The Complete Guide to ACH Batch Processing for Collection Agencies

Accounts receivable management (ARM)

The Complete Guide to ACH Batch Processing for Collection Agencies

Published on:

March 9, 2026

Handling hundreds of consumer payments manually can slow a collection agency down. Your staff has to juggle payment plans, settlement schedules, and bank details while avoiding costly errors. Meanwhile, ACH has quietly become the backbone of U.S. digital payments. In 2025, the ACH network processed35.20 billion payments.

For agencies, that scale creates both pressure and opportunity. When payment processing becomes chaotic, recovery slows, and reconciliation becomes painful. When it runs smoothly, cash flow improves, and operations stabilize.

This guide explains how ACH batch processing works, why it matters in collections, and how agencies can manage high-volume payments more efficiently.

In brief:

ACH batch processing explained. Collection agencies group multiple authorized bank payments into a single submission to move transactions through the ACH network efficiently.

Core workflow steps. Payments move from consumer authorization to batch creation, network clearing, and final settlement between financial institutions.

Common payment types. Recurring payment plans, settlement installments, post-dated debits, and one-time resolutions are frequently processed through ACH batches.

Compliance requirements matter. Agencies must follow Nacha rules, the Electronic Fund Transfer Act, Regulation E, and FDCPA standards when initiating ACH debits.

Technology reduces operational risk. Modern platforms help agencies organize payment activity, maintain records, and monitor large volumes of ACH transactions more effectively.

What Is ACH Batch Processing in Collections?

The Automated Clearing House (ACH) network, governed byNacha, is the system U.S. banks use to move electronic payments between accounts. The network processes transactions in groups rather than one at a time.

ACH batch processing refers to bundling multiple payment instructions into a single ACH file and submitting them together.

An ACH file is a fixed-width, ASCII file, with each line exactly 94 characters in length

For collection agencies managing payment plans, settlements, and recurring debits, batching allows large volumes of transactions to move through the network efficiently.

This is what an ACH file contains:

File Header Record: Identifies the file originator and destination, along with the date and time the file was created.

Batch Header Record: Groups similar transactions together and includes details such as the company initiating the payments and the transaction type.

Entry Detail Records: These are the individual transactions within the batch, including bank routing numbers, account numbers, payment amounts, and recipient information.

Batch Control Record: Provides totals and counts for all entries in the batch to help financial institutions verify accuracy.

File Control Record: Summarizes all batches within the file and confirms the total number of transactions submitted.

Once these records are structured and validated, the file moves through the ACH network according to scheduled processing windows. Understanding that flow makes it easier to see how ACH batch processing works in practice.

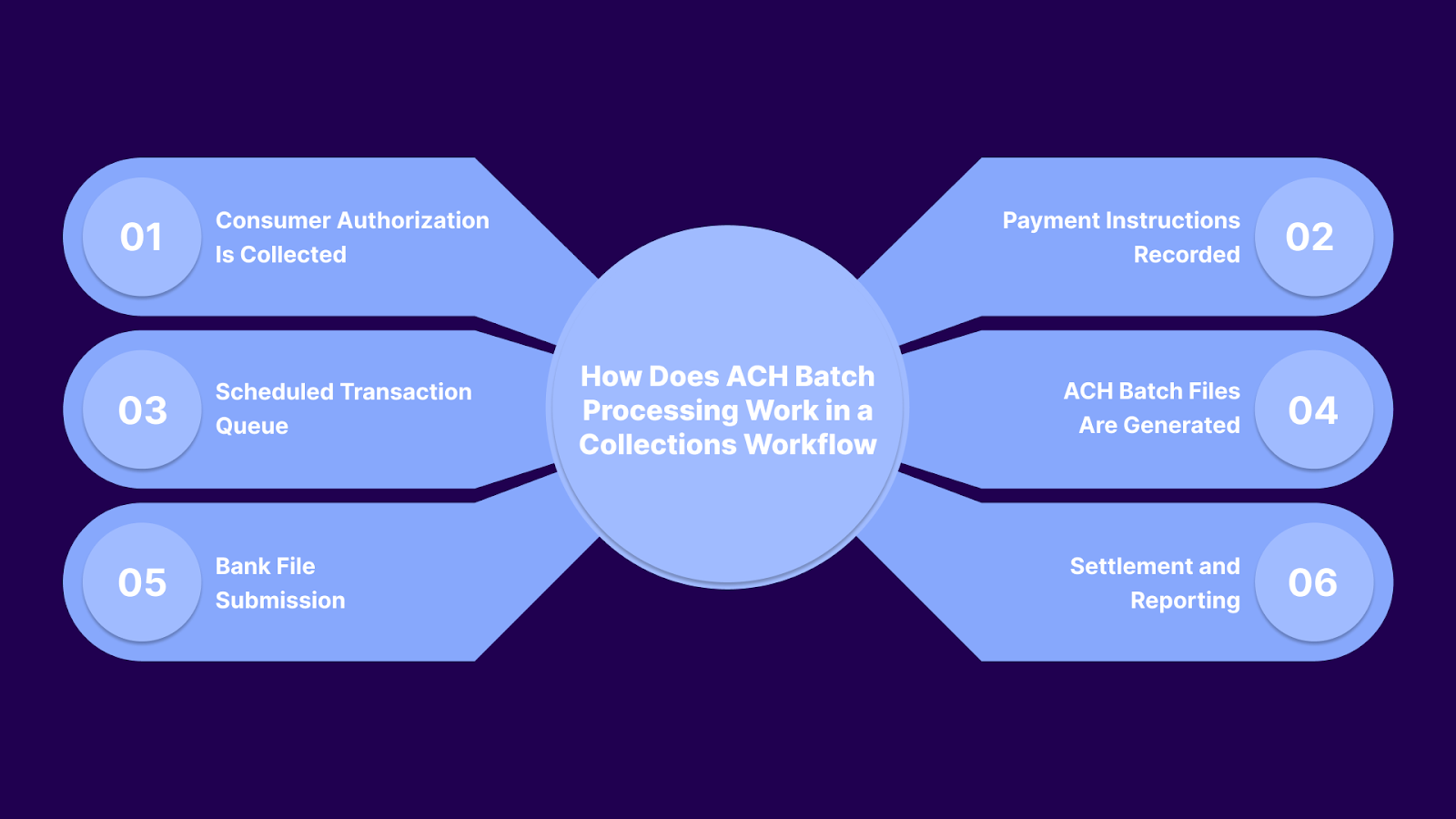

How Does ACH Batch Processing Work in a Collections Workflow

ACH batch processing usually happens behind the scenes after a consumer agrees to make a payment. Instead of sending each transaction individually, agencies group authorized payments and submit them together through the ACH network.

This is how ACH batch processing works for debt payments:

1. Consumer Authorization Is Collected

Before any ACH debit happens, the agency must obtain proper authorization from the consumer. This can happen over the phone, through a payment portal, or via a signed agreement tied to a settlement or payment plan.

That authorization typically includes:

Consumer bank routing and account details

Payment amount and frequency

Date of the first withdrawal

Agreement to ACH debit terms

Record of consent for compliance purposes

2. Payment Instructions Are Recorded in the Agency System

Once authorization is in place, the payment details are entered into the agency’s platform. At this stage, the transaction is prepared for future batch submission rather than being processed immediately.

Operational data captured usually includes:

Consumer account reference or case ID

Scheduled processing date

Payment amount and frequency

Account status and settlement terms

Payment method and authorization record

3. Transactions Are Queued for Scheduled Processing

Collection agencies rarely submit payments the moment they are created. Instead, systems hold transactions until the scheduled processing window so multiple payments can be sent together.

During this stage, the platform organizes:

Payments are scheduled for the same day

Recurring payment plan installments

Settlement payments are due for that cycle

Previously scheduled post-dated payments

Payments across different account portfolios

4. ACH Batch Files Are Generated

When the processing window arrives, the system compiles all eligible transactions into an ACH file. This file follows the Nacha formatting standards so financial institutions can read and route the entries.

The batch file generally contains:

Originating company information

Bank routing details for each entry

Debit or credit instructions

Transaction totals and counts

Control records used for validation

5. Files Are Submitted to the Originating Bank

After the file is generated, it is transmitted to the agency’s payment processor or bank. The financial institution then forwards the transactions into the ACH network for clearing.

At this point, the process involves:

File validation checks

Submission through secure channels

Sorting by receiving banks

Routing through the ACH operator

Confirmation that the batch was accepted

6. Settlement and Reporting

The receiving banks debit consumer accounts and move funds through the network. Agencies then receive reports showing which payments succeeded and which failed.

These updates typically include:

Successful payment confirmations

Returned transactions and return codes

Settlement totals

Updated account balances

Reconciliation data for accounting teams

Collection agencies often manage hundreds or thousands of these payment events simultaneously.Tratta helps manage the steps leading up to ACH processing by organizing consumer authorizations, payment plans, and scheduled transactions in one place.Schedule a free demo today.

Types of Payments Typically Processed in ACH Batches

Collection agencies rarely send a single ACH transaction at a time. Most payments are scheduled, grouped, and processed in cycles so teams can manage volume without creating operational bottlenecks.

That is why the following types of transactions consistently appear in ACH batches:

Recurring Payment Plans Agencies schedule monthly or biweekly debits based on the consumer’sACH agreement, and these payments are grouped into batches when the processing date arrives. This allows agencies to run dozens or even thousands of installments in a single submission.

Settlement Installments Some settlements are split into multiple payments to make repayment more realistic for the consumer. Instead of manually initiating each installment, agencies schedule the payments in advance and allow them to move through batch processing on the agreed dates. This keeps the settlement consistent and reduces administrative work.

One-Time Authorized Debits When a consumer agrees to resolve an account with a single bank payment, that transaction is still often included in the next available batch run. Grouping one-time payments with others helps agencies maintain a consistent processing workflow rather than interrupting operations for individual submissions. It also simplifies reconciliation later.

Post-Dated Payments Consumers frequently authorize payments scheduled for a future date, such as after a paycheck or benefit deposit. Agencies store these payment instructions and release them into the ACH batch once the scheduled date arrives. This approach prevents missed deadlines and keeps payments aligned with the consumer’s financial timing.

Portfolio-Level Payment Runs Some agencies process large volumes of payments across entire account portfolios on specific days of the week or in specific months. These runs may include different payment types, balances, and consumers, all bundled into one submission. Batching enables large payment volumes to move through the ACH network without overwhelming staff.

These payment types reveal how central batching is to everyday collections work. The real question is why agencies rely on ACH batch processing in the first place. This is discussed in the next section.

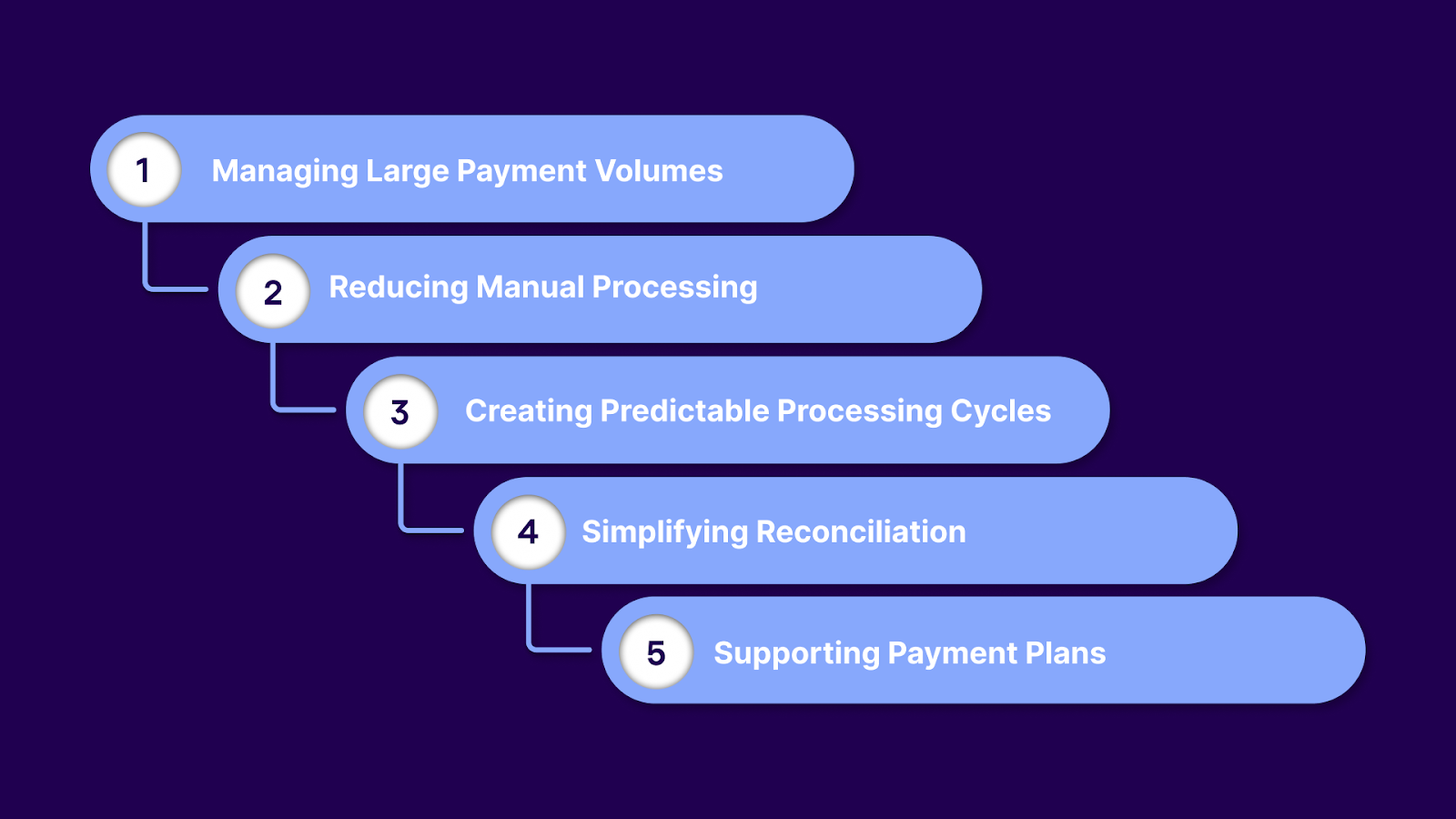

Collection agencies process large numbers of bank payments tied to payment plans, settlements, and scheduled debits. ACH batching helps them move these transactions through the banking system in an organized and scalable way.

These are a few benefits of using ACH batches:

Managing Large Payment Volumes: Agencies can group hundreds or thousands of transactions into one submission. This keeps payment operations efficient as account portfolios grow.

Reducing Manual Processing: Instead of initiating each debit individually, systems prepare and submit payments together. This lowers administrative workload and reduces errors.

Creating Predictable Processing Cycles: Payments scheduled for the same day can be processed in a single run. That structure helps teams plan around ACH clearing windows.

Simplifying Reconciliation: Batch totals make it easier to match deposits with the transactions that created them. Accounting teams can review results faster.

Supporting Payment Plans: Many consumers repay their balances in installments rather than in a single payment. Batching allows those scheduled debits to move through the system consistently.

ACH batching also connects closely to how the network clears payments and when funds actually settle. The next section explains the timelines to help agencies plan payment activity more accurately.

ACH Processing Timelines and Settlement Windows for Debt Payments

ACH payments move through a defined network schedule. For collection agencies running payment plans and settlements, these processing windows determine when debits are submitted, cleared, and settled.

These points explain how the ACH network operates during the business day:

The ACH Network processes payments for about23¼ hours every business day. Settlement occurs multiple times during the day when the Federal Reserve settlement service is open.

The system pauses overnight and remains closed on weekends and federal holidays. Payments scheduled during those periods move in the next available processing cycle.

Because ACH works in batches, agencies usually align payment runs with these operating windows to avoid delays.

2. Non-Business Days

These points describe how timing shifts around weekends and holidays:

If a scheduled debit falls on a weekend or holiday, it typically posts on the next business day.

This timing adjustment is common across industries that rely on ACH payments.

Agencies planning payment schedules need to account for these calendar shifts to avoid missed drafts.

3. Payment Availability

These points explain when funds appear and settle:

Funds move between financial institutions during ACH settlement cycles.

Some banks may show transactions earlier under their internal policies, even though final settlement occurs later.

For agencies, this means consumer accounts may show activity before funds are fully confirmed.

Understanding these timelines is important, but agencies must also follow ACH rules governing authorization, recordkeeping, and consumer protections. Compliance requirements are covered in the next section.

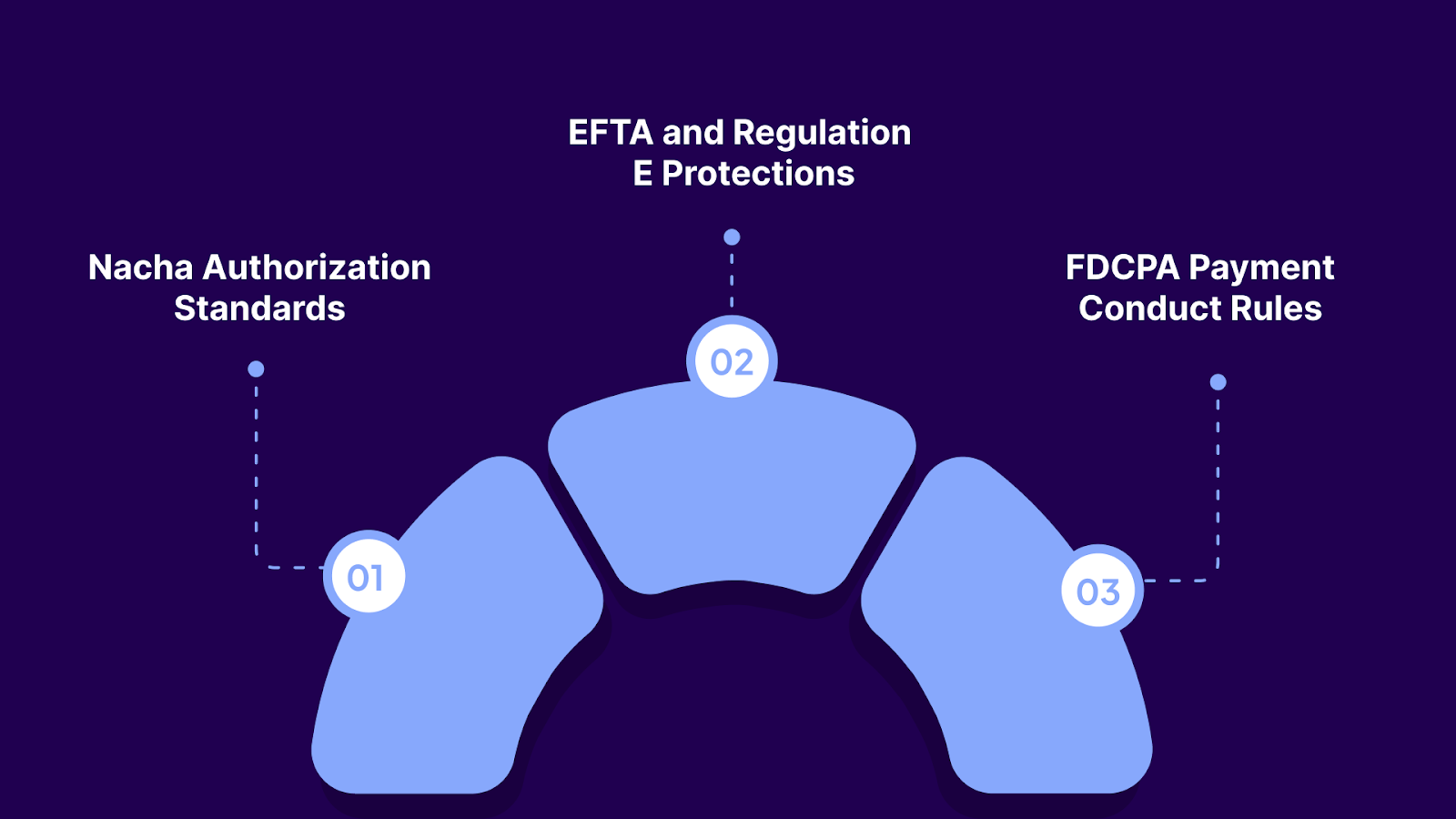

Compliance Requirements for Collection Agencies Handling ACH Payments

ACH payments in collections operate under a layered regulatory structure that combines network rules, federal law, and banking oversight. Agencies initiating debits must ensure the payment itself, the authorization behind it, and the communication around it all meet regulatory expectations.

Collection agencies initiating ACH payments must follow rules from multiple regulatory bodies:

Nacha Authorization Standards Nacha rules require clear consumer authorization before initiating an ACH debit, and agencies must retain that authorization for at least two years after the last transaction. The authorization must specify the amount, method of calculation, and timing of the debit. If a bank requests proof, the originating institution must be able to produce it promptly.

EFTA and Regulation E Protections TheElectronic Fund Transfer Act andRegulation E give consumers the right to dispute unauthorized electronic debits from their bank accounts. Financial institutions investigate these claims, and unauthorized withdrawals can trigger reversals and compliance scrutiny. Agencies, therefore, need verifiable consent and accurate payment records tied to each transaction.

FDCPA Payment Conduct Rules When ACH payments are used to collect debts, theFair Debt Collection Practices Act governs how the authorization is obtained and used. Agencies cannot misrepresent payment terms, withdraw funds earlier than agreed, or process amounts beyond the consumer’s authorization. Clear documentation of payment agreements becomes essential evidence of lawful conduct.

Tratta brings structure to this process by organizing payment agreements, transaction activity, and account records in one system. Instead of teams searching across tools for documentation, they can view payment history and consumer commitments in a single workflow. This visibility helps agencies stay prepared when questions arise around ACH activity.Learn more.

Risks and Challenges in ACH Batch Processing for Collectors

ACH batching improves efficiency, but it also introduces operational and compliance risks that collection agencies need to manage carefully. When large volumes of transactions move together, a single mistake can affect multiple accounts at once.

Challenge

What Happens

Why It Matters for Agencies

Payment Returns

Banks may reject transactions due to insufficient funds, closed accounts, or authorization issues.

High return rates can trigger scrutiny from originating banks and disrupt payment plans.

Incorrect Bank Details

Routing or account number errors cause transactions to fail before settlement.

Staff must investigate failures and reprocess payments, which increases the workload.

Agencies must provide proof quickly or risk reversals and compliance concerns.

Timing Issues

Payments submitted after the processing window move to the next cycle.

This can delay settlements and create confusion for both staff and consumers.

Reconciliation Gaps

Large batches make it harder to trace individual payments without structured reporting.

Finance teams may struggle to match deposits with specific accounts.

These challenges often appear when batch processing relies on manual tracking or disconnected systems. To reduce risk, agencies typically focus on a few operational safeguards:

Validate bank information before scheduling payments.

Keep clear records of consumer authorizations and payment agreements.

Monitor return codes and resolve issues quickly.

Align payment schedules with ACH processing windows.

Maintain clear reconciliation processes for batch submissions.

Managing these risks becomes much easier when agencies rely on systems designed for high-volume payment workflows rather than manual processes.

Risks and Challenges in ACH Batch Processing for Collectors

ACH batching improves efficiency, but it also introduces operational and compliance risks that collection agencies need to manage carefully. When large volumes of transactions move together, a single mistake can affect multiple accounts at once.

Table showing common problems:

Challenge

What Happens

Why It Matters for Agencies

Payment Returns

Banks may reject transactions due to insufficient funds, closed accounts, or authorization issues.

High return rates can trigger scrutiny from originating banks and disrupt payment plans.

Incorrect Bank Details

Routing or account number errors cause transactions to fail before settlement.

Staff must investigate failures and reprocess payments, which increases the workload.

Authorization Disputes

Consumers may claim a debit was unauthorized.

Agencies must provide proof quickly or risk reversals and compliance concerns.

Timing Issues

Payments submitted after the processing window move to the next cycle.

This can delay settlements and create confusion for both staff and consumers.

Reconciliation Gaps

Large batches make it harder to trace individual payments without structured reporting.

Finance teams may struggle to match deposits with specific accounts.

These challenges often appear when batch processing relies on manual tracking or disconnected systems. To reduce risk, agencies typically focus on a few operational safeguards:

Validate bank information before scheduling payments.

Keep clear records of consumer authorizations and payment agreements.

Monitor return codes and resolve issues quickly.

Align payment schedules with ACH processing windows.

Maintain clear reconciliation processes for batch submissions.

Managing these risks becomes much easier when agencies rely on systems designed for high-volume payment workflows rather than manual processes.

How Does Tratta Improve ACH Batch Processing

Trattais a debt-collection payment and engagement platform built specifically for collection agencies, law firms, and creditors. Instead of treating payments, communication, and reporting as separate systems, it brings them into a single environment. This structure becomes especially valuable when agencies are handling large volumes of ACH payments tied to settlements and payment plans.

The following features help collection agencies:

Consumer Self-Service Payment Portal Consumers can log in, verify their accounts, review balances, and authorize payments themselves. This reduces manual intake and ensures that payment details are entered into the system accurately. For ACH workflows, it means payment plans and authorizations can be captured directly from the consumer rather than through agent entry.

Payments and Merchant Services Tratta provides an integrated payment infrastructure designed for debt collection transactions. Agencies can manage consumer payments through a single connected system instead of juggling multiple processors. This simplifies how transactions move from authorization into processing and reconciliation.

Multilingual Payment IVR Consumers can make payments through an automated phone system in multiple languages. This expands access for consumers who prefer phone-based payments instead of digital portals. The result is more consistent payment capture that can later move into agency payment workflows.

Omnichannel Communications Agencies can reach consumers via phone, text, and email from a single platform. Payment reminders, settlement discussions, and follow-ups stay connected to the account record. That visibility helps teams keep track of commitments tied to upcoming ACH payments.

Campaign Management Agencies can segment accounts and automate outreach based on payment behavior or account status. Campaign scheduling and trigger-based workflows help teams scale communication across large portfolios. This is useful when coordinating payment plan activity across many accounts at once.

Reporting and Analytics The platform tracks payments, offers, and consumer interactions from first contact through resolution. Real-time dashboards help agencies understand which strategies and payment arrangements are working. This level of visibility helps teams manage large volumes of transactions more confidently.

Customization and Flexibility Administrators can configure workflows, policies, and communication rules to match operational needs. That flexibility allows agencies to adapt processes as payment volumes or regulatory requirements change. Instead of forcing teams into rigid workflows, the system adjusts to the agency.

Integrations Tratta connects with existing systems through APIs and integrations. This allows account data, balances, and payment activity to remain synchronized across platforms. Agencies avoid the data gaps that often complicate payment processing and reconciliation.

Security and Compliance Built-in safeguards help protect consumer data and support regulatory obligations. The platform logs communications and payment activity, helping agencies maintain clear records. This becomes important when handling sensitive financial information and consumer authorizations.

Tratta works as the operational layer that keeps consumer agreements, communication, and transactions organized. Your agency can run complex payment workflows with far less friction.

Conclusion

ACH batch processing works well when every piece of the workflow is aligned. When it is not, small mistakes can cascade across hundreds of transactions. Missing authorizations, incorrect account data, poorly timed submissions, or weak recordkeeping can lead to payment returns, consumer disputes, and unnecessary operational strain for collection teams.

Trattahelps agencies bring structure to these moving parts. By keeping payment activity, consumer engagement, and account records connected in one system, teams can manage high-volume ACH workflows with better visibility and control. Instead of reacting to problems after batches are submitted, agencies can organize and monitor the process from the start.

If ACH payments are a core part of your recovery strategy, the systems behind them matter. Schedule a free call today to understand how you can simplify complex payment workflows while maintaining clarity across accounts.

Frequently Asked Questions

1. What is ACH batch processing?

ACH batch processing groups multiple payment instructions into a single file and sends them through the ACH network together. Collection agencies use it to process large volumes of authorized consumer payments efficiently.

2. What time are ACH batches processed?

ACH batches are processed during network operating windows on business days. Banks and processors submit files at scheduled intervals, and transactions move through clearing and settlement cycles during the day.

3. What is ACH payment processing?

ACH payment processing transfers money electronically between bank accounts through the Automated Clearing House network. Collection agencies commonly use it for settlements, installment arrangements, and recurring repayment schedules.

4. What are the two types of ACH?

The two main types are ACH debit andACH credit. A debit pulls money from a consumer’s account with authorization, while a credit sends money to another bank account.

5. Why do collection agencies use ACH payments?

ACH payments help agencies manage high volumes of transactions tied to payment plans and settlements. They are cost-efficient, predictable, and easier to reconcile than many other payment methods.

Note: This information is not legal advice. Tratta recommends that you consult with your legal counsel to make sure that you comply with applicable laws in connection with your collection and outreach activities.

Sign up for our monthly newsletter

Debt collection insights that keep you compliant and competitive.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.