Collection agencies are leaving money on the table: over 10% of accounts across 18 US industry segments are 90+ days overdue, according to a Dun & Bradstreet report. As overdue debt piles up, manual processes and fragmented systems make it harder to recover what’s owed, inflating Days Sales Outstanding (DSO) and increasing bad debt exposure.

In fact, manual workflows can add up extra days to DSO, compounding the operational cost of overdue accounts. With rising complexity and more customers choosing digital channels to manage payments, sticking to traditional, labour-intensive methods means missing out on faster resolutions and higher recovery rates.

In this blog, we will explore the critical challenges collection agencies face, why traditional methods fall short, and how adopting automation can help optimize collections processes, increase recovery rates, and enhance debtor engagement, driving efficiency and improving financial outcomes.

Across the United States, late and overdue payments are a widespread operational headache for collection teams, 55% of all B2B invoiced sales are now past due, and businesses often wait over 43 days to receive payment, putting sustained pressure on cash flow, staffing, and decision‑making.

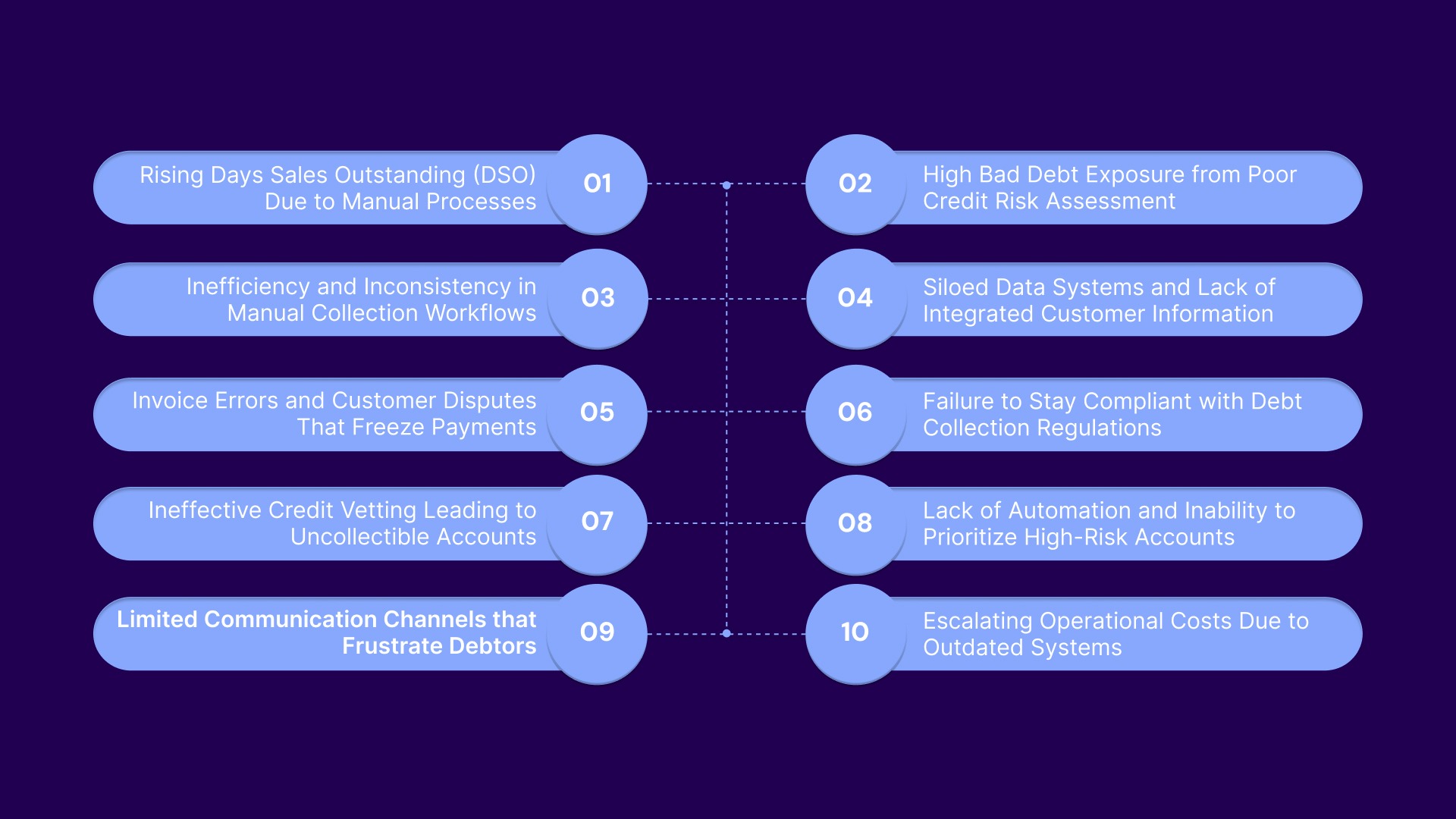

Below are the top 10 challenges collection agencies in the USA are grappling with, which consistently delay recoveries, drain resources, and erode profitability.

Manual collection methods extend DSO by 15-30 days, tying up working capital and creating a cash flow bottleneck. The slower accounts receivable process means agencies are waiting longer to collect what’s owed, which impacts day-to-day operations and the business's financial health.

Agencies face mounting bad-debt levels because credit assessments lack consistency and structure. Without a robust risk management strategy, high-risk accounts go unnoticed, forcing agencies to waste time chasing debts that will never be paid. This leads directly to inflated write-offs and serious financial losses.

Collection teams handling large account volumes manually are plagued by inconsistent workflows, some agents act promptly while others miss critical moments. This lack of standardization causes delayed follow-ups and lost opportunities, increasing time to recover funds.

Many collection agencies still operate with disconnected systems in which AR data, credit reports, and customer communication history are stored in separate tools or platforms. This fragmented data makes it impossible to obtain a real-time, holistic view of each account, preventing agencies from making timely decisions or identifying high-priority accounts that require immediate action.

Manual processes cost an average of $12 to $20 per invoice, compared to roughly $2 to $3 for automated processing. For high-volume AR operations, that gap compounds quickly.

Invoice errors and disputes freeze payments and restart the collection process. Incorrect billing amounts, missing information, or outdated contacts prompt costly delays. Every error diverts resources from collections to issue resolution, prolonging account closure. Agencies must prioritize accuracy to avoid these damaging bottlenecks.

Compliance is a growing concern, as collection agencies face increasing regulatory scrutiny. Manual processes are prone to human error, leading to non-compliance with laws such as the Fair Debt Collection Practices Act (FDCPA), state-specific regulations, and consumer protection laws. Agencies that fail to meet compliance requirements risk legal exposure, penalties, and reputational damage.

Without effective credit vetting, agencies extend credit to customers with poor repayment histories or no intention to pay, leading to wasted resources and increased risk exposure. Poor segmentation means high-risk accounts are handled ineffectively, raising delinquency rates.

Agencies lacking automation tools miss vital early intervention opportunities. Without predictive analytics, they do not flag at-risk accounts until it's too late, forcing teams to tackle accounts overdue by 90+ days when recovery rates are minimal. The cost of collections rises dramatically.

Relying on traditional collection methods like phone calls and emails leaves debtors frustrated and increases the likelihood of missed payments. Consumers now expect digital self-service options that let them manage their payments on their own time. Agencies that don’t offer multi-channel communication are losing touch with debtor preferences, making it harder to engage and collect effectively.

Outdated, manual systems create inefficiency and drive up operational costs for collection agencies. Paper-based processes, manual data entry, and redundant workflows require extra staff, reducing profitability and efficiency. Agencies must urgently modernize their systems to control costs and protect their margins.

When these gaps consistently affect recovery timelines, teams typically move toward platforms that let consumers resolve accounts independently while keeping all interactions compliant and auditable. Tratta's consumer self-service platform is built precisely for this operational need, reducing agent dependency while maintaining the compliance controls collection operations require.

Suggested Read: Guide to Accounts Receivable Risk Management for Collection Agencies

Top-performing accounts receivable teams deploy automation to eliminate operational obstacles and maximize recovery rates. Automated tools drive out inefficiencies, reduce manual labor, and minimize errors. Tratta consistently delivers modernization and tangible results for agencies.

AR automation optimizes collection processes in the following ways:

By offering a consumer self-service platform, agencies can reduce the burden on agents while allowing consumers to take control of their payments. Consumers can review balances, set up payment plans, and settle debts at their convenience. This flexibility speeds up collections, minimizes agent intervention, and improves debtor satisfaction.

An embedded payment system streamlines payments by integrating options into the collection platform. Debtors can pay instantly via credit card, bank transfer, or other methods, accelerating recovery and ensuring prompt processing, which directly reduces DSO.

To effectively communicate with a diverse debtor base, top AR teams are implementing multilingual payment IVR systems. These systems help facilitate collections by offering voice-based payment services in multiple languages. This feature ensures that language barriers don’t delay payments, improving debtor engagement and accelerating recovery.

Top AR teams are adopting omnichannel communications to reach debtors across various platforms: SMS, email, phone, and online portals. This approach meets the debtor where they are, ensuring that messages are received and acted upon promptly. By diversifying communication channels, agencies can increase engagement and resolve payments faster.

Automated campaign management ensures that all accounts are consistently followed up on, with reminders and actions tailored to each account's status. Agencies can schedule collection efforts, automatically escalate issues, and ensure timely follow-ups, improving efficiency and preventing accounts from being overlooked.

Advanced reporting and analytics give AR teams the tools to monitor key metrics like DSO, recovery rates, and payment trends. This data allows agencies to make informed decisions about collection strategies, prioritize high-risk accounts, and track their progress toward financial goals. Real-time analytics enable quick adjustments to improve collection efforts.

Every agency has unique operational needs, and the ability to customize workflows and processes is essential for success. With the flexibility to adapt processes, AR teams can configure automated systems to align with their specific collection strategies. This customization ensures that collections processes are as effective as possible, tailored to each agency’s requirements.

Data integration is crucial for ensuring that all systems work together. REST APIs enable AR teams to integrate existing systems, such as CRM and ERP, with their collection platform. This integration ensures seamless data flow, reduces manual data-entry errors, and provides a unified view of each account, enabling better decision-making and faster collections.

Compliance is a significant concern in debt collection. Automated systems help agencies maintain compliance with laws such as the Fair Debt Collection Practices Act (FDCPA), state-specific regulations, and other industry standards. Automated workflows ensure that each communication is compliant, auditable, and fully documented, reducing legal risks and ensuring transparency in all interactions.

Several collection teams have reported measurable improvements after implementing modern automation tools. For example, a commercial fleet card issuer recovered over $650,000 in just seven months, with card payments nearly doubling as consumers adopted self‑service payment options.

If your team aims to achieve similar recovery outcomes and reduce operational friction, consider scheduling a discussion to explore strategies tailored to your agency’s needs.

Must Read: Accounts Receivable Automation vs Manual Processes Explained

Tracking AR performance without a consistent set of metrics is like managing a portfolio without seeing the positions. The table below covers the benchmarks that matter most for US-based collection operations:

Manual AR operations face a widening performance gap relative to competitors that have automated core processes. The direct cost difference is not marginal.

Beyond direct costs, teams that do not address the structural issues covered here will continue to see DSO creep upward, bad debt exposure rise, and staff capacity consumed by tasks that do not require human judgment. The compounding effect of those losses outpaces the cost of fixing the underlying process.

The shift required is not just a software decision. It starts with an honest assessment of where the current process actually breaks, and building workflow standards that do not depend on individual effort to function.

For teams ready to evaluate a consumer self-service platform that reduces agent dependency while maintaining compliance, explore what Tratta offers, starting with your current DSO and bad debt baselines. From there, the case for change builds itself.

The most common issues are slow payment cycles driven by manual processes, poor credit risk segmentation leading to high-risk portfolios, and inconsistent collection workflows that create compliance exposure. Data silos that prevent real-time visibility into account status compound all three.

It depends on the industry. Retail typically runs 5 to 20 days, professional services 30 to 60 days, and construction 60 to 90 days or more. A practical target is to match or beat your industry median. A DSO exceeding your payment terms by more than 50% warrants immediate review.

Bad debt expense running above 2% of revenue typically signals a structural credit policy problem. At $50 million in annual sales, a 2% bad debt rate represents $1 million in annual write-offs. Reducing that rate to 1% through better credit segmentation and earlier intervention frees $500,000 in recovered revenue.

Yes, when implemented with proper workflow controls. Automated reminder systems that trigger based on aging thresholds ensure consistent, documented outreach. Platforms that provide consumer self-service portals allow debtors to resolve accounts independently, reducing agent contact and the associated compliance risk.

DSO measures the average time receivables have been outstanding. CEI measures how effectively your team is collecting the receivables actually available for collection in a given period. A business can have a low DSO but poor CEI if it is only collecting easy accounts. Together, the two metrics provide a more complete picture of AR performance.

DSO can rise even without revenue growth when billing accuracy declines, approval cycles slow down, or customers begin stretching payment terms due to macroeconomic pressure. In many cases, internal inefficiencies such as delayed invoicing or weak follow-up discipline are the primary drivers rather than customer behavior alone.

Even a small percentage of disputed invoices can disproportionately affect cash flow because payment is paused until resolution. If disputes are not tracked and resolved within defined timelines, they create a backlog that artificially inflates receivables and increases aging risk across the portfolio.

High-performing teams typically review key AR metrics weekly rather than monthly. Weekly tracking helps identify early deterioration in payment patterns, aging trends, or collection gaps before they become structural issues that affect quarterly cash flow targets.

9. How does customer segmentation improve collection efficiency?

Segmentation allows AR teams to prioritize effort based on risk and payment behavior. Instead of treating all accounts the same, high-risk customers receive earlier reminders and tighter follow-ups, while low-risk accounts follow standard cycles. This reduces wasted effort and improves overall recovery rates.

Timing directly affects response rates and payment behavior. Early, consistent, and predictable communication aligned with invoice aging stages leads to faster resolution. Irregular or delayed outreach often results in longer delinquency periods and reduced customer responsiveness.

Note: This content is for informational purposes only and does not constitute legal or financial advice. Tratta recommends consulting legal counsel to ensure compliance with applicable laws related to your collection and outreach activities.