Handling card payments in third-party collections is a critical risk point for law firms. Sensitive payment data often moves across calls, portals, and internal workflows without consistent control over its capture, processing, or storage. The exposure is significant.

According to IBM Security, the average cost of a data breach reached $4.40 million in 2025. Such incidents can disrupt operations, erode client trust, and invite regulatory scrutiny. Where manual processes still exist, the likelihood of gaps increases.

This 2026 guide to PCI-compliant debt collection for law firms outlines core compliance requirements, identifies common vulnerabilities, and explains how to secure payment workflows in a third-party collections environment.

Brief look:

PCI compliance refers to adherence to the Payment Card Industry Data Security Standard (PCI-DSS), a global framework designed to protect cardholder data during storage, processing, and transmission. For law firms engaged in third-party collections, PCI compliance is not limited to IT infrastructure.

It extends to operational workflows, agent interactions, and how payment data flows across systems. Any environment that touches cardholder data falls within scope, making compliance both a technical and procedural requirement.

Importance of PCI compliance for law firms in third-party collections:

The scope of PCI compliance becomes more complex in third-party collections, where law firms act on behalf of creditors and manage external payment flows. In the next section, it is important to clarify whether these requirements formally apply to such firms and how responsibility is defined.

Suggested Read: 2026 Guide to PCI-Compliant Card-Not-Present Debt Payments for Agencies

PCI compliance applies based on how payment data is handled, not simply the role of the law firm. In third-party collections, firms may fall within scope if they store, process, or transmit cardholder data. Where payment handling is fully outsourced to a PCI-compliant provider, the firm’s scope may be reduced, but not entirely eliminated.

The scope and responsibility typically depend on the following factors:

Tratta reduces PCI scope by tokenizing card data at capture and avoiding storage of raw data. Its payment workflows embed secure data handling, access controls, and audit readiness, enabling law firms to manage third-party collections with minimized exposure and compliant operations. Get in touch with us to learn more.

Generic collection tools are often designed for broad use cases rather than the regulatory and operational demands of law firms handling third-party collections. They may support basic payment workflows, but they rarely account for how card data exposure, audit requirements, and legal accountability intersect in this environment.

These limitations typically show up in the following areas:

These gaps directly affect compliance, operational efficiency, and payment outcomes. In the next section, we break down the specific features that enable secure, PCI-aligned payment handling.

Suggested Read: The IVR Payment Gap: What Most Debt Collectors Are Missing in 2026

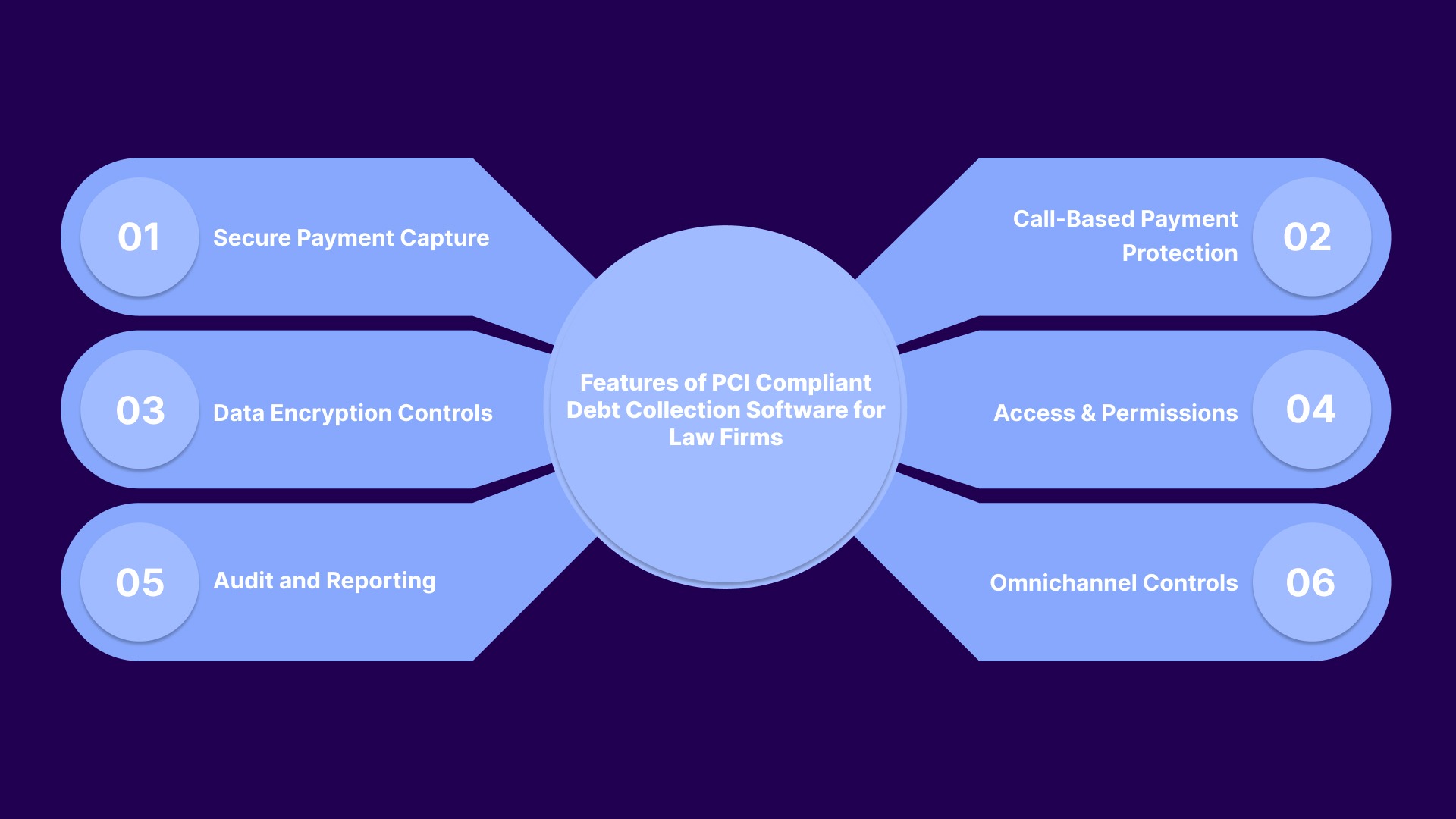

PCI compliance in collections is driven by how payment data is captured, processed, and secured across workflows. For law firms handling third-party collections, the right software must reduce exposure to card data while maintaining audit-ready operations.

The following features define what a compliant, low-risk infrastructure should look like.

Payment data must be collected in a way that avoids unnecessary exposure across systems and agents. This includes shifting payment entry away from manual handling toward controlled, secure environments.

Key capabilities typically include:

Phone payments are one of the highest-risk areas for PCI scope expansion. Without safeguards, card data can be captured in recordings, agent notes, and internal systems.

To mitigate this, solutions should provide:

Cardholder data must be protected both in transit and at rest to meet PCI requirements. Encryption ensures that even if data is intercepted, it cannot be misused.

Effective systems include:

Limiting who can access sensitive data is central to reducing compliance risk. Role-based controls help prevent unnecessary exposure within the organization.

Core controls include:

PCI compliance requires clear visibility into how payment data is handled. Audit trails and reporting ensure accountability and support regulatory reviews.

Important capabilities include:

Collections workflows span multiple channels, each introducing potential exposure points. Compliance must extend across every interaction where payments are initiated.

Solutions should support:

Tratta is built to minimize direct interaction with card data by shifting payments into secure, consumer-driven workflows. Its infrastructure embeds encryption, access controls, and audit tracking directly into the platform, reducing reliance on manual processes. Schedule a free demo today.

PCI compliance plays a central role in managing financial, legal, and operational risk in debt collection. Law firms handling third-party collections operate in environments where payment data moves across multiple systems and interactions.

The importance of PCI compliance is reflected across the following areas:

These factors make PCI compliance an operational requirement for law firms. In the next section, the focus shifts to the practical steps required to implement PCI-compliant collection workflows in a law firm environment.

Suggested Read: Debt Collection and Secure Payment Portal

Implementing PCI compliance involves aligning payment workflows, internal processes, and vendor relationships to reduce exposure to card data across third-party collection activities. A structured approach ensures that compliance is embedded into daily operations rather than treated as a one-time requirement.

The following steps outline how to operationalize PCI-compliant collections:

These steps help embed compliance into both technology and operations, reducing risk across third-party collection workflows. In the next section, a practical checklist outlines how to validate whether your firm’s processes and systems meet PCI compliance expectations.

Suggested Read: Innovative Approaches to Future Debt Collection Strategies

PCI compliance is best validated through clear, repeatable controls across systems and workflows. A checklist approach helps confirm whether payment handling, data security, and operational processes align with PCI DSS expectations.

The checklist below outlines key areas to review.

PCI compliance requires continuous validation across workflows, systems, and teams. A structured checklist, supported by purpose-built technology, helps law firms maintain secure, compliant, and scalable third-party collection operations.

Without a PCI-compliant infrastructure, payment workflows can expose sensitive card data at multiple points, increasing the risk of breaches, regulatory penalties, and operational disruption. Manual handling, fragmented systems, and unclear compliance ownership often lead to audit failures and loss of client trust in third-party collections.

Tratta addresses these risks by embedding secure payment capture, controlled data flows, and audit-ready compliance directly into collection workflows. Its architecture reduces direct exposure to card data while supporting scalable, compliant operations for law firms handling third-party recovery.

Get started with a platform designed for audit-ready, PCI-aligned collections. Book a free demo to see how Tratta helps secure your payment workflows and reduce compliance risk.

PCI-compliant debt collection for law firms refers to managing payment workflows in a way that meets Payment Card Industry Data Security Standard requirements. This includes secure payment capture, restricted access to card data, encryption, and audit-ready processes across third-party collection activities.

Yes, if the firm stores, processes, or transmits card data. The scope depends on how payments are handled, but any exposure to card information brings the firm under Payment Card Industry Data Security Standard requirements.

The 80/20 rule, based on the Pareto Principle, suggests that a majority of recoveries often come from a small portion of accounts. In collections, this guides prioritization and resource allocation.

Costs vary based on scope, systems, and workflows. Smaller firms using secure payment providers may incur minimal direct costs, while larger firms with broader data exposure may face higher expenses for audits, controls, and infrastructure.

Firms can reduce scope by limiting direct handling of card data, using secure payment portals, tokenization, and minimizing agent-assisted payments. Aligning workflows with compliant systems helps lower risk and simplify audits.