that data is properly analyzed, it can reveal trends, opportunities, and risks that may otherwise go unnoticed. Big data helps agencies move from reactive decision-making to a more informed and strategic approach to debt recovery.

Some of the most significant benefits include:

The benefits of big data become even more valuable when applied throughout the collection lifecycle. In the next section, we will explore how collection agencies can use big data across the recovery process to improve engagement, efficiency, and recovery outcomes.

Suggested Read: How Data Transforms Debt Collection Strategies

Big data can support decision-making at every stage of the collection lifecycle. From account placement to final resolution, agencies can use data-driven insights to improve efficiency, consumer engagement, and recovery performance.

The following applications demonstrate how big data creates value throughout the recovery process.

Not every account offers the same recovery opportunity. Big data helps agencies analyze account characteristics and historical outcomes to identify where resources may have the greatest impact.

Big data can support:

Consumers have different communication preferences and repayment behaviors. Big data helps agencies create more targeted engagement strategies based on these differences.

Data can be used for:

Collection success often depends on reaching consumers through the right channel at the right time. Big data helps agencies identify patterns that support more effective engagement.

Insights may improve:

Forecasting helps agencies plan staffing, budgets, and collection strategies. Big data provides greater visibility into future performance trends.

Forecasting applications include:

Large volumes of consumer interactions create compliance challenges. Big data helps agencies monitor activity and identify unusual patterns more efficiently.

Compliance use cases include:

Operational data can reveal performance trends across teams and individuals. Agencies can use these insights to improve coaching and productivity.

Performance analysis can support:

Collecting data is only one part of the process. Agencies also need tools that help organize, analyze, and act on that information.

Tratta supports data-driven collection operations through reporting and analytics, omnichannel communications, campaign management, and integrations. These capabilities help agencies turn operational data into actions that support stronger recovery outcomes and consumer engagement. Schedule a free demo.

Traditional debt management often relies on historical reports, manual reviews, and broad collection strategies. Big data introduces a more dynamic approach by using large volumes of information to support faster and more informed decisions.

Table showing differences:

While big data offers significant advantages, implementation is not without challenges. Agencies must manage data quality, integrations, compliance requirements, and operational adoption. In the next section, we will explore the most common challenges agencies face with big data and how to address them effectively.

Suggested Read: AI and Data Transforming Debt Collection Methods

Big data can improve decision-making and operational performance. However, agencies often face obstacles when trying to collect, manage, and use large volumes of information effectively. Addressing these challenges is essential for maximizing the value of data-driven collections.

Some of the most common challenges include:

Overcoming these challenges often requires more than better data practices. Agencies also need technology that centralizes information and makes it easier to act on insights.

Tratta helps support data-driven collection operations through reporting and analytics, omnichannel communications, campaign management, integrations, and compliance-focused workflows. These features help agencies transform collection data into more informed decisions and measurable recovery outcomes. Call us to learn more.

Big data can only create value when agencies use it effectively. Successful organizations focus on data quality, governance, and operational execution rather than simply collecting more information.

The following best practices can help agencies maximize the impact of data-driven collections.

Agencies also need technology that can collect, organize, analyze, and operationalize information at scale. In the next section, we will explore how the right collection technology can help agencies turn big data into actionable insights.

Suggested Read: Data Analytics in Enhancing Debt Collection Strategies

Tratta is a collection and recovery platform built for third-party collection agencies, creditors, debt buyers, and law firms. While data is essential, value comes from the ability to act on it. Tratta helps agencies transform consumer, payment, communication, and operational data into collection strategies that support better engagement, stronger compliance, and improved recovery performance.

Core features include:

Tratta helps agencies do both by connecting communications, payments, analytics, automation, and compliance within a single platform. Instead of simply generating more data, the platform helps agencies turn information into measurable actions that support stronger recovery outcomes.

Big data has the potential to transform collection operations. However, collecting large volumes of information is not enough. Poor data quality, disconnected systems, limited visibility, and ineffective execution can prevent agencies from turning insights into better recovery outcomes.

Tratta helps third-party collection agencies bridge the gap between data and action. The platform combines reporting and analytics, omnichannel communications, automated campaigns, self-service payments, integrations, and compliance-focused workflows in a single solution.

Looking to get more value from your collection data? Schedule a demo today to explore the platform in action.

Yes. Agencies do not need massive portfolios to benefit from data-driven decision-making. Even smaller organizations can use collection, payment, and communication data to improve efficiency and recovery performance.

The ideal frequency depends on operational needs and account volumes. Many agencies review key performance metrics daily, while broader trend analysis is often conducted weekly or monthly.

Real-time data helps agencies respond more quickly to consumer actions and changing account conditions. This can support faster decision-making and more timely collection strategies.

Common indicators include recovery rates, payment activity, consumer engagement, operational efficiency, agent productivity, and collection costs. Tracking these metrics over time can help quantify business impact.

Big data refers to the large volumes of information collected from various sources. Predictive analytics uses that data to identify patterns and forecast future outcomes, such as payment behavior or recovery potential.