Automation is rapidly reshaping how credit operations are managed. The financial process automation market is expected to reach nearly $50 billion by 2033, growing at a 15% CAGR. The growth reflects a clear industry shift away from manual financial workflows.

For collection agencies, where compliance, documentation, and payment handling must be precise, manual processes increase operational risk. Credit process automation enables standardizing tasks, reducing errors, and managing accounts with greater consistency.

In this article, we examine where risk arises in the collections process and how credit process automation helps agencies manage it more effectively.

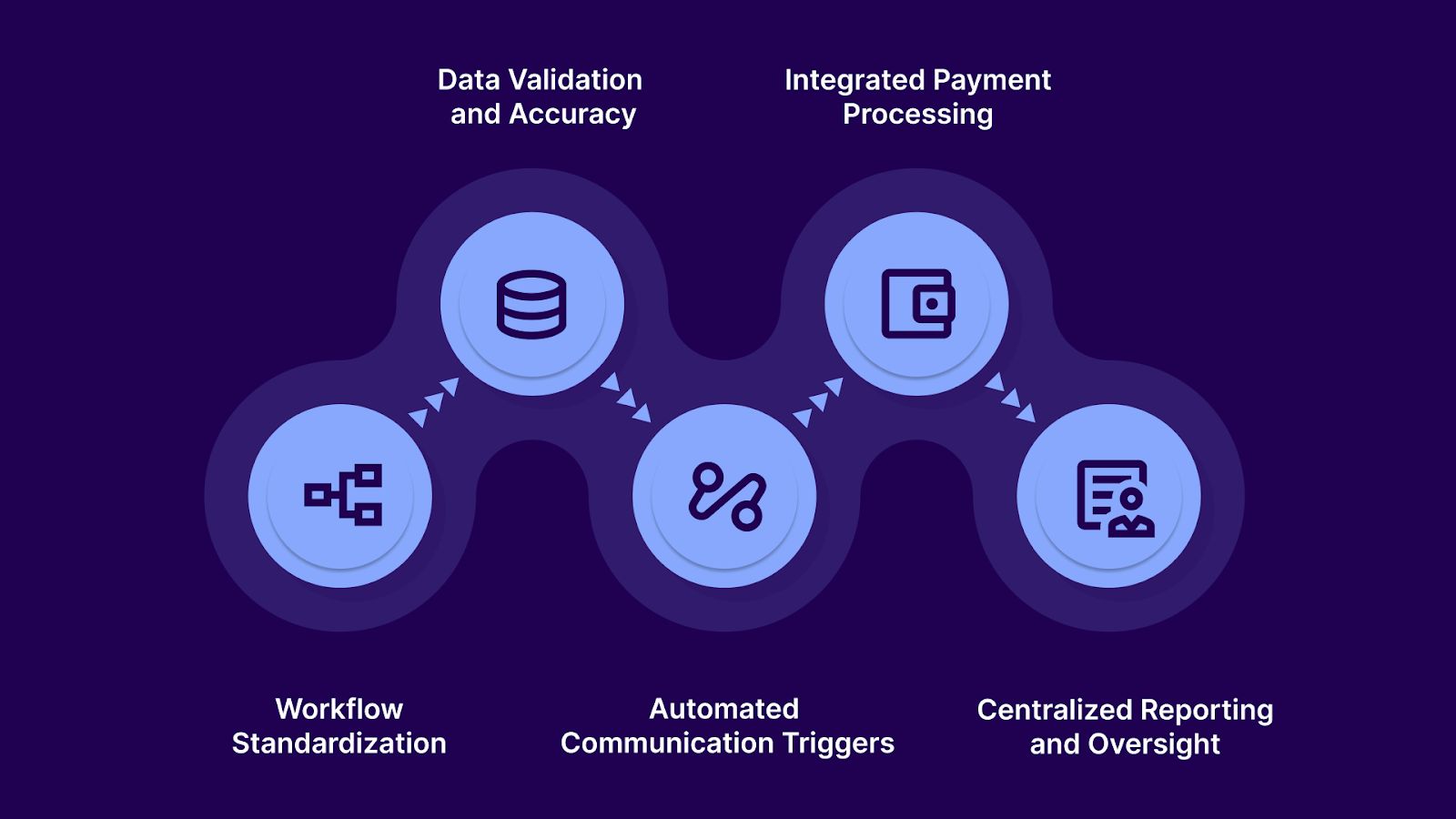

Credit process automation refers to the use of technology to standardize and manage tasks across the credit lifecycle. Instead of relying on manual reviews, spreadsheets, and disconnected systems, automation applies defined rules, data validation, and workflow triggers to move accounts through each stage more consistently.

Key elements of credit process automation include:

As collections become more regulated and operational demands increase, structured automation is moving from a convenience to a strategic necessity. The next section explores why credit process automation is necessary in collections.

Suggested Read: Why Credit & Collection Policies Matter in 2026

Collection work involves constant movement between data, communication, compliance checks, and payment tracking. When these steps rely heavily on manual input, gaps begin to appear.

Common areas where manual processes struggle include:

Understanding these operational gaps helps explain why automation is gaining attention across the industry. To see how it addresses these challenges, it helps to look at where automation directly reduces risk for debt collection agencies.

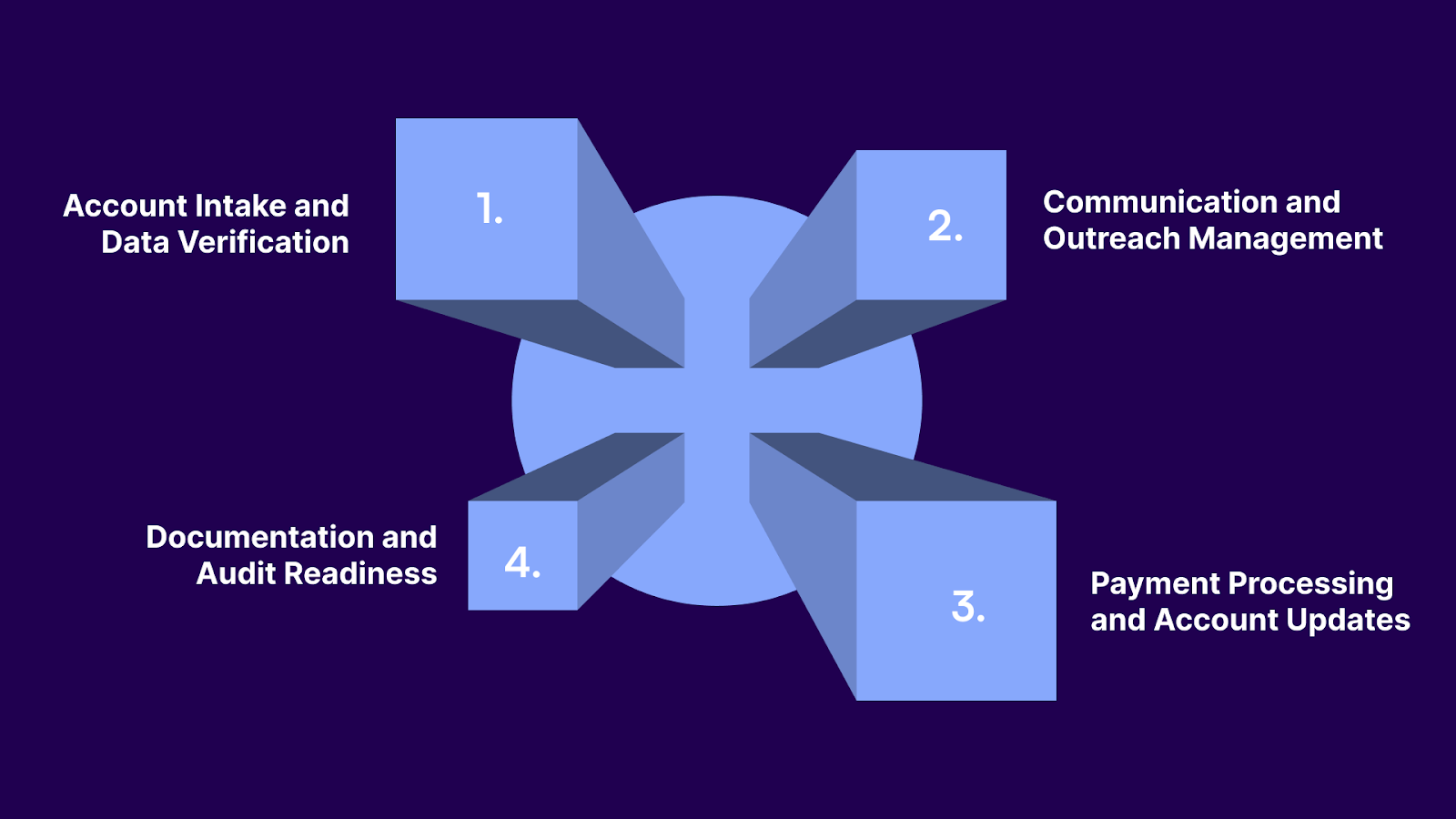

Risk in collections builds when small process gaps accumulate across account handling, communication, documentation, and payments. Automation helps reduce that exposure by structuring how work moves through each stage of the collections lifecycle.

The first risk arises when accounts are added to the system. Incomplete data or incorrect information can affect every step that follows. Automation helps standardize the process of reviewing and preparing accounts before the collection activity begins.

Automation typically supports this stage through:

Consumer communication is one of the most sensitive areas in collections. Manual outreach can lead to missed follow-ups, inconsistent messaging, or timing issues. Automated workflows help ensure outreach complies with defined policies and schedules.

Automation helps manage communication through:

Payments introduce operational and reconciliation risks when handled manually. Delays in updating balances or recording transactions can create confusion for both agencies and consumers. Automation helps keep payment activity synchronized with account records.

Automation helps stabilize this stage by enabling:

Collections activity must be documented clearly to support disputes, audits, or regulatory reviews. Manual documentation often leads to missing notes or inconsistent records. Automation ensures actions are logged and stored consistently.

This typically includes:

Tratta centralizes these controls within one system, giving agencies a clearer view of their collections process. Communication, payments, and account activity are managed through consistent workflows rather than scattered tools. The result is greater operational control and fewer process gaps. Schedule a free demo today.

Automation reshapes how accounts are prioritized, managed, and resolved across the portfolio. The benefits are most visible in areas where agencies traditionally struggle to maintain consistency and control.

These are a few reasons to invest in a credit process automation tool:

Understanding these outcomes is helpful, but realizing them requires thoughtful implementation. The next section outlines the key steps agencies should follow when introducing credit process automation into their operations.

Suggested Read: Credit Management Automation: Benefits and Steps

Credit process automation often begins earlier in the credit lifecycle, during lending and credit evaluation. Decisions made at this stage influence risk exposure, repayment behavior, and eventual collection outcomes.

This is how you can make credit decisions more consistent and reliable.

Decisions made during lending shape how accounts behave later in the credit lifecycle. When those accounts move into collections, Tratta helps agencies manage them with structured automation rather than manual coordination.

Features such as automated communication workflows, self-service payment options, account segmentation, and real-time payment posting help teams maintain consistency while keeping recovery activity controlled and traceable. Get in touch with us to learn more.

Automation becomes most effective when agencies reach a point where manual processes begin to limit consistency and oversight. Recognizing the following signals helps agencies determine when it is time to move toward more structured systems.

These signs are:

Recognizing these signs helps agencies determine whether their operations are ready for automation. The next step is to understand what needs to be in place before implementing automated credit processes.

Suggested Read: Guide to Debt Relief Process Automation for Delinquent Account Recovery

Without clear processes, accurate data, and defined policies, automation simply moves problems faster instead of solving them. Before implementing credit process automation, agencies need to put several essentials in place.

This is how you can make your agency ready for credit process automation:

You need to establish how accounts should move through your organization:

You need to ensure the information powering automation is accurate and consistent:

You need to clarify the rules that guide outreach and documentation:

You need to prepare teams to work within automated systems:

With clear processes, reliable data, and aligned teams, automation becomes far easier to implement effectively. The focus then shifts to the systems that can support these workflows and keep them running consistently. The right tools can help translate well-defined processes into structured, day-to-day operations.

Suggested Read: Automated Credit Decisioning in Collections: A Practical Guide

Tratta is a debt collection and payment platform designed to help agencies manage communication, payments, and recovery workflows more efficiently. It combines consumer engagement tools, payment infrastructure, automation, and reporting to support the full collections lifecycle. Instead of relying on disconnected systems, agencies can manage key collection activities through structured tools built specifically for recovery operations.

Below are the core capabilities that help agencies implement automation more effectively:

This portal allows consumers to log in, view balances, upload documents, and resolve accounts independently. Giving consumers control often increases engagement while reducing agent workload.

Tratta supports secure payment processing and multiple payment methods. Transactions are updated quickly, helping agencies maintain accurate balances and perform reconciliations.

The IVR system enables consumers to make payments or interact with accounts through automated phone options. Multilingual access improves reach and accessibility across different customer groups.

Agencies can connect with consumers through phone, SMS, and email. Coordinated communication helps maintain consistent outreach and engagement across channels.

Campaign tools allow teams to segment accounts, schedule outreach, and trigger actions based on consumer behavior. This helps agencies run structured recovery strategies at scale.

Dashboards and reporting tools provide visibility into payments, interactions, and recovery performance. These insights help agencies refine strategies and monitor progress across portfolios.

Tratta allows agencies to configure workflows, policies, and messaging to match their internal processes. This flexibility helps organizations adapt the system to their operational rules.

APIs and integrations allow Tratta to connect with other systems used by agencies. This helps maintain data synchronization and supports existing workflows.

The platform includes built-in compliance and security controls, including standards such as PCI DSS and SOC 2. These safeguards help agencies manage regulatory obligations and protect sensitive payment data.

These features help agencies move away from fragmented manual processes and toward structured, technology-supported workflows. By combining communication, payments, reporting, and compliance tools, Tratta enables collection teams to operate with greater control and efficiency.

Without structured processes, collection operations can quickly become inconsistent and difficult to manage. Missed follow-ups, inaccurate records, communication gaps, and compliance oversights can quietly build risk across a portfolio.

Tratta helps agencies manage credit and collections activity with greater consistency. It supports automated communication, structured workflows, real-time payments, and clear reporting. The platform can help you reduce risk while giving your team better visibility and control.

If your agency is starting to feel the limits of manual processes, it may be time to rethink how work moves through your organization. Schedule a free call today.

Credit process automation often refers to automating credit decisions and account management earlier in the credit lifecycle. Collections automation focuses specifically on managing delinquent accounts, communication, and payment resolution.

Implementation timelines vary depending on the size of the agency, existing systems, and data readiness. Many agencies begin seeing operational improvements within a few months of deployment.

Yes. Even smaller agencies can benefit from automation by reducing manual tasks, improving organization, and maintaining consistent communication with consumers.

No. Automation handles repetitive tasks such as scheduling outreach, updating records, and processing payments. Agents can then focus on negotiations, dispute resolution, and complex cases.

Automation helps agencies follow defined communication rules, maintain records, and document interactions more consistently, which can reduce the likelihood of compliance errors.