Managing large account inventories through disconnected systems, manual workflows, and limited consumer engagement channels can slow recovery efforts and increase operational costs. At the same time, consumer expectations continue to shift toward digital-first experiences.

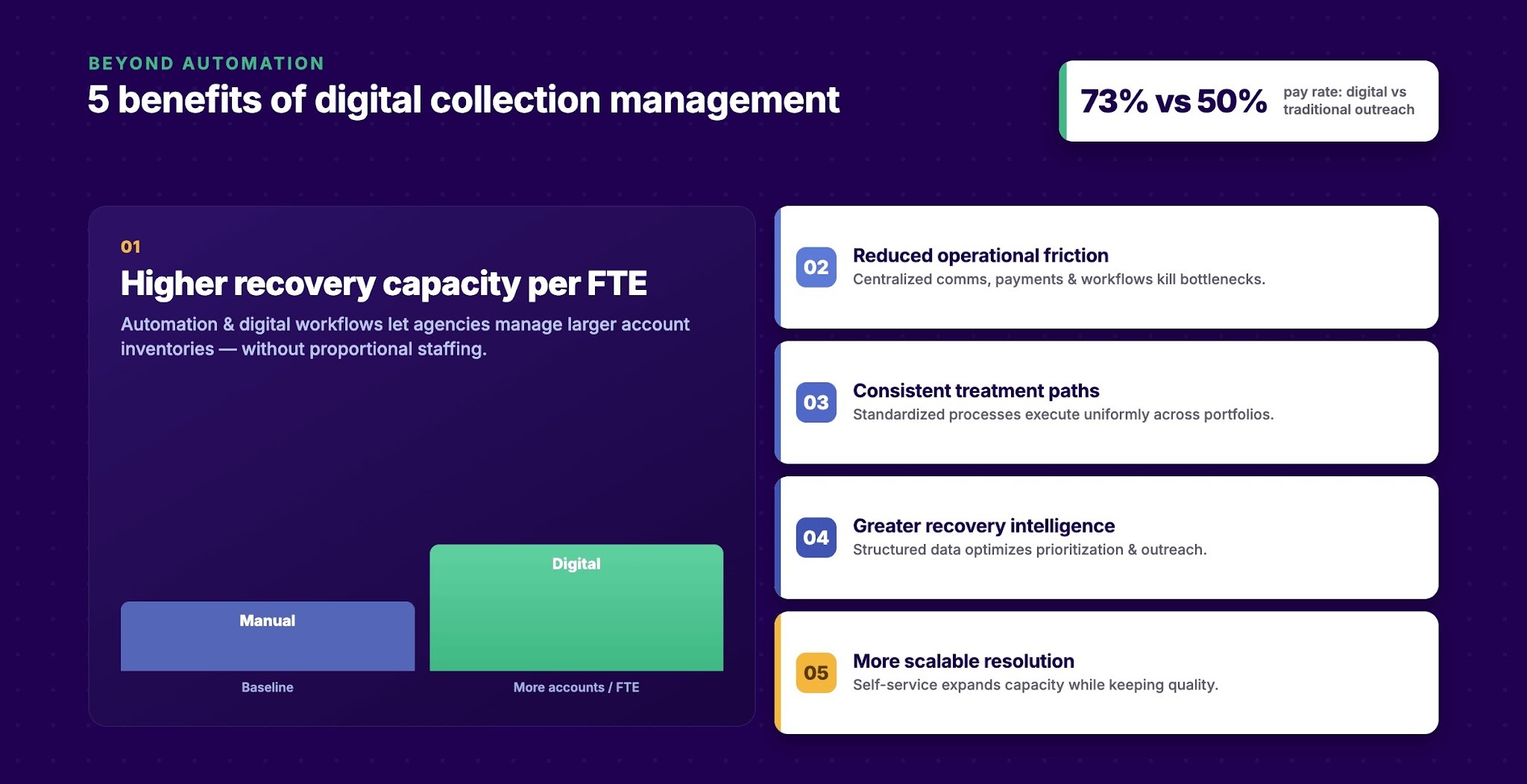

73% of late-stage delinquent consumers made at least a partial payment after receiving digital outreach, compared to 50% contacted through traditional methods. The growing gap highlights the need for more effective digital engagement strategies.

If your agency is evaluating ways to modernize recovery operations, you are not alone. In this article, we will explore how digital collections software works, the features it provides, and the trends shaping collection technology in 2026.

Brief look:

Digital collections software is a technology platform designed to help collection agencies manage recovery operations. It uses digital workflows, communication channels, payment tools, reporting systems, and consumer self-service capabilities.

According to TransUnion, more than 52% of debt collection companies reported increased or significantly increased account volumes over a 12 month period. As portfolio inventories expand, agencies often require more scalable ways to manage consumer engagement, payments, compliance, and operational performance.

In third-party collections, digital collections software is designed to support:

Digital collections platform serves as the operational backbone of modern recovery programs. The next step is understanding how these capabilities can improve collection performance, efficiency, and consumer engagement. In the following section, we will examine the key benefits of digital collection management in debt recovery.

Suggested Read: 9 Benefits of Digital Debt Collection You Can’t Ignore in 2026

Digital collection management changes how agencies allocate resources, manage account inventories, and execute recovery strategies.

Key benefits include:

Achieving these outcomes requires more than isolated collection tools. Tratta helps agencies support digital collection management through consumer self-service, omnichannel communications, payment management, workflow automation, and reporting capabilities. Schedule a free demo today.

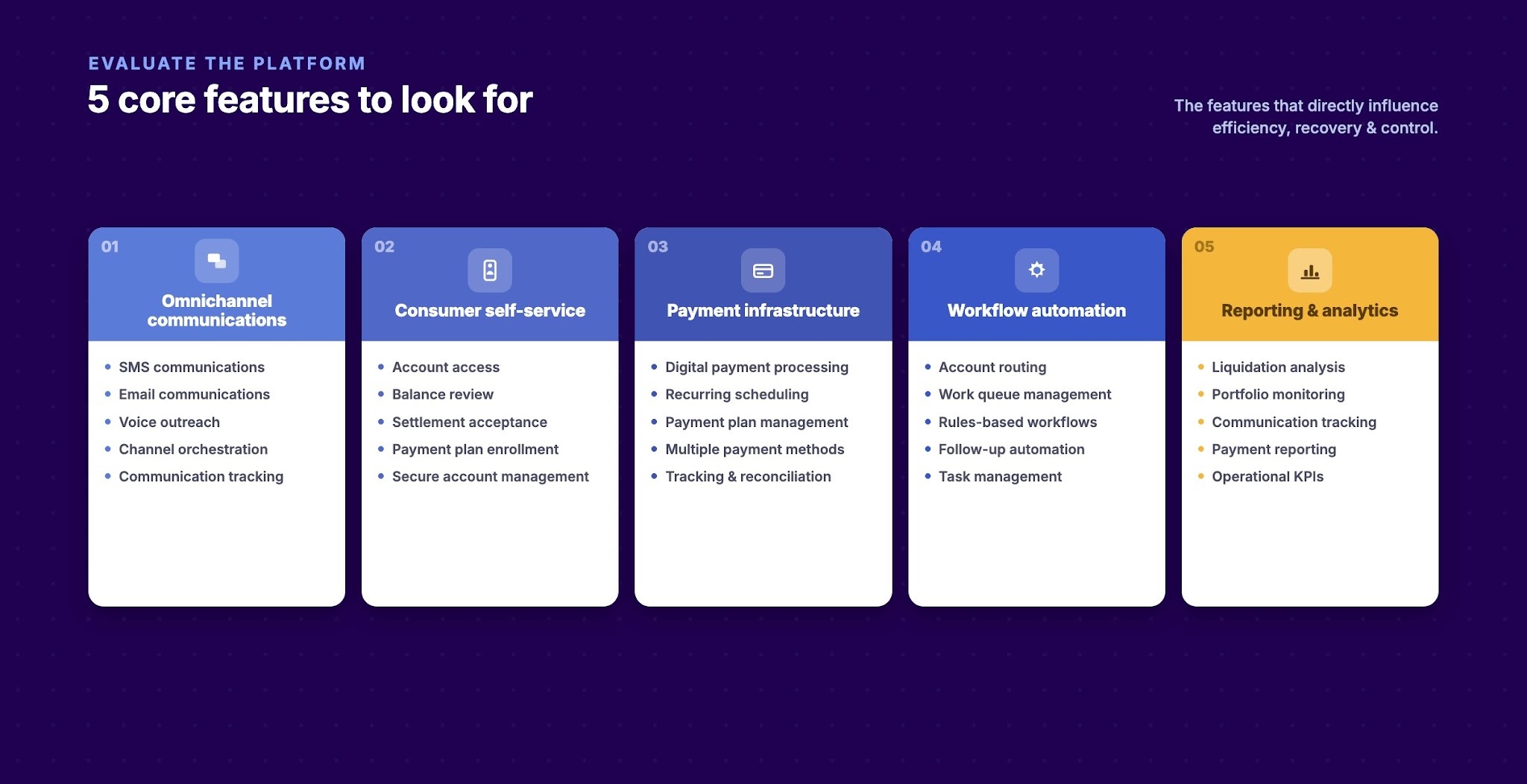

Agencies should evaluate platforms based on their ability to support recovery workflows, consumer engagement, payment execution, and performance management at scale. The most valuable features are those that directly influence collection efficiency, recovery outcomes, and operational control.

Key features include:

Consumer engagement increasingly occurs across multiple communication channels. Agencies need the ability to coordinate outreach while maintaining a consistent consumer experience and complete interaction history.

Key capabilities include:

Many consumers prefer resolving accounts without direct collector involvement. Self-service capabilities can expand resolution opportunities while reducing operational workload.

Important functions include:

Recovery outcomes ultimately depend on successful payment execution. A collections platform should simplify payment acceptance while supporting a variety of consumer payment preferences.

Look for capabilities such as:

Manual recovery processes can create operational inefficiencies and inconsistent account treatment. Workflow automation helps agencies standardize collection activities and improve execution consistency.

Core automation features include:

Effective collection management requires visibility into both operational performance and recovery outcomes. Agencies should be able to evaluate results at the portfolio, campaign, collector, and account levels.

Reporting capabilities should support:

These capabilities often work best when delivered through a single operational platform rather than multiple disconnected systems.

Tratta combines omnichannel communications, consumer self-service, payment management, workflow automation, and reporting capabilities within a single collection environment. This allows agencies to manage core recovery activities through a centralized platform while maintaining visibility across the collection lifecycle. Learn more.

Implementing digital collections software often requires changes to technology, workflows, data management practices, and operational processes. While the long-term benefits can be substantial, agencies that underestimate implementation complexity may experience adoption delays, reporting issues, or reduced operational efficiency.

Table showing common challenges:

Successful implementations typically focus on process readiness as much as technology readiness. Agencies that define operational requirements early are often better positioned to realize value from their investment.

Best practices include:

The next challenge is selecting a platform that aligns with your operational needs. In the following section, we will examine how agencies can evaluate the right digital collections software for their operations.

Suggested Read: ADA Compliance for Debt Collection Platforms: 2026 Guide

Selecting digital collections software involves more than comparing feature lists. The most effective evaluation frameworks focus on business outcomes rather than individual product capabilities.

When assessing potential platforms, consider the following questions:

As collection technology continues to evolve, evaluation criteria are also changing. In the next section, we will examine the digital collections software trends shaping recovery operations in 2026.

Suggested Read: 6 Proven Digital Collections Strategies to Recover More Debt

The digital collections technology landscape continues to evolve as agencies seek greater efficiency, scalability, and consumer engagement.

Digital-first collections can deliver a superior customer experience while reducing collections costs.

- McKinsey & Company

Several trends are expected to influence how agencies evaluate and deploy collection technology in 2026.

These trends reflect a broader shift toward more connected and intelligent recovery operations. While technologies will continue to evolve, the underlying objective remains the same: helping agencies improve execution, increase operational efficiency, and create better consumer experiences at scale.

Digital transformation alone does not guarantee better recovery outcomes. Agencies that implement new technology without addressing workflow design, data quality, consumer engagement strategies, and operational governance may struggle to realize the full value of their investment.

Tratta helps collection agencies centralize critical recovery functions within a single platform. Through omnichannel communications, consumer self-service, payment management, workflow automation, reporting and analytics, and compliance-focused capabilities, agencies can create a more connected digital collections environment.

The right technology can strengthen both operational efficiency and consumer engagement. Schedule a demo to see how we can help improve your collection operations.

Implementation timelines vary based on integration requirements, data migration complexity, workflow configuration, and organizational readiness. Many implementations take several weeks to a few months.

Yes. Most enterprise-grade platforms support multiple portfolios, business rules, reporting structures, and client-specific workflows within a single environment.

Many platforms offer integrations with collection management systems, payment providers, CRM platforms, dialers, and other recovery technologies to reduce operational silos.

Common metrics include liquidation rate, promise-to-pay performance, payment completion rate, consumer engagement rate, right-party contact rate, cost-to-collect, and collector productivity.

Cloud-based platforms often provide greater scalability, faster deployment, lower infrastructure requirements, and more frequent feature updates. However, the best approach depends on an agency's operational, security, and compliance requirements.