Delinquent account volumes are rising rapidly, placing sustained pressure on recovery teams. Collection operations must manage higher workloads, stricter compliance standards, and tighter cost controls, often with limited staffing.

In Q3 2025, 4.5% of all U.S. household debt was in some stage of delinquency, reflecting continued financial strain across consumer credit markets. Yet most debt relief workflows still depend on manual outreach, disconnected systems, and agent-driven execution.

These models struggle to scale as portfolio demands grow. They increase operating costs, elevate regulatory risk, and slow recovery timelines. This guide explains how debt relief process automation reshapes delinquent account recovery and what effective implementation requires.

Brief look:

Debt relief process automation means using software to manage recovery workflows from start to finish. It replaces manual coordination across communication, payments, compliance, and reporting.

Instead of relying on agents to control every step, automation orchestrates these processes in real time. This allows you to scale operations, maintain consistency, and reduce operational risk.

In practice, debt relief automation covers the full recovery lifecycle:

When these workflows operate in isolation, operational complexity rises quickly, and performance suffers. Costs grow, compliance exposure increases, and recovery timelines stretch. In the next section, we cover why traditional debt relief workflows fail at scale.

Suggested Read: Automated Debt Settlement: What It Is And How It Works

Manual processes, disconnected systems, and agent-driven execution create operational friction at every stage of recovery. As your portfolio grows, these issues compound and limit performance.

The most common challenges include:

As these constraints intensify, recovery outcomes become harder to predict and control. In the next section, we cover how the automated debt relief process works.

Suggested Read: Understanding Debt Settlement Law and Procedures

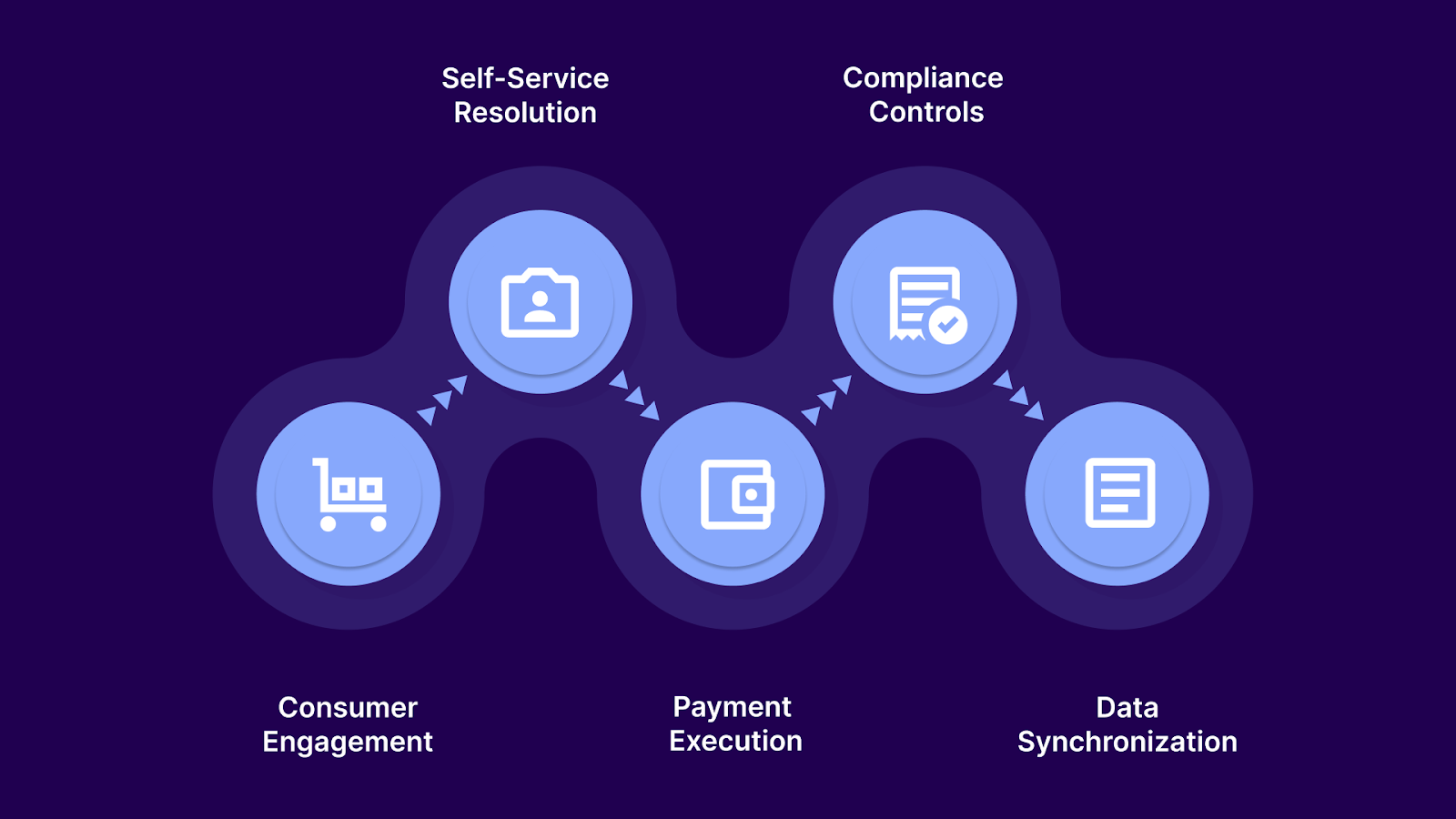

An automated debt relief process simplifies how delinquent accounts move from early delinquency to final resolution. Software coordinates engagement, payments, and compliance in the background. This creates consistency, improves response rates, and reduces operational strain.

In practice, automation supports recovery through five core functions.

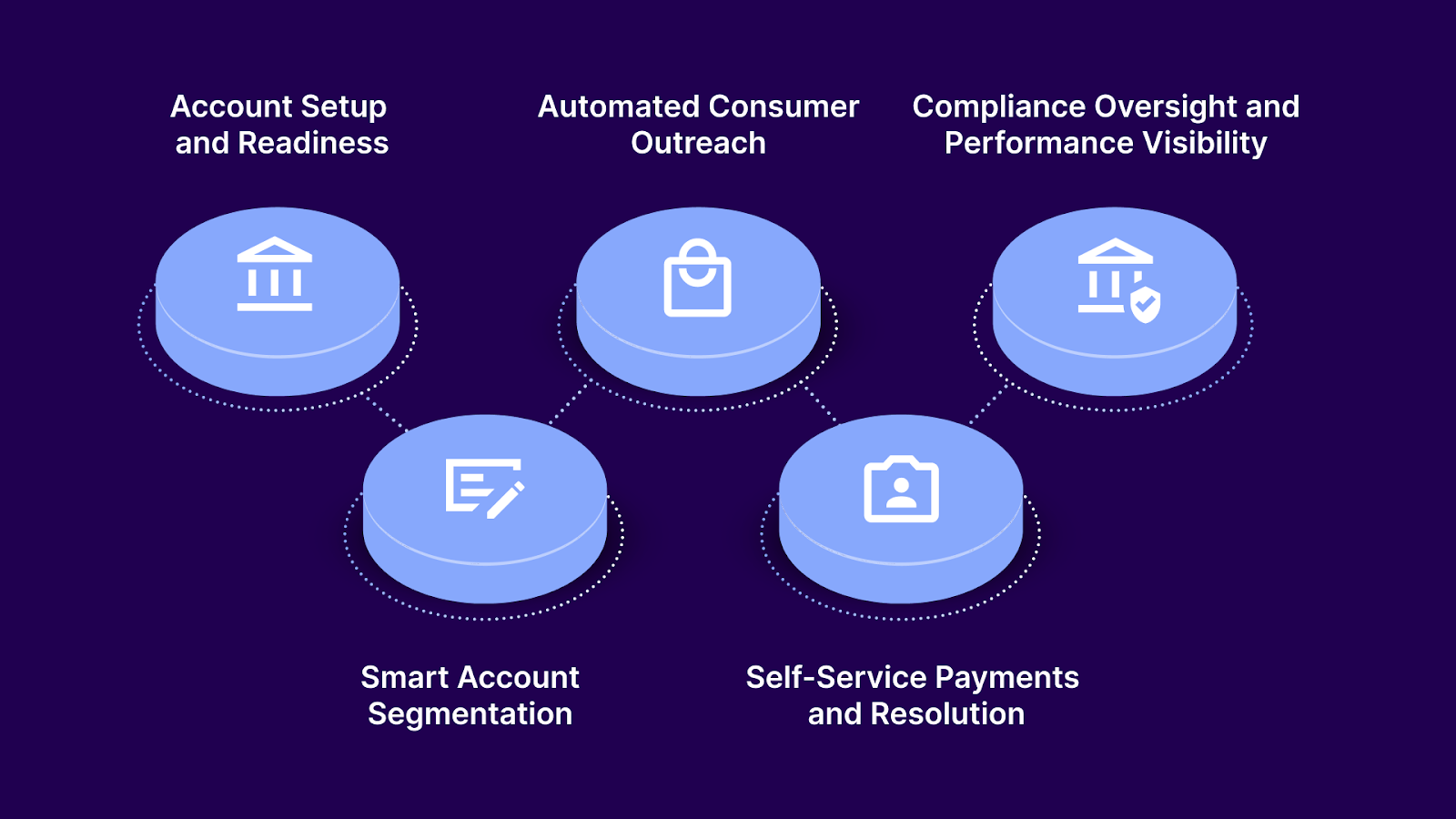

Automating the debt relief process ensures that every delinquent account enters recovery in a structured, consistent way. It removes manual tracking and reduces operational uncertainty. This helps your team stay focused on resolution instead of data management.

At ground level, automation helps you:

Automation helps you move away from one-size-fits-all recovery strategies. Accounts are grouped based on balance size, age, risk, and consumer behavior. This allows you to match the right recovery approach to each segment.

Automation improves segmentation by doing the following:

Automation allows you to reach more consumers without expanding your call center. Outreach runs continuously across digital and voice channels, guided by timing and behavior. This improves contact rates while reducing agent dependency.

In daily workflows, automation allows you to:

Automation directs engaged consumers into secure self-service workflows. This reduces call volume while accelerating payments and settlements. Consumers can resolve accounts on their own terms and timelines.

Automation supports resolution by doing the following:

Further Read: How Do Settlements Work in Self-Service Debt Payments?

Debt relief process automation embeds compliance controls and reporting into every step of the recovery process. This reduces regulatory exposure while improving operational insight. You gain clarity into what is working and where performance can improve.

Automation supports oversight by doing the following:

Tratta supports automated debt relief workflows through its campaign automation engine, which coordinates outreach across SMS, email, and IVR. You can launch segmented, behavior-driven campaigns that adapt based on consumer responses and payment activity. Schedule a free demo today.

Automation transforms how delinquent portfolios are executed, monitored, and optimized. Instead of relying on human coordination, systems drive engagement, payments, compliance, and reporting in real time.

Key operational benefits include:

In the next section, we cover the various signs to implement debt relief automation as soon as possible.

Suggested Read: Debt Settlement Practices That Improve Agency Results

Automation becomes essential when operational complexity outpaces manual control. At this stage, staffing increases, process tweaks, and isolated tools stop delivering meaningful improvements.

These signals indicate that your operation has crossed the threshold where automation is no longer optional:

Manual workflows begin to break once account volumes outgrow daily agent capacity. At this point, operational execution becomes inconsistent and reactive. This shift typically appears when you see:

When servicing costs grow faster than recoveries, operational efficiency is eroding. This indicates that workflow friction is offsetting portfolio growth. Early warning signs include:

As communication volume increases, regulatory exposure multiplies. Manual compliance enforcement becomes increasingly fragile at scale. This typically shows up through:

Lower response rates indicate growing consumer disengagement. Traditional outreach methods struggle to cut through communication fatigue. This pattern becomes visible through:

Volatile recovery outcomes signal that operational control is weakening. Forecasting and planning become difficult under these conditions. Common indicators include:

When these signals appear, automation becomes a structural requirement rather than a performance upgrade. In the next section, we cover how to implement the debt relief process automation successfully.

Suggested Read: AFCC Debt Settlement Explained for Collection Agencies

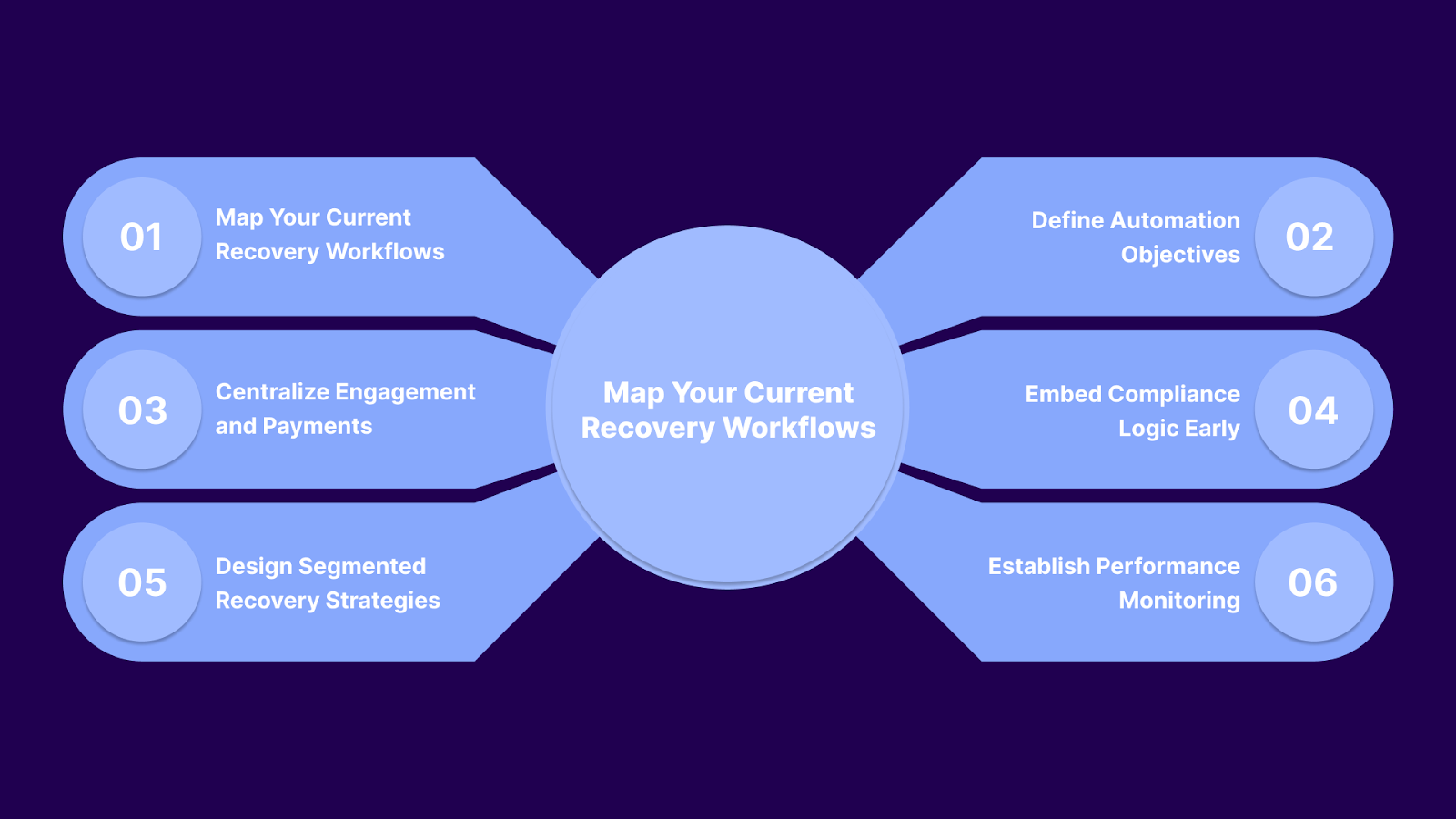

Many agencies fail because they automate fragmented workflows rather than redesign them. A structured implementation approach ensures automation improves recovery outcomes rather than introducing new complexity.

These steps outline how to deploy debt relief automation effectively.

Tratta enables agencies to automate engagement, payments, and compliance within structured recovery workflows. You can deploy segmented campaigns, execute settlements, and monitor performance in real time. This simplifies implementation while maintaining operational control. Learn more.

Automation delivers results only when it is implemented with operational intent. Many agencies invest in automation but fail to achieve meaningful gains due to poor execution choices.

The table below highlights common pitfalls, their real-world impact, and how to correct them.

When these errors persist, automation becomes a cost center instead of a performance driver. Recovery workflows lose coordination, and operational confidence declines.

Best practices that prevent these failures include:

When automation is supported by the right execution framework, it becomes a strategic growth engine. In the next section, we explore how modern technology enables scalable, compliant, and high-performance debt relief automation.

Tratta is a leading debt collection software platform that automates the entire debt relief lifecycle. It replaces fragmented tools with a comprehensive system for engagement, payments, compliance, and reporting.

You get a recovery operation that runs faster, adapts in real time, and maintains consistent performance as portfolios grow. These are the core features:

Tratta Campaigns automate outreach workflows across SMS, email, and voice channels. These workflows adjust dynamically based on consumer behavior and response patterns. This allows you to run continuous, behavior-driven recovery strategies without manual campaign management.

Tratta centralizes consumer engagement across text, email, voice, and IVR. Outreach timing and sequencing adapt automatically based on engagement signals. This improves contact rates while reducing agent workload.

Payments are integrated directly into the recovery workflow. Consumers can complete settlements, installment plans, and recurring payments without friction. This shortens resolution timelines and improves cash realization.

The portal allows consumers to review balances, accept settlements, and set up payment plans independently. This reduces call volume and accelerates resolution. It also improves the overall consumer experience.

The IVR enables automated phone-based payments in multiple languages. This expands account reach and improves accessibility. It also reduces inbound call dependency.

Real-time dashboards provide visibility into engagement, payment performance, and recovery trends. This allows you to monitor campaign effectiveness and optimize strategies continuously. It also improves forecasting accuracy.

Tratta allows you to configure workflows, messaging, disclosures, and settlement logic. This ensures automation aligns with your operational model and compliance requirements. It also supports strategy differentiation across portfolios.

Tratta connects seamlessly with core systems through APIs and data feeds. This keeps balances, statuses, and payments synchronized in real time. It eliminates reconciliation delays and data inconsistencies.

Compliance and security controls are embedded into every workflow. This ensures regulatory adherence across communication, payments, and data handling. It also simplifies audits and reduces risk exposure.

Tratta enables agencies to recover more accounts, faster, and with greater operational confidence. It is built for scale, engineered for compliance, and designed to modernize overdue account recovery.

Manual workflows create operational drag, slow cash realization, and limit your ability to respond to shifting consumer behavior. Without automation, recovery operations become harder to scale, compliance risk rises, and performance becomes increasingly unpredictable.

Tratta enables agencies to automate engagement, payments, compliance, and reporting through a single operational framework. Its campaign automation, embedded payments, compliance controls, and real-time analytics allow you to recover more accounts while maintaining control and visibility.

If you are evaluating automation for overdue account recovery, now is the time to act. Speak to our team to see how automation can reshape your recovery operations.

The 7-7-7 rule limits call frequency, allowing no more than seven calls per account, per week, per phone number, ensuring regulatory compliance while preventing consumer harassment and complaint escalation.

Collection agencies automate debt collection by using software to manage engagement workflows, trigger communications, process payments, enforce compliance rules, and deliver real-time performance insights across delinquent portfolios.

The phrase requests written communication only, but agencies must follow regulatory standards regardless, using compliant engagement workflows, consent tracking, and automated disclosures to prevent violations and ensure consistent, lawful communication practices.

Debt relief programs improve recovery outcomes by increasing engagement, enabling structured settlements, and supporting payment plans, allowing agencies to resolve delinquent accounts faster while improving consumer cooperation and long-term repayment consistency.

Agencies should invest when portfolio growth increases staffing pressure, recovery cycles slow, compliance risks rise, or operational costs escalate, signaling that manual workflows no longer support scalable, predictable recovery performance.