Debt collection teams frequently struggle to get debtors to commit to and complete payment plans. Manual outreach, high card fees, and one-off payments drain resources and reduce recovery rates. One of the biggest levers teams can pull is the payment rail they use.

ACH payments enable predictable, recurring bank debits that reduce friction and lower costs compared to card processing. The reach of ACH is enormous and growing. In just the third quarter of 2025, the ACH Network processed 8.8 billion payments valued at more than $23.20 trillion.

This is up 5.2% in volume and nearly 8.2% in value YOY. Integrating with an ACH processing platform has become a strategic necessity that drives efficiency and materially reduces collection costs. This blog explores 7 leading ACH payment processing companies that make debt collection easier.

Quick look:

ACH, or Automated Clearing House, is the U.S. bank-to-bank payment network. It is governed by Nacha, which defines the operating rules, authorization standards, and risk controls for electronic debits and credits.

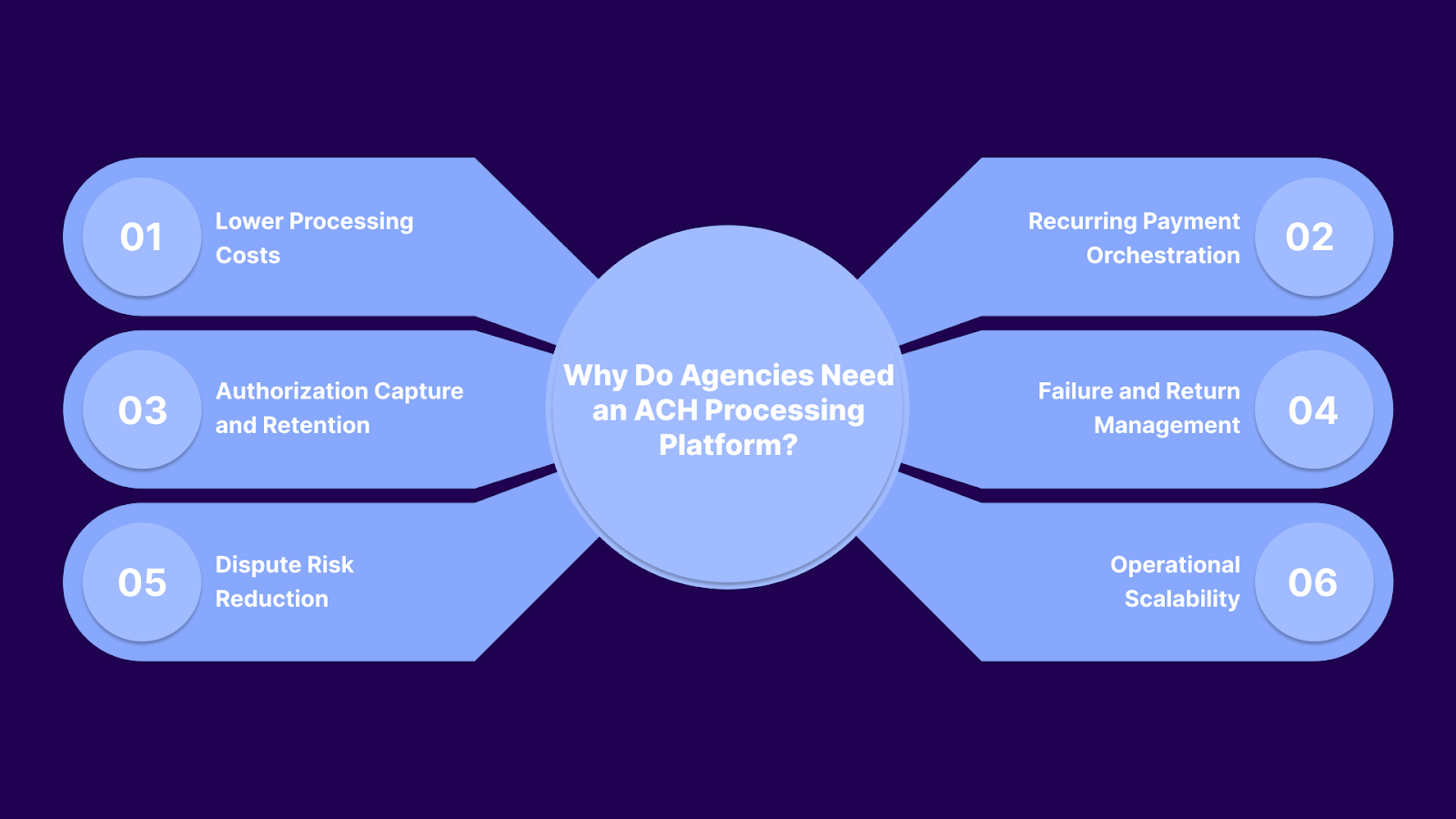

On its own, ACH is only a payment rail. Payment processors are what translate that rail into a usable system for debt collection agencies, handling logic, compliance, and scale.

This is why collection agencies need payment processors:

With payment processors handling the mechanics, agencies can then focus on selecting ACH platforms that align with their collection strategies and compliance needs.

Suggested Read: ACH Credit in Debt Collection: How It Works and Why It Matters

Not all ACH providers are built with debt collection realities in mind. The platforms below are commonly used by agencies because they support recurring payments, authorization tracking, and volume processing.

Table showing a quick comparison of the top ACH payment processing companies:

This is a full breakdown of the best ACH payment processing companies for debt collection agencies:

Payliance is an ACH payment processor focused on high-volume, recurring bank debits, with deep roots in regulated and risk-sensitive industries. It is commonly used to support installment plans, settlements, and scheduled ACH pulls where reliability and authorization control matter more than consumer-facing polish.

Key Features

Pros

Cons

Best Use Case

Best used when your collection operation relies heavily on ACH installment plans and needs a processor experienced with volume, returns, and regulatory oversight. It is less effective if you require consumer self-service portals or flexible, on-the-fly payment plan management.

REPAY is a payment processing platform with a strong focus on ACH transactions for regulated, high-volume use cases. In debt collection, it is commonly used to support installment plans, recurring debits, and settlement payments where authorization control and return handling are critical.

Key Features

Pros

Cons

Best Use Case

Best used when your collection operation relies on ACH as the primary payment method for installment plans and settlements. It is less effective if you need built-in consumer self-service tools or flexible, real-time plan adjustments.

Tratta centralizes ACH payments from providers like REPAY into a single debt collection workflow. It connects payment execution to consumer self-service, automated payment plans, and recovery campaigns. Schedule a free demo today.

ACHNow is an ACH routing and processing layer designed by Sila to help businesses move ACH transactions faster. It uses modern payment rails such as RTP and FedNow alongside traditional ACH. ACHNow serves as a backend orchestration layer that intelligently routes ACH transactions to the most efficient settlement rail.

Key Features

Pros

Cons

Best Use Case

Best for operations that want to accelerate ACH settlement and improve reliability across multiple payment rails without building their own orchestration logic. It is less effective as a standalone payment solution unless paired with systems that handle consumer engagement and recovery workflows.

Authorize.Net is a legacy payment gateway that lets merchants accept credit card and ACH/eCheck payments through a single gateway. In debt collection environments, agencies can use their eCheck capability to electronically withdraw funds from bank accounts, often as part of recurring billing or payment plans.

Key Features

Pros

Cons

Best Use Case

Best for organizations that want both card and ACH/eCheck acceptance under a familiar gateway and already use Authorize.Net for card processing. It is less effective if you need advanced ACH retry logic or deep collections workflows tied directly to payment events.

PaymentVision is a payment processing platform that supports ACH and card payments across one-time and recurring transactions. It is commonly used in repayment and servicing contexts where ACH payments need to be authorized, scheduled, and reconciled at the account level.

Key Features

Pros

Cons

Best Use Case

Best used when ACH payments must be reliably scheduled, authorized, and reconciled across large account volumes, with a strong emphasis on payment posting accuracy and operational control.

Worldpay (part of FIS Global) is a large-scale payment processor offering ACH/eCheck capabilities alongside card and alternative payment methods. Its ACH functionality is typically used as part of a broader payment stack supporting high transaction volumes and standardized payment flows.

Key Features

Pros

Cons

Best Use Case

Best used when ACH payments need to run at scale within a broader payment infrastructure that prioritizes stability, throughput, and standardized processing over customization.

TSYS, now operating under Global Payments, is a large-scale payment processing provider that offers ACH and eCheck capabilities as part of its broader payments infrastructure. Its ACH functionality is typically used to support standardized, high-volume bank debit processing within established payment environments.

Key Features

Pros

Cons

Best Use Case

Works well for collection agencies that process large ACH volumes and prioritize stability over flexibility. It fits operations that rely on standardized payment flows rather than frequent plan changes.

With the ACH platforms laid out, the real question is not which provider offers the lowest fee or cleanest integration. What matters more is whether ACH, as a payment method, actually improves recovery outcomes for collection agencies. This is discussed in the next section.

Suggested Read: Preventing ACH Fraud in Debt Recovery Operations

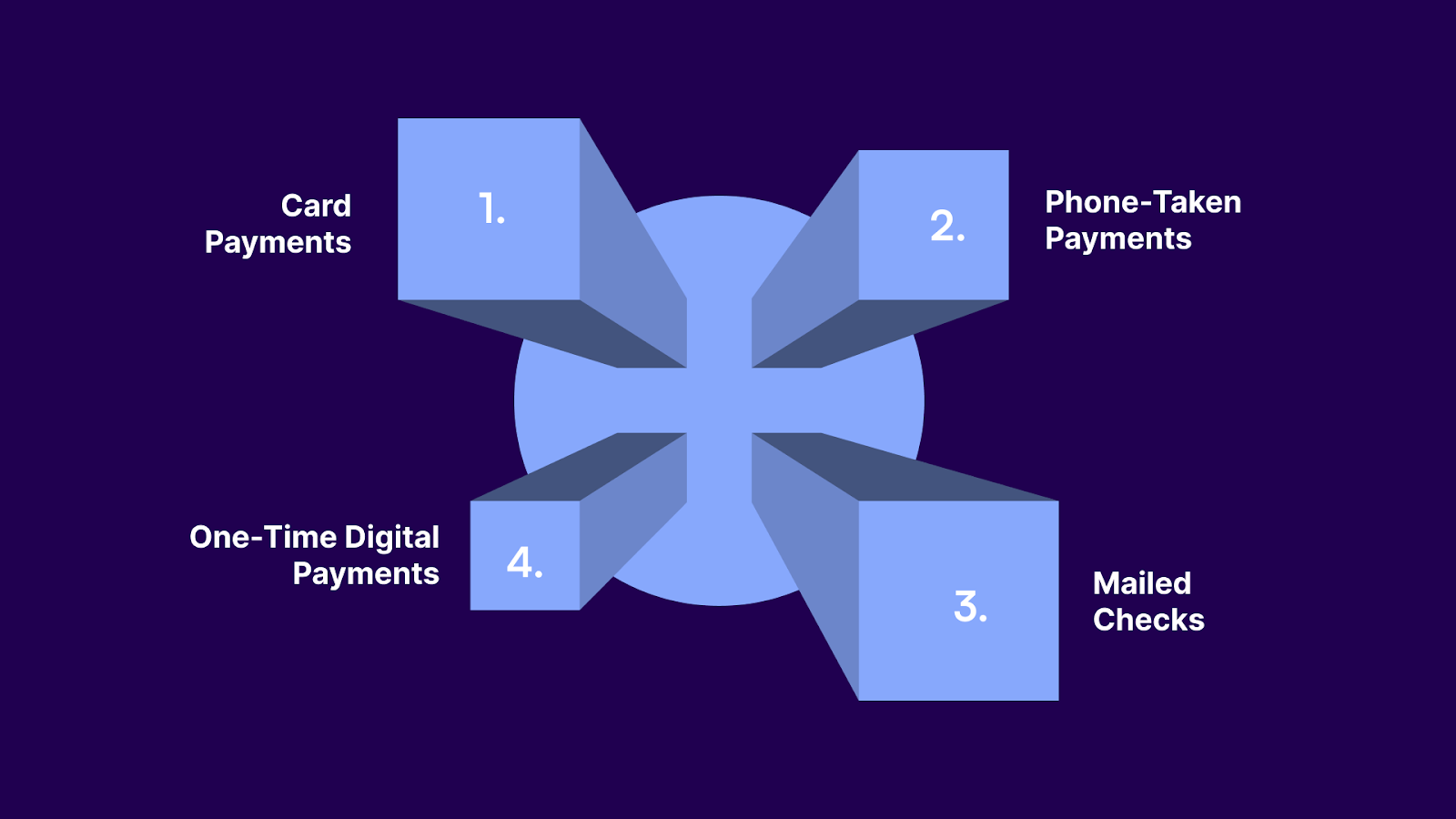

Debt collection involves collecting recurring payments until an account is resolved. Many payment methods can close individual balances, but only a few support sustained recovery across portfolios. ACH stands out because it is built for follow-through, not one-off success.

This is how ACH compares to other collection options:

Outcomes depend heavily on which provider you choose and how well it fits your collection model. Before committing to a processor, agencies need to evaluate ACH options through a recovery lens, not just a pricing or payments lens.

Instead of starting with fees, start with fit. The right ACH partner should support how your agency actually recovers debt, not force you into workarounds.

These are a few questions to ask:

Choosing the right ACH processor solves only part of the problem. Payments still need to connect to account status, consumer actions, and recovery strategy to drive consistent outcomes.

That is where technology becomes the differentiator. It turns ACH transactions into coordinated progress toward resolution rather than isolated payment events.

Suggested Read: How to Use ACH Agreements for Faster Debt Recovery

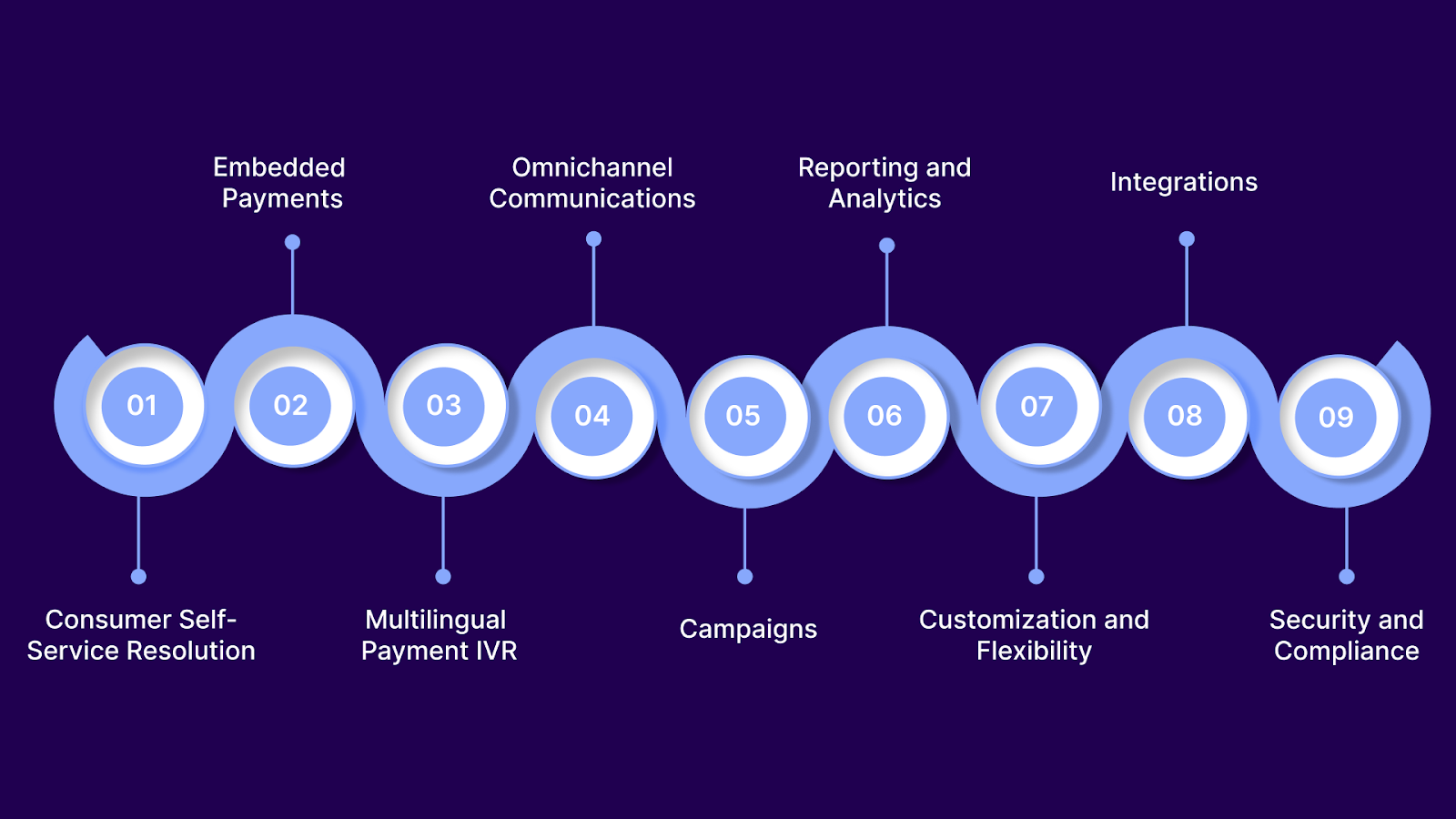

Tratta is a debt collection operations platform that centralizes all collections-related workflows into a single system. It connects ACH and other payment methods directly to account status, payment plans, and outreach strategies. The goal is to turn payments and interactions into consistent, trackable recovery outcomes.

Features that power automated debt collections:

Tratta allows consumers to view balances, make payments, upload documents, and submit disputes without agent involvement. This reduces inbound volume while improving engagement and plan completion. Self-service gives consumers control while keeping agencies focused on higher-value work.

Payments are built directly into the recovery workflow, including ACH and card processing. Payment status updates flow in real time, keeping balances, plans, and account states accurate. This removes friction between payment execution and recovery tracking.

The IVR enables consumers to make payments and interact by phone in multiple languages. Rule-based logic guides callers through secure payment flows without agent assistance. This expands accessibility while reducing call handling costs.

Tratta supports coordinated outreach across phone, SMS, and email from a single platform. Communications can be triggered by account events, missed payments, or plan milestones. This ensures consistent messaging regardless of how consumers engage.

Campaigns let you automate outreach using segmentation, schedules, and behavioral triggers. You can tailor settlement offers and follow-ups by portfolio, account state, or consumer response. This makes outreach more targeted and measurable.

Real-time dashboards show payment performance, plan success rates, and campaign results. You can analyze trends, identify drop-offs, and adjust strategy quickly. Reporting ties recovery activity directly to outcomes.

Workflows, business rules, notices, and user permissions can be configured without custom development. Agencies can align the platform with their existing processes instead of changing how they work. This flexibility supports a range of portfolio types and recovery models.

APIs and webhooks connect Tratta with systems of record, payment providers, and internal tools. Payment events, plan updates, and consumer actions stay synchronized across systems. Integrations reduce manual work and data gaps.

Tratta applies encryption, role-based access, audit trails, and compliance controls across the platform. Regulatory requirements are enforced within workflows, not handled after the fact. This reduces risk and supports audit readiness.

Tratta is built for collection teams that want outcomes, not disconnected activity. By connecting execution to insight and control, it helps agencies recover more with less operational strain.

Choosing the right ACH payment processing platform is an important decision for any debt collection agency. The right provider can lower costs, support payment plans, and reduce friction for consumers. However, ACH alone does not manage recovery, handle engagement, or connect payments to account progress.

Tratta fills that gap by integrating ACH payments into a complete recovery workflow. It centralizes payments, consumer interactions, campaigns, and reporting, so every payment moves an account closer to resolution.

ACH can fuel meaningful recovery when paired with the right platform. Tratta gives you the compliance, visibility, and control to achieve it. Speak to our team today.

1. Who processes ACH payments for debt collection agencies?

ACH payments are processed by ACH payment processors and banks that operate on the U.S. ACH network, which is governed by Nacha. Collection agencies typically work with processors that support recurring debits, authorization storage, returns handling, and compliance reporting rather than consumer P2P tools.

2. Who accepts ACH payments online in debt collection?

Debt collection agencies, creditors, healthcare providers, utilities, and loan servicers commonly accept ACH payments online. ACH is widely used for payment plans and settlements because it supports scheduled debits, lower fees, and predictable recovery across large account volumes.

3. Is ACH better than Zelle for debt collection?

Yes. ACH is designed for recurring, authorized payments with audit trails and return codes, which are critical for compliance. Zelle is a peer-to-peer transfer tool and does not support payment plans, authorization records, or collections workflows.

4. How do you set up ACH payments for consumer payment plans?

Agencies typically use an ACH processor to capture bank authorization and schedule recurring debits. For effective recovery, ACH payments are then connected to payment plans, account status, and follow-up logic through collections technology rather than being managed as standalone transactions.

5. Does ACH processing improve recovery rates in debt collection?

ACH processing improves recovery when it is used for automated payment plans rather than one-time payments. Scheduled debits reduce missed payments, lower agent involvement, and increase plan completion rates, especially when combined with self-service and automated outreach.