Debt recovery has become increasingly complex in recent years. Delinquency rates are rising, regulations are tightening, and consumers expect flexible ways to resolve balances. In the United States, credit card delinquency recently exceeded 3%, the highest level in more than a decade, according to the Federal Reserve.

For collection agencies, law firms, and credit issuers, the challenge is not just contacting consumers. It involves deciding which accounts to prioritize, when to reach out, and how to engage consumers effectively.

Consider a typical scenario. A collections manager reviews thousands of delinquent accounts each week. Some consumers respond to simple reminders, while others require flexible payment options. Without clear insights into repayment behavior and communication preferences, these decisions often rely on guesswork.

Collections intelligence software addresses this challenge. AI-powered platforms analyze account data, predict repayment likelihood, and guide outreach strategies. Instead of reactive workflows, recovery teams gain data-driven insights that help them focus on the accounts most likely to resolve.

In this article, we explain what collections intelligence software is, how it works, and how collection agencies and credit issuers can use it to improve recovery performance.

Collections intelligence software is a platform that uses data analytics, artificial intelligence, and predictive models to help organizations manage and recover delinquent accounts more effectively.

Traditional collections often rely on manual workflows and static reports. In contrast, collections intelligence platforms analyze large volumes of account data such as payment history, account status, and communication activity to identify patterns in repayment behavior.

These insights help recovery teams understand:

AI models evaluate historical payment activity and consumer interactions to estimate repayment likelihood and recommend appropriate collection actions. This allows teams to prioritize accounts with higher resolution potential rather than working through accounts sequentially.

To see why this technology matters, it’s helpful to compare it with the traditional collection systems many organizations still rely on today.

Traditional collection systems primarily support operational tasks such as managing accounts, scheduling calls, and tracking payments. While these tools help organize workflows, most recovery decisions still rely on manual analysis and collector judgment.

Collections intelligence software takes a data-driven approach. It analyzes account data in real time to help teams prioritize accounts, select effective communication channels, and monitor performance more clearly.

These differences also highlight a key issue: many recovery teams still rely on systems built for a very different collections environment.

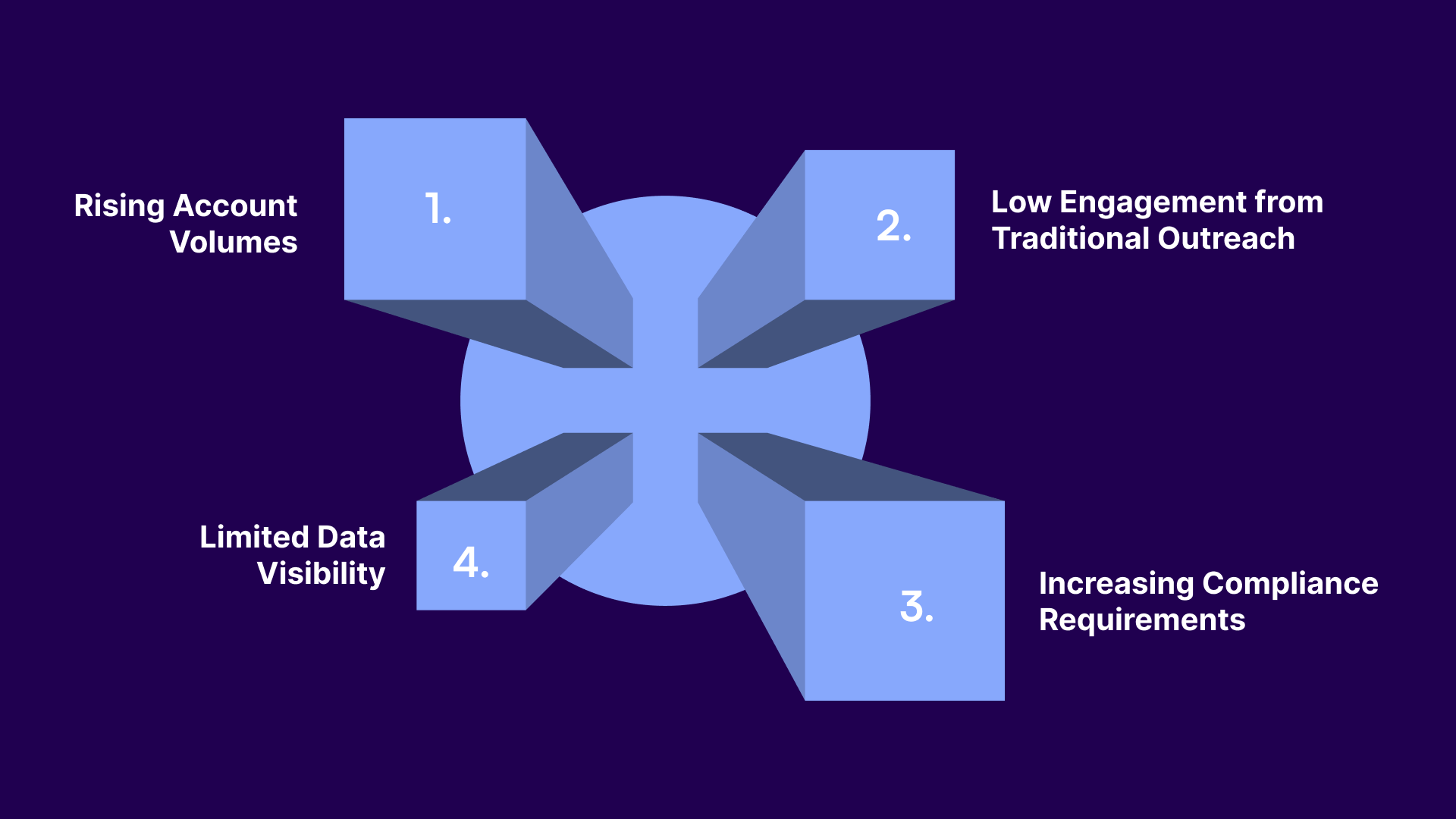

Many collection agencies and credit issuers still rely on processes designed years ago. These workflows often depend on manual account prioritization, dialer-based outreach, and disconnected systems.

As delinquent account volumes grow and consumer communication preferences shift toward digital channels, these methods are becoming less effective.

Financial institutions manage large portfolios of delinquent accounts. As volumes increase, manually reviewing and prioritizing accounts becomes difficult. Without predictive insights or automation, teams may spend the same effort on accounts with very different repayment potential.

Many collections teams still rely heavily on outbound phone calls, which now produce lower engagement rates. Consumers increasingly prefer communication through channels such as SMS, email, and secure payment portals. Without digital communication options, organizations may struggle to reach consumers at the right time.

Debt collection is governed by regulations such as the Fair Debt Collection Practices Act (FDCPA), Telephone Consumer Protection Act (TCPA), and Consumer Financial Protection Bureau (CFPB) guidelines. Managing compliant communication across thousands of accounts can be difficult when processes rely on manual tracking.

Collections teams often manage account data, payment records, and communication history across multiple systems. This fragmentation makes it difficult to identify which accounts are most likely to repay, which outreach strategies work best, and how recovery teams are performing.

Collections intelligence software helps address these challenges by combining analytics, automation, and communication tools to support more informed recovery decisions.

As portfolios grow and communication preferences shift, many organizations are adopting digital collections platforms that bring together analytics, communication tools, and payment infrastructure.

Platforms such as Tratta help collection agencies, law firms, and creditors automate outreach, manage workflows, and offer secure self-service payment options, making it easier for teams to manage accounts and for consumers to resolve balances online. Speak with our team to learn more.

Artificial intelligence is central to modern collections intelligence platforms. By analyzing large volumes of account data, AI identifies patterns in payment behavior and communication responses. These insights help recovery teams prioritize accounts and plan more effective outreach.

1) Predictive Analytics: Predictive models analyze historical payment data and engagement patterns to estimate the likelihood of repayment. This allows teams to focus on accounts with higher repayment potential, detect early signs of delinquency, and allocate resources more effectively.

2) Machine Learning: Machine learning models improve as they process new data. Over time, this increases the accuracy of account prioritization, outreach timing, and payment plan recommendations.

3) Behavioral Segmentation: AI systems group consumers based on payment history, engagement behavior, and financial patterns. This helps teams tailor communication strategies for different consumer groups.

4) Communication Optimization: AI can identify the most effective communication channel and timing for outreach. For example, some consumers respond better to SMS reminders, while others prefer email notifications.

5) Automation and Workflow Intelligence: AI automation manages routine collection tasks such as payment reminders, settlement offers, workflow prioritization, and performance tracking. This reduces manual effort and allows recovery teams to focus on more complex interactions.

These AI technologies enable a range of practical capabilities that help recovery teams manage portfolios more effectively.

Suggested Read: Using SMS for Debt Collection Guide

Modern collections intelligence platforms combine analytics, automation, and digital engagement tools to support efficient recovery operations. These capabilities help organizations prioritize accounts, improve engagement, and maintain compliance while managing large portfolios.

Predictive scoring models analyze historical payment data and account characteristics to estimate repayment likelihood. This helps teams:

These platforms group consumers based on payment history, risk level, and engagement patterns. This allows teams to:

Collections intelligence systems support outreach across multiple channels, including:

This improves engagement and makes it easier for consumers to respond.

Additionally, Tratta's Consumer Self-Service Payment Portal and omnichannel communication capabilities help organizations improve recovery outcomes by making it easier for consumers to engage and resolve balances.

Collections leaders can monitor operations through dashboards that track:

These insights help teams adjust strategies quickly.

Collections intelligence platforms support regulatory compliance by providing:

These features help maintain consistent and compliant communication practices.

When applied across recovery operations, these capabilities improve efficiency and recovery performance.

Collections intelligence software helps collection agencies and credit issuers manage recovery operations more efficiently. By combining analytics, automation, and digital communication tools, these platforms improve decision-making and operational performance.

These benefits become clearer when examining how different organizations apply collections intelligence in real recovery environments.

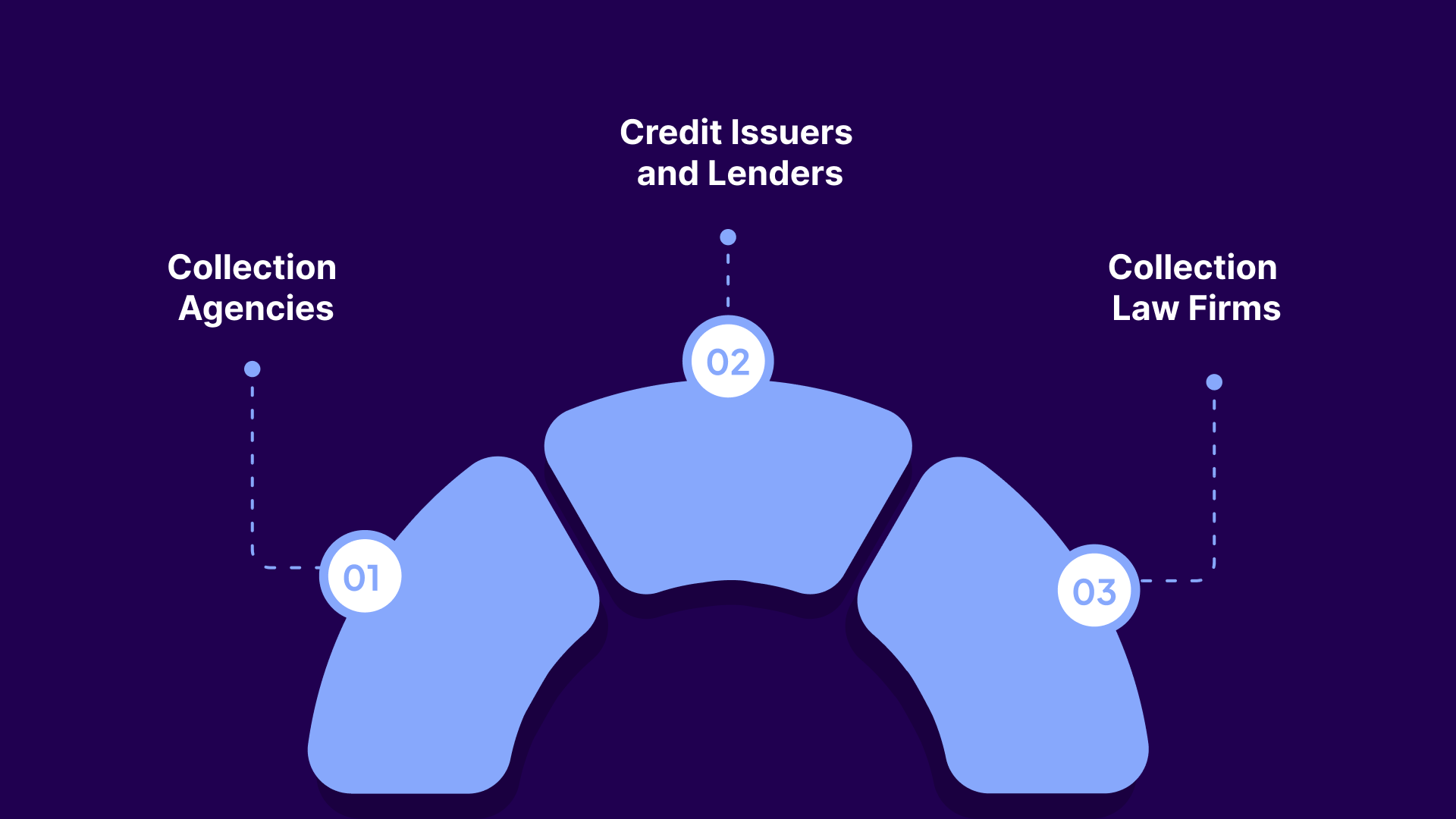

Collections intelligence software supports several organizations involved in debt recovery. By combining analytics, automation, and digital communication tools, these platforms help teams manage accounts more effectively and make informed recovery decisions.

Collection agencies often manage large portfolios from multiple creditors. Collections intelligence tools help agencies:

These capabilities help agencies manage high account volumes while improving recovery efficiency.

Banks, credit card providers, and fintech lenders use collections intelligence platforms to identify early delinquency risks and engage consumers before balances escalate. Common applications include:

These insights help lenders reduce delinquency levels and improve repayment outcomes.

Law firms handling debt recovery rely on structured account data and accurate records to support case decisions. Collections intelligence software helps legal teams:

This improves case management, documentation, and operational oversight.

Beyond operational efficiency, collections intelligence also changes how consumers interact with recovery teams. For organizations evaluating these tools, selecting the right platform is an important step in building a modern collections strategy.

Suggested Read: 10 Practical Tips to Simplify Collections Management

Collection agencies, law firms, and credit issuers should evaluate several factors when selecting a collections intelligence platform.

Organizations looking for these capabilities are increasingly adopting digital-first collections platforms that combine analytics, communication tools, and payment infrastructure.

Many organizations are moving toward digital-first collections platforms to modernize recovery operations. These platforms bring together payment infrastructure, communication tools, analytics, and workflow automation in a single environment. This helps recovery teams manage portfolios more efficiently while giving consumers clearer ways to resolve balances.

Digital-first platforms help organizations:

Platforms such as Tratta support this model by providing a digital collections platform built for collection agencies, law firms, and creditor organizations. Tratta combines consumer self-service payment portals, automated communication tools, reporting capabilities, and system integrations in one environment.

This approach helps recovery teams manage outreach, payments, and compliance workflows more efficiently while allowing consumers to review balances, choose payment options, and resolve debts online.

Collections operations are becoming more complex as account volumes grow and regulatory expectations increase. Traditional recovery methods that rely on manual workflows and limited data visibility often struggle to keep pace with modern collections demands.

Collections intelligence software offers a more effective approach. By combining analytics, automation, and digital communication tools, organizations can prioritize accounts more accurately, improve operational efficiency, and maintain compliance.

Digital-first platforms further strengthen this approach by providing clear account visibility, flexible payment options, and convenient communication channels for consumers.

To learn how digital-first collections technology can support modern recovery operations, explore Tratta’s platform and schedule a demo.

Collections intelligence software is a platform that uses data analytics and AI to improve how organizations manage delinquent accounts. It analyzes payment behavior and account data to help recovery teams prioritize accounts and plan more effective outreach strategies.

The software uses predictive analytics to identify accounts most likely to repay. This allows teams to focus outreach on higher-probability accounts and use the most effective communication channels.

Collection agencies, credit issuers such as banks and fintech lenders, and collection law firms commonly use these platforms. They help manage large portfolios, automate outreach, and monitor recovery performance.

AI analyzes historical payment data, communication patterns, and account behavior to predict repayment outcomes. These insights help teams prioritize accounts and automate routine recovery tasks.

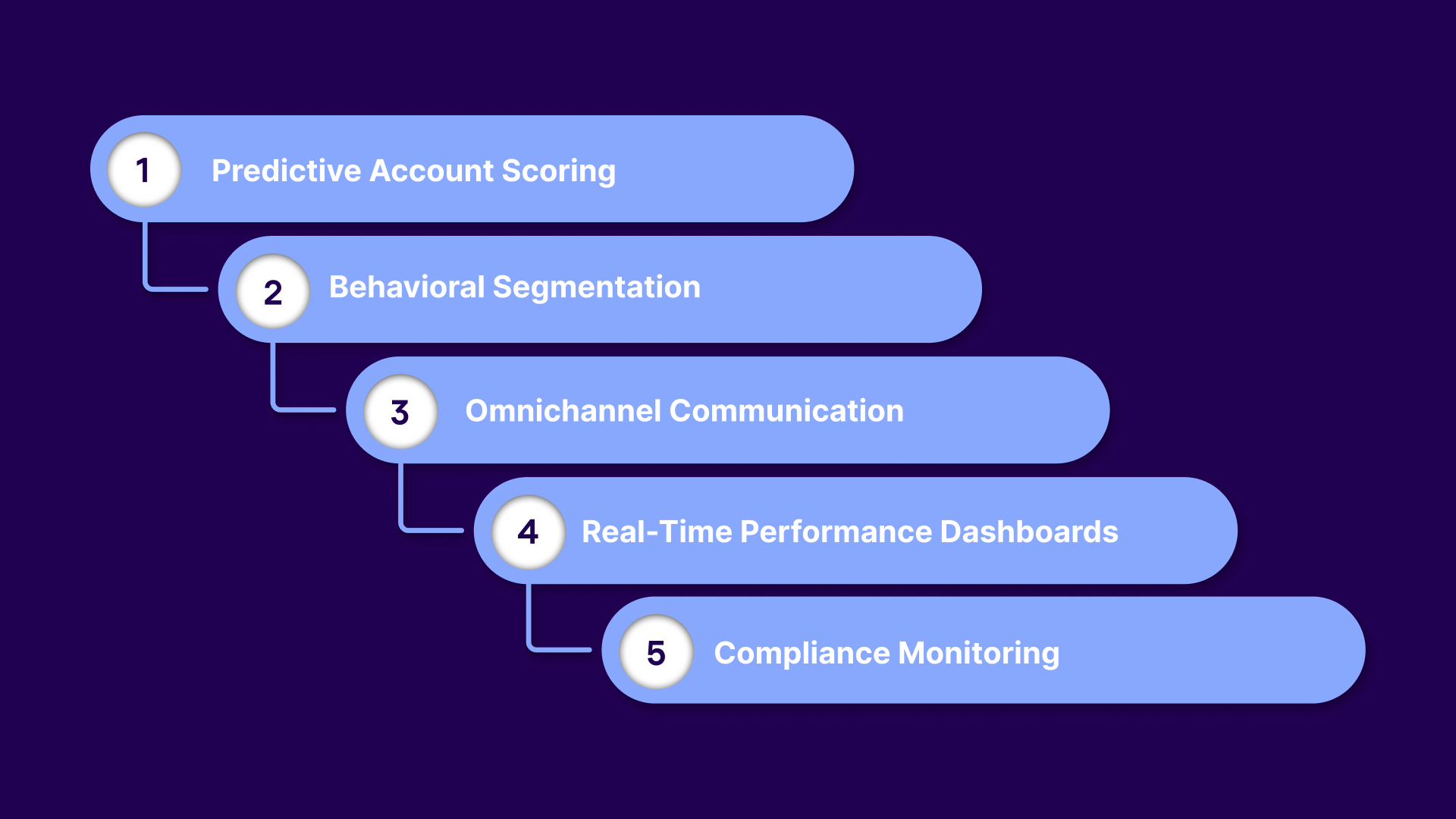

Key features include predictive account scoring, behavioral segmentation, automated workflows, performance dashboards, and compliance monitoring tools. These capabilities help organizations improve recovery efficiency while maintaining regulatory compliance.