Collections management rarely fails all at once. It slows down through missed follow-ups, outdated compliance rules, and inefficient payment processes. Over time, these gaps compound and lead to performance slips.

The problem isn’t effort. It’s the environment. Regulatory scrutiny is increasing, consumer expectations are shifting toward digital self-service, and manual systems aren’t keeping up. The Consumer Financial Protection Bureau (CFPB) continues to rank debt collection among the most common sources of consumer complaints in the US, largely driven by communication gaps.

For collection agencies, law firms, and credit issue companies, simplifying collections management now means reducing risk, improving recovery outcomes, and giving consumers clearer ways to resolve their accounts. This article outlines 10 practical ways to do exactly that, without compromising compliance or the consumer experience.

Collection management is the process of recovering unpaid balances in a structured, compliant way. It includes tracking overdue accounts, communicating with consumers, processing payments, and resolving disputes, all while maintaining accurate records.

For collection agencies, law firms, and credit-focused companies, effective collection management depends on having clear visibility into account data, consistent communication, reliable payment handling, and adherence to regulatory requirements. Teams need to know who owes what, when and how to make contact, and whether each action meets legal standards.

Modern collection management goes beyond manual follow-ups and phone calls. Digital systems now centralize account information, support self-service options, coordinate communication across channels, and automate routine tasks. When done well, this approach reduces risk, improves recovery outcomes, and creates a more predictable, consumer-friendly resolution process.

Suggested Read: Average Collection Period Formula: What it Is and How to Use it?

Collections teams are under pressure from both sides. Consumers want faster, clearer, and more flexible ways to resolve debt. Regulators are increasing scrutiny around communication practices, data handling, and recordkeeping. Managing this environment with manual processes or disconnected systems raises risk and slows recovery.

Simplifying collections helps organizations stay in control. Centralized data, built-in compliance, and digital self-service reduce errors, improve consistency, and allow teams to respond faster without increasing exposure.

Done right, simplifying collections management helps organizations:

This isn’t about doing more outreach. It’s about using the right channels, at the right time, supported by systems built for modern, compliant collections.

Suggested Read: Writing and Responding to Debt Collection Letters for Legal Clients

Now, let’s look at the tips and strategies to address the most common sources of friction in modern collections operations.

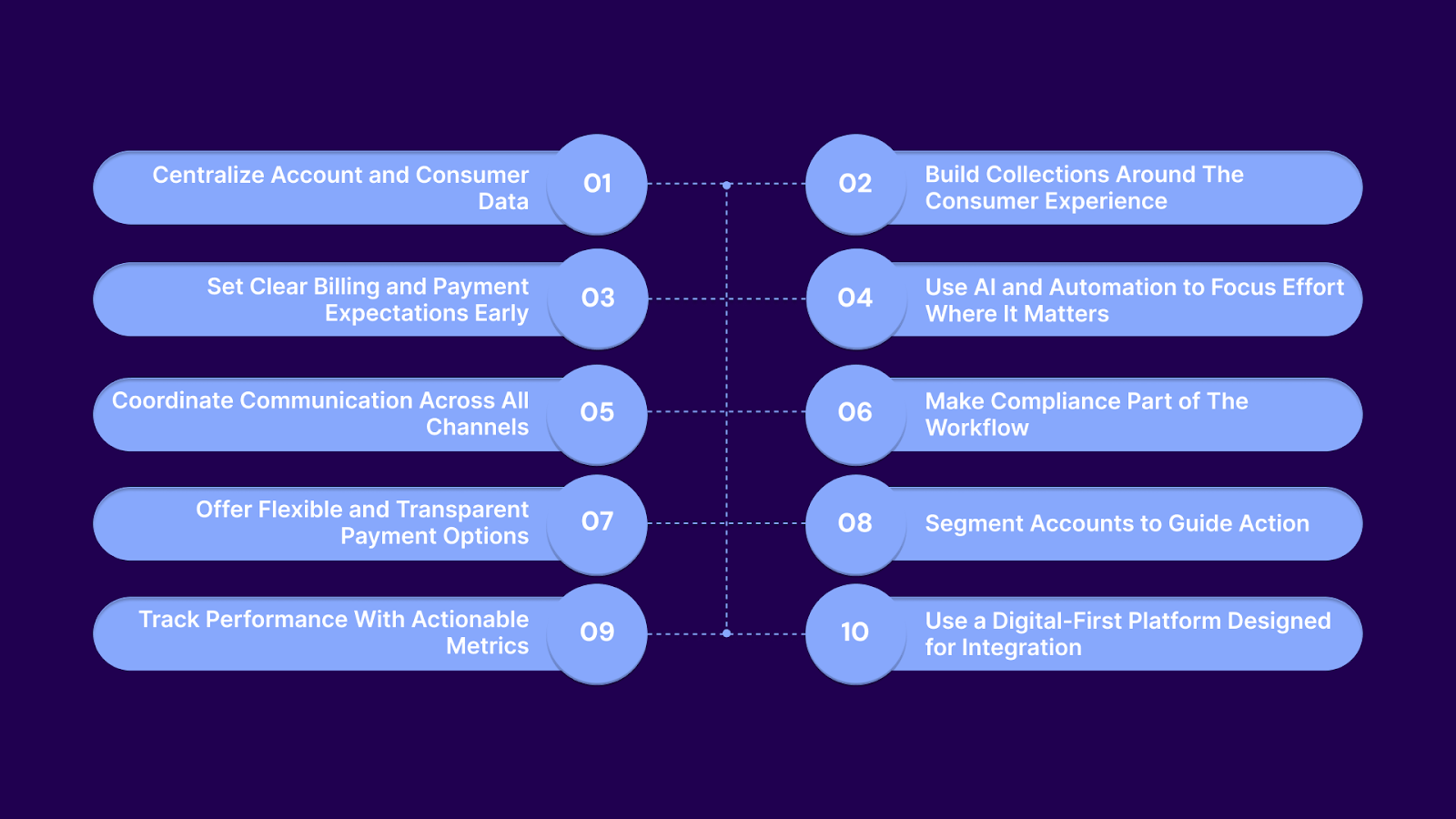

Simplifying collections isn’t about adding more tools or increasing outreach. It’s about removing friction across data, communication, payments, and compliance so teams can operate efficiently while consumers stay informed and engaged.

The strategies below focus on practical changes that bring structure, clarity, and consistency to modern collections operations.

Fragmented systems are a major barrier to effective collections. When account details, payment history, communication logs, and disputes live in separate tools, visibility breaks down. Errors increase, follow-ups repeat, and resolution slows.

A centralized system of record allows teams to:

Without a single source of truth, collections remain reactive instead of controlled.

Collections are no longer agent-only workflows. Many consumers prefer managing their accounts digitally, without repeated calls or manual follow-ups.

Consumer-first workflows prioritize:

When consumers can act on their own terms, agents can focus on higher-value and more complex cases.

Unclear terms create confusion and delay payment. Every invoice should clearly outline:

Clear policies align expectations from the start and support consistent action when payments are missed.

Automation is most effective when it removes repetitive work, not decision-making.

AI and workflow automation can:

This reduces manual effort and helps teams prioritize effectively.

Using multiple channels without coordination creates confusion. SMS, email, calls, portals, and IVR should work together, not in silos.

Effective multi-channel coordination includes:

Organized communication improves response rates and reduces complaints.

Compliance should not depend on memory or manual checks. With evolving rules under FDCPA and Regulation F, manual enforcement increases risk.

Built-in compliance controls help ensure:

Embedding compliance into workflows allows teams to move faster without increasing exposure.

Rigid payment demands slow recovery. Consumers engage more readily when they understand their options and can choose what fits their situation.

Simplified payment experiences include:

Transparency builds trust, and trust improves resolution rates.

Not all accounts require the same approach. Segmenting accounts helps teams focus effort where they will have the greatest impact.

Common segmentation criteria include:

Matching outreach to account type makes collections more efficient and less confrontational.

Data only helps when it drives decisions. Clear dashboards should highlight what needs attention now.

Useful collection metrics include:

This visibility allows teams to adjust early instead of reacting late.

Collections become harder when tools don’t work together. Manual handoffs, duplicate data entry, and reconciliation gaps increase risk and workload.

A digital-first platform supports:

When systems are designed to integrate from the start, collections can scale without adding complexity or headcount.

Suggested Read: The Ultimate Guide to Debt Collection and Recovery for Agencies

These strategies are most effective when supported by systems built to work together. The right technology platform turns simplification from an idea into a repeatable, scalable reality.

Tratta is built on the idea that simplifying collections management takes more than automation alone. It requires coordination across systems, clear consumer experiences, and compliance that works in the background, not as a separate layer.

As a digital-first collections technology platform, Tratta helps collection agencies, law firms, and credit issue companies bring their operations into a single, controlled environment.

Key capabilities include:

Tratta keeps collections consumer-focused and compliant, while giving organizations the structure they need to manage risk and scale responsibly.

Collections management doesn’t need to be complicated to be effective. By simplifying collections through centralized data, built-in compliance, and consumer self-service, organizations can reduce risk while improving recovery outcomes.

Simplifying collections is not a shortcut. It’s a deliberate strategy that brings consistency, control, and clarity to collections operations. If you want to see how it works, explore how Tratta supports simpler, more compliant collections. Book a demo to understand how a digital-first approach can strengthen your process and cash flow.

Collections generally fall into first-party collections, where businesses recover their own receivables, and third-party collections, where agencies or law firms collect on behalf of others. Each requires different workflows, compliance controls, and communication strategies

Collections management is the process of tracking unpaid accounts, communicating with consumers, collecting payments, and ensuring compliance throughout the recovery cycle. It combines data management, outreach, payments, and reporting into a structured operation.

The most effective collection strategies combine clear communication, flexible payment options, and consistent follow-up within legal limits. A balanced approach that uses automation for routine tasks and human judgment for sensitive cases delivers better outcomes.

When consumers can view balances, choose payment options, and manage accounts through self-service tools, engagement improves. This shortens resolution time, reduces call volume, and allows agents to focus on higher-value cases.

Yes. When automation includes built-in compliance controls, it reduces risk by enforcing contact rules, honoring opt-outs, using approved language, and maintaining audit-ready records across channels.

Digital and flexible payment options reduce friction for consumers. When payments are easy to understand and complete, consumers are more likely to follow through, leading to faster recovery and improved results.