Debt recovery has become harder, not easier. Rising consumer debt, tighter regulations, and shifting communication habits are forcing collection teams to rethink how recovery actually works. In the U.S. alone, household debt crossed $18.04 trillion in 2024, according to the Federal Reserve, leaving little room for error.

For collection agencies, law firms, and credit issue companies, that pressure is constant. Payments stall. Compliance risk increases. Operating costs rise. Recovery is no longer a numbers game driven by volume or persistence. It’s a discipline built on control, compliance, and consumer trust.

This is what effective debt recovery looks like today: a structured process, compliant communication, and technology that gives consumers clarity and choice.

Here, we break down the debt recovery process, practical strategies, and the tools modern teams use to recover balances while staying compliant.

Debt recovery is the structured effort to secure payment on delinquent accounts in a compliant and documented way. It includes consumer outreach, dispute handling, payment arrangements, and, when necessary, escalation to legal steps. It is not a single interaction, but an ongoing management function focused on resolution and proper conduct.

For collection agencies and credit issue companies, this means:

Traditional recovery models relied heavily on manual calls and agent-led follow-ups. That approach does not scale. It increases cost, raises compliance risk, and often frustrates consumers.

Modern debt recovery management prioritizes:

At scale, debt recovery must be repeatable, measurable, and controlled. Viewing it this way makes the need for a structured recovery process clear.

Suggested Read: Regulations, Benefits of AI in Debt Collection & the Road Ahead: Insights from ACA 2025

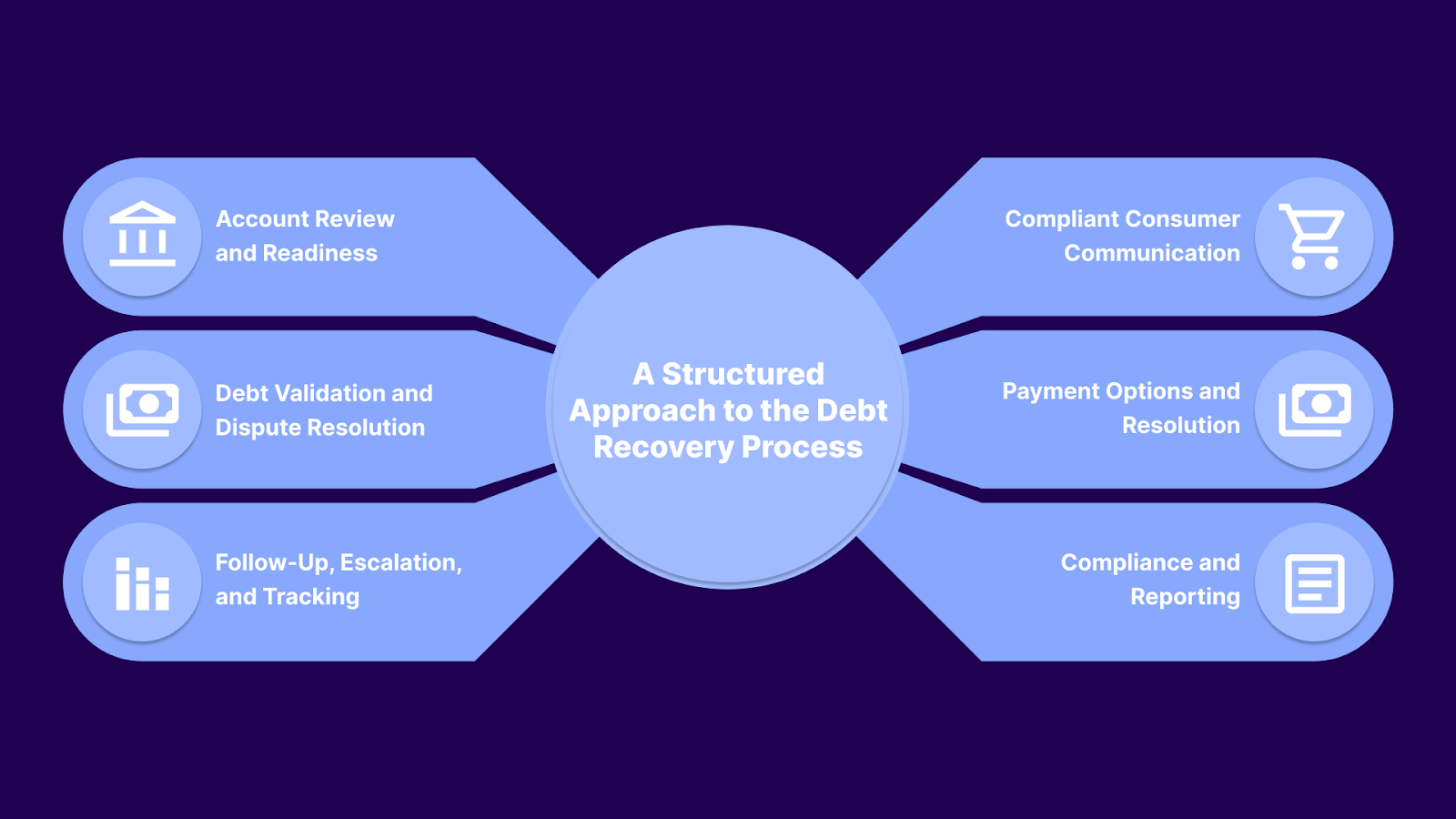

An effective debt recovery process relies on clarity, consistency, and compliance. When each stage is clearly defined, recovery improves, and risk decreases. While tools and timelines may vary, most agencies and credit-focused teams follow the same core framework.

Debt recovery starts with accurate, complete account information. Before any outreach, teams must confirm that the account is actionable.

This includes:

A thorough review at this stage prevents wasted effort and reduces errors later in the process.

Outreach must follow clear regulatory rules. Laws such as the Fair Debt Collection Practices Act and CFPB Regulation F define when and how consumers can be contacted.

Effective communication focuses on:

According to the Consumer Financial Protection Bureau, communication issues remain one of the leading causes of debt collection complaints. Respectful, compliant communication improves response rates and protects the organization.

Consumers have the right to verify debts. When a validation request is made, agencies must respond with accurate and complete information.

Key actions include:

Clear validation processes reduce disputes and support audit readiness.

Once a debt is confirmed, the focus shifts to repayment. Transparent and flexible options increase the likelihood of resolution.

Effective approaches include:

Research from the Urban Institute shows that limited payment flexibility and a lack of clarity often delay resolution. Providing choice helps move accounts toward closure.

Follow-ups should be timely and controlled. Unstructured outreach increases confusion and compliance risk.

Strong processes rely on:

Resolution may include payment, settlement, dispute resolution, or documented escalation.

Compliance runs through every stage of debt recovery.

Teams must maintain:

Under the FDCPA and Regulation F, strong documentation is essential for demonstrating compliance and maintaining long-term operational control.

Suggest Read: How to Use ACH Agreements for Faster Debt Recovery

A defined process creates consistency, but outcomes depend on how well that process is applied. This is where day-to-day strategies make the difference.

Reliable debt recovery results come from disciplined execution, not higher contact volume. Teams that perform well focus on early accuracy, targeted outreach, and system-enforced compliance. The strategies below reflect how experienced agencies and credit issue companies improve recovery while controlling risk.

Recovery success is often determined before the first message is sent. Early outreach works only when the account data is correct.

Before contacting a consumer, teams should:

Addressing these points early prevents invalid outreach, reduces disputes, and avoids restarting the recovery cycle later.

Applying the same approach to every account wastes resources. Effective teams segment portfolios continuously, not just at intake.

Segmentation typically considers:

This allows teams to reserve agent time for complex accounts while routing low-risk balances to digital self-service paths.

Digital communication is effective only when it is intentional and compliant. SMS and email work because they allow consumers to respond on their own terms, not because they increase message volume.

Strong digital outreach:

Without these controls, digital outreach increases complaints rather than payments.

Self-service reduces friction when it replaces, rather than duplicates, agent activity.

Well-designed self-service allows consumers to:

This shortens resolution cycles and reduces inbound calls, allowing agents to focus on negotiation and exceptions.

Recovery stalls when payment terms do not match consumer reality. Flexibility is effective when it is structured, not ad hoc.

Practical flexibility includes:

Clear terms and visibility into obligations reduce abandonment and partial payments.

Manual compliance review does not scale. As volumes grow, enforcement must be automated.

Effective recovery operations:

System-enforced compliance reduces risk without slowing operations.

Disconnected systems obscure what is working and what is not. Centralized data allows teams to adjust strategy based on outcomes.

Teams should analyze:

These insights help refine outreach timing, channel mix, and resource allocation.

Agent productivity declines when time is spent on repetitive tasks rather than decision-making.

Automation should manage:

Agents should handle negotiations, disputes, and escalations. This balance improves recovery quality and reduces burnout.

Clear communication reduces resistance. Vague or aggressive language increases disputes.

Effective messages:

Clarity improves engagement while reducing complaint risk.

Debt recovery conditions change. Consumer behavior, regulations, and portfolio mix evolve over time.

Teams should:

When applied together, these strategies turn debt recovery into a controlled, scalable operation rather than a reactive process.

Suggested Read: SMS Compliance Laws and Regulations

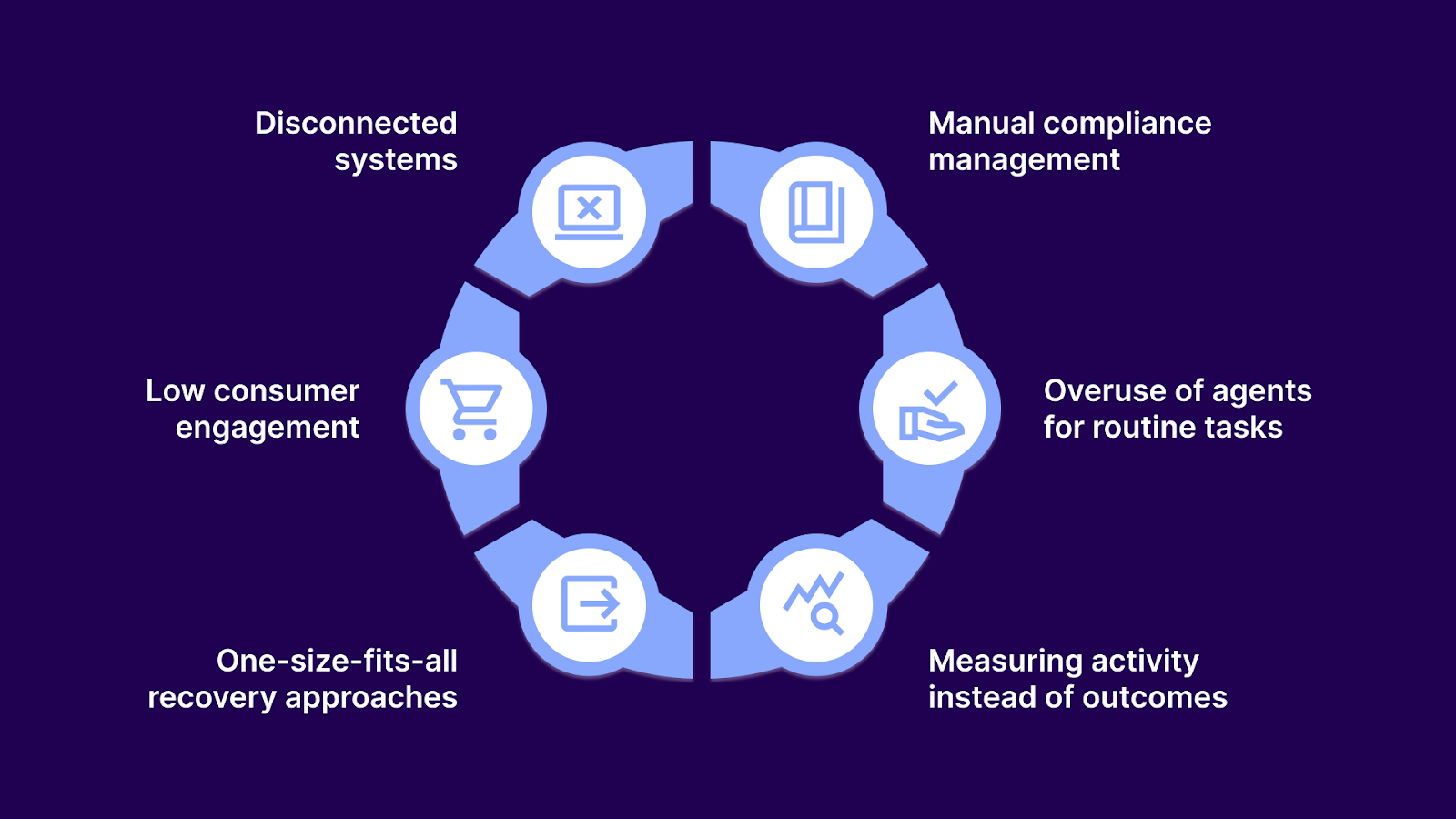

Applying these strategies consistently across large portfolios is difficult without the right systems in place. Even so, recovery efforts can fall short when teams rely on disconnected workflows or manual workarounds.

Debt recovery problems rarely come from a lack of effort. They usually stem from unclear processes, outdated tools, or misaligned priorities. As volumes increase, these issues compound and slow recovery.

Suggested Read: How to Handle Debt in Collections: Strategies for Agencies

Addressing these issues often improves recovery faster than adding more outreach or headcount. Technology plays a critical role in making disciplined recovery possible at scale.

Effective debt recovery depends on systems that reduce manual effort, enforce compliance, and create clear paths to resolution for both teams and consumers. Technology does not replace a recovery strategy. It ensures that the strategy is applied consistently across every account.

Modern debt recovery platforms support this by bringing critical functions into a single workflow:

When these capabilities operate in isolation, teams spend time managing handoffs and correcting errors. When they are unified, recovery workflows remain consistent, compliant, and easier to scale.

Tratta supports this model as a digital-first technology platform. It connects communication, payments, compliance, and reporting in one system, giving organizations visibility and control while allowing consumers to resolve their accounts securely and on their own terms.

Modern debt recovery requires more than outreach tools. It requires systems that enforce compliance, reduce manual work, and give consumers clear ways to resolve accounts. Tratta is built to support this operational reality.

Tratta functions as a digital-first technology platform, not a collections agency. It enables agencies, law firms, and credit issue companies to manage recovery through connected workflows rather than disconnected tools.

Tratta supports:

By centralizing these capabilities, Tratta helps organizations apply recovery strategies consistently at scale while giving consumers secure, straightforward options to resolve their accounts.

Successful debt recovery is built on structure, compliance, and clear communication, not pressure. When agencies and credit issuers treat recovery as a defined workflow, supported by accurate data and consumer-friendly tools, they recover more while reducing risk.

A digital-first approach brings outreach, payments, and compliance into one controlled system. This gives teams clear visibility across every stage of recovery, reduces manual effort, and allows consumers to resolve accounts in a straightforward, secure way.

Ready to see how this approach plays out in your workflows? Request a demo to understand how Tratta balances compliance and operational efficiency.

Debt recovery refers to the process of collecting overdue payments from consumers while following applicable laws and regulations. It focuses on resolving balances in a structured, documented, and compliant way.

Debt recovery emphasizes compliant, consumer-aware resolution using digital tools and self-service options. Traditional debt collection often relies more on manual outreach and agent-led communication.

Debt recovery is governed by regulations such as the FDCPA and CFPB rules. Non-compliance can lead to consumer complaints, penalties, and legal risk, making built-in controls essential.

Digital platforms that support self-service payments, integrated communication, and real-time reporting help reduce manual work, improve visibility, and maintain compliance across recovery efforts.

Consumer self-service allows individuals to review balances and resolve debts on their own time. This improves engagement, shortens resolution cycles, and reduces agent workload and disputes.