Failed payments are one of the most expensive friction points in debt collection. While ACH remains a core payment method, slow settlement times, return risk, and consumer reluctance to share bank details often delay resolution and increase operational effort.

In Q3 2025, the ACH Network processed 8.8 billion payments worth over $23.2 trillion. Yet adoption is changing as consumers increasingly prefer faster, more familiar methods such as cards and digital wallets.

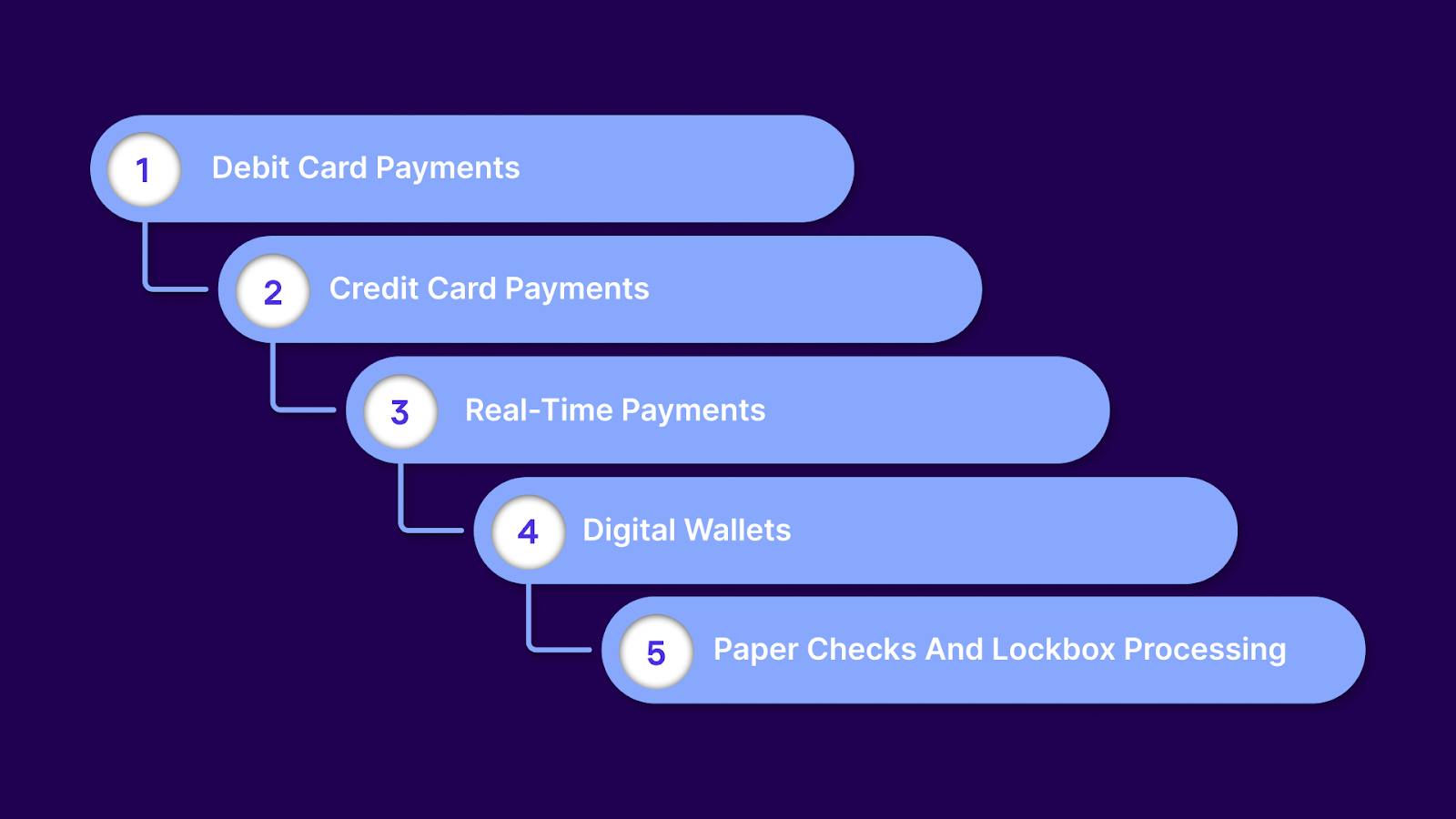

As payment behavior shifts and real-time rails gain traction, agencies must weigh how to collect effectively without depending solely on ACH. This post explores five ACH alternatives that can improve completion rates, enhance the consumer experience, and meet your agency's needs.

Quick look:

ACH payments in the United States operate under the rules and framework set by Nacha, which emphasize security, consistency, and broad participation by financial institutions.

While this makes ACH reliable, it also creates practical constraints for debt collection workflows, where timing, certainty, and consumer confidence are critical to recovery.

Key limitations agencies encounter with ACH include:

ACH transactions typically take one to three business days to settle. This delay creates uncertainty around payment confirmation and slows account resolution, especially for time-sensitive settlements.

Payments can be returned for insufficient funds, closed accounts, or authorization issues. Each return increases operational effort and extends the recovery cycle.

Many consumers are reluctant to share routing and account numbers, particularly in a collections context, which can reduce payment follow-through.

ACH works best for scheduled plans but is less suited for immediate, lump-sum resolutions where instant confirmation matters.

Failed or pending ACH payments often require manual monitoring, re-authorization, and outreach, adding avoidable administrative strain.

Because of these limitations, ACH alone rarely meets every recovery scenario. This is why agencies increasingly rely on alternative payment methods that offer faster confirmation, lower friction, and greater consumer choice.

Suggested Read: How Optimized Payment Portals Boost Debt Recovery Rates

Each alternative serves a specific purpose, with clear strengths and limitations that affect cost, speed, and completion rates.

Below is a structured comparison of the most common ACH alternatives used by collection agencies today.

Debit card payments provide immediate authorization and fast confirmation, making them effective for quickly resolving accounts. Consumers widely trust them and work well for both online and agent-assisted payments.

Key Features:

Pros:

Cons:

Compared to ACH, debit card payments offer immediate authorization and far greater certainty. You know whether a payment succeeds at the moment it is attempted, rather than days later.

The trade-off is higher processing costs, but those costs often offset reduced failures and faster resolutions. For most agencies, debit cards are a strong upgrade for one-time payments and settlements where speed matters more than fees.

Credit cards enable consumers to make immediate payments, often as part of negotiated settlements. They offer a familiar checkout experience and instant confirmation, but they are not appropriate for every consumer or debt type.

Key Features:

Pros:

Cons:

Credit cards outperform ACH when the goal is immediate account closure through a lump-sum payment. They eliminate settlement delays and reduce uncertainty, but they come with the highest processing costs among common alternatives.

Credit cards should not be positioned as a default option for repayment plans. They are best used selectively when quickly closing the account is worth the added cost.

Real-time payments allow funds to move instantly between bank accounts, eliminating ACH settlement delays. These networks provide certainty once a payment is initiated, but availability varies by bank, and consumer awareness is still limited.

Key Features:

Pros:

Cons:

Real-time payments remove the biggest ACH weakness by delivering instant confirmation and fund availability. There are no batch windows, no waiting periods, and far less ambiguity around payment status.

However, limited bank coverage and lower consumer familiarity restrict widespread use today. For agencies handling time-sensitive or high-value payments, RTP is a strong complement, but not yet a full ACH replacement.

Digital wallets streamline payments by removing the need for manual card entry and using tokenized credentials. They are particularly effective on mobile devices, where friction often leads to abandonment.

Key Features:

Pros:

Cons:

Digital wallets reduce friction far more effectively than ACH, especially on mobile devices. Consumers are more willing to complete payments when they do not have to enter bank details manually.

The limitation is that wallets are typically card-backed and not well-suited for recurring plans. Agencies benefit most from wallets in self-service and mobile-first payment journeys.

Paper checks continue to serve consumers who prefer traditional payment methods. While familiar and trusted by some demographics, they introduce delays and operational complexity.

Key Features:

Pros:

Cons:

Despite these drawbacks, checks remain essential for consumers who do not trust or use digital payments. For agencies, checks are about inclusivity, not efficiency, and should be supported without being prioritized.

No matter how a consumer chooses to pay, Tratta has you covered. The embedded payments feature lets agencies offer ACH, cards, and other methods through a compliant system. Payments stay centralized, visible, and controlled, without juggling multiple tools or vendors. Schedule your free demo today.

Suggested Read: Effortless Payment Collection with Automated Software Solutions

One-time payments prioritize speed and certainty, while repayment plans require predictability and long-term reliability. Choosing the wrong payment method for each scenario can increase failures, disputes, and administrative follow-up.

Table showing how all alternatives compare for different recovery options:

ACH remains the most practical option for structured repayment plans, but alternatives outperform it for one-time payments and settlements. You also need to ensure compliance before selecting a method. This is discussed in the next section.

Suggested Read: Understanding How an Electronic Payment System Works

Different rules, dispute mechanisms, and documentation standards govern payment methods. In debt collection, where clarity of authorization and audit readiness are critical, these differences directly affect regulatory exposure.

The table below compares ACH and its common alternatives across the compliance dimensions agencies care about most.

Managing compliance across multiple payment methods quickly becomes complex when each method follows different authorization, dispute, and documentation rules.

Tratta centralizes these controls by embedding compliance logic directly into payment workflows. This allows agencies to offer ACH and its alternatives while maintaining consistent authorization capture, audit trails, and regulatory oversight across every payment type. Schedule a free demo today.

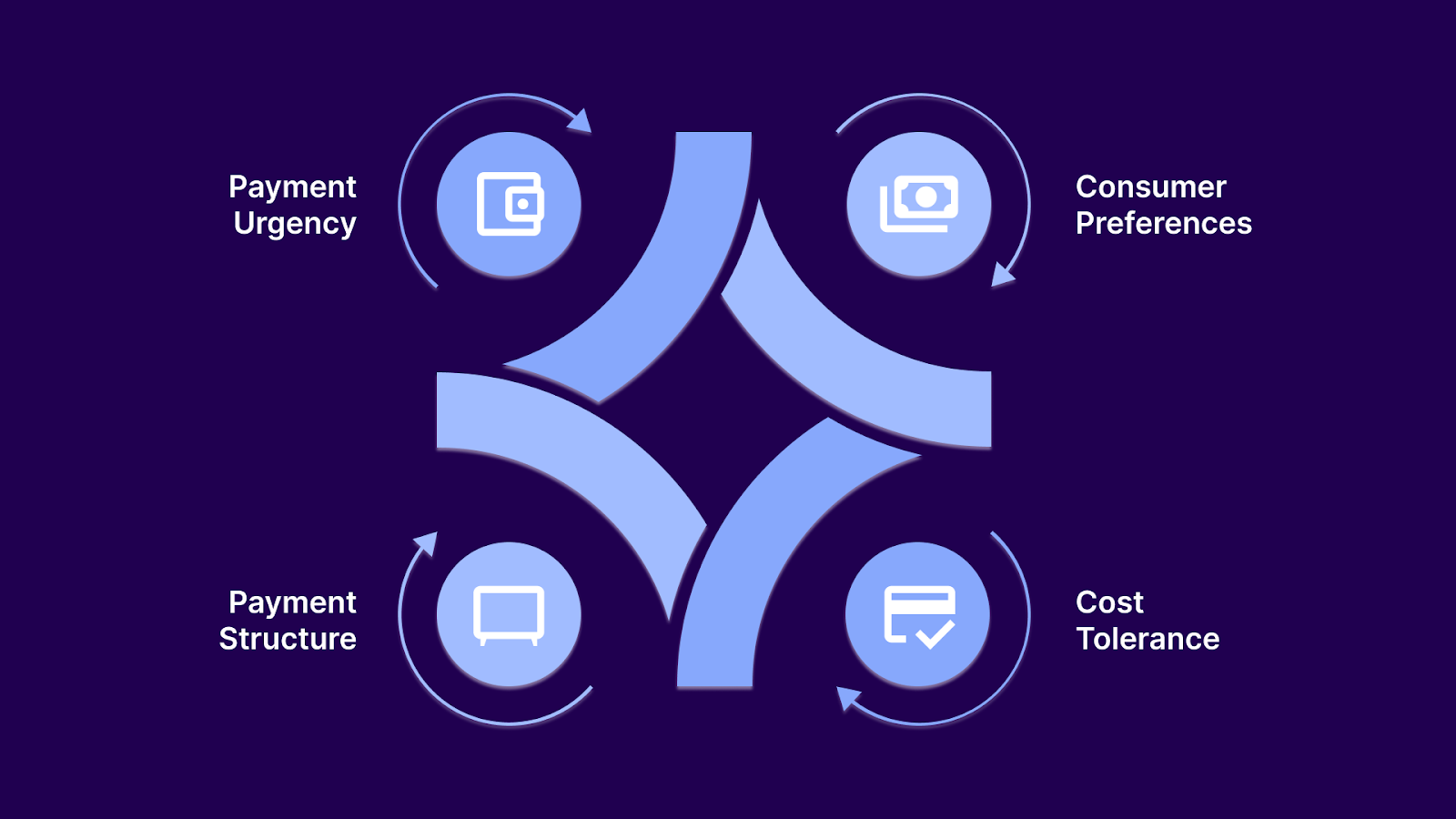

Choosing the right payment method is not about finding a single best option. It is about aligning payment types with consumer intent, timing, and operational reality.

Key factors to consider include:

Relying on a single option forces trade-offs among speed, cost, and completion. This is where orchestration platforms matter.

Suggested Read: How to Use ACH Agreements for Faster Debt Recovery

Tratta is a debt collection and recovery platform built for agencies that need more than a payment rail. It centralizes payments, compliance, and visibility so agencies can support ACH and alternative payment methods without fragmented tools or manual reconciliation.

Multiple payment options, consistent controls, and regulatory oversight are handled within a single system. These are the core features:

The Consumer Self-Service Payment feature gives consumers a secure online place to view balances, choose how to pay, and complete full or partial payments on their own terms. The portal supports multiple payment options, including guest payment flows, to reduce friction and abandoned transactions.

Tratta’s Payments and Merchant Services integrate secure payment acceptance across cards, ACH, and other supported methods in a compliant manner. Payment data is tokenized and handled according to industry standards, ensuring both security and audit readiness.

The Multilingual Payment IVR feature lets consumers pay by phone in their preferred language while updating balances in real time on the platform. It reduces barriers for non-English speakers and meets customers where they are. Real-time updates ensure payments are reflected instantly in reporting and dashboards.

Omnichannel Communications unify outreach across voice, SMS, and email so consumers receive coherent and personalized payment prompts. Tratta tracks every interaction and links messaging directly to payment activity, improving engagement and reducing missed opportunities.

Tratta Campaigns allow agencies to launch automated, rules-based outreach sequences tailored by account attributes or payment behavior. With performance tracking from delivery through payment, agencies can refine messaging and boost ROI on campaigns. Campaign automation saves time while increasing recoveries at scale.

Reporting and Analytics give agencies real-time dashboards and shareable insights to monitor performance across payment methods and campaigns. Teams can spot trends, measure outcomes, and adapt strategies based on data instead of guesswork. This transparency translates to smarter resource allocation and better recovery results.

Tratta’s Customization and Flexibility let agencies tailor workflows, messaging, and interfaces to match their processes and branding. Configurable strategies mean agencies are not forced into rigid templates but can optimize for their unique needs. This adaptability supports operational efficiency while remaining compliant.

With flexible REST APIs and secure integrations, Tratta connects to existing tech stacks, CRMs, and payment systems without disruption. Data flows seamlessly, reducing manual effort and keeping systems in sync in real time. This interoperability amplifies productivity and preserves investment in existing tools.

PCI DSS Level 1 and SOC 2 Type II standards are built into payments and data handling. Regulatory controls like automated compliance rules, audit trails, and secure consent capture minimize legal risk and protect sensitive information.

These features work together to support multiple payment methods without operational fragmentation or compliance gaps.

Payment speed, consumer trust, and method flexibility directly influence completion rates, recovery timelines, and operational costs. Agencies that align payment options to intent, rather than forcing a single default, consistently see better outcomes.

Tratta brings ACH and alternative payment methods together through embedded payments, centralized controls, and built-in compliance. Instead of managing fragmented tools, agencies gain one system that supports choice without sacrificing visibility or governance.

Give consumers more ways to pay without creating more work for your team. Speak with us today to simplify multi-method payments while improving recovery performance.

No. Zelle is not an ACH payment method. It uses bank-to-bank transfers that move funds quickly between enrolled users, but it does not follow standard ACH authorization, settlement, or dispute processes used in debt collection.

Money can be transferred using debit cards, credit cards, real-time payment networks, digital wallets, or paper checks. In collections, these methods are typically used for one-time payments or settlements where ACH delays or authorization risk create friction.

ACH processes payments in batches with settlement delays, while Real-Time Payments move funds instantly with immediate confirmation. RTP reduces uncertainty but has more limited bank coverage compared to ACH.

ACH payments commonly fail due to insufficient funds, closed accounts, revoked authorizations, or incorrect bank details. Each failure creates additional follow-up work and extends the recovery timeline.

Yes, when handled through PCI-compliant systems. Debit and credit card payments can be secure and effective, especially for one-time payments, as long as tokenization, access controls, and audit trails are in place.

No. ACH remains the most practical option for structured repayment plans. High-performing agencies supplement ACH with alternatives to handle settlements, urgent payments, and consumer preference gaps.