Running a collection agency at volume means managing thousands of accounts across multiple debt types, with different contact histories, aging positions, and payment statuses all moving at once. The agencies that recover more from the same portfolio are usually the ones that can see where accounts stand in real time and act before balances become harder to resolve.

That is what receivables performance management is built for. It gives recovery teams a way to track account movement, payment behavior, contact outcomes, and aging risk in time to act, not after the next report confirms the problem.

Receivables performance management (RPM) is the process of monitoring, analyzing, and improving how completely and how quickly a collection agency collects on outstanding balances.

Every agency is running collections. RPM is the layer on top of that work that asks whether those efforts are producing the results the portfolio can support. A team can be active every day and still miss recovery opportunities because account priority, contact timing, or payment access is not being measured clearly enough.

In a collection agency context, RPM spans the full account lifecycle: assignment, outreach, consumer payment, and resolution. It tracks consumer payment rates, contact effectiveness, agent throughput, and reporting currency. For agencies managing portfolios across credit cards, auto loans, healthcare, utilities, and other debt types, RPM keeps account movement, payment activity, and recovery bottlenecks visible to the teams responsible for acting on them.

When receivables performance management breaks down, it rarely shows up as one isolated problem. It shows up through accounts that age further than they should, agents working the wrong queues, and consumers dropping out of payment flows they were ready to complete.

The operational consequences are specific:

In each case, the agency missed the signal early enough to act. The account aged further because no one had a current view of where it stood, what had already happened, and what should happen next.

Also read: Guide to Accounts Receivable Risk Management for Collection Agencies

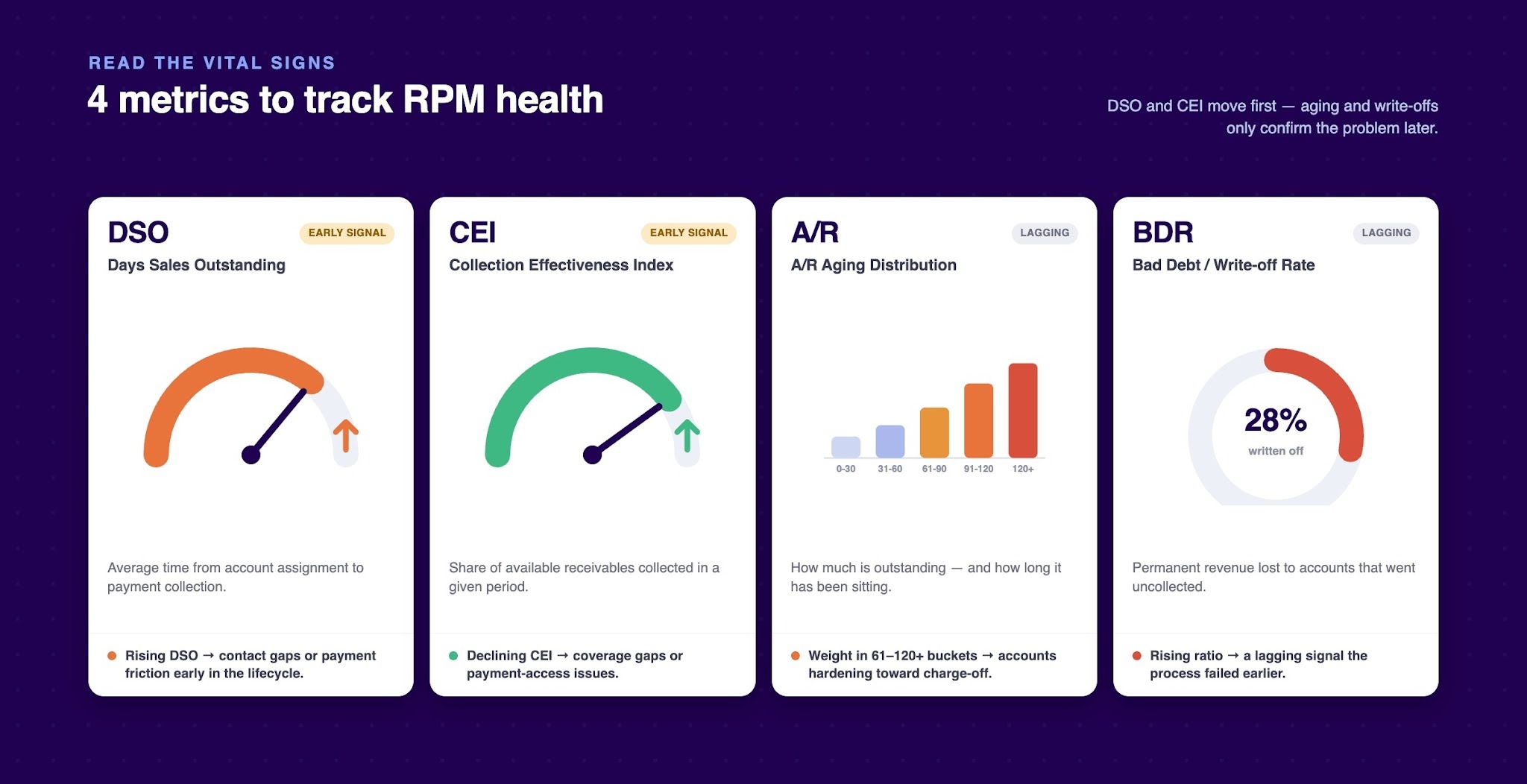

Measurement is where receivables performance management starts. These four metrics give operations leaders a clearer picture of where the recovery process is performing and where it is starting to slip.

For a collection agency, DSO can be adapted as an assignment-to-payment or placement-to-payment timing metric. CEI helps show whether the agency is collecting what should reasonably be collectible during the measured period.

Accounts typically move through aging buckets such as 0–30, 31–60, 61–90, 91–120, and 120+ days. Federal retail-credit guidance classifies open- and closed-end retail loans that are 90 days past due as substandard, while closed-end retail loans generally move to charge-off at 120 days and open-end retail loans at 180 days. That makes earlier aging buckets operationally important because teams still have more room to correct contact, payment, or priority gaps.

DSO and CEI are useful because they can move before write-off-related metrics do. If either is trending in the wrong direction, aging distribution and bad debt ratio often confirm the issue later.

Also read: Top 10 KPI Metrics for Effective Tracking of Accounts Receivable

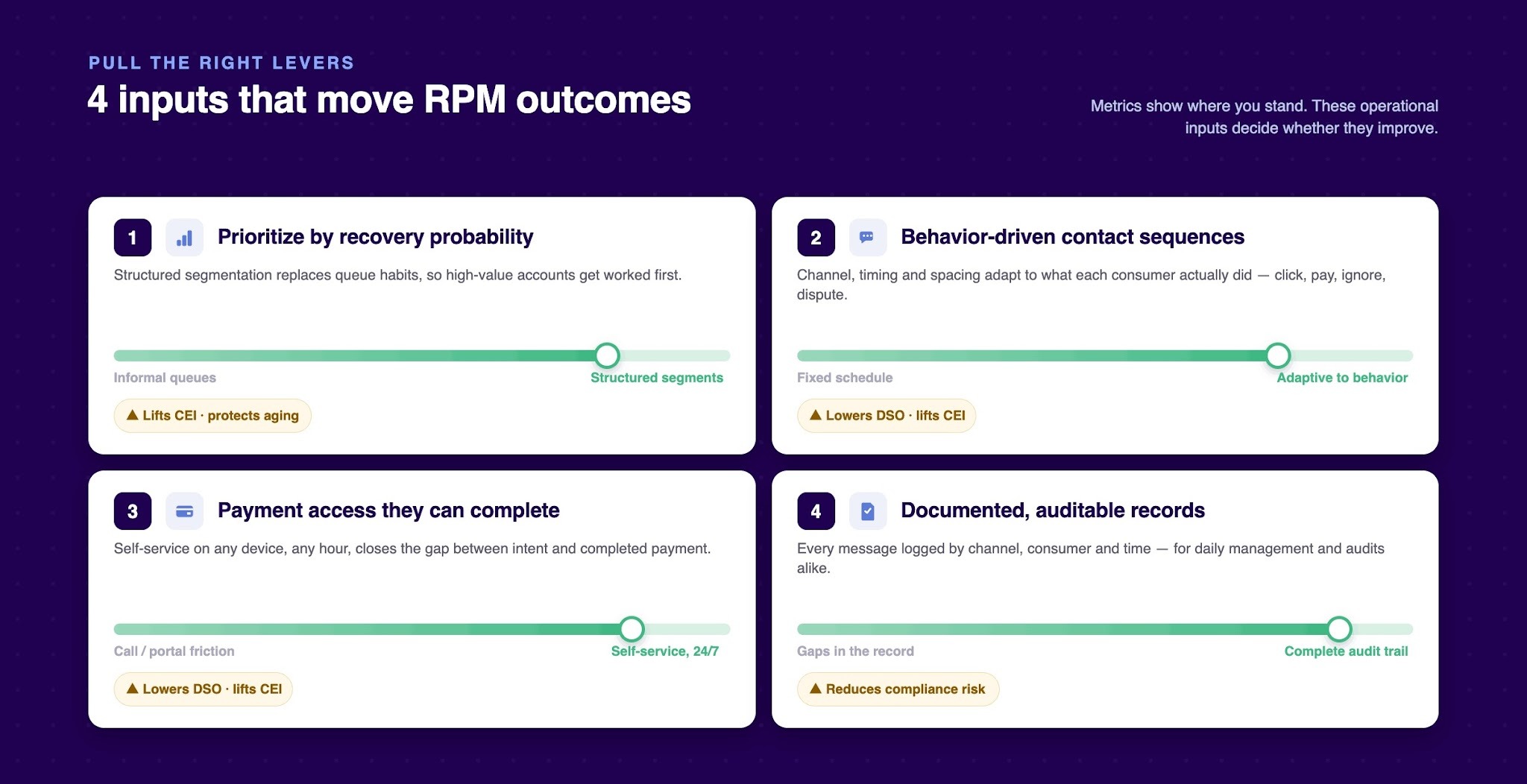

Metrics show where performance stands. These are the operational inputs that determine whether those numbers improve or get worse.

Accounts in a collection agency queue do not carry equal recovery probability. Balances differ by size, days outstanding, prior payment behavior, and consumer response to previous contact. When prioritization is informal, agents can spend time on low-probability accounts while higher-value assignments wait.

Structured segmentation replaces that variability with a repeatable process. The criteria for which accounts get worked first, and in what order, are defined by the operation rather than decided each morning by queue habits.

The timing, channel, and spacing of consumer contact affect how quickly balances reach resolution. A consumer who does not respond to a call may respond to a text the same afternoon. A consumer who clicked a payment link but did not complete the transaction needs different follow-up than one who has not responded at all.

Every contact attempt should be logged against the account record so the team knows what was sent, when, and how the consumer responded. Without that record, contact sequences repeat themselves even when they are not producing movement. The agency is sending outreach, but it is not managing account behavior.

When a consumer is ready to pay, the payment step becomes part of RPM. If payment requires a call during business hours, a difficult portal experience, or waiting for an agent, some consumers who intended to pay will not finish the transaction.

Self-service payment access, available at any hour on any device, can reduce the gap between consumer intent and completed payment. That can reduce payment delay and support stronger DSO and CEI trends.

Collection agencies operate under the FDCPA and related regulatory oversight. RPM needs documentation as well as performance measurement. Operations leaders need to know what communication went out, through which channel, to which consumer, and when.

That record matters for day-to-day account management. It also matters when an account is disputed, reviewed, or audited. A workflow with gaps in its documentation record creates risk even when the communication itself was appropriate.

Most RPM failures start when payment data, contact history, and reporting data are split across tools.

When payment systems, contact tools, and reporting sit in separate platforms, no one on the team has a complete picture of a given account. An agent sees the calls they made. The payment system shows a transaction. The report shows an aging bucket from a pull done earlier in the week. No one can see all three together for the account they are working right now.

The damage is often quiet: a consumer received three calls but no text, a partial payment had no follow-up, or an account stayed marked as active even though it had not responded in five weeks. These gaps accumulate across a portfolio and later show up in DSO, CEI, and write-off rate.

A common structural failure is outreach that runs on a fixed schedule instead of consumer behavior. Every account receives the same sequence regardless of where it is in the recovery process. A consumer who clicked a payment link and dropped off at the form receives the same next-step outreach as one who never acknowledged any contact.

When the outreach system cannot distinguish between those two situations, the agency is managing a calendar. RPM requires managing account-level behavior.

Weekly or manually compiled reports mean operations leaders make decisions from data that is already behind. By the time the team sees that a cohort of accounts has moved past 60 days, those accounts may already be further down the aging path.

Acting on an account at 45 days is different from acting at 75 days. Reporting lag shortens the window for correction before anyone realizes the window has changed.

Also read: Accounts Receivable Collection Policy Every Agency Should Follow

Tratta is debt collection software built for collection agencies, collection law firms, credit issuers, and debt buyers. It brings consumer payments, digital outreach, reporting, and workflow management into one connected platform, which addresses the tool gaps that often cause RPM failures in agencies.

For agencies, the operational impact is specific:

Explore Tratta's collection agency software to see how the platform fits your current workflows.

Also read: Overcoming the Top 10 Accounts Receivable Challenges for Collection Agencies

Receivables performance management tells collection agencies whether their recovery process is working at the level their portfolio allows, and where it is losing ground before the loss becomes harder to correct.

Metrics only help when collection managers and operations leaders can act on them quickly. Stronger RPM comes from contact sequences that respond to consumer behavior, payment access that removes avoidable friction, and reporting that gives operations leaders current account data during the workday.

If your team is still reconciling payment activity, outreach history, and aging reports across separate tools, schedule a demo to see how Tratta supports reporting, self-service payments, and workflow control for collection agency RPM.

Accounts receivable management covers the day-to-day work of tracking and collecting outstanding balances. Receivables performance management adds a measurement layer: using metrics like DSO, CEI, and aging reports to evaluate whether those processes are working and where they need adjustment. One is the work itself. The other is how leaders know whether the work is producing the right movement.

DSO and CEI are useful early signals because they reflect current process performance before losses are permanent. A rising DSO points to contact gaps or payment friction. A declining CEI suggests coverage problems or payment access issues. Bad debt ratio and aging concentration usually confirm what DSO and CEI show earlier, but by that point the accounts have already aged further.

There is no single day when every balance becomes difficult to recover. Risk usually rises as accounts move into later aging buckets and contact history grows stale. Federal retail-credit guidance treats 90 days past due as a key classification point and sets different charge-off timing for closed-end and open-end retail credit. Agencies generally have more room to act in the 0–60 day window, when contact and payment completion are more likely.

RPM disciplines apply regardless of agency size. Mid-size agencies often feel weak RPM more directly because they have less room for manual workarounds. A structured metrics framework and connected workflows matter when operational resources are tight.

Self-service payment access can reduce the delay between intent and payment completion. For agencies, that matters because fewer abandoned payment attempts can improve assignment-to-payment timelines and support stronger collection effectiveness. Consumers who run into friction, such as a required phone call, limited hours, or a difficult interface, are more likely to delay or abandon the payment.