Inconsistent credit and collection practices can slow recoveries and create compliance risks for collection agencies. When teams rely on informal processes, follow-ups become inconsistent, documentation gaps appear, and account resolution takes longer than necessary.

These challenges are becoming more common as delinquent debt grows. According to the Federal Reserve Bank of New York, about 4.8% of U.S. household debt was delinquent at the end of 2025.

For collection agencies handling large portfolios, this pressure is familiar. More accounts mean more decisions about when to escalate, negotiate, or close cases. Without clear policies, those decisions often vary across teams and systems.

That is why strong credit and collection policies matter more than ever. In this article, we explain why they matter in 2026 and outline the key elements agencies should include when strengthening their collection frameworks.

Quick look:

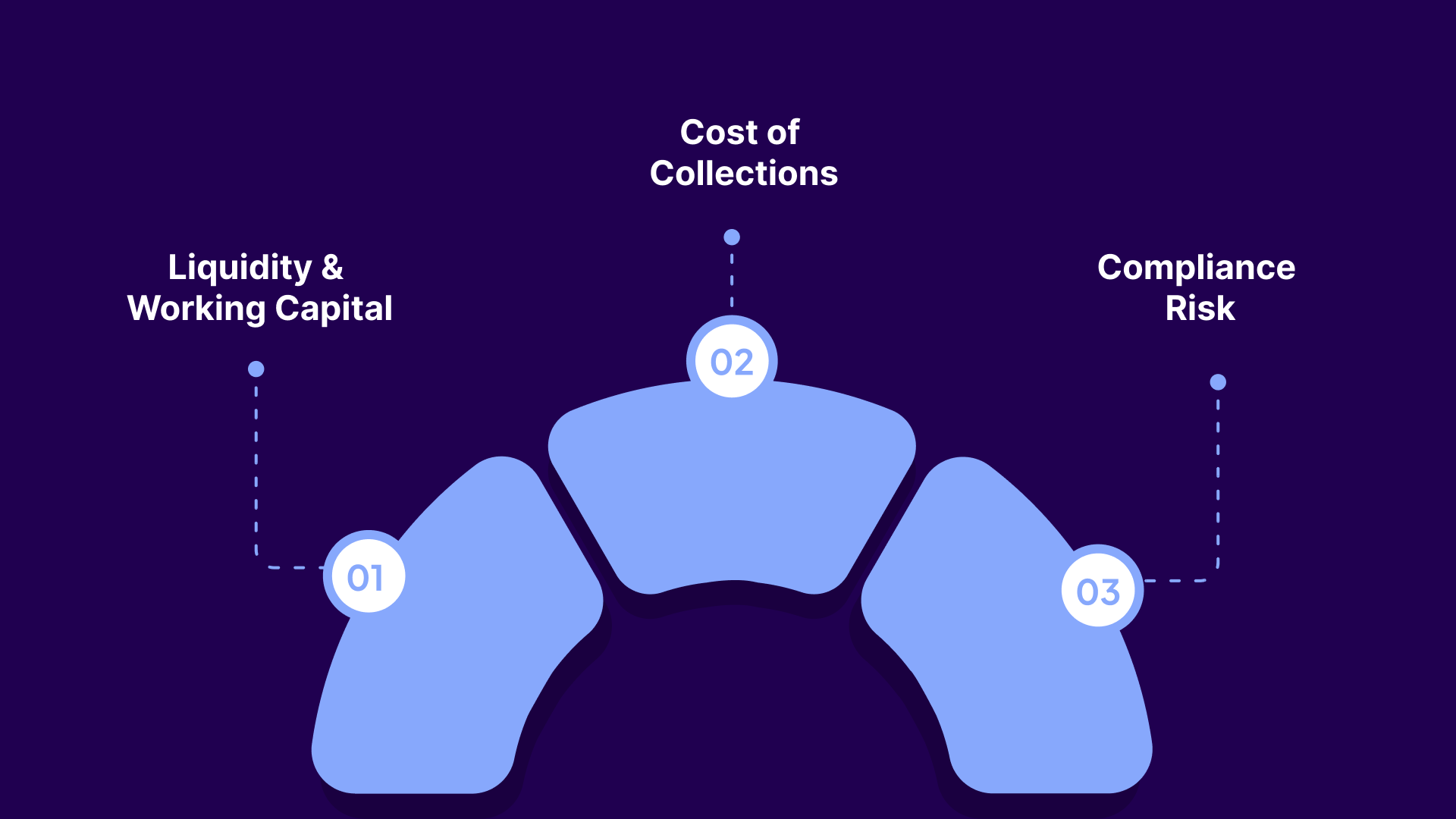

Agencies that manage large numbers of accounts rely heavily on predictable payment behavior. When credit and collection steps vary across teams or are left to individual discretion, recovery becomes harder to forecast.

A clearly defined policy establishes how accounts are managed and progress through the collection workflow. This prevents delays, reduces confusion, and creates a consistent experience for both staff and consumers.

Strong policies influence several operational and financial outcomes:

When credit terms and collection follow-ups are consistent, agencies gain more accurate visibility into when payments are likely to arrive. This gives agencies clearer visibility into expected recoveries and cash flow from collections.

Unstructured processes lead to repeated manual work, extended call times, higher litigation costs, and unnecessary escalation. A documented approach helps teams manage accounts efficiently, reducing time spent on each case.

Policies ensure communication, documentation, disclosures, and account-handling steps follow federal and state guidelines. This reduces the risk of disputes, regulatory issues, or consumer complaints.

Operational visibility helps teams understand how these levers affect recovery outcomes. Tratta offers Reporting and Analytics to track payment patterns, recovery performance, and workflow efficiency, helping agencies monitor liquidity, collection costs, and compliance exposure. Schedule a free demo today.

When teams follow clear procedures, decisions become consistent, workflows move faster, and recovery outcomes become easier to predict. Without that structure, processes vary across staff and systems, leading to delays, higher costs, and inconsistent results.

Table showing the operational impact of credit and collection policies:

To deliver consistent results across teams and portfolios, these policies must translate into clear structures that guide everyday decisions and workflows. The following components outline what makes a credit and collection policy effective in practice.

Suggested Read: Guide to Choosing a Credit Management Platform for Collections

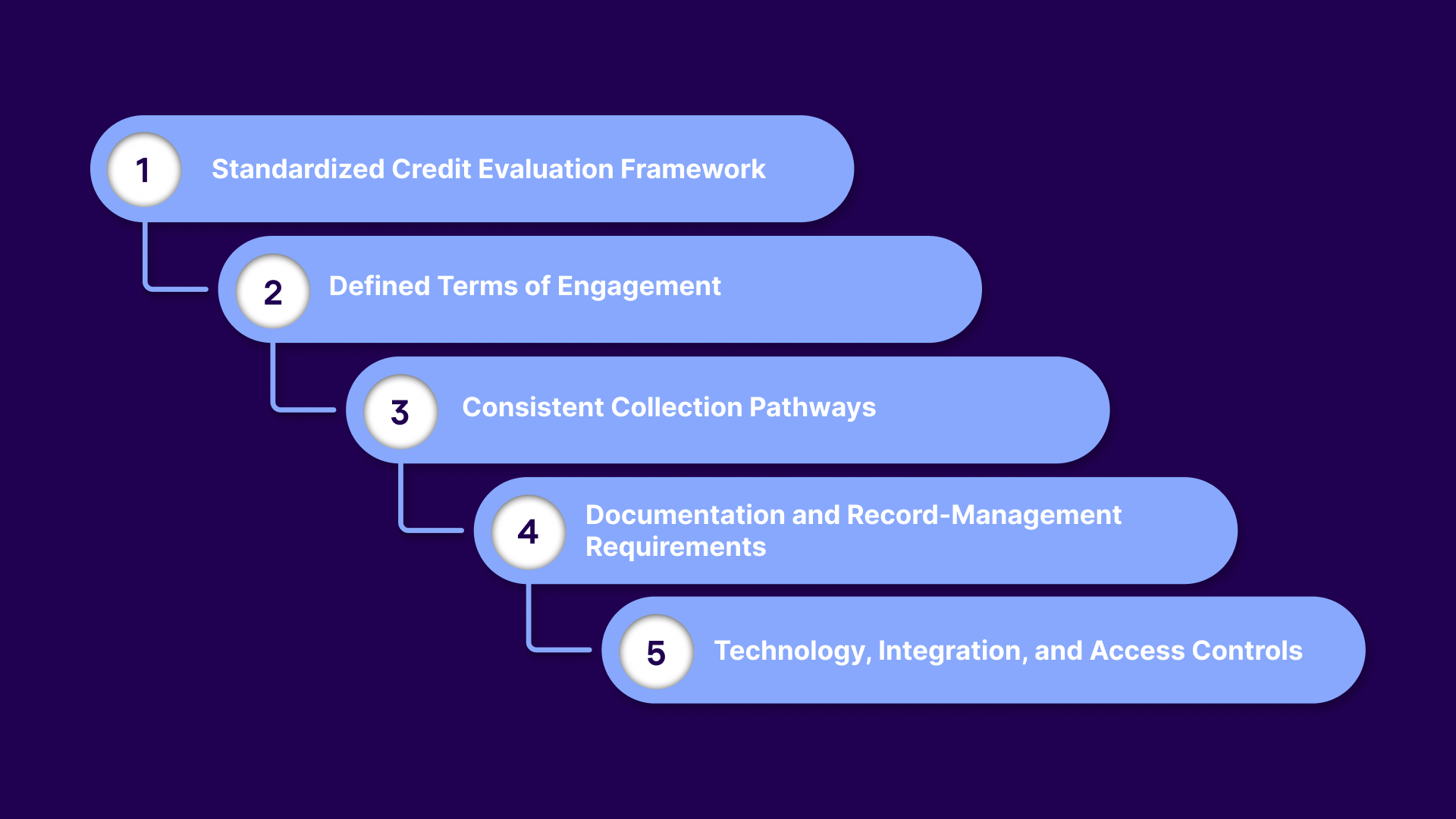

A strong credit and collection policy provides agencies with a clear framework for evaluating, managing, and resolving accounts. The components below form the structure that teams rely on to make consistent decisions and maintain organized workflows.

The policy should clearly outline how decisions are made and which factors influence account prioritization and next steps. This ensures that every account is assessed using the same approach.

Key elements include:

A well-structured policy defines the repayment terms, available resolution options, and timelines for how accounts are handled and resolved.

This section should include:

The policy must outline how overdue accounts move through the collection journey. This helps teams stay aligned and ensures follow-ups are handled at the right time.

Components often include:

A good policy doesn’t only define actions, it also defines how those actions should be recorded. This is crucial for transparency, compliance, and internal coordination.

Documentation guidelines may include:

Modern credit and collection operations depend heavily on reliable technology. A policy should outline the tools and systems that support workflow consistency, such as:

Effective policies must also adapt to changes in payment behaviour, technology, and regulatory expectations. That is where designing a policy fit for today’s environment becomes essential.

Suggested Read: Challenges Faced by Credit Officers & Their Impact on Collections

An innovative credit and collection policy needs to reflect how consumers behave today and how payment operations have evolved. In 2026, that means using data, digital tools, and flexible workflows that can adapt to changing volumes and regulations.

A policy built on these factors is easier to maintain, more consistent for teams to follow, and more relevant to the current payment environment.

Data strengthens decision-making across the entire process. Dashboards and behavioral insights help teams understand:

When a policy is built on real patterns rather than assumptions, agencies can refine repayment terms, update follow-up timelines, and adjust escalation rules with greater accuracy.

Automation reduces manual work and helps teams stay consistent. Features such as self-service payment portals, multilingual IVR, and embedded payment options allow consumers to resolve accounts at their own pace. This reduces the need for repeated follow-ups and shortens the time it takes to collect payments.

Digital self-service also creates more predictable workflows by handling routine cases automatically while leaving more complex accounts for staff review. The result is a policy that supports efficiency without compromising compliance or consumer experience.

Payment behavior has shifted significantly in recent years. More consumers prefer resolving accounts online, and agencies are adopting digital collection tools to match those expectations.

At the same time, regulatory oversight continues to evolve, and policies must reflect:

A credit and collection policy must support both routine and peak workloads. High-volume environments need processes that can adjust quickly, whether due to seasonal increases, new portfolios, disputes, or regulatory changes.

Scalable policy design includes:

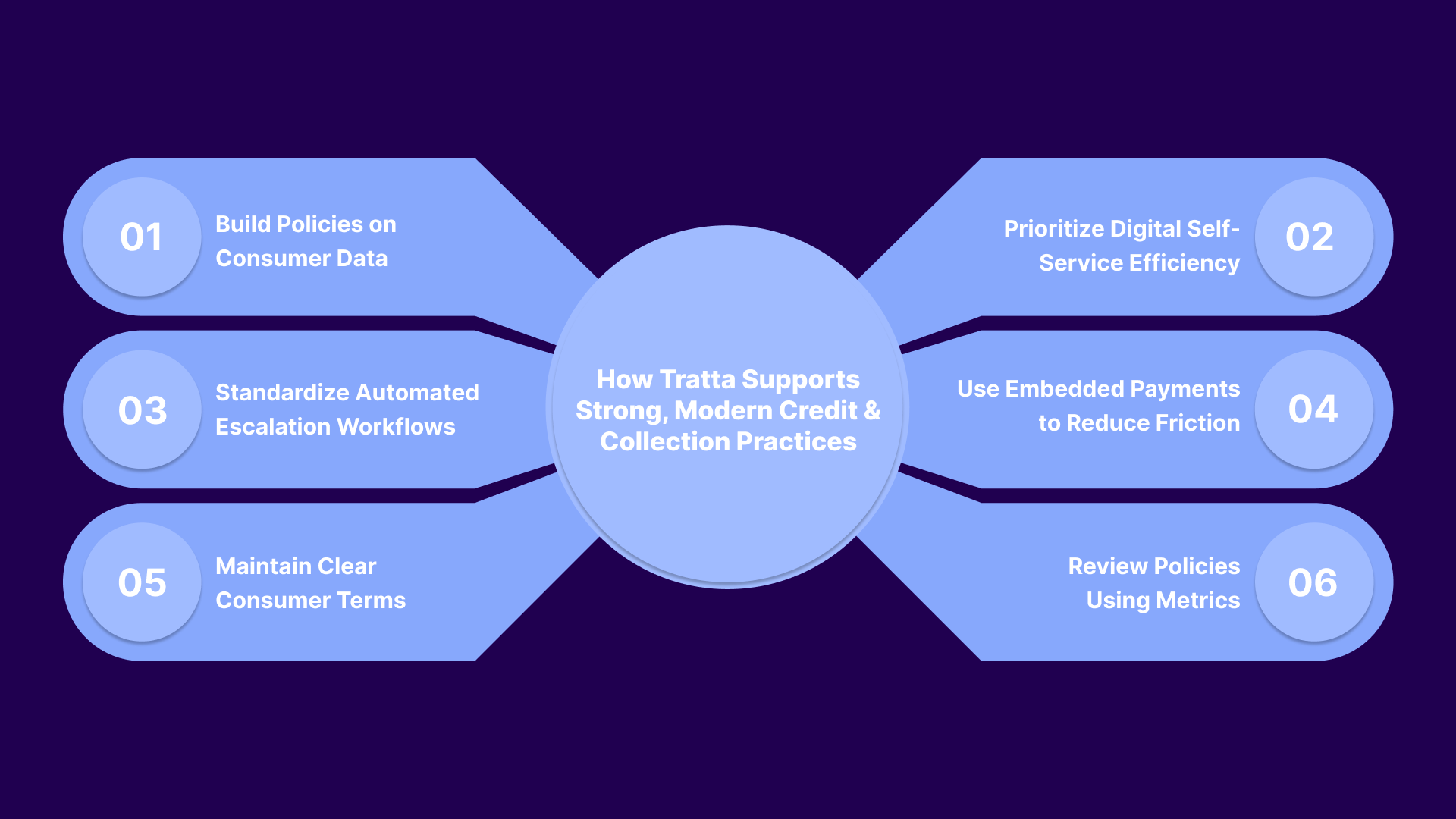

Tratta helps agencies translate these policy principles into daily operations. Tools such as the consumer self-service payment portal, automated campaigns, and reporting dashboards allow teams to apply consistent workflows while giving consumers flexible ways to resolve accounts. Get in touch with us to learn more.

A credit and collection policy becomes meaningful only when its impact is visible in the numbers. These metrics help teams understand whether their workflows, terms, and follow-up practices are producing the outcomes they expect.

These indicators show whether your policy is performing as intended:

A mid-sized organization updated its credit and collection policy in late 2025. The changes included clearer credit terms, automated reminders, and structured escalation steps supported by digital self-service.

Within six months:

This example shows how aligned workflows, consistent decision-making, and accessible repayment options translate into measurable outcomes.

The next step is ensuring those policies are supported by the right technology to maintain consistency, scale workflows, and translate strategy into daily operations.

Suggested Read: How to Handle Debt in Credit Collections

Tratta is a cloud-based debt collection platform designed to help agencies manage consumer payments, communications, and account resolution through a connected system. By combining digital payment tools, consumer self-service options, and operational analytics, the platform supports structured credit and collection workflows at scale.

The practices below reflect how agencies strengthen recovery outcomes when policies are supported by the right technology:

Policies gain their strength from accurate insights rather than assumptions. Understanding how consumers interact with repayment options helps teams refine their collection strategies and repayment options.

Our reporting and analytics give teams visibility into:

High-volume portfolios run more efficiently when consumers can resolve their accounts independently. Self-service options reduce unnecessary calls, lower operational costs, and create a smoother experience for everyone involved.

Consumer Self-Service Platform supports this best practice by enabling consumers to:

When escalation depends on individual judgment, outcomes vary and compliance risks grow. Strong policies outline clear follow-up timelines, communication rules, and escalation paths.

Tratta’s customizable workflows reinforce this structure by ensuring that every account:

Friction during repayment leads to delays, abandoned sessions, and incomplete payments. A strong policy supports quick, direct payment options that match how consumers prefer to pay.

Embedded payments help agencies:

Consumers should be able to understand their repayment choices without complex explanations.

Tratta supports transparency through:

The strongest credit and collection policies need to improve as volumes, consumer behavior, and regulations change. Regular reviews ensure the policy stays relevant and effective.

Tratta’s dashboards support this by tracking:

These insights help teams identify improvements and keep the policy aligned with current needs. If you want clearer processes, better visibility, and smoother payment experiences, then Tratta can help.

A clear credit and collection policy helps agencies manage accounts consistently and maintain predictable recovery performance. When policies are supported by reliable data, structured workflows, and accessible payment options, teams can resolve accounts faster and reduce operational strain.

Tratta supports this shift with tools such as consumer self-service payments, automated workflows, and reporting dashboards. It helps teams apply policies consistently and monitor performance across portfolios.

If you want more visibility into your collections workflow, see how Tratta can support your process. Schedule a demo to explore the platform in action.

A credit and collection policy sets rules for managing accounts and repayment pathways. It helps agencies follow consistent steps, reduce delays, and maintain predictable cash flow from collections. A defined policy also supports compliance and creates a smoother experience for both staff and consumers.

Most agencies review their policies every 6 to 12 months. Updates become necessary when regulations change, payment behavior shifts, or new technology is introduced. Regular reviews ensure the policy remains practical, compliant, and aligned with day-to-day operations.

Technology makes workflows more consistent and predictable. Tools like self-service portals, automated reminders, embedded payments, and analytics dashboards reduce manual work, support compliance, and help teams resolve accounts faster. These features also give consumers flexible payment options.

A reliable policy covers account evaluation criteria, limits, payment terms, follow-up workflows, escalation rules, and performance tracking. It also outlines how teams use digital tools and communication channels. Including these elements creates a structured approach that supports better cash flow and fewer disputes.

Collection agencies prioritize accounts based on factors such as balance size, account age, prior payment behavior, and likelihood of recovery. Segmentation models help teams focus efforts on accounts with higher recovery potential while automating lower-priority cases. This ensures resources are allocated efficiently across large portfolios.